CENTRUS ENERGY

From Broker to Builder: The Domestic Enrichment Wager, the 2028 Supply Cliff, and Whether the American Centrifuge Programme Can Execute Before the Policy Window Closes

1. Corporate Profile & The National Security Trade

Centrus Energy is a nuclear fuel supplier generating approximately $450 million in annual revenue from a business in structural transition. Today it earns income by brokering Russian and French-enriched uranium to U.S. utilities under contracts that expire in 2028. Tomorrow it intends to become the first U.S.-owned domestic uranium enricher to operate at commercial scale since the federal gaseous diffusion programme was shut down in 2013. The investment case concerns whether an industrial reconstruction programme of a kind not attempted in the United States in more than a generation can be financed and executed before the policy window that created the demand closes.

The company operates through two segments with fundamentally different economics.

The Low-Enriched Uranium segment purchases separative work units from TENEX, the commercial subsidiary of Russia’s Rosatom state nuclear corporation, and from Orano, the French state-affiliated nuclear group, and resells enriched uranium hexafluoride to commercial utilities across the United States, Europe, and Asia.

The Technical Solutions segment operates the American Centrifuge Plant demonstration cascade in Piketon, Ohio, under contract with the U.S. Department of Energy, producing High-Assay Low-Enriched Uranium for government research, development, and national security applications.

The national security framing of the investment case is substantive rather than marketing language. In February 2026, the National Nuclear Security Administration, the DOE component responsible for maintaining and modernising the U.S. nuclear weapons stockpile, notified Centrus of its intent to sole-source certain uranium enrichment activities from the company without competitive bidding. Sole-source notifications are issued when the procuring agency has determined that only one responsible source exists capable of satisfying the requirement at the required specification and timeline.

The NNSA notification is therefore simultaneously a statement of Centrus’s unique operational capability and a confirmation that the national security enrichment requirement is sufficiently urgent and specialised that the standard competitive procurement process would not produce an adequate result. The notification has not yet converted into a specific funded contract, but it indicates that addressable government revenue is broader than the $900 million commercial HALEU task order and extends into classified programme work that cannot be publicly dimensioned.

Centrus occupies the highest barrier-to-entry stage of the nuclear fuel cycle, uranium enrichment, and holds a regulatory and operational monopoly on HALEU production in the United States. The investment question is whether a company with a forty-year development history and one bankruptcy on the same programme can execute the commercial build that the current policy environment is requiring, on a timeline that does not outlast the financial buffer the balance sheet provides.

2. The USEC Origin: Bankruptcy, Reinvention, and the Weight of Institutional History

Centrus is attempting to execute the same industrial programme that its predecessor failed to complete over two decades of effort. The American Centrifuge absorbed more than a billion dollars in combined federal and private capital under USEC without reaching commercial scale. Understanding why USEC failed is required to assess whether the conditions producing the failure have changed sufficiently, and whether the management team and capital structure now executing the programme are genuinely different in the ways that matter most.

The United States Enrichment Corporation was created in 1992 under the Energy Policy Act as a government-owned entity to manage the federal government’s uranium enrichment capacity. The two gaseous diffusion plants it operated had been built during the Cold War and were consuming electricity at three to four times the rate of the modern gas centrifuge enrichment technology deployed by Urenco in Europe and TENEX in Russia.

The privatisation thesis was that private capital and management discipline could modernise the enrichment infrastructure and retain a domestic U.S. enrichment capability against growing competitive pressure from allied and Russian centrifuge operators who could produce SWU at a fraction of the electricity cost that gaseous diffusion required.

The structural problem USEC could not resolve was the cost disadvantage inherent in gaseous diffusion technology. The Paducah plant consumed approximately 3,000 kilowatt-hours of electricity per SWU; modern centrifuge enrichment consumes approximately 50 kilowatt-hours per SWU. At U.S. industrial electricity prices, this differential made domestic gaseous diffusion production cost uncompetitive against both Urenco and TENEX, which were simultaneously expanding centrifuge capacity and contracting with U.S. utilities at prices USEC could not match from its production cost base.

The company’s strategy to escape this trap was the American Centrifuge, a domestically designed gas centrifuge programme that had been in conceptual development since the 1970s under the Atomic Energy Commission and in engineering development since the 1980s at the DOE’s Oak Ridge and Portsmouth laboratories. USEC licensed the American Centrifuge technology from the DOE and began the commercialisation programme in earnest in the early 2000s, selecting the Piketon site as the commercial deployment location.

The American Centrifuge programme consumed hundreds of millions of dollars in federal and private capital through the 2000s and early 2010s without completing the transition from pilot demonstration to commercial deployment. The DOE provided loan guarantees, cost-sharing agreements, and direct research funding across multiple administrations; USEC invested operating cash flow from the gaseous diffusion plants; and the company drew on credit facilities to supplement programme funding. The centrifuge technology was demonstrated to operate at pilot scale, a 120-machine test cascade operated successfully at Piketon and validated the machine design, but USEC was unable to secure the commercial financing required to construct the full commercial plant.

The financing requirement was measured in billions of dollars, and private capital markets were unwilling to commit at the required scale to a programme whose economics depended on energy policy that had not been legislated and whose timeline had repeatedly slipped. The Paducah gaseous diffusion plant, USEC’s only operating revenue source of material scale, became commercially unviable as SWU market prices declined through the 2010s and electricity costs rose, and was shut down and returned to the DOE in May 2013. The company filed for Chapter 11 bankruptcy in March 2014 carrying $530 million in debt.

The American Centrifuge technology has been in development for approximately forty years, has consumed well over one billion dollars in combined federal and private capital, and passed through one corporate bankruptcy without reaching commercial scale. The difference between now and every prior attempt is not the technology, the centrifuge works. The difference is that the legislative and policy environment has eliminated the competitive alternative that previously made domestic enrichment commercially optional.

The critical difference between the USEC failure mode and the current Centrus opportunity is the policy environment rather than the technology or the management team. USEC was attempting to commercialise centrifuge enrichment in a market where Russian SWU was available at competitive prices without restriction, it was competing on commercial economics against state-subsidised foreign producers whose cost structures it could not match from an uncompetitive gaseous diffusion revenue base while simultaneously trying to fund a multi-billion-dollar industrial programme.

The Prohibiting Russian Uranium Imports Act of 2024 has removed the primary competitive pressure entirely. The DOE’s $3.4 billion in domestic enrichment awards across multiple companies provides the government capital the USEC-era programme lacked. The $1.9 billion cash balance Centrus brings to the buildout, accumulated through profitable LEU brokerage and capital market transactions, is a financial foundation USEC never achieved at any comparable stage of the programme.

The management team currently executing the buildout is led by CEO Amir Vexler, who joined Centrus as Chief Operating Officer in 2018 and became CEO in 2022. Vexler oversaw the HALEU Operation Contract through Phase 1 and Phase 2 completions, both delivered on time and on budget, which is the most directly relevant track record evidence available for assessing execution capability. The prior USEC management generation operated under different constraints: inadequate capital, competitive Russian supply, and a regulatory and political environment that did not treat domestic enrichment as a national security imperative.

