BETA TECHNOLOGIES, INC.

Electric Aviation at the Certification Threshold: Can a $3.9 Billion Backlog and Aftermarket Economics Convert Pre-Revenue Investment into Durable Cash Flow?

1. Corporate Profile & The Enabling Technologies Thesis

BETA Technologies is a vertically integrated electric aerospace company that designs and manufactures its own batteries, motors, flight controls, and charging systems, then sells them to other aircraft makers, the military, and into its own aircraft. That recurring revenue model is the thesis. The aircraft is just the delivery mechanism.

The company’s central thesis rests on a distinction that the electric aviation industry has largely failed to communicate to equity investors with precision. BETA calls its technology stack the Enabling Technologies platform, a term that is commercially meaningful rather than marketing language. An aircraft OEM that integrates third-party batteries, third-party motors, and third-party avionics earns revenue once at the point of aircraft sale and then cedes the aftermarket economics to its component suppliers.

BETA’s vertical integration is designed to capture not just the aircraft sale but the entire lifetime revenue relationship with the operator: the replacement battery sets (estimated at 18 to 20 per aircraft over an operational life), the serviced motor and inverter systems, the charging network access fees, and the data and monitoring services that the proprietary battery management system enables.

At the scale of hundreds of aircraft per year in service, the difference between these two business models is the difference between a capital goods manufacturer and a long-duration recurring revenue platform, and it is that long-duration platform economics that the current investment case is priced to reflect, even though the aircraft delivering those economics has not yet received type certification.

The four revenue streams that BETA’s business model is designed to generate are: first, aircraft sales at estimated list prices of $4 to $4.5 million per unit, covering the CX300 eCTOL, the A250 eVTOL, and the MV250 hybrid-electric defence platform; second, battery aftermarket sales at estimated recurring revenue of approximately $13 million per aircraft over its operational life; third, propulsion and motor component supply to third-party aircraft manufacturers under multi-year agreements, of which the Eve Air Mobility pusher motor supply contract (up to $1 billion over 10 years per BETA’s December 2025 earnings disclosure) is the most commercially visible; and fourth, charging network access fees from operators who use BETA’s deployed charging infrastructure.

As of Q1 2026, the only active revenue streams are engineering and consulting services, primarily government defence contracts and commercial R&D agreements, and early component deliveries under the Eve supply agreement. The product revenue streams that will eventually dominate the income statement have not yet activated because the ALIA aircraft have not received FAA type certification, and the installed base of operational aircraft from which aftermarket revenue will flow does not yet exist.

This pre-revenue-scale structure makes the current financial statements a structurally misleading guide to long-run investment value if read in isolation. The income statement shows annual losses in the hundreds of millions of dollars and revenues in the tens of millions. Those figures are the correct representation of a company in the certification phase of an aerospace development programme, they are not a signal of business model failure or commercial irrelevance.

The correct framework for evaluating BETA’s investment case is to assess the quality of the assets being built during this investment phase: the patent portfolio of 460-plus issued patents, the manufacturing facility producing conforming aircraft, the customer relationships with creditworthy operators across six demand verticals, the charging network spanning 123 deployed sites across four countries, and the 139,000-plus nautical miles of flight test data that constitute the evidence base for FAA certification. The question is whether the current enterprise value appropriately discounts the time and risk required to convert those assets into the revenue and margin profile that the aftermarket model implies.

2. Founding Vision and IPO Context

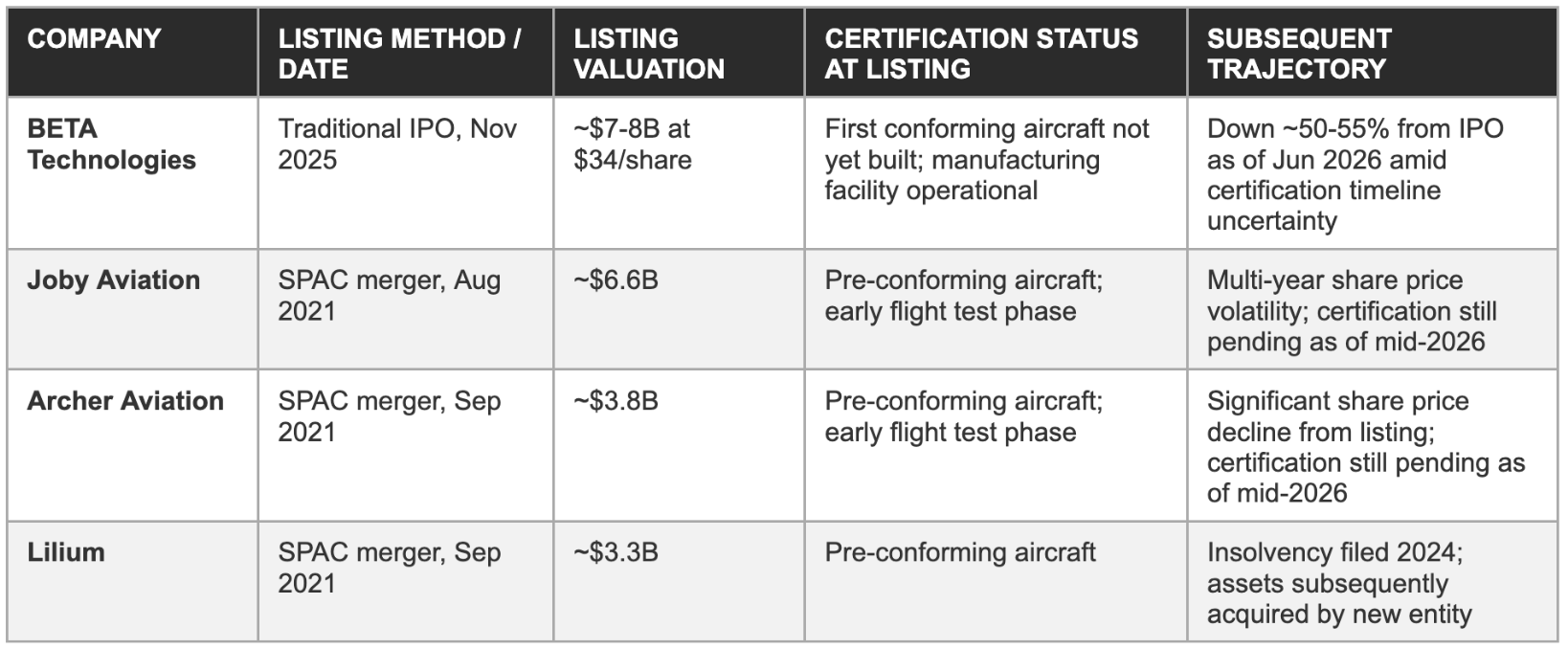

Kyle Clark delayed BETA’s IPO until the company had a manufacturing facility, a $3.5 billion backlog, and a GE Aerospace partnership. The contrast with the 2021 SPAC-era eVTOL cohort is the most useful benchmark for understanding what that discipline bought BETA.

Clark founded BETA with a specific and tightly bounded engineering conviction: that the path to commercially viable electric aviation required full-stack technology ownership at the component level. The dominant alternative approach among eVTOL developers has been to integrate motors from established suppliers, batteries from cell manufacturers, avionics from aerospace tier-1 companies, and focus engineering resources on airframe design and systems integration, an approach with strong aviation historical precedent.

Clark’s assessment was that this approach carried a structural flaw specific to electric aviation: the recurring economics would accrue to the component suppliers rather than to the aircraft manufacturer, because the batteries requiring replacement, the motors requiring service, and the charging infrastructure necessary for operations would all be owned by third parties. To capture the full economic value of electric aviation, including the aftermarket that every aerospace manufacturer understands as the structural source of long-run profitability, the aircraft manufacturer had to own the enabling technology at the component level.

The patent portfolio BETA assembled over eight years, 460-plus issued patents as of mid-2026, covering battery chemistry and pack architecture, motor and inverter design, flight control algorithms, charging equipment design, and the software systems connecting them, is the legal and technical expression of that founding conviction. Each patent represents a specific engineering problem that BETA solved in-house rather than delegating to a supplier, and each solution is now a proprietary asset that a competitor seeking to replicate BETA’s aftermarket model would have to design around, license, or develop independently. The investment required to build this portfolio in the pre-revenue phase was funded by approximately $1.7 billion raised across multiple private financing rounds between 2018 and the IPO.

The decision to delay the IPO also had a cost. BETA absorbed eight years of operating losses funded entirely by private capital, during which founders, early employees, and early investors were illiquid in a business that was spending hundreds of millions of dollars annually on assets that did not yet generate meaningful revenue. Whether the delayed IPO strategy produced better long-term outcomes for public market shareholders than an earlier listing would have is a counterfactual that cannot be resolved.

What is observable is that BETA arrived at the public markets with a manufacturing facility producing conforming aircraft, a commercial backlog growing at $375 million per quarter, and a GE Aerospace partnership that none of the 2021 SPAC cohort achieved, and that the subsequent financial distress of multiple SPAC-era peers validates the risk that BETA avoided by deferring the IPO until the asset base was substantive.

IPO pricing context versus SPAC-era peers

3. Product Architecture: The ALIA Platform, MV250, and the Three-Aircraft Strategy

Three aircraft share one technology foundation. The CX300 is the near-term certification priority, the A250 eVTOL follows roughly a year behind, and the MV250 extends the platform into defence. Shared batteries and motors mean each new variant costs far less to develop than the first.

The ALIA CX300: The certification priority

The ALIA CX300, marketed under the eCTOL (electric conventional takeoff and landing) designation, is a fixed-wing, fully electric aircraft accommodating a pilot and up to four passengers or equivalent cargo volume. The aircraft has a wingspan of approximately 50 feet, a maximum range of approximately 250 nautical miles per charge under standard conditions, and a cruise speed in the range of 150 to 170 miles per hour, positioning it competitively against the Cessna Caravan and comparable single-engine turbopropeller aircraft that dominate the short-haul regional cargo and air taxi markets. Ground charging time using BETA’s Charge Cube equipment is under one hour, enabling multiple revenue-generating cycles per day on short-haul routes where turnaround speed is a commercial constraint.

The CX300 is designed for operations from standard general aviation airports without vertiport infrastructure, a deliberate strategic distinction from purpose-built eVTOL designs that require significant landing infrastructure investment before commercial operations can begin. The CX300’s customer base comprises cargo operators, medical transport services, offshore logistics providers, and regional air taxi operators, all of whom already operate from existing airport infrastructure and would face prohibitive cost and timeline in building new vertiport-class landing facilities before deploying a new aircraft type. The operational compatibility with existing infrastructure reduces the deployment friction for early customers and accelerates the timeline to first revenue-generating flights after certification.

