ADEIA INC.

The Toll Booth and the Transition: IP Monetisation at Scale, Pay-TV Decay, and Why the CEO Succession Is the Decisive Near-Term Variable

1. Corporate Profile & The IP Licensing Toll Booth Thesis

Adeia owns patents that other companies must use to build and sell products in media and semiconductors. It collects royalties without manufacturing anything. That structural position defines every dimension of the business model, the moat, and the risk profile.

What the business actually is

Adeia is a research, development, and intellectual property licensing company. headquartered in San Jose, California. The company became an independent public entity in October 2022 following its separation from Xperi Holding Corporation, a prior consolidation vehicle that had accumulated media and entertainment technology assets. The rationale for the separation was to isolate the IP licensing franchise from Xperi’s product and consumer-facing operations, on the thesis that the two businesses had structurally different investor bases, capital allocation requirements, and valuation frameworks.

Pure-play IP licensing businesses generate high cash conversion ratios with limited capital expenditure and no inventory or supply chain risk. Product businesses require sustained investment in development cycles, manufacturing relationships, and go-to-market infrastructure. Housing both within the same public entity creates analytical noise and capital allocation conflicts. The separation resolved that tension by creating two distinct public entities with distinct strategies.

The resulting company operates as a single segment, IP Licensing, with no manufacturing, no product revenue, and no cost of goods sold in the traditional sense. Its primary operating costs are research and development expenditure (to expand and sustain the portfolio’s relevance as underlying technologies evolve), selling, general and administrative expenses (including the legal, licensing, and relationship management infrastructure required to negotiate and administer hundreds of agreements globally), amortisation of intangibles from historical M&A activity, and litigation expense incurred in enforcing the portfolio against unlicensed users.

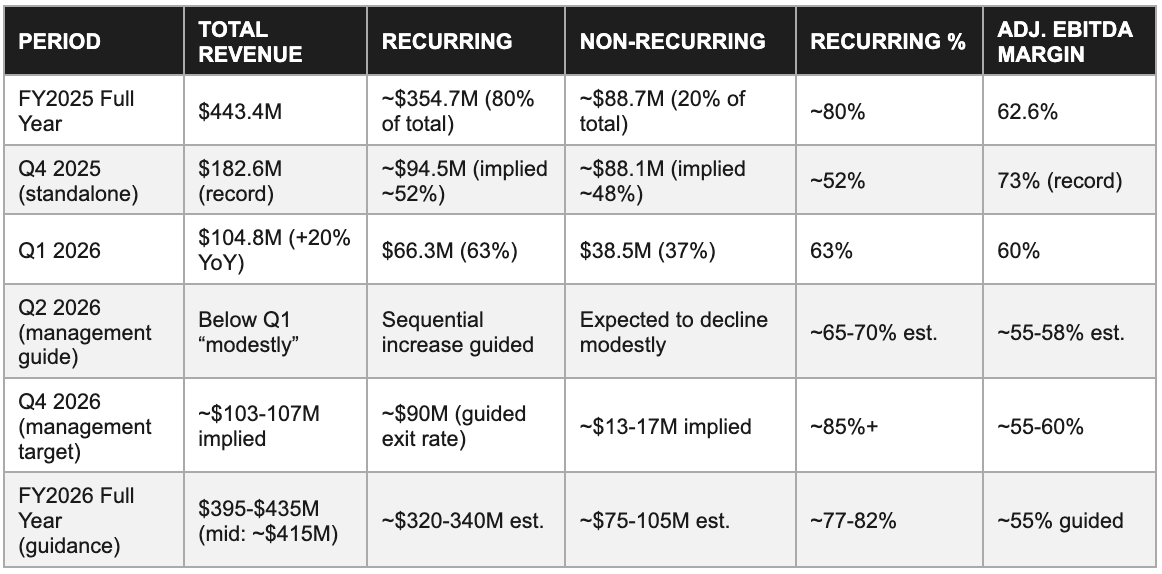

None of these cost categories is analogous to the variable cost structures of manufacturing or services businesses. With the partial exception of litigation expense, they are largely fixed in the near term relative to revenue, which is the structural origin of the business’s high adjusted EBITDA margins, 62.6% for FY2025, 60% in Q1 2026, and guided at approximately 55% for the full year FY2026 with pressure from rising litigation costs.

The toll booth framing and its commercial precision

The toll booth metaphor is precise for a specific and commercially important reason.

Adeia’s patents cover processes and technologies that are embedded in products consumers and enterprises use regardless of Adeia’s involvement in their production. A smart television that incorporates a content discovery interface, a streaming application that generates personalised content recommendations, a NAND flash memory chip manufactured using hybrid bonding stacking techniques, a social media feed that surfaces content based on engagement history, these products use Adeia’s IP because the technology is foundational to their functionality, not because the manufacturers chose Adeia as a preferred supplier over a competitive alternative. The relevant technology is embedded in the underlying architecture of the product category itself.

The commercial consequence of this position is asymmetric relative to product or services businesses. A cable operator cannot deliver a modern electronic programme guide to its subscribers without employing content navigation and guide technologies covered by Adeia’s portfolio. A manufacturer of high-bandwidth memory for AI accelerators cannot achieve the interconnect density required by the application without employing chip stacking techniques that Adeia’s DBI portfolio addresses. A streaming platform that delivers personalised content recommendations at scale, without licensing Adeia’s portfolio, faces the choice of litigation risk or a design-around effort that would require re-engineering core recommendation systems at material cost and with uncertain technical outcomes.

Licensing Adeia’s portfolio is typically the economically rational choice for large technology companies that have assessed their exposure honestly and concluded that the licensing fee is less costly than the alternatives. The structural asymmetry explains why the historical customer renewal rate has exceeded 90%: once a company has assessed the portfolio, agreed terms, and integrated the licensing relationship into its compliance infrastructure, the decision calculus at renewal strongly favours continuation over disruption.