The institutional knowledge of why the prior programme failed is embedded in the current strategic choices: the emphasis on building the cash position before the capital deployment phase begins, the fixed-price task order structure that transfers cost risk to Centrus but also disciplines cost management, and the Palantir analytics partnership that addresses the manufacturing precision requirements that eluded the earlier programme generation.

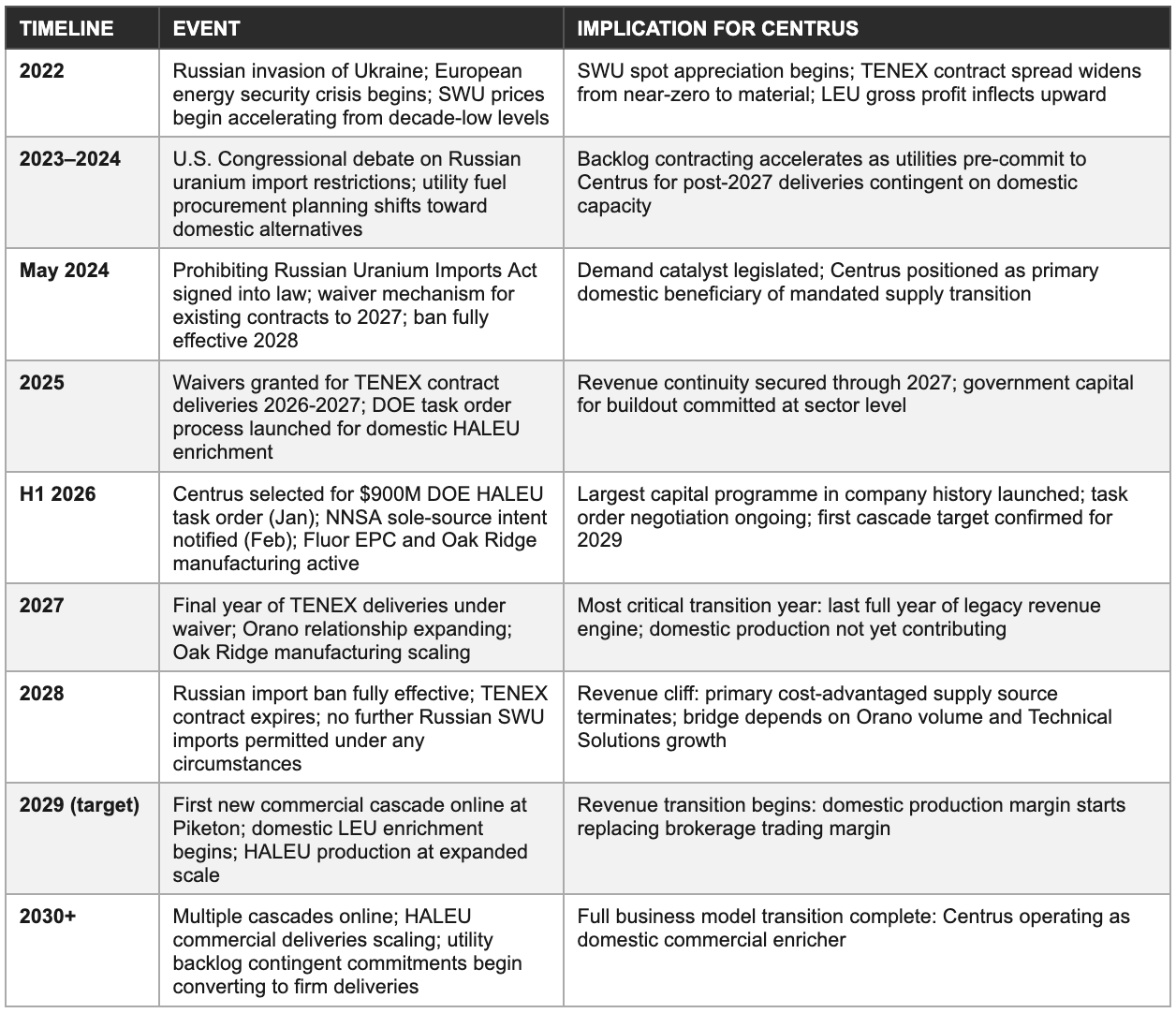

3. The Russian Ban, TENEX Dependency, and the 2028 Supply Cliff

Centrus’s current revenue depends on Russian enrichment services it will be legally prohibited from purchasing by 2028. The company building the domestic replacement for Russian supply is simultaneously the one most financially exposed to that supply’s removal. This structural tension is the defining analytical feature of the near-term investment case and the origin of both the opportunity and the primary downside risk.

The Prohibiting Russian Uranium Imports Act

The Prohibiting Russian Uranium Imports Act was passed by Congress with bipartisan support and signed into law in May 2024. The legislation bans the importation of Russian-origin uranium and uranium enrichment services into the United States. The ban includes a carefully designed transition mechanism: existing contractual deliveries may continue through 2027 subject to waivers issued by the Secretary of Energy, with the ban becoming fully effective and waiver-ineligible from January 1, 2028.

Russia’s Rosatom and its commercial subsidiary TENEX supplied approximately 24% to 27% of the enriched uranium fuelling U.S. commercial nuclear reactors at the time of the ban’s enactment. This is not a marginal supply share that could be displaced without consequence. Urenco and Orano, the two primary Western enrichers, are operating near capacity on existing long-term utility contracts and cannot simply absorb the Russian volume without new capacity additions.

The DOE’s $3.4 billion in domestic enrichment awards across multiple companies reflects the government’s recognition that market forces alone cannot build the replacement capacity within the ban’s timeframe. The legislative mandate, combined with the capital commitment, constitutes the most explicit federal industrial policy for civilian nuclear fuel production since the Atomic Energy Commission era.

The broader geopolitical context reinforces the ban’s durability. Russia’s invasion of Ukraine in 2022 triggered a fundamental reassessment of energy supply security across all commodity markets. European utilities, which had been even more dependent on Russian natural gas than U.S. nuclear utilities were on Russian SWU, experienced the practical consequences of energy geopolitical risk in real time during 2022 and 2023. The lesson absorbed by institutional energy buyers globally, that supply concentration in geopolitically adversarial nations carries risks that a price discount cannot compensate for, is embedded in the contracting preferences of utilities, pension fund energy investors, and energy security policymakers in a way that will persist beyond any single political cycle.

The demand for domestic enrichment reflects a durable shift in procurement risk management by the utilities that are Centrus’s customers.

The TENEX Supply Contract: Economics and the 2028 cliff

Centrus’s 2011 TENEX Supply Contract is the commercial foundation of the current LEU segment and the primary generator of the company’s profitability since the reorganisation. Under the contract, Centrus purchases SWU from TENEX at pricing that was contractually reset in 2018 to reflect then-prevailing market levels of approximately $80 to $100 per SWU. Since the 2018 reset, the SWU spot market has appreciated dramatically, from approximately $45 to $55 per SWU in 2019 to approximately $160 to $190 per SWU in 2025, a quadrupling driven by the accumulated geopolitical supply anxiety described above.