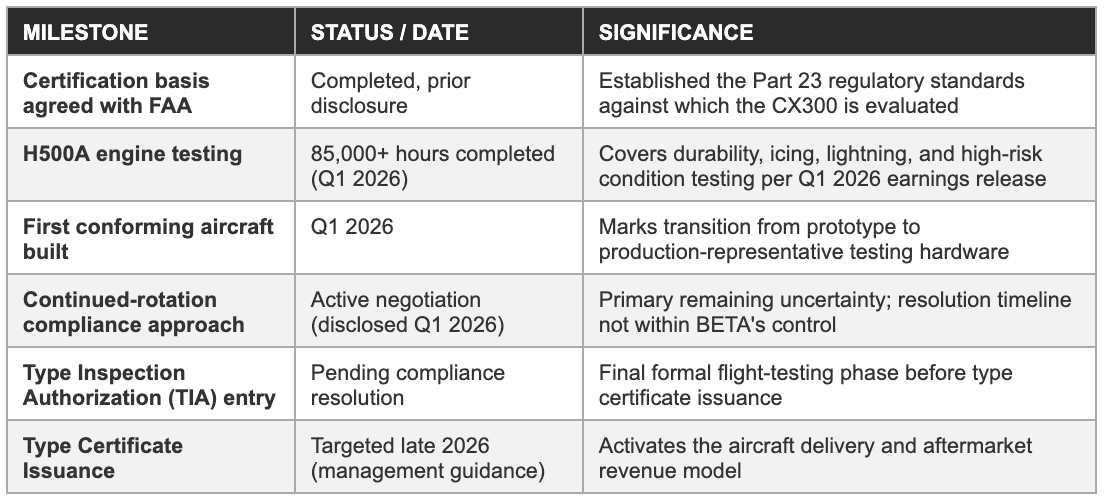

The CX300’s certification pathway is under the FAA’s Part 23 framework, which governs small fixed-wing aircraft with maximum certificated takeoff weight below 19,000 pounds and nine or fewer passenger seats. Part 23 is a mature regulatory framework with decades of precedent, established means of compliance, and a defined certification process that the FAA has administered for thousands of previous aircraft type designs. The first company-conforming CX300 aircraft, meaning an aircraft built to production-representative specifications rather than prototype configuration, was completed in Q1 2026, per the Q1 2026 earnings release. This milestone marks the transition from the development-and-prototype phase to the formal regulatory testing phase that precedes type certificate issuance.

The ALIA A250: The eVTOL variant

The ALIA A250 is BETA’s eVTOL variant, a tiltrotor design capable of vertical takeoff, transition to fixed-wing cruise, and vertical landing. The A250 shares the same 50-foot wingspan, the same passenger capacity, and the same battery architecture and motor platform as the CX300. That shared architecture is the core economic rationale for the dual-variant approach: the marginal engineering and certification cost of the second variant is substantially lower than the development cost of the first because the batteries, motors, inverters, and flight control software have already been developed, tested, and validated for the CX300 programme. The incremental engineering work for the A250 concerns the mechanical lift system design, the transition-phase flight control algorithms, and the structural modifications required for the tiltrotor configuration, significant engineering work, but a fraction of the full-stack development investment required for the CX300.

The A250 is expected to receive FAA certification approximately one year after the CX300 under the base case timeline. The A250’s certification pathway is under the powered-lift category framework, the newer, less precedented regulatory process, which is the structural reason it follows rather than parallels the CX300’s programme. The passenger market addressed by the A250 carries higher per-seat revenue potential than the cargo and logistics applications that the CX300 will initially serve, making the A250 the higher-margin product line over the medium term. The strategic sequencing therefore trades near-term revenue opportunity for near-term certification risk reduction, a trade-off that management has characterised as value-maximising over the full investment horizon.

The MV250: The Defense Channel

The MV250 is a hybrid-electric platform developed in partnership with GE Aerospace, targeting U.S. military logistics, resupply, and medical evacuation missions. The hybrid propulsion architecture combines BETA’s electric motor and battery systems with a GE-developed turbogenerator that extends operational range beyond the 250-nautical-mile envelope of the pure-battery ALIA variants, a critical requirement for military missions where range constraints translate directly to operational effectiveness. The preliminary design review for the MV250 turbogenerator was completed in Q1 2026, per the Q1 earnings release, marking progress toward the detailed design review that precedes prototype construction and military qualification testing.

Military procurement in the United States typically operates under cost-plus contract frameworks for development programmes, providing revenue visibility that is relatively insulated from commercial demand cycles and independent of FAA civilian certification timelines. A military aircraft does not require FAA type certification, it requires qualification under the relevant military airworthiness framework, which is administered by the applicable branch of the U.S. armed forces and follows a different regulatory process from civilian certification.

The MV250 programme therefore provides BETA with a revenue pathway that is not blocked by the CX300 certification timeline. General Dynamics’ contract to design and manufacture propulsion systems for classified undersea applications extends the enabling technologies into a domain entirely distinct from aviation, demonstrating the platform’s applicability across propulsion environments and generating cost-plus engineering revenue with multi-year contract durations.

4. The FAA Certification Sequence: The Central Investment Variable

Every projection in this report depends on one variable outside the market’s control: when the FAA certifies the CX300. That event converts 289 firm orders into deliveries and starts the aftermarket clock. Aviation certification history is the best guide to how that timeline typically slips.

FAA type certification for a new aircraft design is a sequence of regulatory processes, each of which must be completed before the next can begin. The sequence for the CX300, under Part 23, begins with acceptance of the certification basis, the set of regulatory standards against which the aircraft will be evaluated, agreed between the FAA and BETA through the Type Certificate Application process. It continues with the development and FAA acceptance of means of compliance documents, the specific tests, analyses, and demonstrations that BETA will use to show compliance with each element of the certification basis.

The Type Inspection Authorization then permits formal FAA-witnessed flight testing on company-conforming aircraft. Upon completion of all required test points and resolution of any open compliance findings, the FAA issues the type certificate. Each stage is sequential; a finding at any stage that requires additional testing or analysis adds time to the overall schedule regardless of the progress made on other compliance items.

BETA’s position in this sequence as of Q1 2026 is advanced: the first conforming aircraft has been built, 85,000-plus hours of engine testing have been completed on the H500A propulsion system, and the company is progressing through the formal compliance demonstration phase. The specific compliance item introducing timeline uncertainty is the continued rotation testing, a certification sub-system test evaluating the aircraft’s behaviour during the rotation phase of takeoff, which is an operationally critical flight phase for a conventional takeoff aircraft operating in high-density, obstacle-constrained environments.

The Q1 2026 earnings call disclosed that BETA and the FAA are in active negotiation regarding the compliance approach for this test sequence. Management characterised this as a normal regulatory dialogue rather than a fundamental disagreement about airworthiness, but acknowledged that the resolution timeline is not fully within BETA’s control.

The significance of this disclosure is its specificity. An active, identified compliance negotiation with the FAA at the sub-system level is a different category of risk from the general ‘regulatory uncertainty’ that investment prospectuses cite as a risk factor in boilerplate language. It is a specific technical and regulatory question whose answer determines whether the TIA flight testing phase can proceed on the current schedule or requires additional testing before the compliance question is resolved. If the FAA accepts BETA’s proposed compliance approach in Q2 or Q3 2026, the continued-rotation compliance item could be resolved without affecting the late 2026 certification target. If the FAA requests additional testing data, the resolution could extend into 2027, compressing the certification window by three to nine months from the current target.

Peer context provides the most useful external calibration for BETA’s certification timeline risk. Joby Aviation completed the first conforming aircraft flight test in early 2026 with 850-plus test flights accumulated, targets commercial operations in 2026, and has experienced certification milestones that arrived later than their original developer guidance, though the magnitude of the delay has remained within approximately one year of original targets. Archer Aviation received 100% means-of-compliance acceptance from the FAA in early 2026 and targets certification ahead of the 2028 Los Angeles Summer Olympics, having similarly experienced timeline extensions from its original 2024 certification guidance.

The pattern across the eVTOL industry, and specifically across the novel aircraft categories that share regulatory characteristics with BETA’s programme, is that certification processes run approximately six to eighteen months longer than developer guidance, primarily because regulatory compliance negotiations at the sub-system level require FAA deliberation time that developers cannot accelerate.

BETA’s Part 23 pathway is structurally simpler than the powered-lift framework that Joby and Archer are navigating, providing a meaningful basis for expecting that BETA’s timeline risk is lower at the framework level. The novel elements in BETA’s Part 23 certification are the electric propulsion system, the battery pack architecture, and the associated power electronics, areas where the FAA has issued Special Conditions to address regulatory gaps in existing Part 23 standards for electrically powered aircraft. These Special Conditions introduce some sub-system compliance complexity even within the otherwise familiar Part 23 process, which is the mechanism by which the continued-rotation testing question has become the current primary compliance focus.

The most important near-term observable for BETA’s investment case is any communication, from BETA, the FAA, or regulatory filings, regarding resolution of the continued-rotation testing compliance negotiation. Resolution within Q2 or Q3 2026 would confirm the late 2026 certification target as achievable. A request for additional testing would shift the base case to H1 2027 and compress the FY2027 revenue outlook accordingly. Investors should treat the absence of negative news as neither confirmation nor denial; aerospace certification compliance negotiations are typically not disclosed until resolved.

The eIPP programme selection announced in March 2026 adds an important dimension to the certification analysis: the programme is designed to enable initial commercial operations under a provisional regulatory framework before full type certification is complete. This means that even if full type certification slips from late 2026 to early 2027, BETA may be able to begin limited revenue-generating aircraft operations in the eIPP corridors in late 2026 under the provisional eIPP authority, providing early commercial operations data and potentially limited aircraft revenue that the current guidance does not reflect.

The eIPP therefore functions as a partial hedge against the binary nature of the certification event, not eliminating the timing risk, but creating a pathway for limited commercial activity to begin in the interval between advanced certification testing and final type certificate issuance.

Certification programme milestones to date

5. The Enabling Technologies Business: Propulsion, Batteries & Aftermarket Economics

The aircraft sale is the entry point. The battery replacement cycle is the thesis. BETA estimates lifetime aftermarket revenue per aircraft at roughly three times the sale price, turning a capital goods business into something closer to a long-duration subscription model.

Battery architecture and replacement economics

BETA’s battery system is a proprietary lithium-ion cell pack designed specifically for aviation applications, where safety, energy density, charge rate, and thermal management requirements are materially different from those of ground-based electric vehicle batteries. Aviation-grade battery packs must pass more stringent safety certification standards than automotive-grade packs, must operate reliably across wider temperature ranges, and must meet structural requirements for airframe integration that add design complexity relative to automotive pack architectures.

BETA’s battery management system (the software and hardware system that monitors cell state, manages charging, balances pack performance, and enforces safety limits during flight) is proprietary and integrated with the aircraft’s flight control system at a depth that would make substitution of a third-party battery pack without BMS modifications a significant engineering and recertification undertaking.

This BMS integration creates the structural basis for the aftermarket captivity that drives the recurring revenue model. An operator seeking to source replacement batteries from a third-party supplier faces two obstacles.

First, the third-party cells must meet the aviation safety standard that the original BMS was designed and tested to manage; any cell with different chemistry, energy density, or thermal characteristics would require BMS modifications and potentially a supplemental type certificate, a costly and time-consuming regulatory process.

Second, the structural integration of the battery pack into the BETA airframe, the mechanical mounting, electrical interfaces, and cooling circuit connections, is designed around BETA’s proprietary pack dimensions and interface specifications, creating a physical constraint on interchangeability.

These two barriers together create a captive aftermarket dynamic analogous to the proprietary consumable model in industrial printing and medical device businesses, where the initial hardware placement establishes a recurring revenue relationship that is difficult for the customer to exit without significant cost and operational disruption.