Scale and reach of the licensing programme

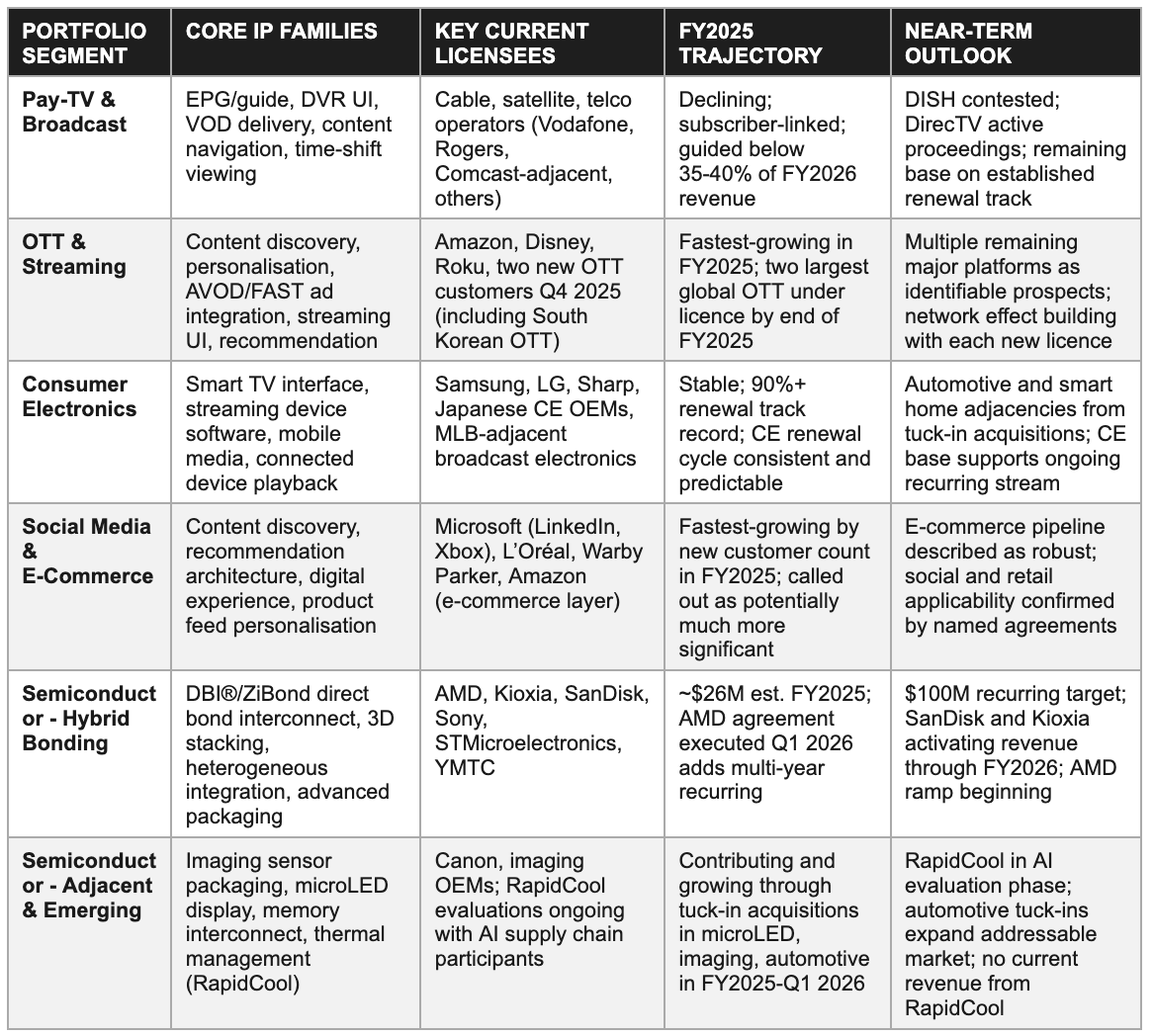

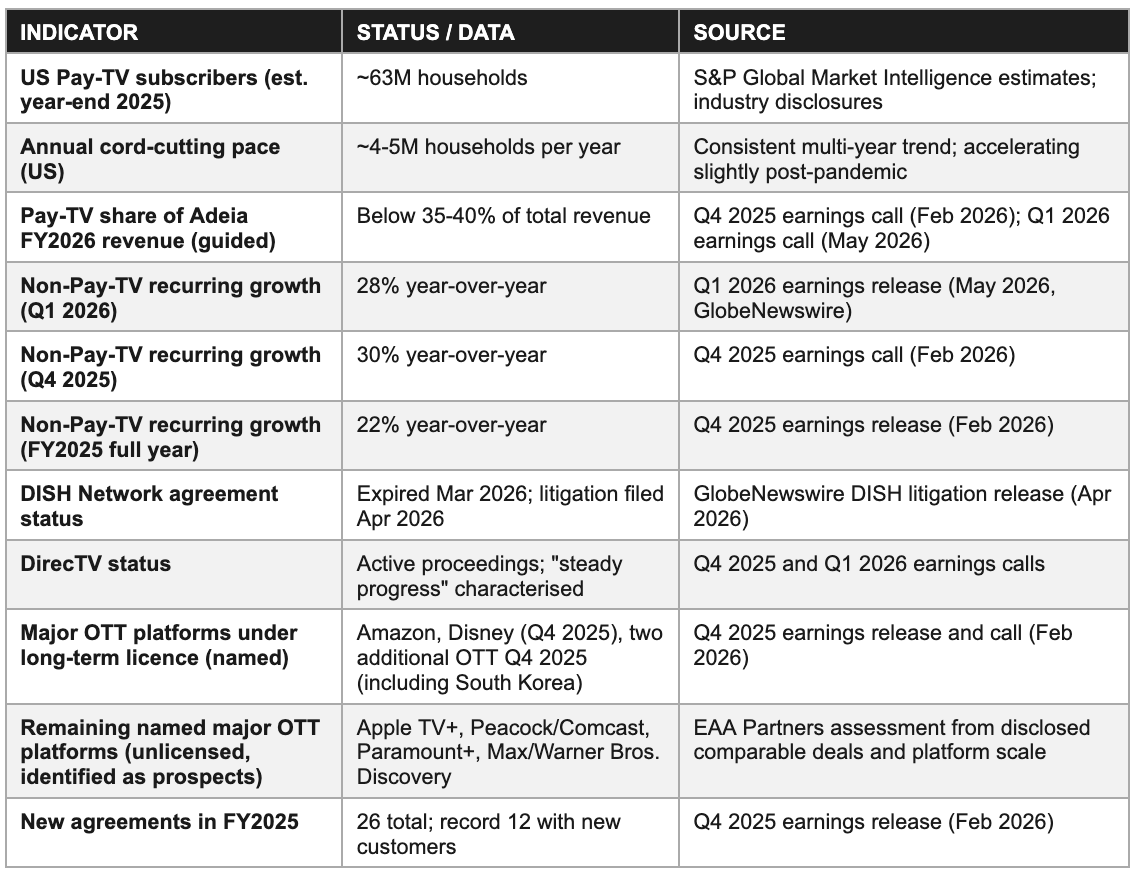

As of Q1 2026, Adeia’s portfolio exceeds 13,750 patent assets worldwide, the result of three consecutive years of double-digit portfolio growth through a combination of internal R&D investment running at approximately $67.5 million in FY2025, and five tuck-in acquisitions in Q1 2026 alone following six in FY2025. The company has executed over 145 licence agreements with customers since its October 2022 separation, spanning Pay-TV operators, over-the-top streaming services, consumer electronics manufacturers, e-commerce platforms, social media companies, and semiconductor firms across North America, Europe, Japan, South Korea, Taiwan, and China.

Management articulated a long-term annual revenue target of $500 million on the Q1 2026 earnings call, approximately 13% above the FY2025 record of $443.4 million. The target is achievable through three identifiable and non-speculative mechanisms: the conversion of remaining major OTT platforms and digital experience companies that employ covered technologies to licensed status; the growth of semiconductor recurring revenue from the current estimated $26 million toward the separately articulated $100 million semiconductor-specific long-term target; and the continued organic compounding of the existing customer base through renewals that capture improved economic terms reflecting an expanded evidence base and higher-value portfolio.

The $500 million target requires execution of the existing strategy across identifiable prospects in already-penetrated verticals, not a paradigm shift or entry into unproven new markets.

2. The Patent Portfolio: Two Vertical Pillars, One Compounding Asset

A patent portfolio is the productive asset of a pure-play licensor, it compounds through R&D and tuck-in acquisitions rather than depreciating through use. Adeia's two-vertical structure across media and semiconductor creates distinct franchises with different growth trajectories, customer bases, and competitive dynamics.

Portfolio scale, growth, and origination strategy

Since the October 2022 separation, the portfolio has grown by a meaningful multiple through the combination of internal origination and tuck-in acquisitions. Internal R&D, running at approximately $67.5 million in FY2025, serves dual purposes simultaneously: sustaining the technical relevance of existing patent families as the underlying technologies evolve, and originating new filings in adjacent areas where demand is emerging ahead of commercial licensing activity.

The company’s stated preference is an approximately 85-15 split between internal R&D and external acquisition, prioritising internally originated IP as the primary driver of long-term portfolio value because internally developed patents carry the full economic benefit without the acquisition premium paid to a seller.

Tuck-in acquisitions serve the complementary function of adding coverage in areas where the gap between the existing portfolio and a near-term commercialisation opportunity is too large to bridge through organic origination within the relevant timeframe. The five tuck-in acquisitions completed in Q1 2026 alone, following six in FY2025, expanded the portfolio into microLED display technology, advanced automotive connectivity, and additional imaging sensor IP, areas where the growth trajectory of consumer electronics creates prospective licensing demand that the existing portfolio would not have fully captured.

Management described the tuck-in pipeline as active and characterised individual acquisitions as targeted rather than transformative in capital cost: total capital expenditure in FY2025 was approximately $2 million, with tuck-in acquisition costs modest relative to the portfolio value they add. The operational efficiency of the tuck-in strategy, deploying modest capital to fill specific licensing gaps rather than pursuing large platform acquisitions that require balance sheet leverage, is a structural advantage of the pure-play licensing model over integrated technology companies whose IP acquisitions must also serve product development objectives.

The media portfolio: From set-top box to the full digital experience stack

The media IP portfolio is the legacy franchise. It traces its commercial lineage to Rovi Corporation’s content discovery and guide technology business, TiVo’s navigation, search, and digital video recording IP, and DTS’s audio technology licensing programme, all combined through the series of acquisitions that preceded the Xperi holding structure and then separated into Adeia.

The portfolio covers the full lifecycle of digital media consumption: how content is indexed and made discoverable across a large and heterogeneous catalogue; how personalised recommendations are generated and surfaced to individual users based on engagement history and contextual signals; how content guides and navigation systems function across device categories including televisions, set-top boxes, streaming sticks, mobile devices, and browser-based players; how digital audio is encoded, transmitted, and reproduced across multi-channel configurations; and how content metadata is structured to enable guide and navigation functionality at scale.

Each of these functions is addressed by multiple overlapping patent families, creating portfolio depth that makes design-around efforts more technically challenging and expensive than a shallow or narrow portfolio would produce.

The commercial significance of this portfolio has expanded as the relevant technology platforms have evolved. The cable industry’s electronic programme guide, which was the original commercial application of Rovi’s guide IP, required personalised content navigation for a catalogue of hundreds of channels. Netflix, at its 2025 scale, requires personalised content navigation for a catalogue of tens of thousands of titles across multiple content categories, languages, and format types.

The underlying intellectual problem, how to present a large content catalogue in a way that efficiently connects an individual user with the content most likely to satisfy their expressed or inferred intent, is the same problem at a different scale and in a different delivery environment.

Adeia’s portfolio, which was developed against the cable context, retains applicability in the streaming context because the core invention claims cover the discovery and navigation function at the level of the user experience, not the specific technical implementation of any particular delivery mechanism. This level of claim abstraction is what allows a portfolio built for linear television to remain commercially relevant for on-demand streaming, AI-driven recommendation, and e-commerce product discovery simultaneously.

The e-commerce and social media applicability is the newest and most commercially promising expansion of the media portfolio’s licensing surface. Content discovery and recommendation are structurally identical problems whether the content being discovered is a television programme, a social media post, or a consumer product. An e-commerce platform that surfaces product recommendations based on a user’s browsing and purchase history is solving the same recommendation problem as a streaming service surfacing viewing recommendations based on watch history.

Adeia’s agreements with L’Oréal and Warby Parker confirm the portfolio’s applicability to consumer retail e-commerce; the Microsoft agreement, which covers LinkedIn’s content feed recommendation and Xbox’s game library navigation, confirms the applicability to social and gaming platforms. Management characterised e-commerce as a vertical that “could be much more significant in the future,” and the tuck-in acquisition activity in Q1 2026 targeting automotive connectivity suggests that automotive infotainment, the next large content navigation platform after mobile and streaming, is the subsequent expansion surface being prepared.

Portfolio segment overview

3. Hybrid Bonding: The Semiconductor Bet and Its AI Tailwind

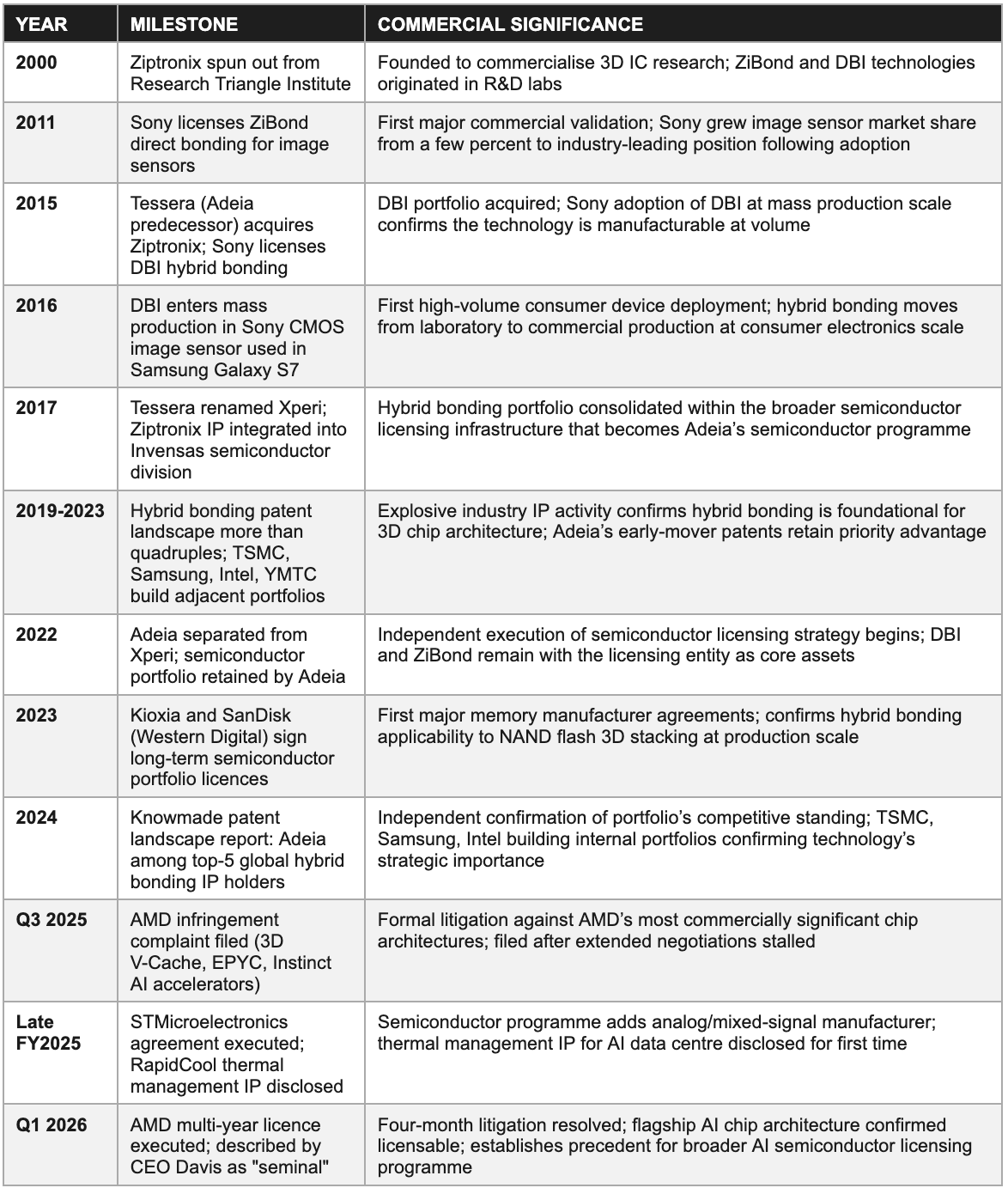

Adeia’s DBI® hybrid bonding technology was originated in 2005, entered mass production through Sony’s image sensors in 2016, and has since become foundational to AI chip architecture. The rise of high-bandwidth memory for AI accelerators has made a two-decade-old niche packaging investment into a commercially material licensing asset.