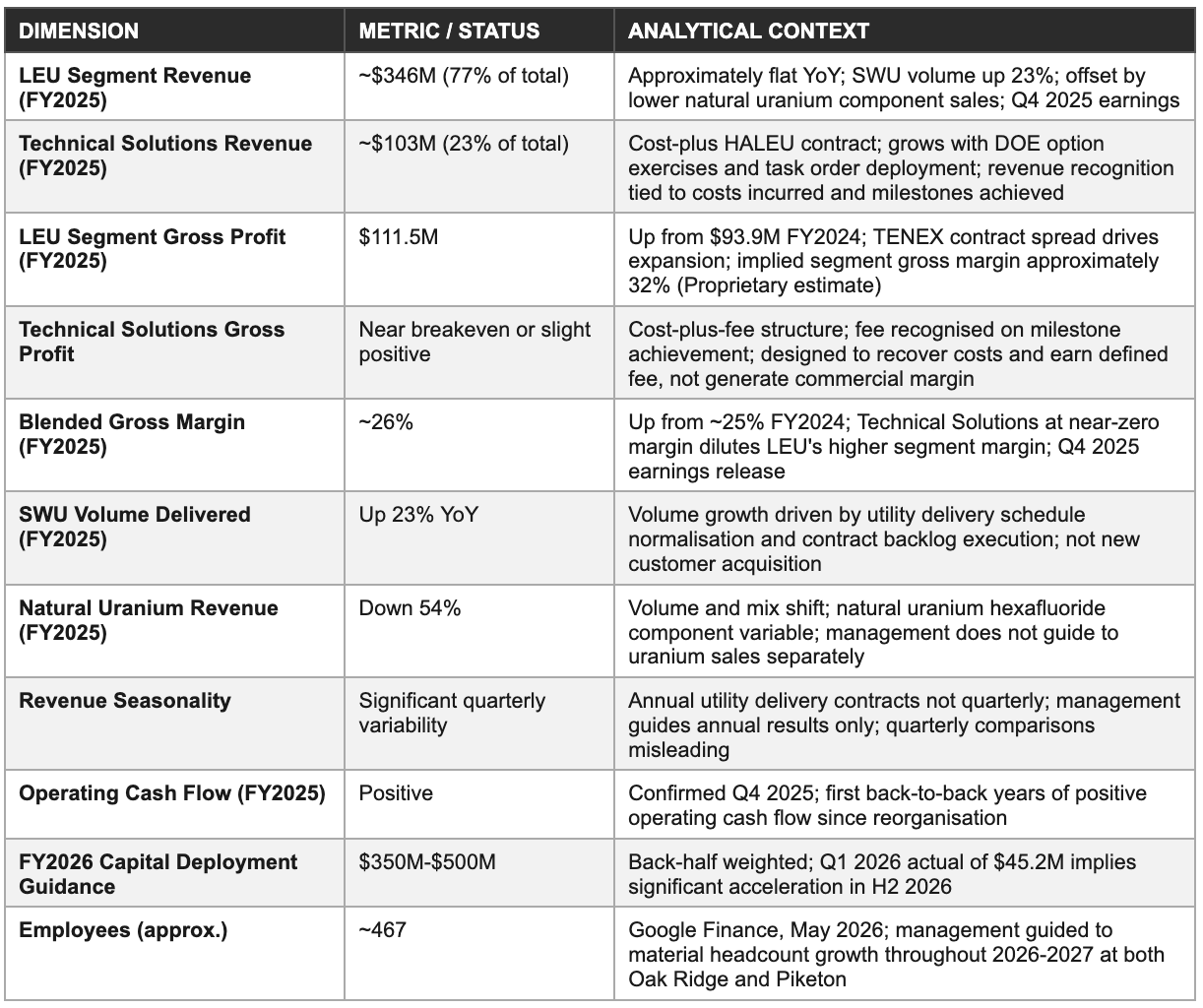

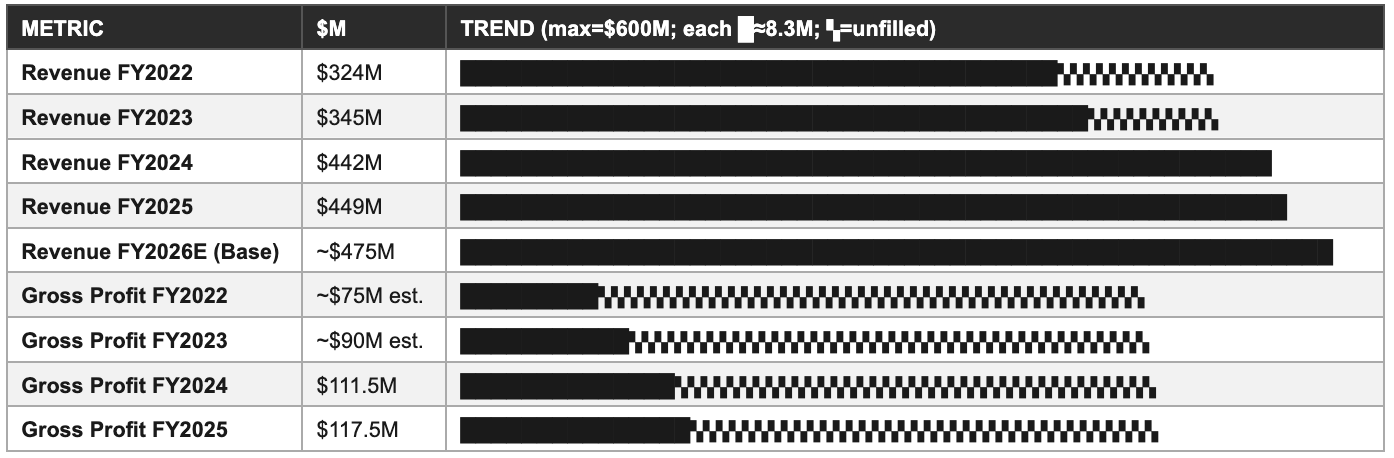

Each SWU purchased from TENEX at the 2018 contract rate and resold to a utility at the current market rate generates a margin that would be unavailable if Centrus were purchasing at spot. The LEU segment gross profit of $111.5 million in FY2025 from approximately $346 million in revenue, an implied segment gross margin of approximately 32%, is the financial expression of this price arbitrage.

The commercial paradox is precise: the Russian supply embargo that will ultimately terminate the TENEX contract is the same force that is elevating SWU prices above the TENEX contract rate, widening the margin on each delivery made while the contract remains active. Every metric ton of TENEX SWU delivered under the 2026 and 2027 import waivers is delivered at the below-market contractual price into a market where the spot replacement cost is significantly higher, generating a windfall margin that is financing the domestic enrichment buildout designed to replace that same Russian supply. Centrus is, in a precise financial sense, being paid by the geopolitical disruption of its primary supplier to construct the infrastructure that will make it independent of that supplier.

The TENEX contract expiry in 2028 creates the most important financial event in the near-term investment case. When the contract expires, the LEU segment’s cost of goods sold resets from the 2018-vintage TENEX price to whatever Centrus can source from Orano and the spot market. Orano’s pricing reflects current market conditions rather than a decade-old contractual rate, meaning the contracted cost advantage disappears permanently at expiry.