The estimated 18 to 20 battery replacement sets over an aircraft lifetime, disclosed in BETA’s S-1 prospectus, is an engineering estimate based on the expected charge cycle life of aviation-grade lithium-ion cells at the discharge depths and charge rates that BETA aircraft operations require. At the guided 18-to-20-set replacement cadence and an estimated replacement battery price of $600,000 to $750,000 per set (proprietary estimate based on the implied $13 million lifetime aftermarket figure), the aftermarket revenue per aircraft exceeds the initial aircraft sale price in each of the first several replacement cycles, compounding over the aircraft’s life to an estimated $13 million total.

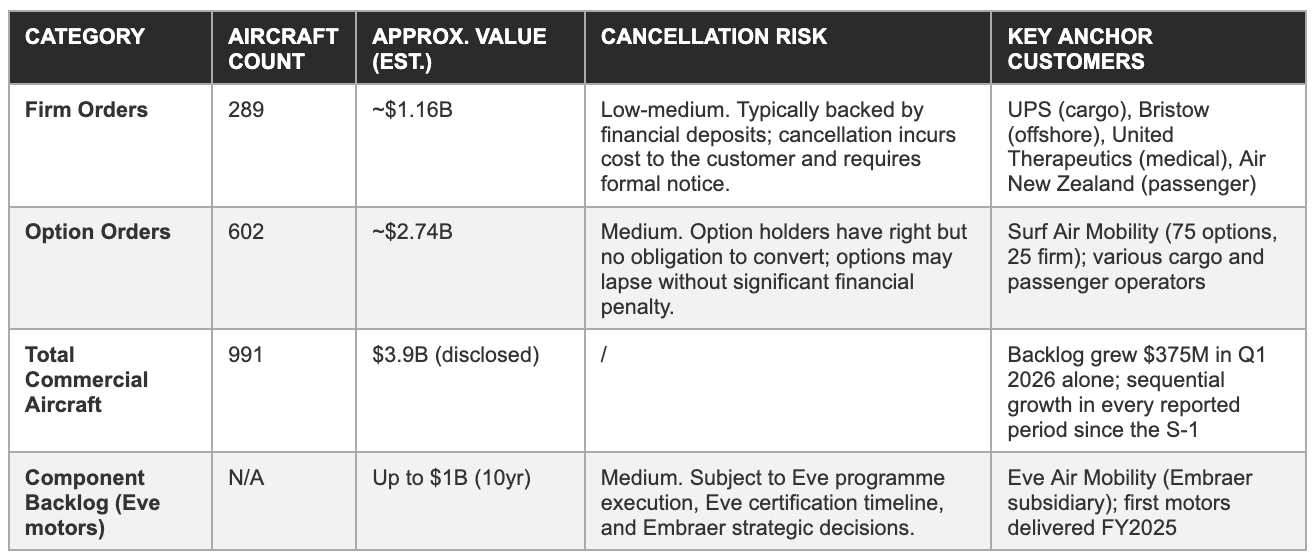

Across 289 firm-order aircraft, the implied future aftermarket revenue opportunity from the confirmed order book alone is approximately $3.75 billion, nearly equal to the entire disclosed commercial backlog value, from deliveries that have not yet occurred and replacement cycles that will not begin until the late 2020s.

Propulsion component supply: The Eve Air Mobility relationship

The Eve Air Mobility pusher motor supply agreement, valued at up to $1 billion over 10 years and disclosed in December 2025, represents the most commercially visible third-party validation of BETA’s propulsion technology. Eve Air Mobility is a subsidiary of Embraer, the third-largest commercial aircraft manufacturer in the world by deliveries.

Eve’s decision to source its pusher motors from BETA rather than from an established aerospace motor supplier, or to develop proprietary motors in-house as several competitors have chosen, is a commercial endorsement that carries more analytical weight than a standard customer order, because Eve had the capability and financial resources to pursue alternatives. The supply agreement covers both conforming prototype aircraft and future production units over the 10-year horizon, creating a revenue relationship that scales with Eve’s programme execution.

The analytical assessment of this revenue stream requires a view not only on BETA’s programme but on Eve’s certification progress and commercial traction, a second-order dependency that introduces execution risk outside BETA’s direct control. The $1 billion aggregate agreement value, even realised over 10 years at approximately $100 million annually at maturity, would represent a revenue stream equivalent to approximately 2.5 times BETA’s total FY2025 revenue from a single component supply relationship, demonstrating the scale of third-party propulsion demand that the enabling technologies platform can address independent of BETA’s own aircraft delivery timeline.

The charging network: Infrastructure moat or capital sink?

The charging network is the most capital-intensive element of BETA’s enabling technologies platform and the element whose commercial logic is most frequently questioned by investors focused on near-term cash consumption. As of Q1 2026, BETA has deployed 123 charging sites globally, including 57 active sites. The network’s commercial logic is most coherently understood as a prerequisite for commercial aircraft operations rather than as a standalone revenue business.

An operator who has purchased BETA aircraft needs to know that charging infrastructure will be available at the destinations its aircraft will serve before it can commit to specific routes and schedules. A deployed network along commercially relevant corridors expands the viable route set for every operator, increasing the commercial utility of the aircraft and therefore the willingness to pay for the initial aircraft purchase.

The Florida Department of Transportation agreement signed in Q1 2026, deploying 34 chargers and thermal management systems across Florida transportation corridors under a public-private cost-sharing structure, is the first disclosed example of a model for reducing BETA’s per-site capital expenditure burden through government infrastructure partnerships. If this model proves replicable across the 26 U.S. states where BETA has eIPP coverage, the total capital expenditure required for BETA’s domestic charging network could be meaningfully reduced relative to a fully proprietary rollout. The per-site capital expenditure reduction would not appear in the near-term income statement but its effect on the cash runway and the timing of network contribution to adjusted EBITDA is material.

Reference comparison: Jet engine aftermarket economics

The closest precedent for BETA’s proprietary aftermarket model in conventional aerospace is the jet engine maintenance, repair, and overhaul business, where manufacturers such as GE Aerospace, Rolls-Royce, and Pratt & Whitney have built multi-decade recurring revenue relationships from engines initially sold at thin or even negative margins. The comparison is useful for sense-checking BETA’s aftermarket assumptions against an established industry pattern, while recognising that the underlying technology and maintenance cycles differ.

The comparison suggests that BETA’s projected aftermarket margin (60 to 70 percent) is materially higher than the conventional jet engine aftermarket margin (25 to 35 percent), reflecting the more direct OEM control over the battery as a sealed, safety-certified unit relative to the broader ecosystem of licensed third-party maintenance providers that has developed around jet engine servicing over decades.

Whether BETA can sustain that wider margin advantage once its installed base reaches a scale comparable to the jet engine MRO market is an open question that the bear case in Section 13 addresses directly. The multiple of lifetime aftermarket revenue to initial sale price (approximately 3x in both cases) is a more durable point of comparison, since it reflects the physical reality of component replacement cycles over an aircraft’s operational life rather than a margin assumption that could compress under competitive or regulatory pressure.

6. Commercial Backlog Analysis: $3.9 Billion - Composition and Cancellation Risk

The $3.9 billion backlog is BETA’s headline figure in every investor communication. It deserves decomposition: firm orders and options carry very different cancellation risk, and the aggregate number treats them as equivalent.

The implied average aircraft price derived from dividing the total backlog value by total aircraft count is approximately $3.93 million per aircraft. Against management’s guided list price of $4 to $4.5 million, this blended figure sits at the lower end of the range, a combination of volume discounts offered to anchor customers who committed early and at scale (UPS, Bristow), a mix effect from cargo-configured aircraft carrying lower price points than passenger-configured variants, and option-related pricing structures where conversion price may be set at the time the option was granted rather than at prevailing list prices.

The distinction between firm orders and options is the most analytically important decomposition of the backlog figure. A firm aircraft order in aerospace is typically backed by a purchase deposit, usually 5 to 10 percent of aircraft purchase price, that the customer forfeits if it cancels. The deposit creates a financial deterrent to cancellation that gives firm orders meaningfully higher conversion probability than options, which typically require no financial commitment beyond the option fee itself. Options in commercial aerospace are routinely used by operators to preserve fleet planning flexibility without full financial exposure, and they are equally routinely allowed to lapse when the operator’s fleet strategy changes or when a competing aircraft better suits its needs at the time of conversion.

The eVTOL industry’s history with option books provides a cautionary reference case. Vertical Aerospace, prior to its 2023 financial restructuring, reported a headline order book of approximately $6 billion including options from Virgin Atlantic, American Airlines, and several other carriers. As certification delays extended and commercial viability came under uncertainty, multiple option holders withdrew commitments.

The lesson for BETA is that option order books in electric aviation should be evaluated with meaningful probability discounts on conversion rate, and that the headline backlog figure overstates the committed delivery pipeline by approximately 60 percent at the firm-order conversion level.

The geographic and end-market diversification of the backlog is one of its most important risk-mitigating characteristics. Medical transport, offshore oil services and logistics, express cargo, regional passenger aviation, and defence represent five distinct demand verticals whose commercial drivers are largely uncorrelated. A disruption to the offshore oil services market that reduces Bristow’s fleet expansion plans would not affect United Therapeutics’ organ transport programme or UPS’s logistics investment. This diversification means that a single commercial or macroeconomic event is unlikely to trigger simultaneous cancellations across the firm order book in the way that a single regulatory or technology event could theoretically affect a less diversified backlog.

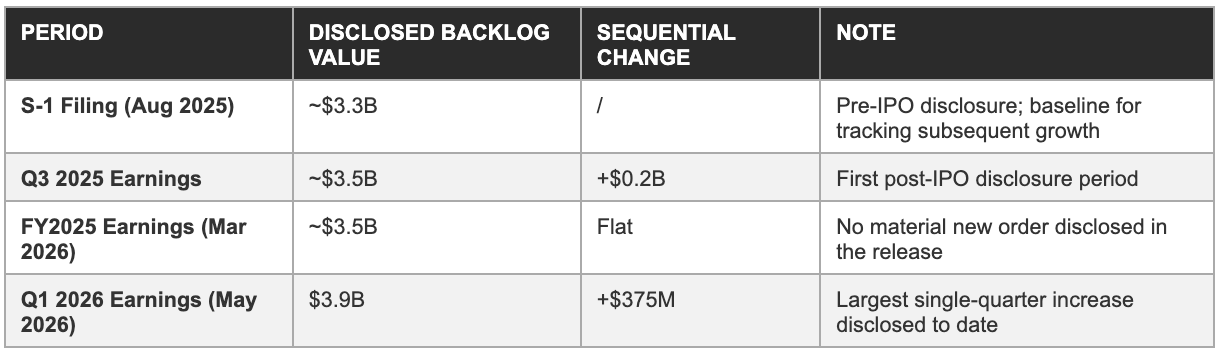

Backlog growth history

The pattern of backlog growth, sequential increases in three of the last four disclosed periods, with no disclosed period showing a net decline, is itself a relevant data point. A backlog that is eroding through cancellations would show declining sequential values even as new orders are announced; the absence of any disclosed decline suggests that, to date, gross new order additions have exceeded any option lapses or cancellations that may have occurred. This does not prove that the backlog is immune to future erosion, particularly if the certification timeline extends materially, but it is the most direct evidence available that the demand side of the investment case has not yet shown signs of deterioration.