The technology: Why it is important for AI

Hybrid bonding enables the vertical stacking of multiple chips with direct metal-to-metal and dielectric-to-dielectric connections, replacing the solder bumps used in conventional flip-chip packaging. The technical advantages are substantial and directly relevant to AI computing requirements. Interconnect pitch, the distance between individual connections, can be reduced below 10 microns and in advanced implementations below 1 micron, compared to tens of microns in conventional bump-based approaches.

This pitch reduction enables interconnect density that is orders of magnitude higher than prior-generation packaging, translating directly into the memory bandwidth, power efficiency, and signal latency improvements that AI chip performance fundamentally requires.

High-bandwidth memory, the stacked DRAM architecture essential for AI accelerators and large language model inference workloads, relies on vertical die stacking at precisely the interconnect density that hybrid bonding enables. TSMC’s SoIC platform, Samsung’s X-Cube architecture, SK Hynix’s HBM3 and HBM3E products, and AMD’s 3D V-Cache technology all employ direct bonding techniques with significant technical and patent overlap with Adeia’s DBI and ZiBond portfolio.

As AI workloads continue to scale in model size and inference throughput requirements, the memory bandwidth requirements of the associated hardware scale proportionally. The architecture of choice for addressing that bandwidth scaling is stacked memory using direct bonding techniques that Adeia’s patents address. The AI compute buildout, driven by hyperscaler capital expenditure running at hundreds of billions of dollars annually across the major cloud platforms, is therefore a direct demand driver for the technologies that Adeia’s semiconductor licensing programme covers.

The direct metal-to-metal contact in hybrid bonding also facilitates more efficient heat dissipation than solder-based interconnects, a commercially meaningful advantage as AI chip power consumption increases. NVIDIA’s Blackwell architecture, AMD’s MI300X and MI325X, and custom AI silicon from hyperscalers including Google (TPU), Amazon (Trainium/Inferentia), and Microsoft (Maia) all generate thermal loads that challenge conventional air and liquid cooling approaches. The performance advantages of hybrid bonding in both interconnect density and thermal efficiency position it as a necessary rather than optional technology for the next generation of high-performance compute.

The patent position: Pioneer advantage and its scope

Adeia’s DBI portfolio originated with Ziptronix’s R&D activity beginning in 2000 and the formal introduction of DBI technology in 2005, a full decade before the semiconductor industry’s broad adoption of hybrid bonding at scale. This early-mover position creates priority claims that post-2015 filings by TSMC, Samsung, Intel, and others cannot easily circumvent. A patent filed in 2005 on a direct bond interconnect process step has a priority date that precedes the industry’s subsequent patenting activity by ten or more years; subsequent filings on the same or closely related processes must distinguish themselves from the Ziptronix prior art or accept that their claims are bounded by Adeia’s earlier filings.

The Knowmade 2024 patent landscape analysis, a specialist IP intelligence report, identified TSMC, Adeia, YMTC, Intel, and Samsung as the leading hybrid bonding patent holders, with Adeia explicitly described as having adopted an aggressive strategy to assert its patents and licence its portfolio to semiconductor companies including Sony, YMTC, Micron, and Kioxia. The pioneer advantage is real and has been commercially validated through successful assertion.

The portfolio’s assertability has been empirically validated across multiple enforcement cycles. Adeia has successfully licensed its semiconductor portfolio to Sony, YMTC, Micron, Kioxia, SanDisk, STMicroelectronics, Canon, and AMD. Each of these agreements represents a commercial acknowledgment by a major semiconductor company that Adeia’s patent claims are valid, applicable, and worth licensing rather than challenging. This track record is not merely a historical artefact; it is an active commercial precedent that informs subsequent negotiations.

A company evaluating whether to contest or licence Adeia’s semiconductor portfolio can observe that companies including AMD, which has its own substantial patent portfolio and the resources to litigate aggressively, concluded that licensing was the appropriate resolution after four months of active litigation. That precedent reduces the negotiating leverage of future holdouts who might otherwise calculate that Adeia would prefer settlement over sustained litigation.

DBI hybrid bonding commercial timeline

4. Revenue Architecture: Recurring vs. Non-Recurring, and Litigation as a Monetisation Tool

Headline revenue is a poor guide to underlying momentum at Adeia. The stream is bimodal: a recurring royalty base that reflects the genuine run-rate health of the programme, and a non-recurring layer from newly executed agreements that creates large quarterly swings. Litigation is the enforcement mechanism that converts unlicensed use into contracted revenue, its costs are investments in future income, not expenses to minimise.

The structure of revenue

Recurring revenue comprises royalty streams from active multi-year licence agreements. In the Pay-TV segment, these are typically structured as a fee per subscriber per month, meaning that as Pay-TV subscriber bases contract industry-wide, recurring revenue from those agreements compresses mechanically, even without any change in the per-subscriber rate or the agreement terms.

This subscriber-linkage is the mechanism through which structural industry decline flows directly into Adeia’s quarterly financial results, independently of any change in the portfolio’s commercial strength or the licensing programme’s execution quality. In the media OTT, semiconductor, consumer electronics, and e-commerce segments, agreements are more commonly structured as fixed-fee recurring payments over the agreement term, providing greater revenue visibility and immunity from underlying market volume fluctuations.

Non-recurring revenue arises primarily from the up-front component of newly signed agreements and from recognition of amounts attributable to prior-period usage. When Adeia concludes a licensing negotiation that covers a period during which the customer was operating without a licence, as is typically the case when litigation precipitates a resolution, a portion of the total economic value represents past-period use and is recognised immediately. These up-front recognition events can be very large relative to the recurring base.

The Disney agreement signed in Q4 2025 transformed that quarter from a typical recurring-revenue period into a record $182.6 million result; management characterised Q4 as approximately 50/50 recurring and non-recurring, implying the Disney non-recurring component was approximately $88 million in isolation. For full-year FY2025, the annual mix was 80% recurring and 20% non-recurring per management’s Q4 2025 earnings call disclosure, a ratio that understates the quarterly volatility because it averages three near-normal recurring quarters with the Disney-dominated fourth quarter.

The Q1 2026 recurring revenue of $66.3 million against Q4 2025’s implied $94.5 million reflects three distinct and separable mechanical factors. The DISH Network agreement expiry at end of March 2026 removed a long-standing Pay-TV customer’s recurring stream from the base. Subscriber-linked compression in the remaining Pay-TV base continued at the structural industry pace of approximately 4 to 5 million US Pay-TV household losses per year. And the SanDisk and Kioxia agreements, both executed in late FY2025, contributed zero revenue in Q1 2026 due to the specific timing and recognition mechanics of those agreements. Management confirmed these customers are expected to provide meaningful contributions across Q2–Q4 2026.

These three factors are mechanical and their resolution is observable: DISH via litigation settlement, SanDisk and Kioxia via agreement activation in subsequent quarters.

Revenue mix by period

Litigation as an integral revenue mechanism

IP licensing companies enforce their patents through negotiated licensing, where the prospective licensee acknowledges the IP’s validity and agrees to terms, or through patent infringement litigation, where the IP owner files a complaint to compel negotiations or obtain a judicial determination. Adeia employs both approaches, with a stated preference for negotiated outcomes but a demonstrated and consistent willingness to litigate when negotiations stall.

The imperative is to recognise that litigation at Adeia is not a defensive activity, an unusual circumstance, or a sign of commercial weakness. It is an integral part of the revenue generation mechanism: litigation is the tool that converts an unlicensed user into a licensed one, recovers past-period royalties for the uncontracted period, and sends a market signal that the enforcement programme is credible and active.

The litigation pipeline produces identifiable future revenue catalysts with defined resolution timelines.

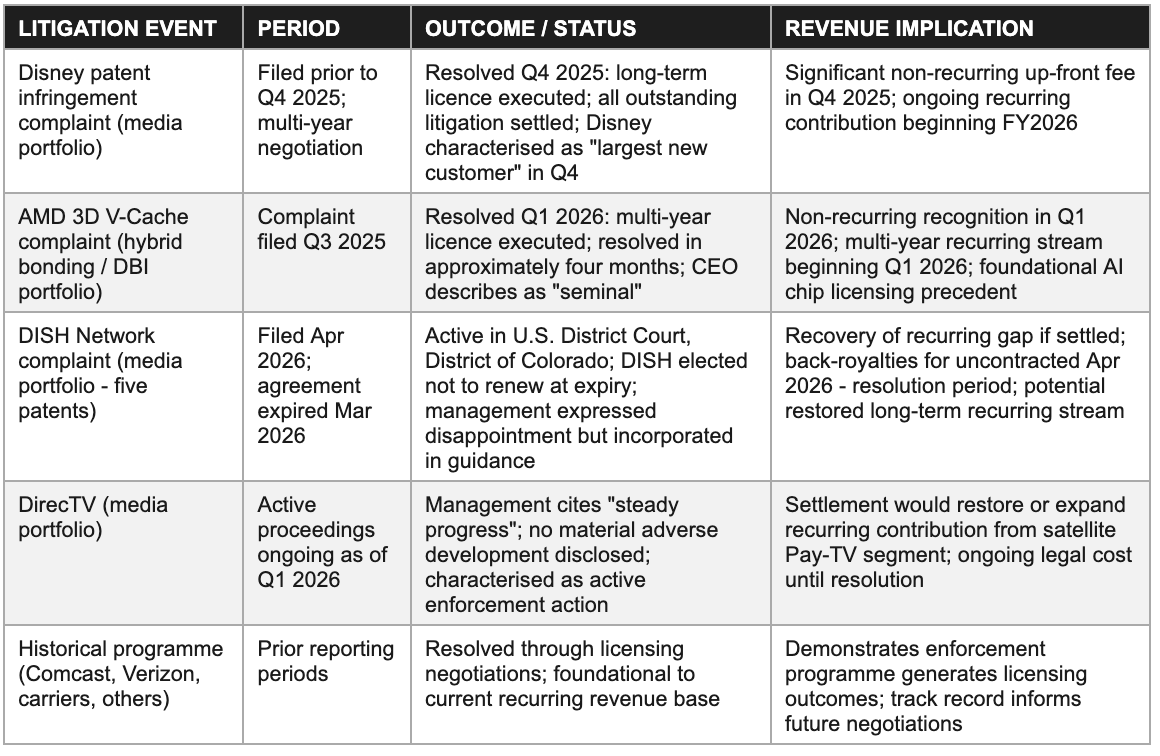

When Adeia files a complaint against a major technology company, that filing initiates a process that historically resolves within 12 to 36 months through a negotiated licence agreement. The Disney resolution, which covered all outstanding litigation and produced a long-term licence, and the AMD resolution, which occurred in approximately four months of active proceedings, both demonstrate that litigation is not a prolonged drain on resources without commercial outcome.