The gross margin on any continued LEU brokerage business after 2028 compresses from approximately 32% toward the narrower margin available on Orano-sourced SWU purchased at market rates. The domestic enrichment programme is designed to replace this compressed brokerage margin with a production-cost margin on domestically enriched uranium, but the timing of that replacement, specifically whether Piketon’s first cascade comes online in 2029 or later, determines the width and duration of the revenue and margin trough that investors must underwrite.

The 2028 transition timeline

Geopolitical risk to the waiver period

The 2026 and 2027 import waivers covering Centrus’s TENEX deliveries are subject to continued DOE processing and to the geopolitical conditions surrounding U.S.-Russia relations. An escalation in sanctions, in response to a significant military, cyber, or energy weaponisation event involving Russia, could trigger a reassessment of the waiver programme. The probability of outright waiver revocation is low given that the waiver mechanism was deliberately legislated by Congress to prevent a supply shock, and both the DOE and Congress have strong institutional interest in not creating a civilian nuclear fuel crisis before domestic alternatives are available.

The more realistic risk is partial: a TENEX counterparty decision to prioritise domestic Russian supply over export contracts under force majeure, a logistics disruption from sanctions on financial clearing or shipping routes, or a unilateral Russian export restriction used as energy leverage. Each of these scenarios has precedent in the broader energy sector from 2022 onward, and none can be fully foreclosed by the U.S. waiver mechanism. Management has disclosed the waiver status publicly and has not indicated any delivery disruption through the Q1 2026 reporting period, but the tail risk is real and investors should model a partial TENEX disruption scenario rather than treating 2026 and 2027 deliveries as fully secured.

4. Business Model Architecture: The Two-Segment Structure and Its Contradictions

Centrus operates two business models simultaneously with opposite capital profiles, opposite margin structures, and opposite risk exposures. The LEU segment is a capital-light trading operation generating cash today from a contracted SWU price arbitrage that terminates in 2028. The Technical Solutions segment is a capital-consuming government contractor producing HALEU at cost-plus economics that are the operational foundation of the company’s future value. The interaction between these two engines is the financial core of the investment case.

The LEU segment: Brokerage economics and their limits

The LEU segment generates revenue by purchasing SWU from state-owned foreign enrichers at contracted rates and reselling the resulting enriched uranium hexafluoride to utility customers at prices reflecting current market conditions. Centrus does not enrich uranium in this segment, it functions as an intermediary with long-duration supply contracts on both the purchase side (TENEX at 2018-vintage pricing, Orano at terms not publicly disclosed) and the delivery side (utility customers at pricing negotiated in multi-year fuel supply agreements).

The economic value generated between the two sides of the transaction is the LEU segment’s gross profit, which reached $111.5 million in FY2025 on revenue of approximately $346 million. The margin is approximately 32% at the segment level before corporate overhead allocation.

The brokerage model is capital-efficient precisely because Centrus does not own enrichment infrastructure for this segment, does not bear the capital cost of operating centrifuge cascades, and does not carry the electricity cost that is the primary production cost in enrichment. Its primary cost is the TENEX and Orano contracted SWU purchase price, which constitutes cost of goods sold. The gross margin of approximately 32% on LEU segment revenues in FY2025 is a trading margin on a spread between a below-market supply contract and current-market resale prices.

This distinction is critical for forecasting: when the TENEX contract expires and Centrus’s supply cost resets to market rates, the trading margin compresses to whatever the company can earn on Orano-sourced SWU purchased at current market rates resold to utilities at contracted delivery prices. That post-TENEX margin will be materially narrower than the current margin, and the width of the gap depends on Orano contract terms that Centrus has not publicly disclosed.

Revenue recognition in the LEU segment occurs when enriched uranium is physically delivered to a utility customer under a completed delivery obligation. Because utility fuel contracts specify annual delivery quantities and pricing on fixed schedules, LEU revenue has significant quarterly variability, a large delivery in Q3 under a utility contract creates a revenue spike in that quarter, while a quarter with no scheduled deliveries generates minimal LEU revenue regardless of the total contracted backlog outstanding.

Management consistently guides to annual results rather than quarterly run rates, and explicitly warns in earnings releases that quarterly comparisons are not meaningful for assessing underlying commercial momentum. Analysts and investors who build quarterly revenue models for Centrus will routinely misread the data because the quarterly pattern reflects delivery scheduling rather than business activity levels.

The Technical Solutions segment: Government manufacturing economics

The Technical Solutions segment generates revenue under the DOE HALEU Operation Contract on a cost-plus-incentive-fee basis. Revenue equals costs incurred plus target fees recognised upon milestone achievement. The segment is designed to recover costs and earn a defined government contract fee, not to generate a commercial return on investment in the traditional sense.

Its value to the Centrus investment case is operational and regulatory rather than financial: the demonstration cascade at Piketon that has produced more than one metric ton of HALEU cumulatively is the proof of concept for the American Centrifuge at HALEU enrichment levels, the operational basis for the NRC’s confidence in the expansion licence framework, and the commercial credential that enabled Centrus to win the $900 million DOE HALEU task order against competing proposals from other defence and nuclear contractors.

The Technical Solutions segment is expected to grow substantially in FY2026, FY2027, and FY2028 as the $900 million HALEU task order is negotiated, finalised, and deployed. Revenue from the task order will be recognised as costs are incurred and milestones achieved under the fixed-price structure, a different recognition pattern from the prior cost-plus demonstration contract but still milestone-driven rather than continuous.

The fixed-price structure is analytically important: it means Centrus bears execution cost risk above the contracted ceiling, creating a direct linkage between manufacturing efficiency at Oak Ridge, construction execution at Piketon, and the financial return on the task order. This is why the Palantir-identified $300 million in potential cost savings is a margin management tool as much as an operational efficiency initiative, in a fixed-price government contract, the difference between estimated cost and actual cost flows directly to or from the contractor’s economic return.

Unit economics summary

The structural contradiction between the two segments resolves as a financial bridge problem: the LEU brokerage provides the cash that finances the Technical Solutions buildout; the buildout provides the production capacity that generates future revenue when the LEU brokerage terminates. The question is whether the bridge is long enough. A two-year revenue gap, between the 2028 TENEX expiry and meaningful domestic production in 2030, is manageable with the $1.9 billion cash buffer.

A gap extending to three years or more compresses the cash buffer toward levels that create capital market anxiety about the 2030 convertible note maturity. The base case assumes a gap of approximately twelve to eighteen months between TENEX expiry and material domestic production contribution, bridged partially by Orano-sourced brokerage at compressed margins and partially by Technical Solutions task order revenue growing through 2028.

5. HALEU and the Piketon Buildout: From Demonstration Cascade to Commercial Scale

High-Assay Low-Enriched Uranium is the fuel that does not exist in commercial Western supply, is required for most advanced reactor designs under development, and is the primary reason the federal government has committed over $900 million specifically to Centrus’s enrichment expansion. The Piketon buildout is simultaneously the realisation of a forty-year technology programme and the largest capital deployment event in the company’s history.