Sizing the addressable market independently of the backlog provides a useful sanity check on how much of the total opportunity the current order book represents. The U.S. helicopter fleet engaged in commercial cargo, medical, and offshore logistics roles numbers in the low thousands of aircraft, with average fleet age exceeding 20 years across several of these categories, implying a multi-decade replacement cycle that is already underway independent of electric aviation adoption.

If electric aircraft capture even a modest share of this replacement cycle, alongside genuinely incremental demand from routes that are not economically served by helicopters today due to operating cost, the total addressable aircraft count for BETA’s CX300 and A250 combined plausibly extends into the thousands of units over a 15-to-20-year horizon. Against that backdrop, the current 991-aircraft backlog represents an early but proportionally modest fraction of the total opportunity, which is the structural argument for why backlog growth, rather than backlog absolute size, is the more important variable to track going forward.

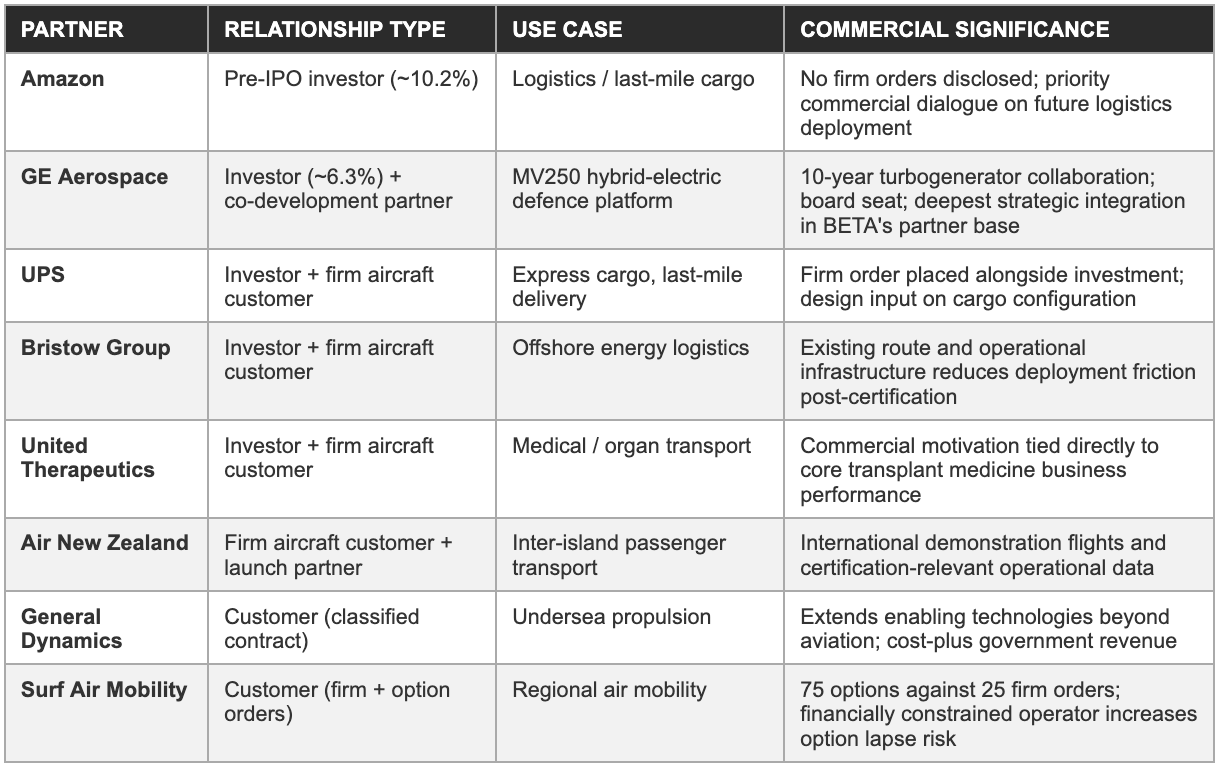

7. Strategic Partnerships & The Investor Ecosystem

Amazon, GE Aerospace, UPS, Bristow, and United Therapeutics are simultaneously investors, customers, and distribution partners. That overlap is unusual for a pre-certification aerospace company and is why BETA’s backlog carries more credibility than a typical speculative order book.

Amazon’s position as a pre-IPO investor through its Climate Pledge Fund reflects a strategic thesis about the long-term economics of last-mile and regional cargo logistics. Amazon’s delivery network includes thousands of daily routes involving time-sensitive cargo movements where helicopters or small fixed-wing aircraft are the current operational solution in urban-dense or geographically constrained markets.

Electric aviation offers potential to reduce operating costs on those routes, BETA has cited estimates of approximately 42 percent lower operating cost per flight hour compared to equivalent conventional aircraft, while improving Amazon’s environmental footprint against its Climate Pledge commitment to net-zero carbon by 2040. Amazon has placed no publicly disclosed firm aircraft orders as of Q1 2026, but the investment creates a priority commercial dialogue positioning BETA as preferred supplier in any future Amazon electric aviation programme.

GE Aerospace’s relationship is structurally the most consequential partnership in BETA’s portfolio. The $300 million equity investment, 10-year co-development agreement for the hybrid turbogenerator, board seat, and warrant package create strategic integration that goes well beyond a financial investment. GE brings propulsion engineering expertise accumulated over a century of jet engine development, military programme management experience across the full lifecycle from development through sustainment, established relationships with FAA certification engineering staff developed across decades of certification programmes, and a global supply chain infrastructure that BETA’s manufacturing organisation can leverage for the MV250 and potentially future civil programmes.

The 10-year co-development agreement is structured as a genuine engineering collaboration with GE engineers embedded in the programme alongside BETA’s design team, creating technical knowledge transfer that benefits BETA’s engineering capability beyond the specific MV250 application.

Bristow Group’s position as both an investor and a firm aircraft customer is analytically significant because of Bristow’s specific operational profile. As the world’s largest provider of offshore energy support helicopter services, operating across the Gulf of Mexico, North Sea, Australia, and several other offshore regions, Bristow faces an economics profile characterised by high fuel costs, demanding maintenance requirements, and multi-jurisdiction regulatory compliance. These are precisely the cost and complexity characteristics that electric aviation is designed to improve.

Bristow’s firm orders for BETA aircraft cover routes where the CX300’s 250-nautical-mile range is operationally viable, and are backed by a commercial motivation independent of speculative market development: Bristow already operates the relevant routes and already has the operational infrastructure to deploy electric aircraft when they become available. The investment and order combination creates alignment that makes Bristow’s commitments among the most credible in the entire backlog.

United Therapeutics represents a demand category, organ transport, whose operational requirements align with BETA’s aircraft capabilities in a way that removes most commercial risk from the order. Organ transplant logistics require rapid, reliable transport of human organs across routes that often cannot be served by scheduled commercial aviation within the time constraints imposed by organ viability windows. Current solutions involve helicopter charters, small fixed-wing aircraft, and a complex coordination system that is costly and unreliable.

BETA’s aircraft, operating at 150 to 170 miles per hour with under one hour recharge time, can serve most major organ transport corridors in the continental U.S. within viability windows for the most commonly transplanted organs. United Therapeutics, which owns a significant portfolio of transplant medicine businesses, has a direct commercial incentive to invest in and deploy BETA aircraft: faster, more reliable organ transport improves transplant outcomes, which is the primary value driver for its transplant medicine portfolio.

Air New Zealand’s relationship extends beyond a simple aircraft order. The airline selected the ALIA CX300 as the launch platform for its Mission NextGen Aircraft programme, targeting inter-island commercial passenger routes. BETA shipped an ALIA aircraft to New Zealand in late 2025 for demonstration flights, has since conducted customer flights there, and is establishing the ground charging infrastructure required for commercial inter-island operations.

New Zealand was identified as a natural launch market due to its compact inter-island geography, high domestic fuel costs relative to U.S. averages, and a regulatory environment historically receptive to novel transportation technologies. The international operational data generated by these flights, covering performance in Tasman Sea weather conditions, contributes to the certification evidence base and demonstrates commercial operability in a non-U.S. regulatory context that strengthens BETA’s international commercial credibility.

Key relationship summary

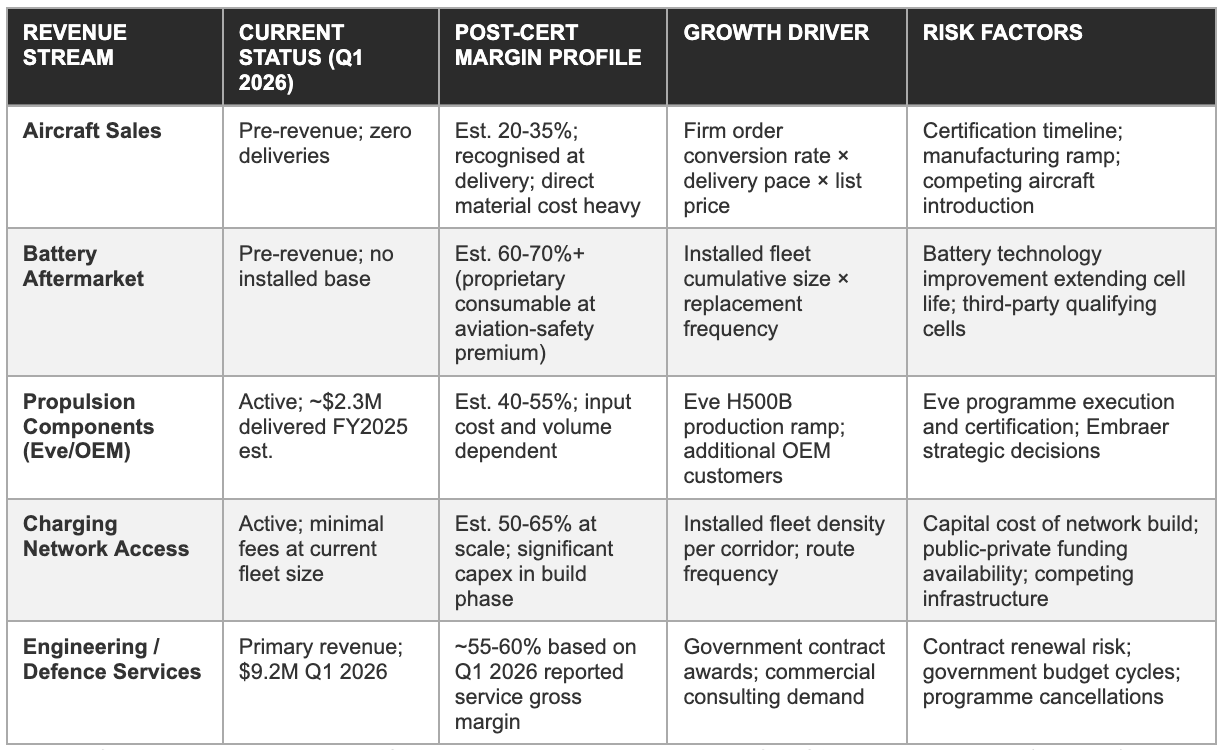

8. Business Model Architecture & Revenue Stream Economics

BETA must transition from services revenue to a four-stream product model, aircraft, aftermarket, components, and charging access, each with different margins and different dependence on certification. Understanding that sequencing matters more than the current income statement.