The speed of the AMD resolution is particularly noteworthy: four months from complaint to executed multi-year licence is substantially faster than the typical 18 to 36 month patent litigation timeline, suggesting that the strength of the portfolio against 3D V-Cache architectures was sufficiently clear that AMD concluded early settlement was preferable to prolonged litigation.

Litigation programme overview

Investors who model only the cost side of the litigation programme, the approximately $25–35 million of annual legal expense in FY2025–FY2026, without modelling the probability-weighted revenue recovery from DISH and DirecTV are systematically undervaluing the programme. A DISH settlement that includes back-royalties for the period from April 2026 to resolution date, plus a renewed multi-year agreement at rates reflecting the current subscriber base, represents a combined non-recurring and recurring revenue impact that could be material relative to the annual litigation cost.

The same logic applies to DirecTV: resolution would remove a recurring revenue uncertainty, reduce ongoing litigation costs, and confirm the enforcement programme’s continued effectiveness across the full Pay-TV operator universe.

5. The Pay-TV Decay Problem: Structural Headwind or Manageable Glide Path?

Pay-TV subscriber declines are structural. The investment question is whether non-Pay-TV recurring growth through OTT, semiconductors, and e-commerce is running ahead of or behind the legacy erosion in absolute dollar terms, and whether DISH and DirecTV represent isolated financial distress events or the start of a broader defection pattern.

The foundation and its erosion

Pay-TV was the founding commercial application for the media licensing portfolio. The content guide and navigation IP developed from Rovi and TiVo’s technology base was originally licensed to cable, satellite, and telco TV operators who needed those technologies to build user interfaces for linear television delivery. As the installed base of Pay-TV subscribers expanded through the 2000s and early 2010s, this licensing programme generated substantial and growing recurring revenue from a stable and expanding licensee base.

The structural reversal of subscriber growth, which began as a measurable trend around 2013 and accelerated meaningfully from approximately 2018 onwards, created a mechanical revenue headwind that has been embedded in Adeia’s financial trajectory ever since and predates the separation from Xperi.

The US Pay-TV subscriber universe has declined from a peak of approximately 100 million households in the mid-2010s to an estimated 63 million as of year-end 2025, with industry projections suggesting continued annual attrition of approximately 4 to 5 million households through the end of the decade. The revenue impact on Adeia operates through two simultaneous mechanisms: the per-subscriber royalty paid by each operator declines as the subscriber count falls within each agreement’s subscriber-linked fee structure, and the total market generating subscriber-linked fees contracts as the industry-wide subscriber base shrinks.

Renewal negotiations in this environment are inherently adversarial: operators under revenue pressure seek to renegotiate licensing terms downward at renewal, arguing that the declining subscriber base justifies reduced total fees. Adeia’s historical 90%-plus renewal rate has been achieved despite these dynamics by demonstrating that the portfolio’s value extends beyond the declining linear subscriber base into connected device, streaming delivery, and over-the-top applications that the operators are simultaneously developing, applications that typically carry their own per-user or fixed-fee licence obligation.

The DISH non-renewal: Context, significance, and what happens next

DISH Network’s decision not to renew its agreement with Adeia upon expiry at end of March 2026, and Adeia’s subsequent filing of a patent infringement complaint in the U.S. District Court for the District of Colorado in April 2026, is the most significant recent development in the Pay-TV segment. The analytical imperative is to contextualise this event correctly: it is a commercially meaningful adverse development, but it is not evidence of a general Pay-TV customer defection pattern, and its specific drivers are company-specific rather than industry-representative.

DISH has been in prolonged financial and operational distress. The company completed a contested and structurally complex merger with EchoStar, which involved multiple regulatory conditions, debt restructuring, and operational integration challenges, and has sustained multi-year subscriber losses across both its satellite TV platform and its Sling TV virtual MVPD service. DISH’s ability and willingness to commit to multi-year IP licensing fees is constrained by its balance sheet position in a way that a financially healthy Pay-TV operator’s would not be.

The decision not to renew a long-term licensing agreement, triggering litigation, is consistent with a company under severe balance sheet pressure making near-term cost reduction decisions that accept long-term legal risk in exchange for immediate cash conservation.

The path forward is defined by the litigation. Adeia has demonstrated, twice in the preceding eighteen months, that patent infringement complaints against major technology companies resolve through negotiated licences within a compressed timeframe. The Disney resolution covered all outstanding litigation and produced a long-term agreement; the AMD resolution occurred in four months. DISH’s financial constraints, which limit its capacity to sustain expensive, prolonged patent litigation against a well-funded licensor with a strong enforcement track record, may similarly accelerate a resolution.

A DISH settlement that includes back-royalties for the uncontracted period beginning April 2026, plus a renewed multi-year agreement at rates reflecting the current and projected future subscriber base, represents the base case outcome and is incorporated in Adeia’s FY2026 guidance construction.

Pay-TV and diversification metrics

6. The CEO Succession: Leadership at an Inflection Point

Paul Davis announced his intention to step down as CEO by Q4 2026 for health reasons. The timing is important: the succession is occurring while the semiconductor programme is at its most commercially demanding, DISH and DirecTV litigation requires sustained direction, and the OTT pipeline is at its highest deal velocity. Who comes next, and with what background, is the most important unobservable variable in the near-term investment horizon.

Davis’s tenure: The commercial and financial legacy

Paul Davis has led Adeia and its predecessor entities for nearly 15 years, with four years as CEO of the standalone public company since the October 2022 separation. His tenure at the helm of the separated entity has been characterised by three dominant achievements.

The first is financial restructuring at pace: the term loan was reduced from approximately $800 million at separation to $398.6 million by Q1 2026, a reduction of approximately $400 million in under four years achieved entirely through operating cash flow generation without equity dilution. The pace of debt reduction has consistently exceeded what the market modelled, contributing to multiple credit quality improvements culminating in the S&P upgrade to BB/Stable in Q2 2026.

The second is portfolio expansion at consistent double-digit rates: the patent portfolio grew by over 35% from separation through Q1 2026 through three consecutive years of double-digit expansion. This growth reflects sustained investment in internal R&D at approximately $67.5 million in FY2025 and a disciplined tuck-in acquisition programme that added 11 acquisitions in FY2025 and Q1 2026 combined. The portfolio growth is commercially important because it expands the addressable licensing surface, creates new product innovation arguments in renewal negotiations, and demonstrates to prospective licensees that Adeia is an active innovator rather than a passive holder of legacy IP.

The third is commercial execution at record pace: FY2025 produced 26 agreements, a record total and a record 12 with new customers. This deal cadence represents a meaningful acceleration from prior years and reflects both the portfolio’s expanding applicability and Davis’s personal relationships with the procurement and legal leadership of major technology companies. The landmark deals of his tenure, Amazon, AMD, Disney, Google (renewed), Kioxia, Microsoft, SanDisk, span every major vertical in the licensing programme and collectively transformed Adeia from a Pay-TV-dependent legacy licensor into a diversified multi-vertical IP platform.

Davis’s institutional knowledge of the bilateral licensing relationships with over 145 counterparties, and the negotiating dynamics, relationship history, and proprietary commercial intelligence embedded in those relationships, represents an asset that cannot be fully documented or transferred. A licensing negotiation with a major technology company is a multi-year relationship built on personal credibility, consistent behaviour, and the counterpart’s assessment of the licensing organisation’s reliability as a long-term partner.

Davis has personally overseen the most consequential licensing conversations in the company’s recent history. The risk that his departure disrupts the continuity of those relationships, particularly in the DISH and DirecTV proceedings, where his personal knowledge of the prior agreement terms and relationship context is directly relevant, is real and must be modelled explicitly rather than dismissed as immaterial.

The board’s succession plan and its structure

The board’s stated succession plan involves Davis remaining in the CEO role until a successor is identified and appointed, with the target for completion by Q4 2026. The Transition Committee is chaired by board chairman Dan Moloney, who has served on the Adeia board since before separation and therefore possesses institutional knowledge of the company’s strategic history that reduces the transition committee’s information disadvantage relative to an external search.

A nationally recognised executive search firm has been engaged, with both internal and external candidates being evaluated. Management’s reference to a senior leadership realignment completed in Q4 2025 suggests the board has identified and developed internal candidates over an extended period, which would shorten the search timeline and reduce the integration risk associated with an external appointment who must build relationships with 145-plus licensees from scratch.

The market’s reaction to the announcement was severe: ADEA fell approximately 17% in the trading session following the Q1 2026 earnings release, which combined operating results that beat consensus expectations on revenue, earnings, and cash flow with the CEO departure announcement. The single-session decline on a fundamental beat confirms that investors ascribe significant value to Davis’s personal institutional knowledge and treated the departure as an unquantified strategic risk that the strong financial results were insufficient to offset.

The stock decline represents a governance discount that has been applied to the operating business performance and that will only be removed when the successor’s identity and credentials provide the market with sufficient information to quantify the transition risk.

Why the successor’s background is decisive

IP licensing businesses are more sensitive to leadership background than most other business models because the CEO’s credibility with counterparts, comfort with patent litigation risk, and strategic vision for portfolio monetisation shape deal terms, enforcement decisions, and the pipeline of prospective licensees in ways that compound over time. Three distinct successor profiles would produce meaningfully different strategic trajectories over the three-to-five year investment horizon.

A successor with a legal and IP enforcement background would likely maintain or intensify the litigation programme against DISH, DirecTV, and potential future targets, maximising the probability of recovering licensing revenue from contested relationships and sending a market signal that the enforcement culture is intact. This profile is most likely to accelerate the DISH and DirecTV resolutions and to approach the OTT holdout pipeline from an enforcement-first posture.

The risk is that an overly adversarial reputation in the market slows voluntary licensing discussions with prospective licensees who would prefer to negotiate rather than litigate. A successor with a technology commercialisation background, someone who has built licensing programmes at a major technology company, semiconductor manufacturer, or established IP licensing firm, would bring credibility in technical conversations with chip engineers and procurement leadership that is genuinely difficult to replicate through relationship transfer alone.

This profile is most likely to accelerate the semiconductor programme’s expansion toward the $100 million target and to engage effectively with the AI supply chain participants evaluating RapidCool. A successor with a corporate development orientation might assess whether M&A, acquiring additional IP platforms or considering strategic combinations with other pure-play licensors, creates portfolio scale advantages that organic licensing cannot achieve within the target timeframe.

7. Leverage & The 2026 Revenue Contraction Question

Adeia delivered record revenue, EBITDA, and net income in FY2025, then guided a revenue decline for FY2026. Investors who read that as demand deterioration are applying the wrong frame. The FY2025 record was inflated by the Disney agreement’s non-recurring component; the contraction is mechanical, and disaggregating it from underlying commercial momentum is the prerequisite for any accurate forward model.