What HALEU is and why no western commercial substitute exists

High-Assay Low-Enriched Uranium is uranium enriched to between 5% and 20% U-235 content, compared to the 3% to 5% enrichment level of conventional low-enriched uranium used in today’s operating commercial reactor fleet. HALEU is a fuel design requirement for most advanced reactor technologies currently under development and regulatory review, including the X-energy Xe-100 high-temperature gas-cooled reactor (recently selected for a DOE advanced reactor demonstration programme), the TerraPower Natrium sodium-cooled fast reactor, and numerous microreactor designs targeting defence, remote power, industrial heat, and space propulsion applications.

These designs exploit the higher energy density of HALEU to achieve superior fuel efficiency, smaller plant footprints, longer refuelling intervals, and in some cases passive safety characteristics that conventional LEU cannot enable at equivalent power output. The absence of Western commercial HALEU supply is a structural void that requires deliberate public investment to close because the economics of building HALEU production capacity do not yet work without government subsidy.

The advanced reactor fuel demand that would justify commercial HALEU production at scale will not materialise until reactors are deployed; reactor deployment requires HALEU to be available; HALEU production requires capital investment that precedes the reactor demand. This chicken-and-egg dynamic is precisely why the DOE is funding domestic HALEU production through the task order mechanism rather than waiting for private capital to find the economics attractive. The government is essentially pre-purchasing the supply chain necessary for the advanced reactor programme it is simultaneously funding, which is the same approach it used in the 1950s and 1960s to develop the civilian nuclear industry from the weapons programme’s infrastructure.

Centrus’s 16-centrifuge cascade at Piketon is the only U.S.-licensed, operational HALEU production facility. Cumulatively it has produced more than one metric ton of HALEU UF6, delivered to the DOE for research, development, and national security applications. This production track record, limited in volume but unique in domestic regulatory authorisation and operational history, is the competitive moat that other HALEU development programmes cannot replicate on any timeline shorter than three to five years.

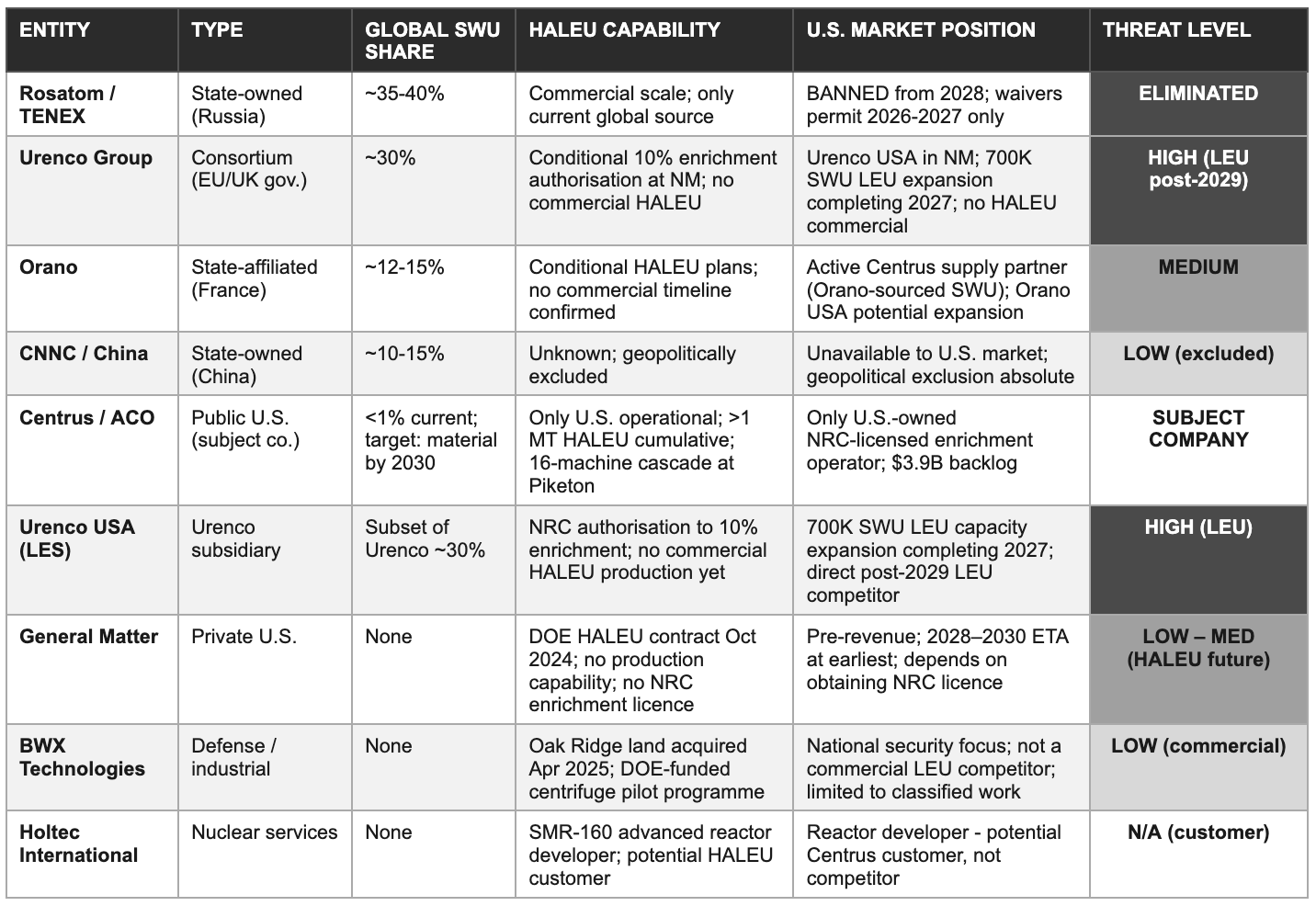

The competing programmes, Urenco USA’s conditional authorisation for enrichment to 10% at its New Mexico facility, General Matter’s October 2024 DOE contract with no production capability, BWX Technologies’ April 2025 Oak Ridge land acquisition, are all at earlier stages of operational readiness than Centrus. The regulatory and operational head start that Centrus holds is not permanent, the window narrows as competitors execute their own programmes, but it is material for the 2028 to 2031 period that is most commercially significant for the first wave of advanced reactor deployments.

The American Centrifuge technology

The American Centrifuge is a gas centrifuge enrichment machine developed by the DOE and its predecessor agencies from the 1970s onward. Gas centrifuge enrichment works by spinning uranium hexafluoride gas in a rotor at high velocities, exploiting the slight mass difference between the U-235 and U-238 isotopes to cause the heavier isotope to concentrate at the outer wall of the centrifuge rotor while the lighter, more enriched fraction migrates toward the center.

The separation achieved by a single centrifuge is small, requiring thousands of centrifuges operating in cascade configurations to achieve commercial enrichment levels at useful throughput rates. The American Centrifuge machine is designed to a higher performance specification than some earlier centrifuge generations, achieving SWU output per machine that reduces the total number of machines required for a given capacity target.

The technology’s most important strategic characteristic is domestic manufacturability. Urenco’s centrifuge technology is governed by the Treaty of Almelo, a 1970 tripartite agreement among the UK, Netherlands, and Germany that controls technology transfer and prohibits independent manufacturing by non-treaty parties. Russia’s centrifuge technology is state property unavailable for export. China’s is similarly restricted. The American Centrifuge is the only commercially viable centrifuge enrichment technology that the United States can manufacture domestically, using a domestic supply chain, without technology transfer from foreign governments.