The revenue transition from services to products is the central financial event in BETA’s investment horizon. Engineering services revenue, the category generating all of BETA’s meaningful current income, is labour-intensive and contract-bound, scaling with headcount and contract scope rather than with the multiplicative economics of a product business. The engineering services margin of approximately 55 to 60 percent at the gross level (implied by Q1 2026 service revenue of $9.2 million against the reported gross margin of 57.6%) is healthy, but the absolute gross profit generated on $35 to $40 million of annual services revenue, approximately $19 to $24 million, is wholly inadequate to absorb the R&D and G&A expense base that the certification and MV250 programmes require. The business model cannot reach profitability through services revenue growth alone.

Aircraft sales will generate the largest individual revenue events but at the lowest margins in the product portfolio. At an estimated $4 million list price and 25 percent gross margin, each aircraft sale generates approximately $1 million of gross profit, a meaningful contribution at volume but a modest fraction of the $17 million lifetime revenue relationship that the same aircraft represents when the aftermarket is included. The aircraft sale is therefore best understood as the customer acquisition event for a multi-decade recurring revenue relationship, not as the primary value generator in the model.

Battery replacement, at the estimated 60 to 70 percent gross margin, is the primary driver of the long-term gross margin thesis. At approximately $600,000 to $750,000 per replacement set, each replacement cycle generates gross profit of approximately $360,000 to $525,000. Across 18 to 20 replacement cycles, the cumulative aftermarket gross profit per aircraft is estimated at approximately $7 to $10 million, exceeding the gross profit from the initial aircraft sale by a factor of seven to ten. The installed base has a compounding characteristic: each delivered aircraft creates a recurring gross profit stream that continues for the aircraft’s operational life, and the aggregate recurring gross profit grows with each new delivery cohort without requiring additional sales force investment or new customer acquisition effort.

The charging network access fee model carries the most uncertain economics at the current development stage, because access fee structures in electric aviation infrastructure have not yet been established in commercial practice at meaningful scale. The relevant analogies from other infrastructure businesses, EV charging networks, airport fueling systems, suggest that access fee revenue at commercial scale could generate gross margins of 50 to 65 percent once the network reaches utilisation levels allowing fixed infrastructure costs to be spread across sufficient volume. Both fleet scale and network density must reach threshold levels simultaneously before this margin profile activates; the eIPP programme and public-private infrastructure partnerships are the primary mechanisms for compressing the timeline to that threshold.

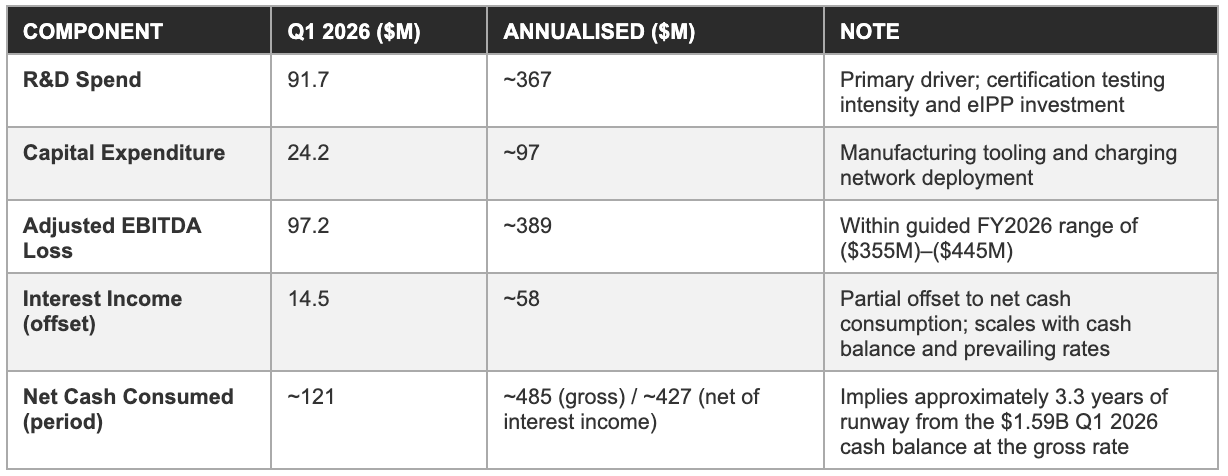

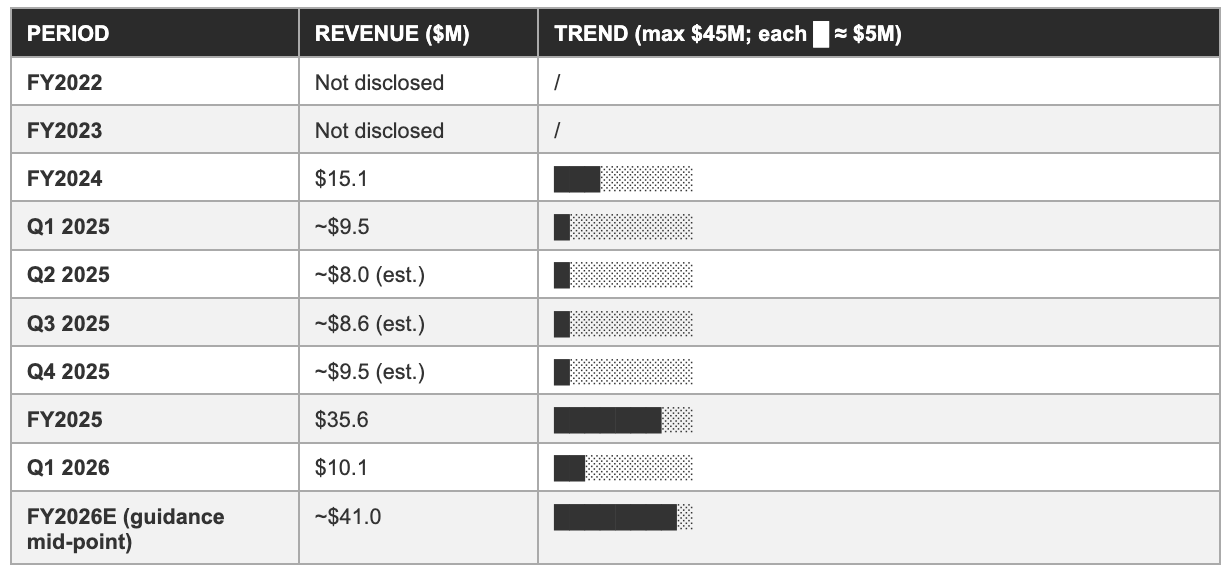

9. Financial History & The Loss Trajectory

The losses are the expected cost of building a long-duration aerospace asset base, not a sign of failure. The real question is whether the assets justify the spend and whether the cash on hand lasts until revenue arrives.

Cash burn composition - Q1 2026

Revenue trend: Visual comparison

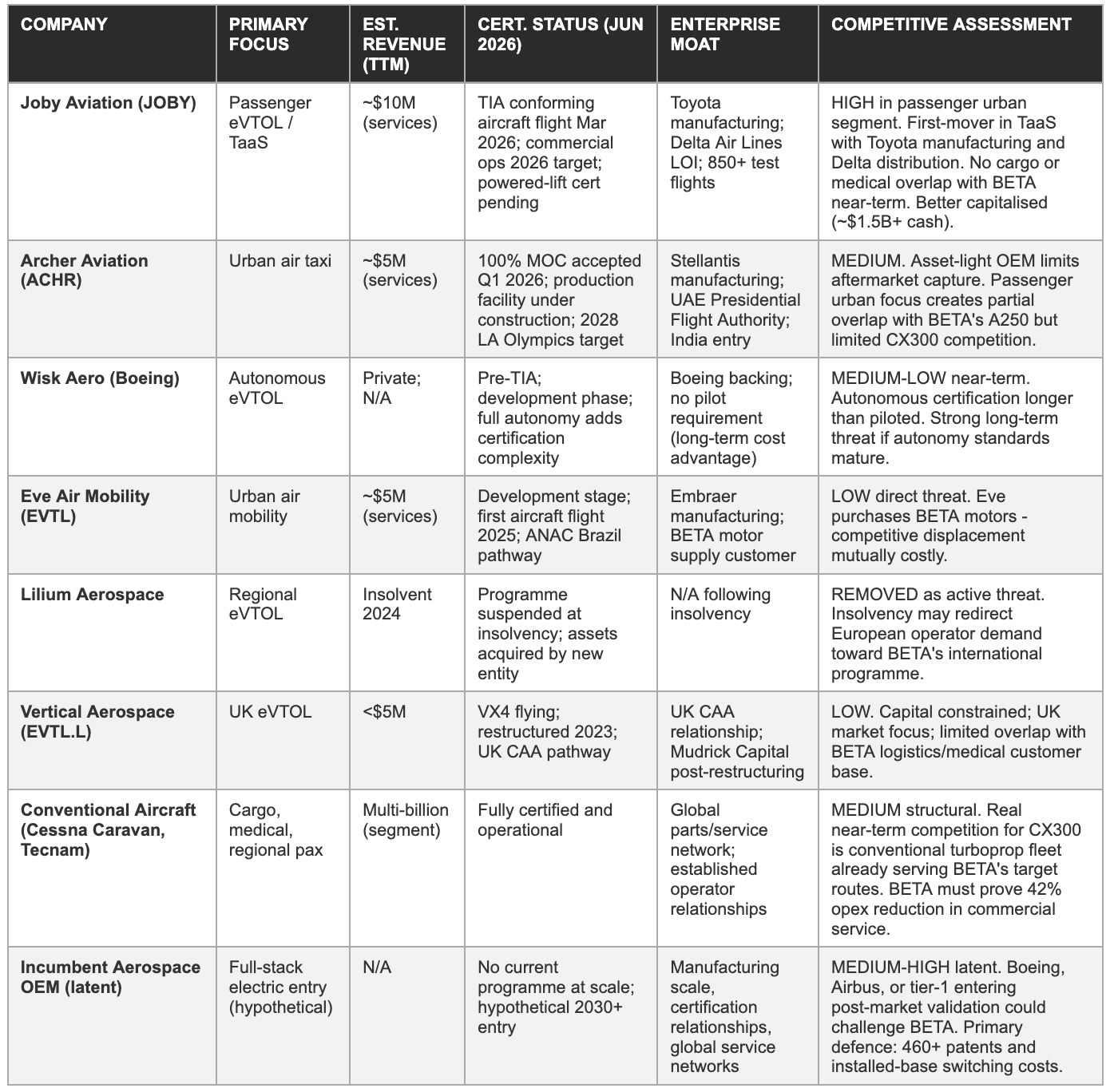

10. Competitive Landscape

The eVTOL sector has sorted into survivors and casualties since 2024. BETA’s edge is its eCTOL-first certification strategy and its aftermarket architecture, distinctions easy to miss when comparing companies on flight-hour claims alone.

BETA’s differentiated position within this competitive landscape rests on four observable characteristics.