The operating leverage story: Why margins matter more than revenue

The most significant element of the FY2022–FY2025 financial history is the margin expansion trajectory, not the revenue trajectory. Adjusted EBITDA margins have expanded from an estimated sub-60% range in FY2022–2023 to 62.3% in FY2024, 62.6% for FY2025, and a record 73% in Q4 2025 on the Disney-elevated revenue base. This expansion reflects two structural forces working simultaneously.

The first is amortisation declining: intangible amortisation from the legacy Rovi, TiVo, and DTS acquisition pools is declining as those pools amortise toward zero, from an estimated $110 million in FY2022 to $56.6 million in FY2025 and continuing to decline through the guidance period. Since amortisation is a non-cash charge, its decline improves both reported operating income and the cash-to-earnings conversion ratio without requiring any revenue growth.

The second is the incremental margin structure of the business. CFO Keith Jones confirmed on the Q4 2025 earnings call that approximately 40% of incremental revenue in FY2024–2025 converted to incremental adjusted EBITDA, a confirmation that the business model generates meaningful operating leverage as revenue scales.

When a new licence agreement is signed, the associated recurring revenue stream is added with minimal incremental cost: no new manufacturing capacity is required, no new supply chain is needed, and the legal and licensing infrastructure required to administer the agreement is largely fixed. The primary incremental cost is the R&D investment required to sustain the portfolio’s technical relevance, which is a relatively fixed annual commitment rather than a per-agreement variable cost.

Five analytical frames for the FY2026 contraction

The FY2026 guidance of $395–$435 million against FY2025’s $443.4 million requires five distinct analytical frameworks to evaluate correctly. Investors who apply only one or two will systematically reach incorrect conclusions about the business’s underlying commercial health.

The first frame is the Disney non-recurrence. The Disney agreement signed in Q4 2025 included a material up-front fee component for past-period use and outstanding litigation resolution. This was recognised in Q4 2025 and inflated the FY2025 base. The Disney recurring royalty stream will contribute ongoing revenue, but the up-front recognition event inflated the FY2025 total in a way that cannot be replicated in FY2026 without a comparably sized new platform deal.

Removing the estimated non-recurring Disney component from FY2025 revenue provides a more relevant comparison base for FY2026 guidance, and that adjusted comparison narrows the apparent year-over-year gap significantly, potentially from a headline 8% decline to a flat or modestly positive comparison against the underlying recurring and normalised non-recurring base.

The second frame is the DISH gap. The DISH recurring stream that expired at end of March 2026 represents a real reduction in the FY2026 recurring base that is incorporated in guidance. It is not, however, a permanent impairment: the litigation filed in April 2026 is the recovery mechanism, and a settlement would restore the recurring stream in a future period. The DISH gap is a timing issue with a defined resolution pathway, not a structural loss of licensing relevance.

The third frame is the SanDisk and Kioxia timing. Both agreements, executed in late FY2025, contributed zero revenue in Q1 2026 due to agreement structure and recognition mechanics. Management confirmed these customers will deliver meaningful contributions across Q2–Q4 2026. The semiconductor recurring trajectory through the remaining three quarters is therefore an upward driver that was absent in Q1 but builds as the year progresses — meaning the FY2026 guidance is back-half loaded in a way that makes Q1 results an unreliable guide to full-year outcomes.

The fourth frame is guidance construction methodology. Adeia raised its FY2025 guidance in December 2025 when the Disney agreement was signed, demonstrating a clear pattern: guidance is issued conservatively against the contracted and visible base, and updated when material incremental transactions close. The FY2026 guidance issued in February 2026 was constructed without knowing which specific large transactions would close during the year. Q1 2026 results of $104.8 million above the top of the implied quarterly guidance range confirm the conservatism pattern continues.

The fifth frame is the quarterly trajectory within the guided range. Management guided H1 and H2 2026 revenue as relatively equal, with Q2 modestly below Q1’s $104.8 million. The full-year midpoint of approximately $415 million implies a second-half average of approximately $103–107 million per quarter, consistent with the recurring revenue recovery toward the $90 million quarterly exit rate. This trajectory is not linear: it implies acceleration through Q3 and Q4 as semiconductor agreements activate and the OTT pipeline produces additional agreements. Investors who model FY2026 as a flat quarterly run-rate miss the back-half recovery that management has explicitly guided toward.

Capital return and balance sheet trajectory

The capital allocation framework operates across four simultaneous uses: mandatory term loan amortisation, the quarterly dividend of $0.05 per share (approximately $22 million annually at current share count), the share repurchase programme with $150 million of remaining capacity, and tuck-in portfolio acquisitions funded from operating cash flow. The balance sheet trajectory is straightforwardly positive: the term loan at $398.6 million as of Q1 2026 will be reduced to an estimated $370–400 million by year-end FY2026 and continue declining through FY2027–FY2028 as operating cash flow exceeds the combination of dividends, buybacks, and tuck-in acquisition costs.

The S&P upgrade to BB/Stable in Q2 2026 is an external validation of this trajectory and opens the equity to a broader institutional investor base that requires investment-grade or near-investment-grade credit quality from its portfolio companies. Further credit quality improvement as leverage continues declining is a potential additional catalyst for equity re-rating independent of the operating results.

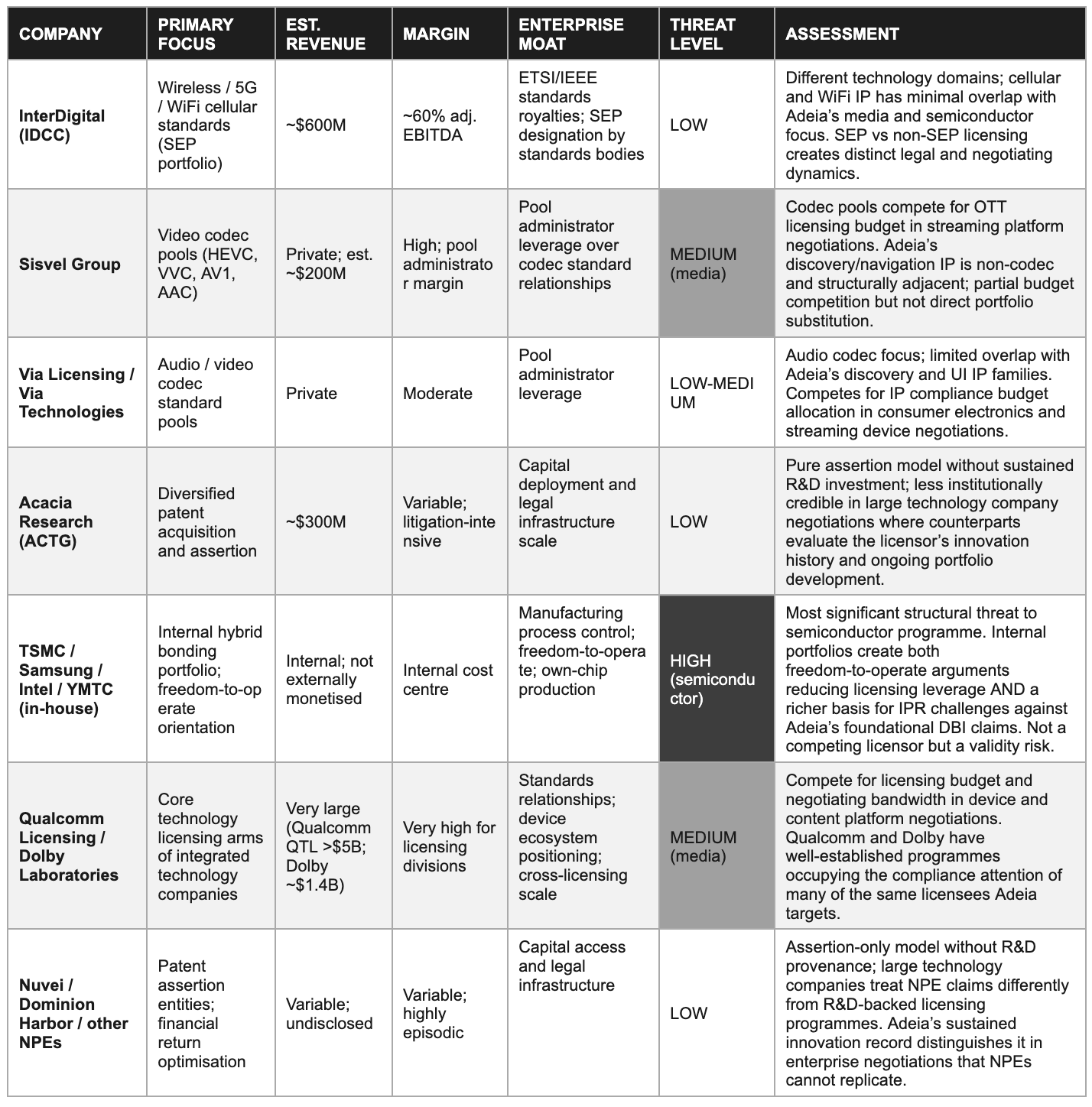

8. Competitive Landscape: IP Licensors, Standards Bodies, and the In-House Threat

Adeia competes in a market with few direct analogues. Most nominally comparable entities are either standards-essential patent administrators, assertion vehicles without R&D backing, or integrated technology companies whose licensing arms are ancillary to product businesses. The most material competitive threat to the semiconductor programme comes not from external licensors but from the chip manufacturers building internal hybrid bonding portfolios.

The media licensing competitive context

The media licensing market has no single dominant competitor with a portfolio that directly replicates Adeia’s scope across content discovery, guide navigation, recommendation, audio, and streaming delivery IP simultaneously. Content discovery and navigation IP is not concentrated in a single competing portfolio; it is distributed across a combination of standards bodies (who administer codec pools but not discovery or navigation IP), integrated technology companies (whose media IP is primarily for internal use rather than external licensing), and a fragmented collection of smaller IP holding companies with narrower portfolios that address individual sub-segments of the media technology stack.

In practice, the competitive dynamic in a major OTT platform or consumer electronics negotiation is less about choosing between Adeia and a direct competitor’s offering and more about the licensee’s assessment of Adeia’s specific portfolio validity, the cost-benefit calculus between licensing and litigating, and the budget prioritisation between multiple concurrent IP compliance obligations. The standards-based codec licensing market, administered by pools including HEVC Advance, MPEG LA, and Sisvel for HEVC, VVC, and AV1 codec standards, competes with Adeia indirectly for IP compliance budget and negotiation attention from OTT platforms and consumer electronics manufacturers.

A major streaming service managing HEVC codec licence compliance, AV1 adoption decisions, and Adeia’s content discovery and navigation licensing conversation simultaneously is allocating a finite IP compliance budget across multiple programmes. The codec pools represent a separate and adjacent IP obligation rather than a direct portfolio substitute, but their presence does create budget competition that affects the timing and economic terms of Adeia’s media negotiations.