This manufacturing independence is strategically important for national security reasons that extend beyond the civilian HALEU market: enrichment technology is dual-use, and the ability to maintain domestic centrifuge manufacturing capability is a strategic asset regardless of any specific commercial contract’s economics. The DOE has explicitly stated this consideration as a factor in its enrichment programme investment decisions.

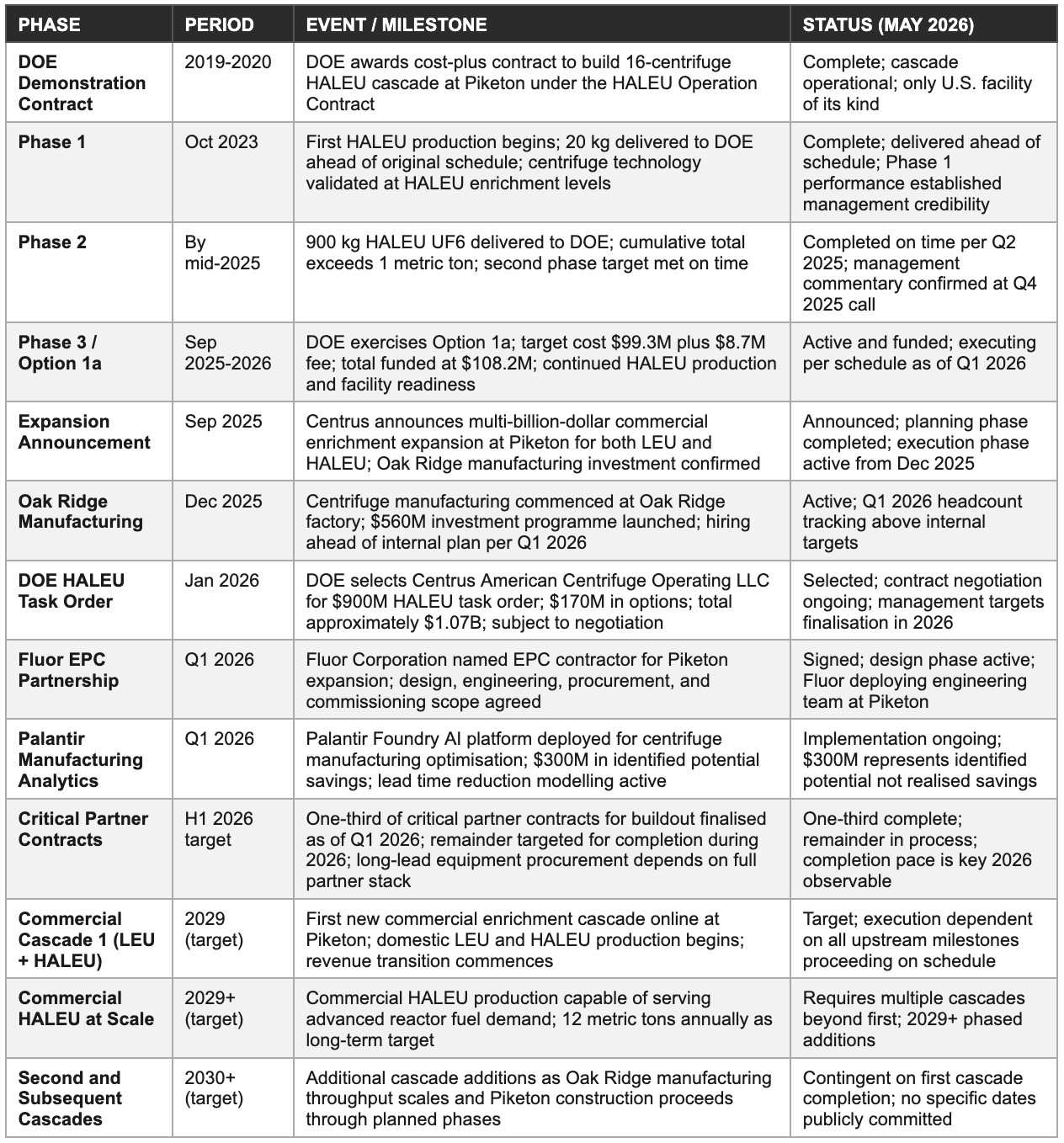

The three-workstream buildout programme

The commercial expansion programme executes across three concurrent workstreams that must be coordinated with engineering precision to meet the 2029 first-cascade target.

The first workstream is centrifuge manufacturing at Oak Ridge, Tennessee, where the $560 million investment programme launched in December 2025 is expanding centrifuge production capacity. The Oak Ridge factory is the throughput constraint for the entire buildout: the rate at which completed centrifuges can be produced and shipped to Piketon determines how quickly new cascade capacity can be installed and commissioned. Management disclosed at Q1 2026 that hiring at Oak Ridge is tracking ahead of internal plan, a positive leading indicator for manufacturing ramp, though early hiring pace does not guarantee later manufacturing throughput consistency.

Centrifuge manufacturing requires specialised machining of components to tight tolerances, vacuum assembly in controlled environments, and systematic quality control at each stage; any step where the production process degrades from specification creates rework cycles that compress the delivery timeline for downstream cascade installation.

The second workstream is the Piketon site expansion, for which Fluor Corporation has been contracted as Engineering, Procurement, and Construction manager. Fluor is one of the largest and most experienced EPC contractors in the world, with a track record in nuclear, energy, and complex government infrastructure projects that includes some of the most technically demanding programmes in U.S. industrial history. The EPC scope covers design of the expanded cascade buildings and process infrastructure, procurement of long-lead equipment including electrical switchgear, process gas systems, instrumentation and control systems, and commissioning of the completed cascades as centrifuges are delivered from Oak Ridge.

The EPC model transfers construction management risk to a contractor with specialised project delivery capability, but Centrus retains the technology risk, the performance of the American Centrifuge machines at commercial scale remains Centrus’s responsibility, and no EPC agreement transfers technology execution risk.

The third workstream is procurement of critical long-lead materials and equipment. At Q1 2026, management disclosed that approximately one-third of critical partner contracts had been finalised, with the remainder targeted for completion during 2026. Long-lead items in enrichment plant construction include specialised electrical equipment, vacuum system components, gas handling and purification systems, monitoring and control instrumentation, and structural fabrications that require 18 to 36 months between order placement and on-site delivery.

Any delay in finalising supplier contracts in the first half of 2026 creates a corresponding equipment delivery delay that flows directly into the 2029 first-cascade timeline. This is the most immediately observable execution variable in the near term, and the Q2 and Q3 2026 earnings calls will provide the first measurable data points on whether the partner contracting progression is tracking from one-third to full completion as management has guided.

Buildout programme timeline

The Palantir Foundry deployment warrants specific commentary. Management disclosed at Q1 2026 that the Palantir implementation has identified approximately $300 million in potential cost savings and lead time reductions across the manufacturing and procurement programme. In the context of a fixed-price task order where cost overruns reduce Centrus’s economic return, this claim is analytically material: if even a third of the identified savings are realised through better procurement scheduling, manufacturing process optimisation, and materials yield improvement, the fixed-price task order economics improve meaningfully.