First, the eCTOL-first Part 23 certification strategy positions the CX300 to receive type certification earlier than any purpose-built eVTOL competitor because the regulatory pathway has fewer unresolved technical standards and longer institutional precedent.

Second, the vertical integration of batteries, motors, flight controls, and charging infrastructure creates an aftermarket revenue capture opportunity that no pure-OEM competitor has replicated.

Third, the customer base concentrated in cargo, medical, and logistics applications means BETA’s commercial success is less dependent on vertiport infrastructure development, public consumer adoption, and urban air traffic management maturation.

Fourth, the GE Aerospace partnership provides access to defence procurement channels and hybrid propulsion technology that distinguishes BETA from every other eVTOL developer without a comparable tier-1 aerospace partner.

The structural threat commanding most caution over a five-to-ten year horizon is from aerospace incumbents choosing to enter electric aviation after early developers have absorbed the regulatory development cost and demonstrated commercial viability. Boeing, Airbus, Textron Aviation, and their tier-1 supplier ecosystems possess manufacturing scale, FAA certification relationships, global service networks, and balance sheets that dwarf any current eVTOL developer.

BETA’s 460-plus patent portfolio and first-mover customer relationships are the primary structural defences, but patents expire and design-arounds are standard competitive strategy. The window during which BETA’s first-mover position translates into structural market leadership, rather than temporary incumbency that incumbents subsequently challenge, is the most uncertain long-horizon variable in the investment case.

11. The eIPP Programme: Government as Commercial Catalyst

BETA’s selection in seven of eight eIPP programmes is the most significant development since the GE partnership, and the one investors most often dismiss as government risk rather than commercial acceleration.

The eVTOL Integration Pilot Program was announced by the U.S. Department of Transportation and the FAA in March 2026, implementing the executive orders on advanced air mobility and drone dominance signed early in the Trump administration. The programme is designed to accelerate commercial eVTOL deployment by establishing federally sanctioned operating corridors, providing co-funding for ground infrastructure, establishing regulatory precedents for commercial operations under FAA oversight, and building the political and public-acceptance groundwork for multi-state commercial launches.

The eight initial programmes span diverse geographies and use cases, from the New York/New Jersey metropolitan corridor covering passenger operations to Texas DOT multi-city regional cargo links, North Carolina medical operations, Florida commuter routes, and Pacific Northwest logistics applications.

BETA’s selection reflects both BETA’s geographic diversity of customer commitments and its operational capability across a broader range of mission profiles. Cargo, medical, offshore logistics, and passenger operations are represented across BETA’s seven eIPP selections, each served by a different customer partner who provides the operational infrastructure the eIPP requires. This breadth positions BETA as the de facto lead platform developer for the eIPP programme, a status commercially valuable beyond the immediate infrastructure co-investment, as it establishes BETA’s aircraft, charging equipment, and operational protocols as the default reference standard against which future eIPP expansions and commercial deployment frameworks will be evaluated.

The $50 million incremental investment that BETA is absorbing in 2026 to participate in eIPP programmes covers the engineering labour, aircraft-specific modifications for eIPP operational requirements, and preliminary infrastructure deployment required to support eIPP operations that are expected to begin after aircraft certification is received. Management disclosed this incremental cost alongside the guidance revision, characterising the decision to absorb it as reflecting conviction that the commercial acceleration value exceeds the near-term cash cost.

That characterisation is a management assertion whose value will only be observable in the revenue and market share outcomes following 2026, but the eIPP selections represent a government-validated endorsement of BETA’s operational readiness across seven use cases and geographic markets, an endorsement carrying procurement signalling value in commercial customer conversations beyond the direct eIPP programmes.

The Florida Department of Transportation agreement signed in Q1 2026 is the most concrete evidence of the public-private cost-sharing model that the eIPP enables. BETA will deploy 34 chargers and thermal management systems across Florida corridors, with the Florida DOT contributing land rights, permitting support, and co-investment in infrastructure. If this model proves replicable across 26 U.S. states with eIPP coverage, the total capital expenditure required for BETA’s domestic charging network could be reduced by 30 to 50 percent relative to a fully proprietary rollout. That cost reduction manifests in a lower capex requirement over the 2027-to-2030 build period, invisible in near-term income statements but material to the cash runway and the timing of network contribution to adjusted EBITDA.

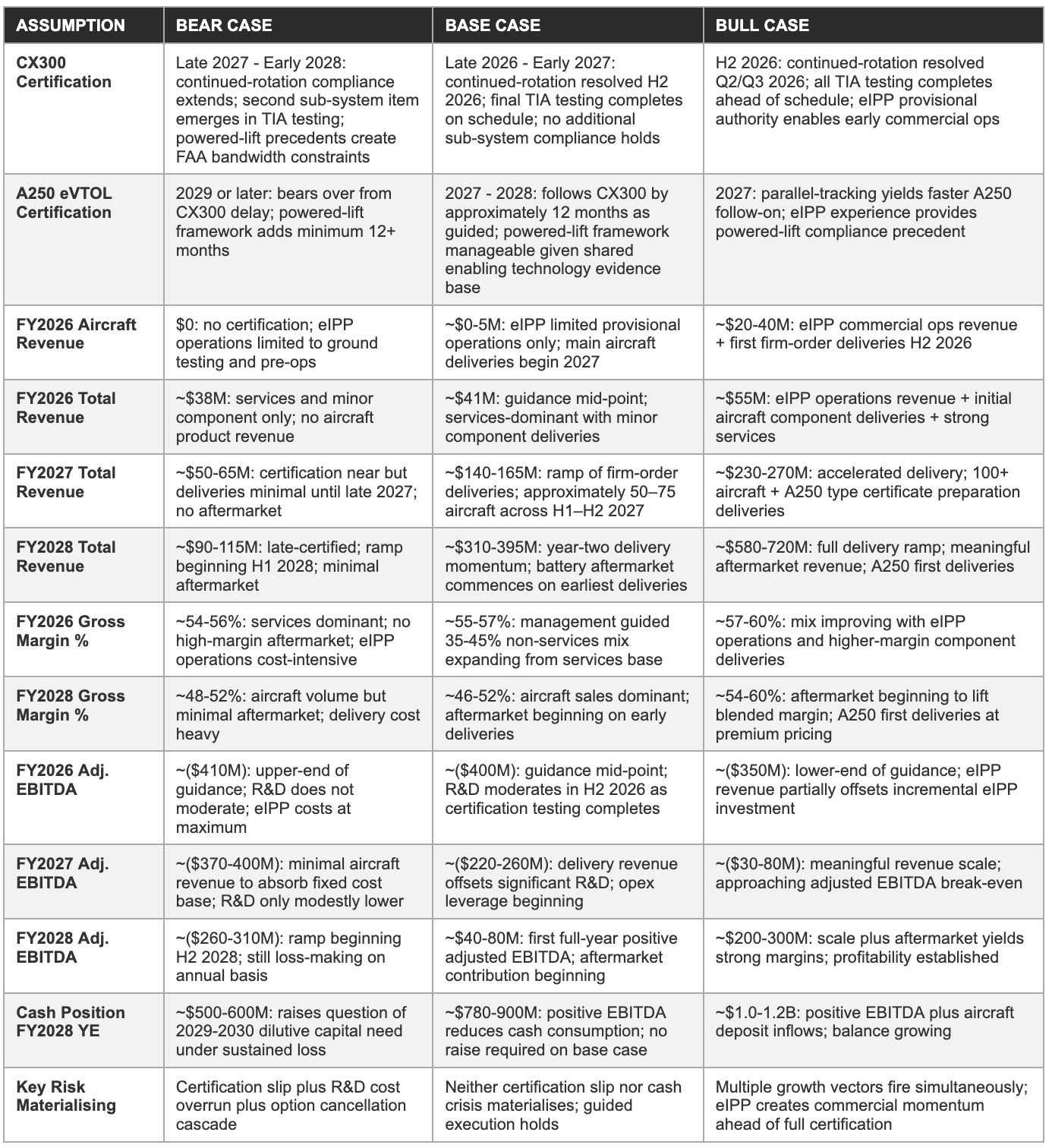

12. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios are anchored entirely on certification timing. Bear: a slip to 2027-28 with cash becoming the central risk. Base: certification late 2026/early 2027. Bull: H2 2026 with eIPP revenue arriving early. Every assumption is stated explicitly.

Model assumptions

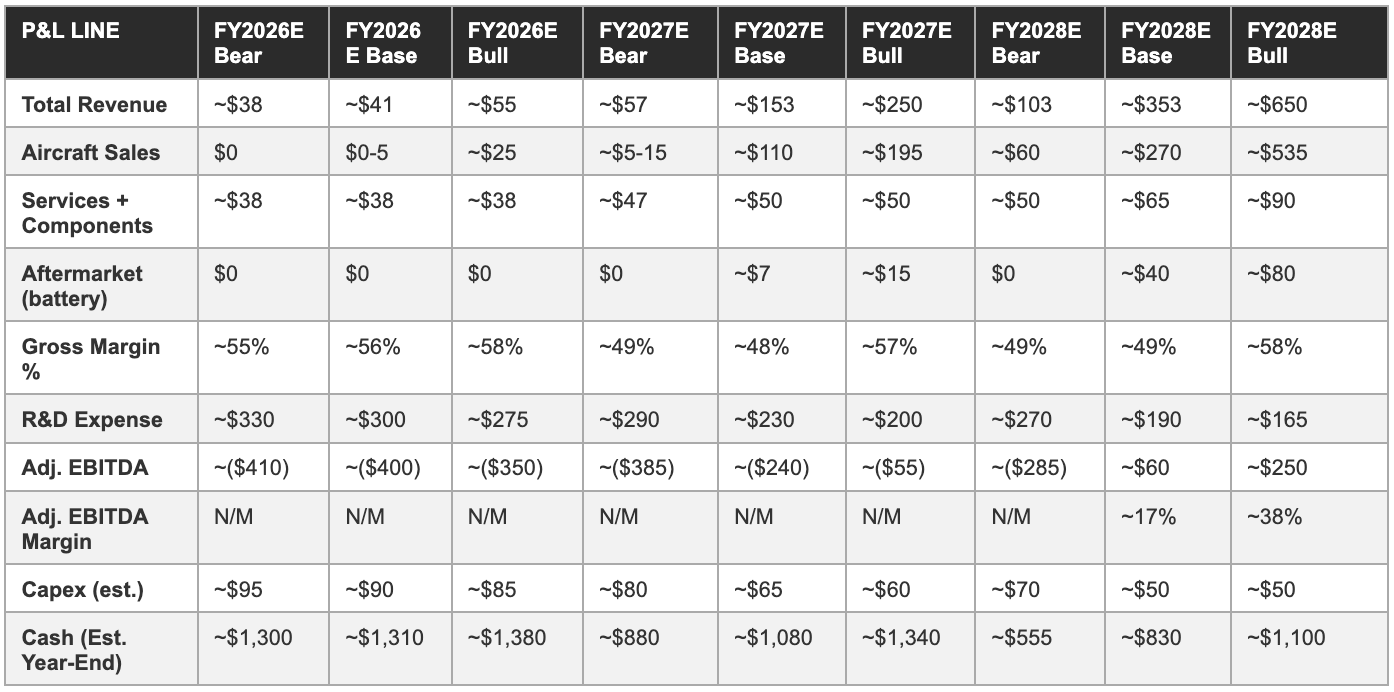

Three-year P&L projection

The bear case cash position of approximately $555 million by FY2028 year-end is the most important near-term financial risk signal to monitor. A cash position below $600 million entering FY2029 under the bear case would likely trigger a market expectation of dilutive equity issuance, which could occur at valuations materially below the current trading range if certification remains unresolved and commercial revenue is still minimal. The combined cash position and $185 million notes payable would create financial pressure that the current investment case does not reflect. The distinction between the bear and base case is therefore not only a revenue and margin outcome difference, it is a capital structure outcome difference with binary characteristics for shareholder returns.