Adeia’s institutional credibility relative to non-practising assertion entities is a genuine commercial differentiator in large technology company licensing negotiations. A major OTT platform or consumer electronics manufacturer assessing an IP licensing request evaluates the counterpart’s portfolio provenance, enforcement track record, and reputational standing alongside the legal merits of the specific claims.

Adeia’s sustained R&D investment at approximately $67.5 million in FY2025, its track record of over 145 executed agreements with identifiable named counterparts, its record of enforcing and resolving (Disney, AMD, and a long history of Pay-TV carrier agreements), and its 15-year operating history distinguish it from assertion-only entities and establish a credibility threshold that shorter-tenure entrants cannot replicate on any reasonable timeline.

The semiconductor competitive landscape: Internal portfolios as the primary risk

The semiconductor competitive landscape around hybrid bonding IP is structurally more complex than the media landscape. TSMC, Samsung, Intel, and YMTC have each built substantial patent portfolios in advanced packaging and hybrid bonding adjacent technologies since 2019, representing a more than fourfold increase in the total patent landscape over five years.

The Knowmade 2024 patent landscape analysis identified TSMC, Adeia, YMTC, Intel, and Samsung as the five leading hybrid bonding patent holders, with each occupying different positions in the commercial ecosystem simultaneously: TSMC as both a manufacturing services provider to companies that license Adeia’s portfolio and a potential validity challenger; Samsung as a licensee through its image sensor business and a potential challenger through its memory and logic packaging operations; Intel as a foundry competitor to TSMC building its own advanced packaging portfolio through Foveros Direct.

The key analytical distinction is that these internal portfolios are built primarily for freedom to operate, ensuring manufacturers can produce advanced packages without licensing obligations to each other, rather than for external monetisation. They are not, as of Q1 2026, operating external hybrid bonding licensing programmes that compete directly with Adeia for royalty revenue from chip designers and system vendors.

The competitive threat they pose is therefore to Adeia’s future licensing leverage rather than its current revenue stream: as the manufacturers’ internal portfolios grow and become more technically sophisticated, they create a larger body of prior art that constrains the breadth of Adeia’s future patent filings, and they provide a richer basis for inter partes review challenges against Adeia’s most commercially important existing claims. The timeline for an IPR to run from filing to PTAB decision is typically 12 to 18 months, meaning that an IPR filed in 2026 would have a decision in 2027–2028, directly within the investment horizon for the semiconductor revenue ramp.

Competitive landscape assessment

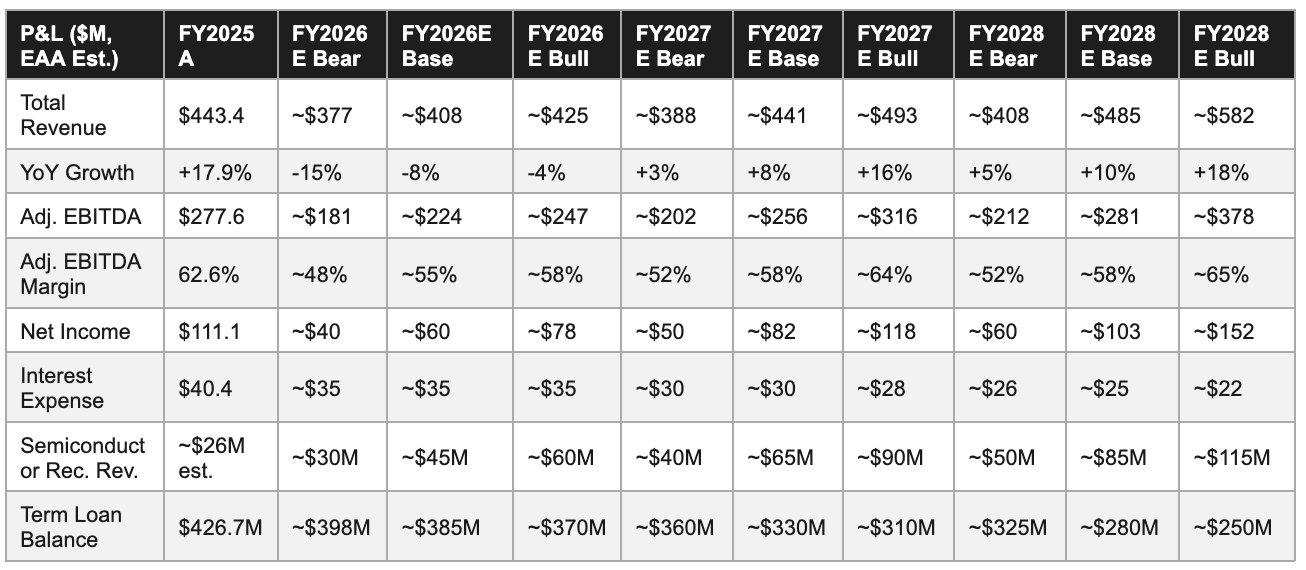

9. Forward Financial Model: Bear / Base / Bull Through FY2028

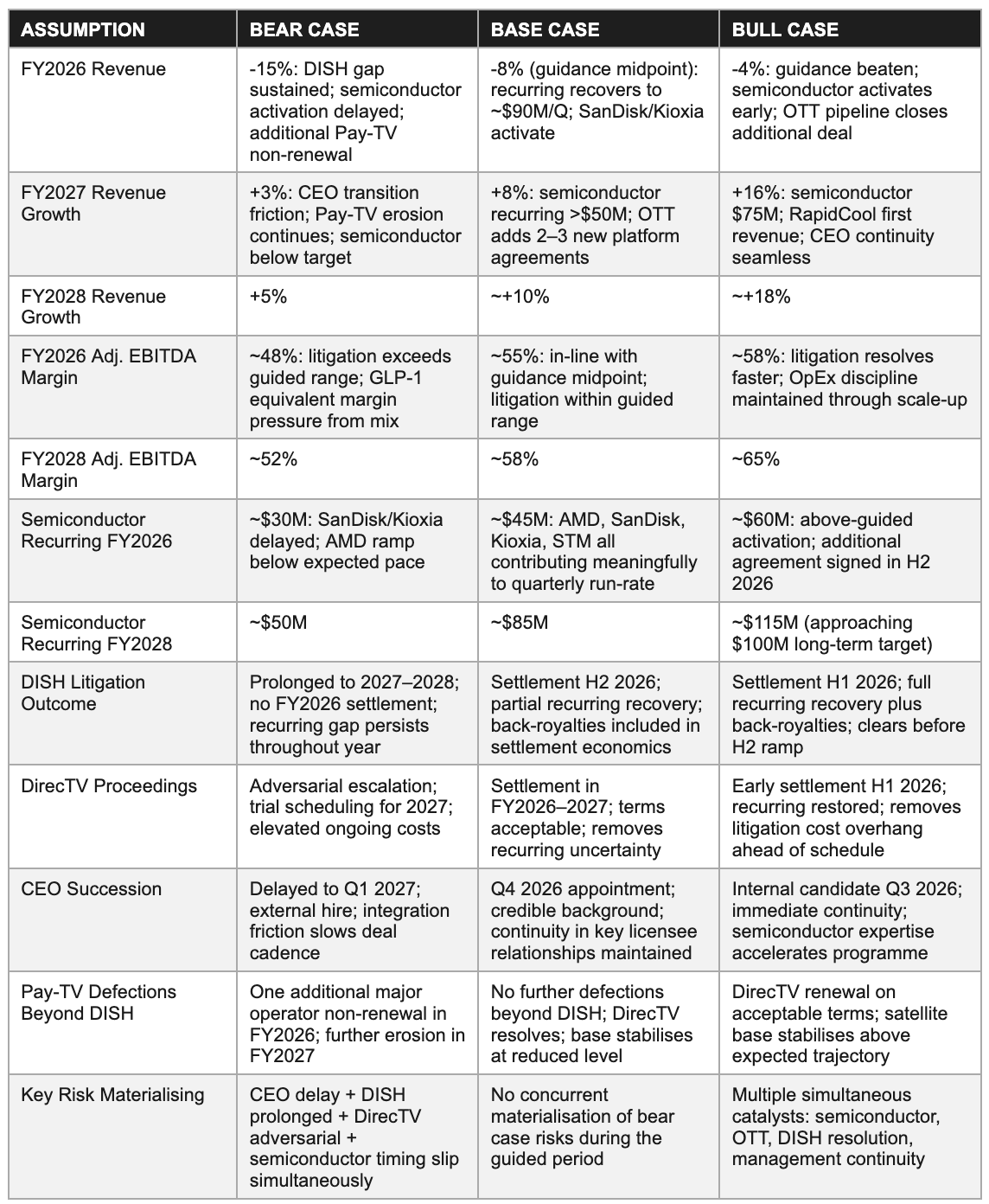

The three-scenario model anchors the base case to management’s FY2026 guidance, with FY2027 and FY2028 driven by explicit assumptions on Pay-TV decay, semiconductor ramp, litigation outcomes, and CEO succession. The bear case requires four risks to partially materialise concurrently; the bull case requires multiple catalysts to fire simultaneously. Both are individually plausible, neither is the most probable outcome.