However, the $300 million figure represents identified opportunities derived from Palantir’s data modelling of the programme, not confirmed reductions in purchase orders or labour costs. The distance between a model identifying cost optimisation opportunities and actual realisation of those savings in procurement contracts and manufacturing throughput is substantial, and the Palantir partnership should be tracked through future earnings disclosures for evidence that the model outputs are converting to actual cost performance.

6. Government as Customer, Regulator, and Financier: The Policy Dependency Architecture

The U.S. federal government simultaneously serves as Centrus’s largest customer, its primary capital source for the enrichment buildout, its operating licence grantor, the architect of the import prohibition that created the demand catalyst, and the landlord of its primary operating facility. This multi-role relationship is the defining structural feature of the investment case. It is the source of revenue durability, the origin of bureaucratic execution risk, and the primary determinant of the valuation multiple that institutional investors assign to the business.

The DOE as commercial customer and capital allocator

The Department of Energy has been Centrus’s most important commercial relationship since the HALEU Operation Contract was signed in 2022. That contract funded the three-phase HALEU demonstration programme through a cost-plus-incentive-fee structure.

Phase 1 (20 kg delivery, completed October 2023 ahead of schedule), Phase 2 (900 kg delivery, completed on time in mid-2025), and Phase 3 including Option 1a (funded at $108.2 million including target fee as of September 2025) collectively demonstrated the American Centrifuge’s HALEU production capability across multiple delivery cycles and validated Centrus’s project management competence at the scale of the demonstration programme.

The cost-plus structure of the demonstration contract meant that Centrus bore no fixed-price risk during the pilot phase, all costs were reimbursed, and the incentive fee was earned upon milestone completion, which allowed the company to demonstrate capability without bearing the capital risk of a commercial development investment.

The $900 million HALEU task order announced in January 2026 represents a qualitative shift from demonstration funding to commercial-scale deployment capital. DOE selected American Centrifuge Operating, LLC through a competitive evaluation that assessed technical capability, past performance on the HALEU demonstration contract, management capacity for a programme of this scale, and cost proposal. The task order is currently in negotiation, with finalisation expected during 2026 per management’s Q1 2026 guidance.

Unlike the demonstration contract, the task order is structured as a fixed-price award: Centrus receives defined payments for delivering defined enrichment capacity milestones, and any cost overrun above the fixed-price ceiling is borne by Centrus. This contract structure is DOE’s mechanism for transferring execution risk to a contractor that has demonstrated sufficient capability, it is a vote of confidence in Centrus’s programme management, and it also creates the incentive for Centrus to invest in cost management tools like the Palantir deployment that would be less urgent under cost-plus economics.

Beyond the HALEU task order, DOE has deployed $3.4 billion across multiple domestic enrichment suppliers as part of a structured programme to rebuild U.S. enrichment capability. The multi-supplier approach, including parallel awards to Urenco USA, Orano USA, and potentially others in addition to Centrus, signals that DOE is managing the programme as a portfolio rather than concentrating all risk in a single contractor relationship. This has two implications for Centrus investors.

On the positive side, the portfolio approach increases the political durability of the enrichment programme as a whole: Congressional support is distributed across multiple states and supplier relationships rather than concentrated in a single project that could become a political target. On the risk side, the parallel DOE investments mean that Centrus’s HALEU monopoly window narrows as competitor programmes progress, and the commercial pricing premium available to the first mover may compress as additional Western supply enters the market in the early 2030s.

The NRC licence: An institutional moat that required decades to build

The Nuclear Regulatory Commission licences all commercial uranium enrichment activities in the United States. The licensing process for a new enrichment facility requires a facility licence application documenting site characterisation, facility design at detailed engineering level, safety analysis demonstrating adequate protection of public health and worker safety, environmental impact assessment, quality assurance programme documentation, and financial qualification.

NRC technical review alone typically takes three to five years under normal processing; the full process from application to licensed operation has historically taken five to ten years for complex nuclear facilities. A competitor entering the enrichment market with a new application in 2025 could not receive a new licence and commence commercial operation before the early 2030s at the earliest under any realistic regulatory scenario.

Centrus holds the operating licence for the Piketon facility, maintained continuously since the American Centrifuge Plant was originally licensed under the USEC regime. The licence continuity through the USEC bankruptcy, the Chapter 11 reorganisation, and the subsequent restructuring as Centrus is a critical asset that competitors cannot replicate without going through the full NRC licensing process. The expansion of the Piketon facility for the commercial enrichment programme occurs within the existing licensed boundary, allowing the company to add cascade capacity under the existing licence framework through regulatory notifications and specific approval requests for defined modifications rather than a full new licence application.

The incremental regulatory process for expansion is meaningfully less burdensome than a greenfield licence application, reducing both the time and cost required to bring new enrichment capacity into operation at an already-licensed site. Management has characterised the NRC process for the current expansion as a managed compliance exercise rather than a programme-level execution risk, an assessment that is credible given the regulatory continuity of the facility and the relatively precedented nature of expanding an operating enrichment cascade within existing licensed infrastructure.

The DOE facility lease and the NNSA relationship

Centrus operates the Piketon facility under a lease with the Department of Energy, which retains ownership of the site as a federally managed facility with origins in the Cold War weapons programme. The lease reflects the site’s federal origins and is similar in structure to other DOE technology transfer arrangements where private operators manage federally owned industrial infrastructure.

The lease creates a structural dependency, Centrus cannot relocate enrichment operations from Piketon without negotiating a fundamentally different governmental relationship, but it also provides a form of operational continuity assurance: the DOE has a vested interest in maintaining an operating enrichment facility at Piketon as a national security and energy security asset, creating alignment between the government’s interests as landlord and Centrus’s interests as operator that would not exist if the two were purely commercial counterparties.

The NNSA sole-source notification in February 2026 is the most strategically significant government relationship development of the prior twelve months. The National Nuclear Security Administration’s designation of Centrus as the sole-source provider for certain enrichment requirements confirms that the national security enrichment market is accessible to Centrus without competition. Sole-source procurement is used by the government when only one responsible source capable of satisfying the requirement exists, the notification is therefore a formal government determination that no other company can provide what NNSA needs, which is the strongest possible statement of Centrus’s unique capability in the enrichment domain.

The potential revenue from NNSA engagement is not publicly dimensioned because NNSA programme requirements are classified, but the structural significance is clear: a government customer with classified enrichment requirements and unlimited procurement authority has designated a single commercial vendor as its sole viable source. The commercial implications of this relationship, once the sole-source notification converts into a specific funded contract, are likely to be material to the Technical Solutions segment revenue trajectory beyond the HALEU commercial task order alone.

The federal government’s multi-role relationship with Centrus creates revenue quality that is simultaneously more durable and less transparent than conventional commercial contracts. More durable because the counterparty is the sovereign with legislatively mandated demand and unlimited purchasing authority. Less transparent because appropriations cycles, NNSA classification requirements, and procurement bureaucracy create information gaps that commercial contract disclosures do not. Investors must price both dimensions.