The base case revenue of approximately $353 million in FY2028 at a 49 percent gross margin and approximately $60 million adjusted EBITDA implies that the income statement has crossed into profitability territory but has not yet generated sufficient EBITDA scale to drive significant multiple expansion from the current enterprise value. At a 15x EV/EBITDA multiple applied to $60 million of base case FY2028 EBITDA, the implied enterprise value is $900 million, below the current EV range of approximately $2.1 to $2.6 billion. This confirms that the current valuation prices in execution beyond the base case, or requires a longer-duration discounted cash flow framework capturing the aftermarket’s compounding revenue contribution through 2035 and beyond. Investors who cannot or will not hold across that extended horizon face genuine multiple compression risk even under base case execution.

The bull case’s FY2028 revenue of approximately $650 million at a 38 percent adjusted EBITDA margin implies approximately $250 million of adjusted EBITDA. At a 15x EV/EBITDA multiple, the implied enterprise value is approximately $3.75 billion, or a market capitalisation of approximately $5.3 billion after adding back the estimated cash balance of approximately $1.1 billion and deducting the $185 million notes payable. Against a current market capitalisation estimated in the $3.7-to-$4.2 billion range, the bull case delivers meaningful but not dramatic upside from current levels on this particular valuation methodology.

The transformative long-duration value creation, driven by the aftermarket’s compounding effect on an installed base that grows with every delivery cohort, materialises over a decade-plus horizon that conventional equity market valuation frameworks struggle to price efficiently, which is precisely why the current multiple appears to offer asymmetric upside to investors with the holding period required.

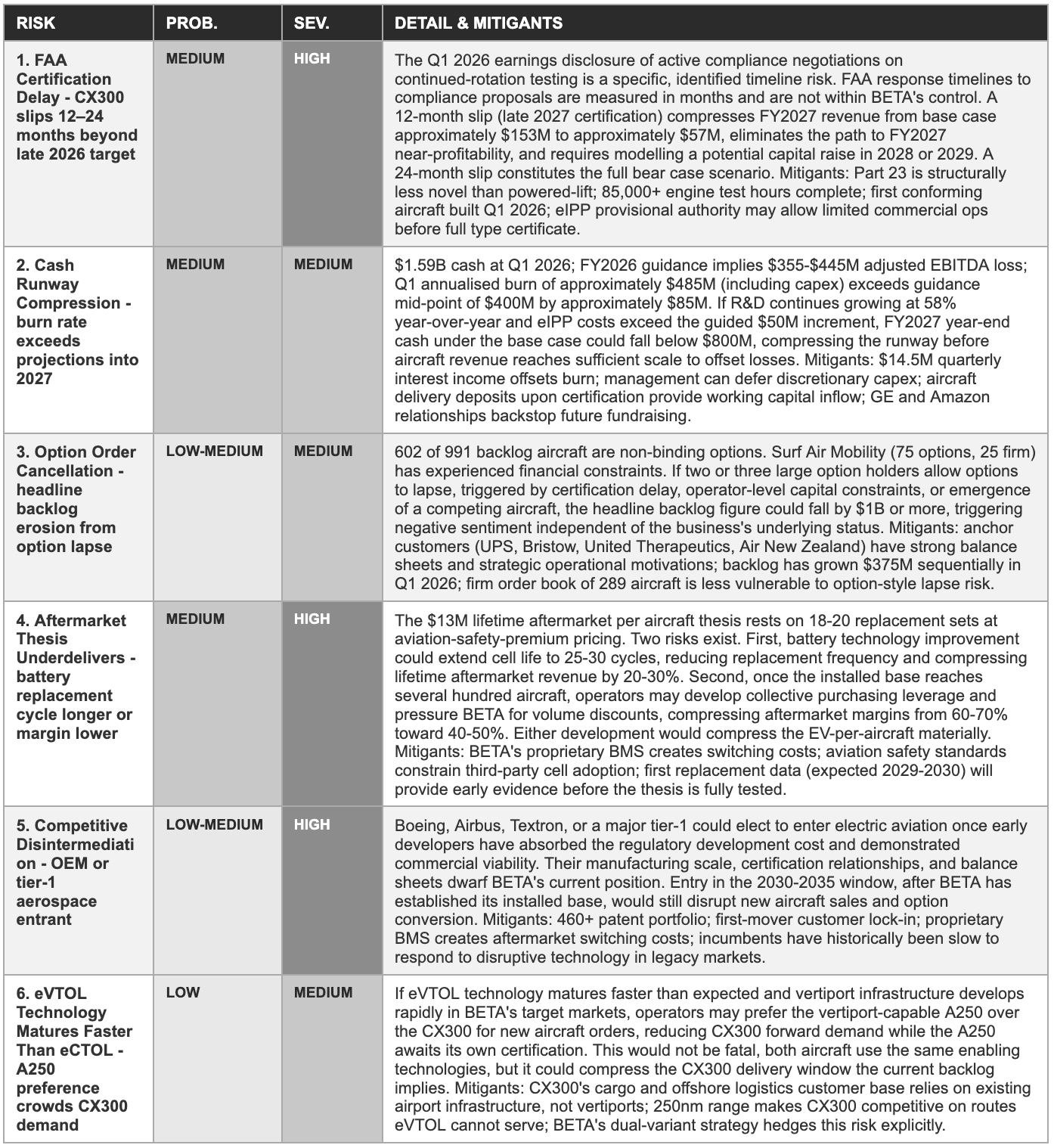

13. Risk Matrix

Six risks are assessed below, each a variable that determines which scenario plays out. Probability reflects likelihood within 24 months; severity reflects long-term damage if it materialises.

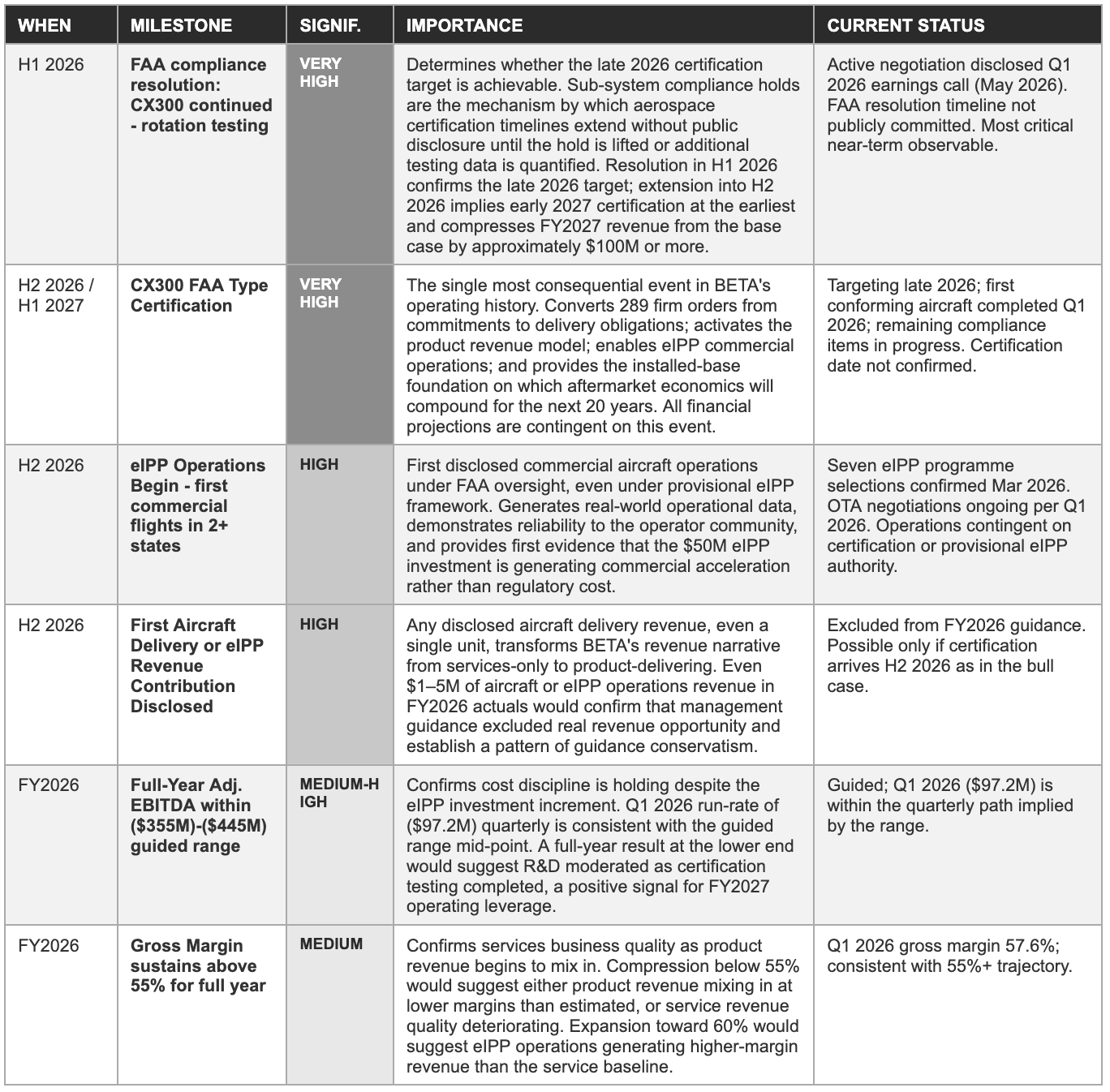

14. Milestone Tracker: What to Watch Through 2028

Twelve observable proof points across 2026-28. Two matter more than the rest: the FAA’s compliance resolution on continued-rotation testing, and the certification date itself.