Scenario assumptions

Three-year P&L projection

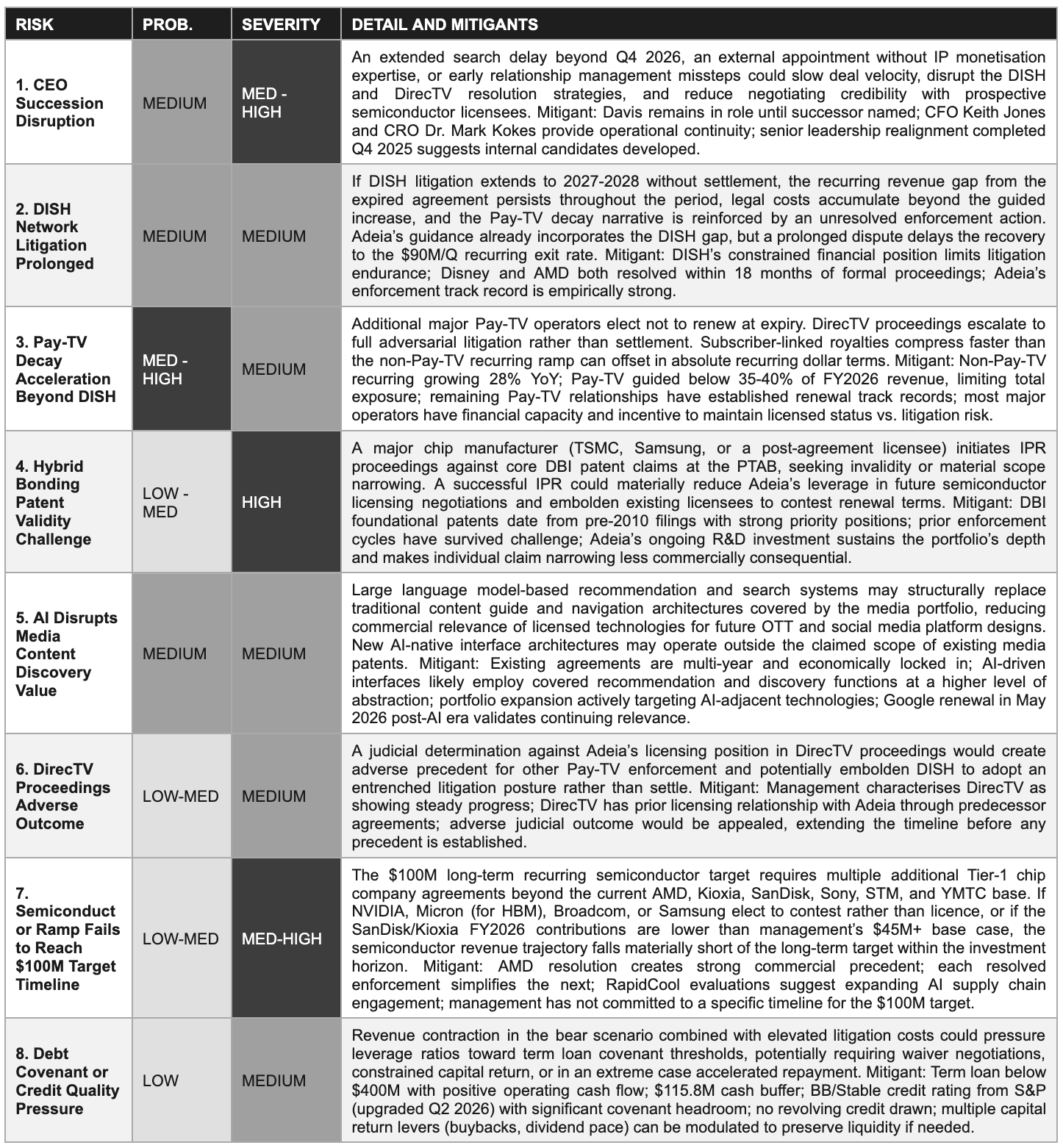

10. Risk Matrix

Each risk below is a specific variable whose outcome determines which scenario is realised. Probability reflects the likelihood of a significant negative outcome within 24 months. Severity reflects the degree of long-term impairment if it materialises. Mitigants are stated for each risk to ensure the bear case receives equal analytical rigour.

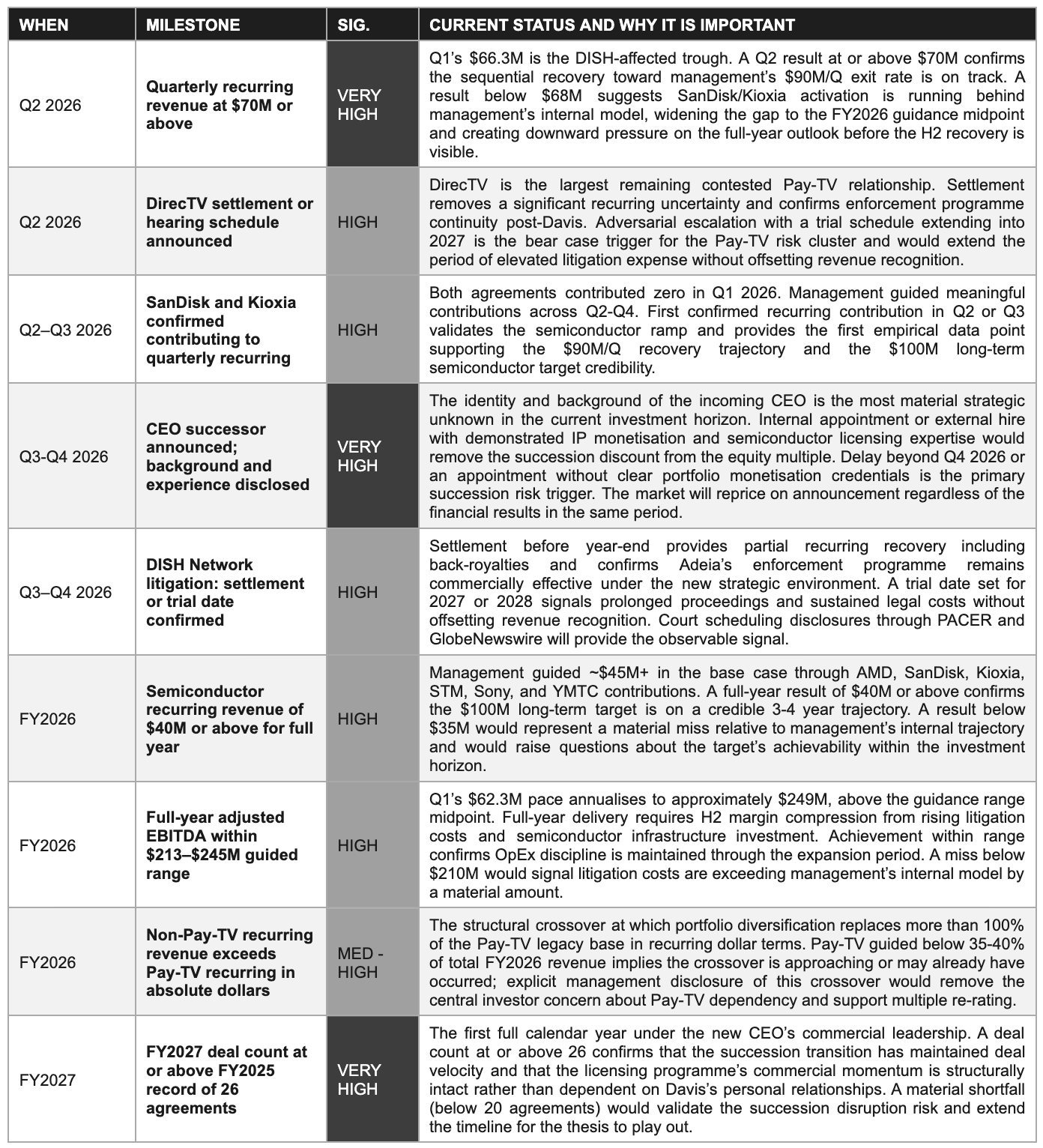

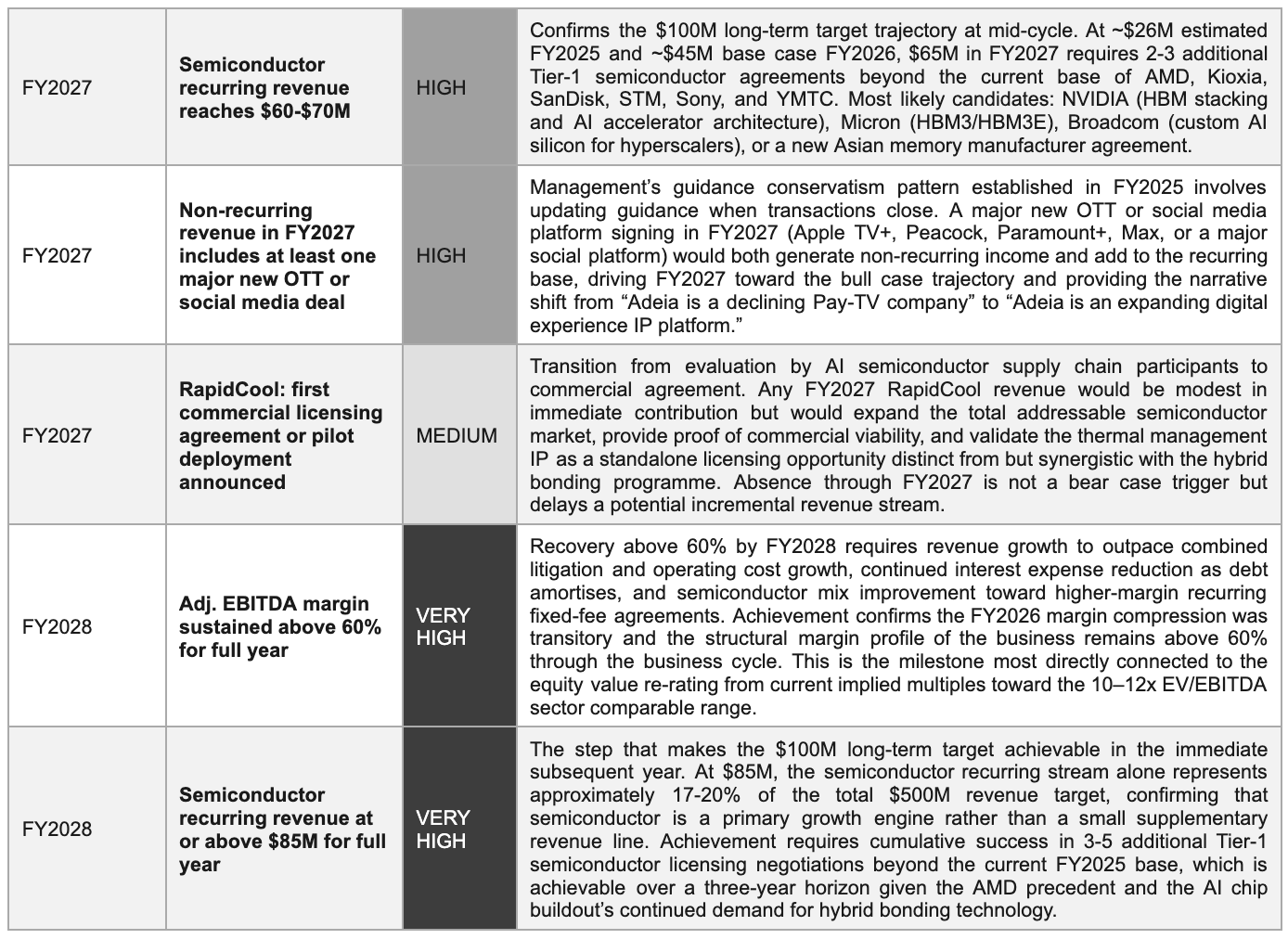

11. Milestone Tracker: What to Watch 2026-2028

The milestones below are the observable proof points that will confirm or challenge the base case. The Q3-Q4 2026 cluster is the most information-dense period: CEO succession, DISH resolution, and semiconductor activation are all expected within the same window, and their collective outcomes will determine whether the market narrative shifts from succession discount to diversification progress.

12. Opinion & Investment Perspective: Bull, Base & Bear Cases

What follows is our view as of Jun 2026, presented to give the bull, base, and bear cases equal analytical weight. The stock fell approximately 17% on a fundamental beat the day CEO succession was announced. That disconnect between reported performance and market price is the analytical starting point.

The bull case: Four pillars that are each individually achievable

The first pillar is the semiconductor revenue ramp and its inherent commercial momentum. Adeia owns foundational hybrid bonding patents for a technology that is central to AI chip architecture. The AMD agreement establishes that the DBI portfolio is licensable at the frontier of commercial semiconductor design. SanDisk and Kioxia are existing licensees whose revenue contributions are expected to activate meaningfully through FY2026. STMicroelectronics has been under licence.