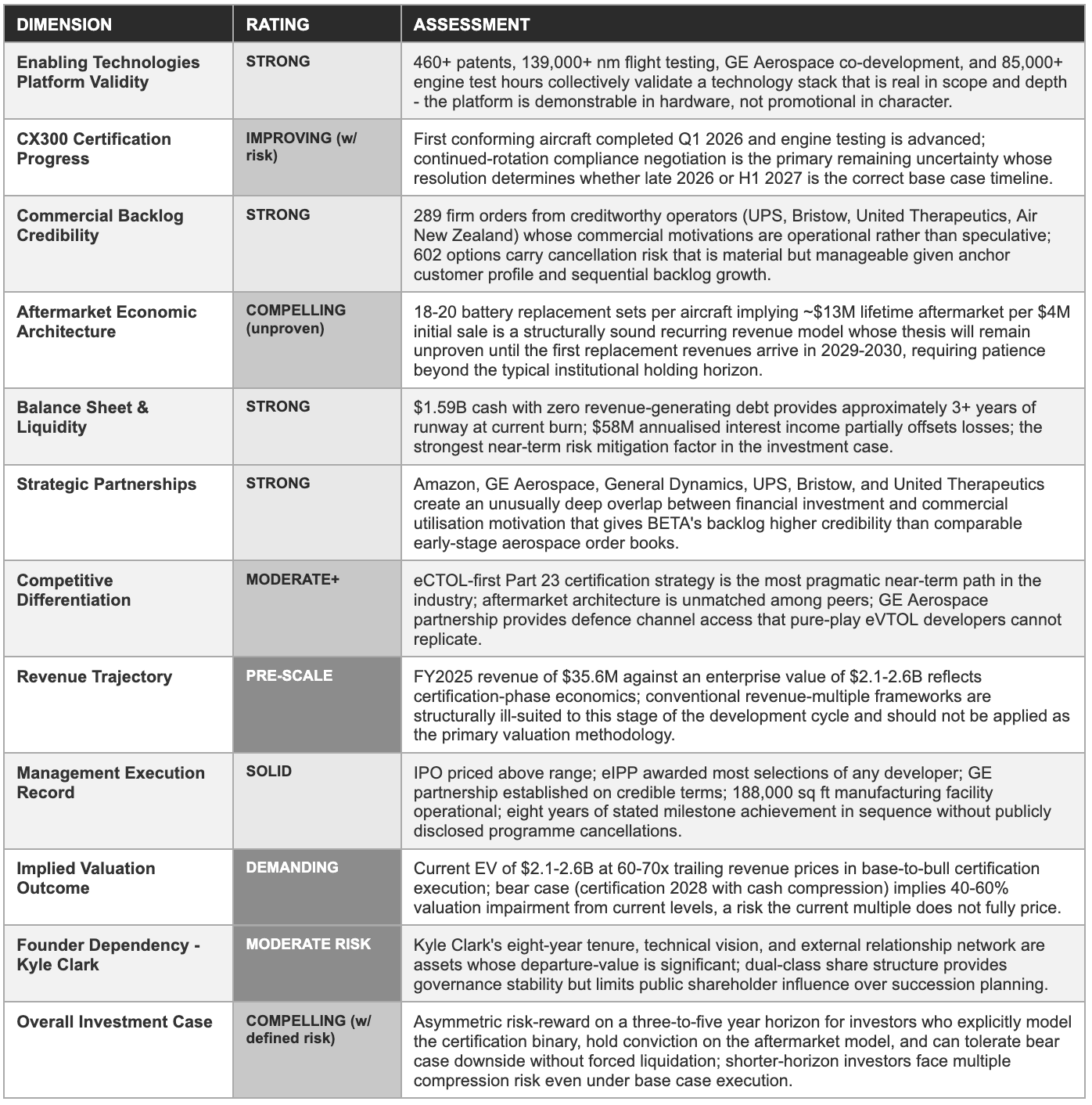

15. Investment Scorecard & Opinion

The technology, capital position, and demand validation are stronger than the valuation’s skepticism suggests, but the case hinges on one unresolved, time-bound event. The scorecard below summarises twelve dimensions; the bull and bear cases get equal weight in the analysis that follows.

The bull case: Four pillars

The first pillar is the demonstrable technology. Eight years and approximately $1.7 billion of private capital have produced a technology stack that is observable in hardware: 460-plus issued patents, an aircraft that has flown 139,000 nautical miles across multiple international jurisdictions under varied weather and operational conditions, a manufacturing facility producing conforming aircraft against an active certification programme, and a propulsion motor that passed FAA Part 35 type certification for electric aircraft, a first in U.S. aviation history. These are documented milestones against which the investment thesis can be measured. The technology stack is real, defensible via the patent portfolio, and represents a foundation that no well-funded competitor could replicate in under five years from the day it decided to try.

The second pillar is the demand structure. The $3.9 billion backlog across cargo, medical, offshore logistics, defence, and passenger applications is supported by customers whose motivations for electric aviation adoption are operational rather than speculative. UPS needs to reduce the cost and environmental impact of time-sensitive short-haul deliveries. Bristow needs to reduce the operating cost of offshore personnel and cargo transport. United Therapeutics needs to accelerate organ transport where ground and conventional air options are time-constrained. Air New Zealand needs to electrify inter-island routes where fuel costs represent a disproportionate share of operating expenses.

Each motivation is independent of BETA’s stock price, independent of the broader eVTOL sector narrative, and durable across the certification timeline regardless of its specific date. The 289 firm orders backed by these motivations will convert to delivery obligations upon certification because the underlying operational need that generated the order persists through the certification period.

The third pillar is the aftermarket architecture. The combination of a proprietary battery management system, a charging network that BETA deploys and controls, and a patent portfolio covering the enabling technologies across the full stack creates a recurring revenue model whose long-duration economics dwarf the initial aircraft sale in present value terms. At the estimated $13 million lifetime aftermarket per aircraft, the 289 firm-order aircraft represent a future aftermarket revenue opportunity of approximately $3.75 billion from deliveries that have not yet occurred. The compounding nature of installed base economics means that every delivery cohort adds to the recurring revenue base without requiring new customer acquisition, creating a flywheel dynamic that strengthens the business model with each passing year of the post-certification commercial phase.

The fourth pillar is the balance sheet. BETA holds $1.59 billion in cash with $185 million in notes payable, generating $58 million in annualised interest income, and has no revenue-generating debt. In an industry where competitor solvency is a genuine concern, BETA’s capitalisation is a competitive asset in enterprise customer conversations. An operator evaluating a long-term fleet commitment needs confidence that the manufacturer will still be in business to provide battery replacements, software updates, and maintenance support in year five, year ten, and year fifteen. BETA’s balance sheet provides that confidence in a way that a competitor with twelve months of runway cannot match, and it functions as a procurement differentiator in exactly the customer segments where BETA is competing for firm orders.

The bear case: Three concerns

The first and most acute concern is certification delay. The continued-rotation testing compliance negotiation disclosed in Q1 2026 is a specific, identified risk item, not a vague concern about regulatory complexity, whose resolution timeline is not within BETA’s control. The FAA’s response time to a compliance proposal is governed by the agency’s internal processes, its workload at a time when multiple novel aircraft programmes are simultaneously in active certification, and the technical complexity of the specific compliance question being addressed.

A request for additional test data from the FAA in response to BETA’s compliance submission could extend the negotiation by three to six months, pushing the expected certification date from late 2026 into mid-2027. A further complication could extend the timeline further. Multiple eVTOL developers with fewer active sub-system compliance items than BETA currently has have experienced certification slips of 12 to 24 months from their publicly guided timelines, and the pattern is consistent enough across the industry to warrant material probability weighting rather than dismissal as a tail risk.

The second concern is that the aftermarket thesis is structurally unverifiable for three to four years after any plausible certification date. The first battery replacement cycles for the earliest delivered aircraft will not begin until 2029 at the earliest under the bull case, and 2030 or later under the base case. During this interval, the $13 million lifetime aftermarket per aircraft estimate is a model input rather than an observable financial fact.

If battery technology improves faster than the current degradation curve implies the replacement frequency could fall materially below the 18-to-20-cycle estimate without investors having any data to signal the revision. This structural uncertainty means that the most important economic variable in the business model will be unprovable for years after the investment decision is made. Investors requiring demonstrated revenue evidence for every major model assumption before committing capital will find the aftermarket thesis permanently unsatisfying until 2030.

The third concern is the long-duration nature of the investment cycle relative to conventional institutional holding periods. BETA raised approximately $1.7 billion in private capital over eight years, and an additional $1.02 billion in its IPO, for a total capital raise of approximately $2.72 billion against FY2025 revenue of $35.6 million. The capital efficiency ratio of approximately $76 of capital raised per dollar of current annual revenue is not the metric of a traditional value investment, it is the metric of an infrastructure company whose assets generate revenue over decades rather than quarters. Investors who evaluate BETA against conventional capital efficiency screens will find it fails consistently, and there is no short-duration catalyst that will resolve that appearance within one to two years.

The investment requires genuine conviction that the aftermarket model will generate the revenue and margin profile the architecture implies, sustained across a holding period that most institutional mandates are not structurally positioned to maintain. That institutional constraint is as much a risk to the investment as any of the operational variables, because forced liquidation at an inopportune point in the certification cycle can impose realised losses even when the underlying business is executing correctly.

The bottom line

BETA occupies a position in electric aviation that is differentiated from every other publicly listed developer, and that differentiation is grounded in demonstrable assets rather than aspirational claims. The aircraft flies across 139,000 nautical miles and four international jurisdictions. The manufacturing facility produces conforming hardware against an active certification programme. The backlog represents demand from creditworthy operators with genuine operational motivations that persist independent of the stock price. The GE Aerospace partnership provides strategic depth that a capital raise alone could not purchase. The patent portfolio defends the enabling technologies against competitive replication with a protection horizon extending to 2040. The balance sheet provides the runway required to reach the certification event that activates the revenue model.

The asymmetric observation is that the three-to-five year expected value of the investment, probability-weighted across the bear, base, and bull scenarios, is positive for investors who can maintain their position through the certification uncertainty period without forced liquidation. The companies that generated the largest returns in aerospace investing history, including in the commercial jet transition of the 1950s and 1960s, the turboprop commuter revolution of the 1980s, and the regional jet development of the 1990s, were typically held through exactly the kind of certification-and-early-commercial-phase uncertainty that BETA currently inhabits.

The analogy is imperfect, the enabling technologies model is genuinely novel, the aftermarket thesis is unproven, and the regulatory environment for electric aviation is still being established, but the structural pattern of patient capital being rewarded in aerospace technology transitions is the most relevant historical reference for assessing the probability that BETA’s investment case delivers across the appropriate time horizon.

The two highest-stakes near-term observables: (1) any FAA or BETA communication resolving or extending the continued-rotation testing compliance negotiation, this determines whether late 2026 certification is achievable or must be re-guided; (2) FY2026 Q3 earnings call disclosure of any first aircraft delivery revenue or eIPP operations contribution. All other milestones are secondary until these two data points are resolved.

Sources

This report draws on the following publicly available materials: BETA Technologies Q1 2026 earnings release (May 2026); FY2025 full-year earnings release (March 2026); Q3 2025 earnings release (November 2025); S-1 registration statement and prospectus filed in connection with the November 2025 IPO; BETA company press releases covering the GE Aerospace partnership and co-development agreement, the Eve Air Mobility motor supply agreement, the Florida Department of Transportation charging agreement, and the eVTOL Integration Pilot Program selection announcement (March 2026); U.S. Department of Transportation and FAA public materials on the eIPP programme; PitchBook data on share count and private financing history; Stockanalysis.com analyst consensus and price target data (June 2026); company investor presentation materials accompanying the Q1 2026 and FY2025 earnings calls; and trade press coverage from The Air Current, Aviation Week, and FlyingMag used for competitive landscape and peer certification status context.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Beta Technologies, Inc. (NYSE: BETA) or any other security. All information is sourced from publicly available materials believed to be reliable as of June, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.