The path from an estimated $26 million in FY2025 semiconductor recurring revenue to the $100 million long-term target is populated by identifiable and quantifiable prospective licensees: NVIDIA, whose Blackwell architecture and HBM3E memory stacking relies on direct bonding techniques at scale; Micron, whose HBM3 and HBM3E products are central to the AI memory supply chain; Broadcom, whose custom AI silicon for hyperscaler customers employs advanced heterogeneous integration; and Samsung, whose HBM production and 3D NAND operations both employ bonding techniques that overlap with the DBI portfolio.

Each incremental semiconductor agreement is not merely revenue in itself; it is a commercial precedent that simplifies the next negotiation by demonstrating that the IP is recognised as valid and relevant by technically sophisticated buyers who could have contested rather than licensed.

The second pillar is the media portfolio’s demonstrated durability and expanding commercial applicability. The FY2025 record of 26 agreements, spanning OTT, social media, e-commerce, consumer electronics, Pay-TV, and semiconductors is the strongest evidence that the portfolio retains commercial relevance as technology platforms evolve. The Google licence renewal in May 2026, extending a relationship that dates to 2012, is the most salient recent proof point: Google is among the world’s most technically sophisticated IP evaluators and has access to world-class patent counsel, and its consistent renewal of the Adeia media licence across more than a decade reflects a sustained commercial assessment that the portfolio covers relevant technologies across Google’s current and anticipated product architecture. The OTT expansion, with Amazon and Disney both under long-term agreements, creates the licensed-base dynamic that accelerates conversion of the remaining unlicensed major platforms.

The third pillar is the debt reduction compounding equity value per share independently of revenue performance. The term loan reduction from approximately $800 million at separation to $398.6 million by Q1 2026 has mechanically increased equity value: holding enterprise value constant, each dollar of debt repaid transfers directly to equity holders. The continuing amortisation trajectory, funded by operating cash flow that has been consistently positive and growing, implies another $150–$200 million of term loan repayment over FY2026–FY2028 in the base case. Combined with the $150 million remaining share repurchase authorisation, the per-share equity improvement from capital return is material relative to the current implied market capitalisation.

A company that simultaneously reduces its share count and its debt, while maintaining positive operating cash flow, is generating per-share value even in periods of modest headline revenue growth. The interest expense reduction alone, from approximately $55 million in FY2022 to an estimated $35 million in FY2026 and continuing to decline, contributes approximately $14–15 million of additional annual after-tax income that arrives regardless of deal activity.

The fourth pillar is the established guidance conservatism pattern that creates systematic upside optionality. Adeia raised FY2025 guidance in December 2025 when the Disney agreement was signed, demonstrating a clear pattern: guidance is issued conservatively against the contracted and visible base, and updated when material incremental transactions close.

Q1 2026 results of $104.8 million above the implied quarterly guidance range confirm the pattern persists. In the bull case, FY2026 guidance is beaten by $15–25 million through a combination of semiconductor agreement activation ahead of schedule, an additional major OTT or social media deal closing in H2, and DISH settling earlier than the guided timeline. Management’s pattern of issuing floors rather than ceilings means that any significant new transaction signed during FY2026 represents potential upside to the currently guided range.

The Bear Case: Four concurrent pressures and their interaction

The bear case is credible, internally coherent, and warrants the same analytical depth as the bull case. It requires four pressures to materialise partially or fully within a twelve-to-eighteen month window.

The first is CEO succession disruption: an extended search beyond Q4 2026, an external hire without relevant IP or semiconductor licensing expertise, or early relationship management failures that slow deal velocity below the FY2025 record pace in the first full year of the new CEO’s tenure.

The second is DISH litigation prolonged without settlement: DISH adopts an entrenched posture, motivated by the calculation that its financial distress makes the litigation cost manageable relative to the licensing obligation, and the case runs to 2027–2028 before resolution.

The third is semiconductor revenue ramp underperformance: SanDisk and Kioxia contribute less than guided in FY2026 due to activation delays, no new Tier-1 semiconductor agreement is signed in H1 2026, and the full-year semiconductor total is approximately $30 million rather than the $45 million base case.

The fourth is an additional major Pay-TV non-renewal: a second operator elects not to renew, adding another gap to the recurring base that OTT and semiconductor growth cannot immediately offset in the same year.

In the bear case, FY2026 revenue declines to approximately $377 million, adjusted EBITDA compresses to approximately $181 million at roughly 48% margin, and net income falls to approximately $40 million. The balance sheet does not face distress in this scenario: the $115.8 million cash position, no drawn revolving credit, BB/Stable credit rating, and positive operating cash flow (even in the bear case, the business generates meaningful cash from its existing contracted recurring base) provide substantial runway.

The damage is primarily to the investment narrative and to the equity multiple: a period of concurrent succession uncertainty, Pay-TV non-renewals, and semiconductor underperformance creates a sustained narrative of deterioration that is difficult to reverse until observable proof points emerge. At 7x EV/EBITDA on FY2027 bear case adjusted EBITDA of approximately $202 million, the implied enterprise value is approximately $1.4 billion, translating to equity of approximately $1.1 billion or roughly $9–10 per share, consistent with the lower end of the current trading range.

The critical distinction between the bear case and a structural impairment of the investment thesis is that the bear case is time-limited and reversible. The hybrid bonding patents do not expire in the relevant investment horizon; the media portfolio’s applicability to digital content platforms does not diminish as a result of bad quarterly results; the debt reduction trajectory continues mechanically. A 12–18 month period of adverse reported results driven by succession and litigation timing delays the realisation of the portfolio’s value, it does not impair the value itself.

13. Investment Scorecard & Conclusion

The scorecard consolidates the twelve preceding sections. The paths to the bull and base cases are multiple and grounded in execution the company has already demonstrated. The path to the bear case requires a specific concurrent sequence of adverse outcomes. That asymmetry, at the current implied multiple, is the core of the investment case.

The bottom line

Adeia owns two franchises with genuinely durable and empirically validated characteristics. The media IP portfolio, built over decades of R&D investment, enforced through a litigation programme with a strong commercial track record, renewed at over 90% historically, and now covering the full spectrum of digital content consumption from Pay-TV through OTT, social media, e-commerce, and AI-driven recommendation, generates consistent and growing cash flows from a diversifying base of over 145 licensees.

The semiconductor portfolio, centred on hybrid bonding IP that was pioneered before the rest of the industry recognised its commercial significance, is positioned at the intersection of the two most powerful technology trends of the current decade: AI compute at scale and the advanced memory architectures those workloads require. Both franchises benefit from the same structural advantage: the relevant technologies are embedded in products that large companies cannot easily design around without material cost and engineering risk, creating a recurring licensing obligation that produces royalty revenue independently of Adeia’s ongoing commercial execution in any given quarter.

The near-term investment case is complicated by three live uncertainties, each of which is real, quantifiable, and has a defined resolution timeline. The CEO succession is the most significant: Davis built many of the bilateral relationships and negotiating frameworks that underpin the current licensing programme, and a transition without a credible successor in place risks disrupting institutional continuity at a commercially active moment when the semiconductor programme, the DISH litigation, and the OTT pipeline all require sustained strategic direction.

The Pay-TV decay is structural and the DISH and DirecTV situations represent its most acute current expression: two major satellite Pay-TV operators in contested relationships simultaneously is the fastest-moving negative catalyst in the current reporting environment. And the FY2026 revenue contraction will generate negative year-over-year comparisons in the quarterly results through the first half of the year, creating headline metric pressure that is disconnected from underlying commercial quality but real in its near-term market impact.

These three uncertainties share a common and analytically important characteristic: all are resolvable within a defined and observable timeframe. The CEO succession has a stated Q4 2026 target with an active search process underway. The DISH and DirecTV proceedings will produce observable outcomes within twelve to twenty-four months. The FY2026 revenue contraction will lap the Disney-inflated FY2025 base by Q4 2026, at which point the year-over-year comparison reverses into a growth narrative even under the base case assumptions.

An investor who holds through the clarity-gaining period, with explicit modelling of the debt reduction as equity value creation independent of revenue growth, explicit treatment of Pay-TV erosion as a manageable and decelerating headwind rather than a catastrophic impairment, and explicit conviction on the hybrid bonding opportunity at the intersection of AI and advanced semiconductor packaging, is holding a business whose fundamental earnings power is substantially above what the current implied multiple reflects.

The single most important insight from this analysis is that Adeia’s investment case at the current implied multiple range concerns execution across outcomes that are observable within a twelve-to-twenty-four month window. CEO successor quality, semiconductor revenue trajectory, and DISH resolution timing are all resolvable uncertainties with defined timelines. Investors who hold through that clarity-gaining period with explicit modelling of each variable, rather than applying a uniform discount for aggregate uncertainty, may find that the current implied multiple represents a materially attractive entry point on a three-to-five year investment horizon.

The multi-year investment case rests on three observable and achievable outcomes: that the CEO transition is executed credibly and deal velocity is maintained at or near the FY2025 record pace through FY2027; that hybrid bonding IP monetisation continues building toward the $100 million recurring revenue target as additional Tier-1 semiconductor companies recognise their licensing obligations following the AMD precedent; and that the media portfolio’s demonstrated applicability to OTT, social media, and e-commerce generates enough new recurring agreements to more than offset the Pay-TV erosion in absolute recurring dollar terms by FY2027.

None of these outcomes requires a technological breakthrough, a macroeconomic tailwind, or a management performance that exceeds the company’s own recent track record. They require Adeia to continue doing what it has demonstrated the capacity to do across four years as a public company and 15 years of operating history: enforce valid patents, sign multi-year agreements with major technology companies, expand the portfolio into adjacent technologies, and allocate capital with discipline.

Sources

This analysis is based exclusively on publicly available information as of Jun 2026. Primary sources: Q1 2026 earnings release (May 2026, GlobeNewswire); Q1 2026 earnings call transcript (May 2026, The Motley Fool / Globe and Mail); Adeia 10-Q Q1 2026 (SEC EDGAR, May 2026); Q4 2025 earnings release and full-year FY2025 results (Feb 2026, GlobeNewswire); Q4 2025 earnings call transcript (Feb 2026, The Motley Fool); Adeia 10-K FY2025 (SEC EDGAR, Feb 2026); Q3 2025 earnings release (Nov 2025, GlobeNewswire); Q2 2025 earnings release (Aug 2025, GlobeNewswire); Q1 2025 earnings release (May 2025, GlobeNewswire); CEO transition announcement (May 2026, GlobeNewswire); Google licence renewal announcement (May 2026, GlobeNewswire); DISH Network litigation filing press release (Apr 2026, GlobeNewswire); S&P credit upgrade reference (Q1 2026 earnings call, May 2026); Adeia pioneering hybrid bonding announcement (Jun 2024, GlobeNewswire); Hybrid Bonding Patent Landscape Analysis 2024 (Knowmade / Research and Markets, Sep 2024, BusinessWire); 3D InCites coverage of Ziptronix / Sony licence (Mar 2015); Semiecosystem Adeia IP history (Nov 2025); Fintool Adeia earnings analysis (Feb 2026 / May 2026); StockTitan 10-Q analysis (May 2026).

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Adeia, Inc. (NASDAQ: ADEA) or any other security. All information is sourced from publicly available materials believed to be reliable as of June, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.