Policy durability across administration cycles

The Prohibiting Russian Uranium Imports Act requires a Congressional vote to reverse, not merely an administrative decision. The bipartisan nature of its passage, energy security motivating Republican support, clean energy manufacturing motivating Democratic support, and the absence of any meaningful domestic political constituency for restoring Russian uranium imports makes legislative reversal the lowest-probability risk in the investment case.

The more realistic policy risks are softer: annual appropriations reductions that slow task order funding tranches, procurement bureaucracy that extends contract negotiations beyond management’s 2026 finalisation target, or inter-agency coordination delays that push regulatory milestones into the following fiscal year. Each of these delays is manageable individually with the $1.9 billion cash buffer absorbing the programme impact.

The cumulative effect of multiple smaller delays, if every step in the DOE procurement and appropriations process takes six months longer than management’s current projections, is what creates the risk of the 2029 first-cascade target slipping into 2030 without any single catastrophic failure. Investors should assess the policy risk not as a binary (ban reversed / not reversed) but as a timeline distribution where the central estimate is the 2029 target and the realistic range extends through 2031 under various combinations of procurement and appropriations delay.

7. The LEU SWU Pricing Cycle, Backlog Quality, and Revenue Mechanics

The $3.9 billion total backlog extending to 2040 is the most important commercial asset the company holds, but its quality requires careful reading. The LEU segment backlog is largely contingent on completing the enrichment expansion, it represents utility commitments made in anticipation of domestic capacity that does not yet exist at commercial scale. The SWU pricing cycle driving gross margin expansion since 2019 reflects geopolitical supply anxiety rather than structural demand growth, and the transition from brokerage margin to production margin is the financial bridge the investment case must cross without a structural break in the company’s cash generation.

SWU price dynamics: The mechanics of the current margin

Separative work units are the standard currency of uranium enrichment services. One SWU represents the amount of work required to produce a defined quantity of enriched uranium at a target enrichment level from a defined quantity of natural uranium feedstock at natural abundance. SWU is traded in both spot and long-term contract markets. The spot market reflects current supply-demand conditions for immediate or near-term enrichment services; the long-term contract market reflects multi-year agreed prices embedded in utility fuel supply agreements that provide price certainty over planning horizons of five to fifteen years.

Prior to 2019, SWU spot prices had been depressed for most of the decade following the 2011 Fukushima accident, which triggered reactor shutdowns across Japan, reduced global enrichment demand, and left the market with excess capacity from Western and Russian enrichers. The spot price bottomed in the range of $40 to $50 per SWU in the 2015 to 2019 period, making enrichment an unattractive investment and discouraging new capacity development globally.

The price recovery that began in 2019 and accelerated sharply from 2022 onward was driven by a convergence of supply security reassessment events: the post-COVID inventory drawdown by utilities, growing recognition of Russian supply concentration risk before the formal import ban, European energy security policy shifts after 2022, and ultimately the 2024 legislative restriction. By 2025, SWU spot prices had reached approximately $160 to $190 per SWU, roughly four times their 2019 lows, representing a 24% compound annual growth rate over six years that management cited explicitly in the Q4 2025 earnings call.

The specific implication for Centrus is that its TENEX contract, reset in 2018 to then-prevailing rates of approximately $80 to $100 per SWU, now provides access to enrichment services at less than half the current spot cost. Each SWU purchased from TENEX at the 2018 contract rate and resold to a utility at a delivery price reflecting 2022, 2023, or 2024 market conditions generates a gross margin that would be unavailable if Centrus were purchasing at spot.

This is a temporary windfall from a lucky contract timing that happens to coincide with the largest SWU price cycle in the industry’s recent history. The windfall is real, it is generating significant cash, and it is financing the buildout. But investors should understand that the current LEU gross margin is a time-limited price arbitrage that terminates when the TENEX contract expires.

Revenue and gross profit trend

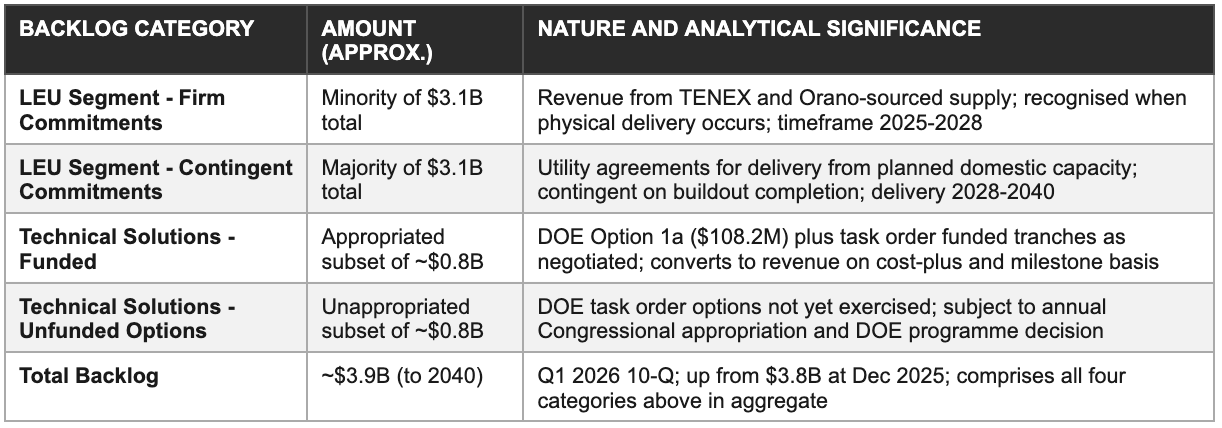

Backlog quality: Firm versus contingent

The $3.9 billion total backlog extending to 2040 comprises two fundamentally different categories of commercial obligation that have different implications for revenue recognition, cash flow timing, and the business’s vulnerability to execution delay. The first category is firm delivery commitments: contracts under which Centrus is obligated to deliver a specified volume of enriched uranium on a defined schedule, sourced from the TENEX supply relationship, the Orano relationship, or existing inventory held on the balance sheet.

These commitments generate revenue when physical delivery occurs, are not contingent on future events, and are receivable as long as Centrus maintains its supply relationships and the utility customer honours payment terms. Firm commitments represent the near-term revenue base through 2027.

The second category is contingent commitments: utility agreements to purchase enriched uranium from Centrus’s planned domestic enrichment capacity, contingent on Centrus securing the funding and completing the Piketon expansion on or near the targeted schedule. These commitments are commercially significant, they represent utility decisions to pre-reserve domestic enrichment capacity years before its availability, which is evidence of genuine demand conviction by sophisticated institutional energy buyers, but they are not firm order book entries in the traditional sense.

A utility that has signed a contingent commitment with Centrus is not legally obligated to pay if Centrus fails to deliver because the expansion does not complete; the commitment is conditioned on Centrus’s performance. The backlog cannot be read as fourteen years of uninterrupted forward revenue visibility. It is more accurately understood as a long-duration option held by utilities over Centrus’s future production capacity, an option that becomes progressively more valuable to both parties as the buildout milestones are achieved, but that requires Centrus to perform against specific delivery commitments starting in 2028 to convert the option into contracted revenue.

8. Balance Sheet Architecture: Cash Position, Convertible Notes, and Legacy Pension Liability

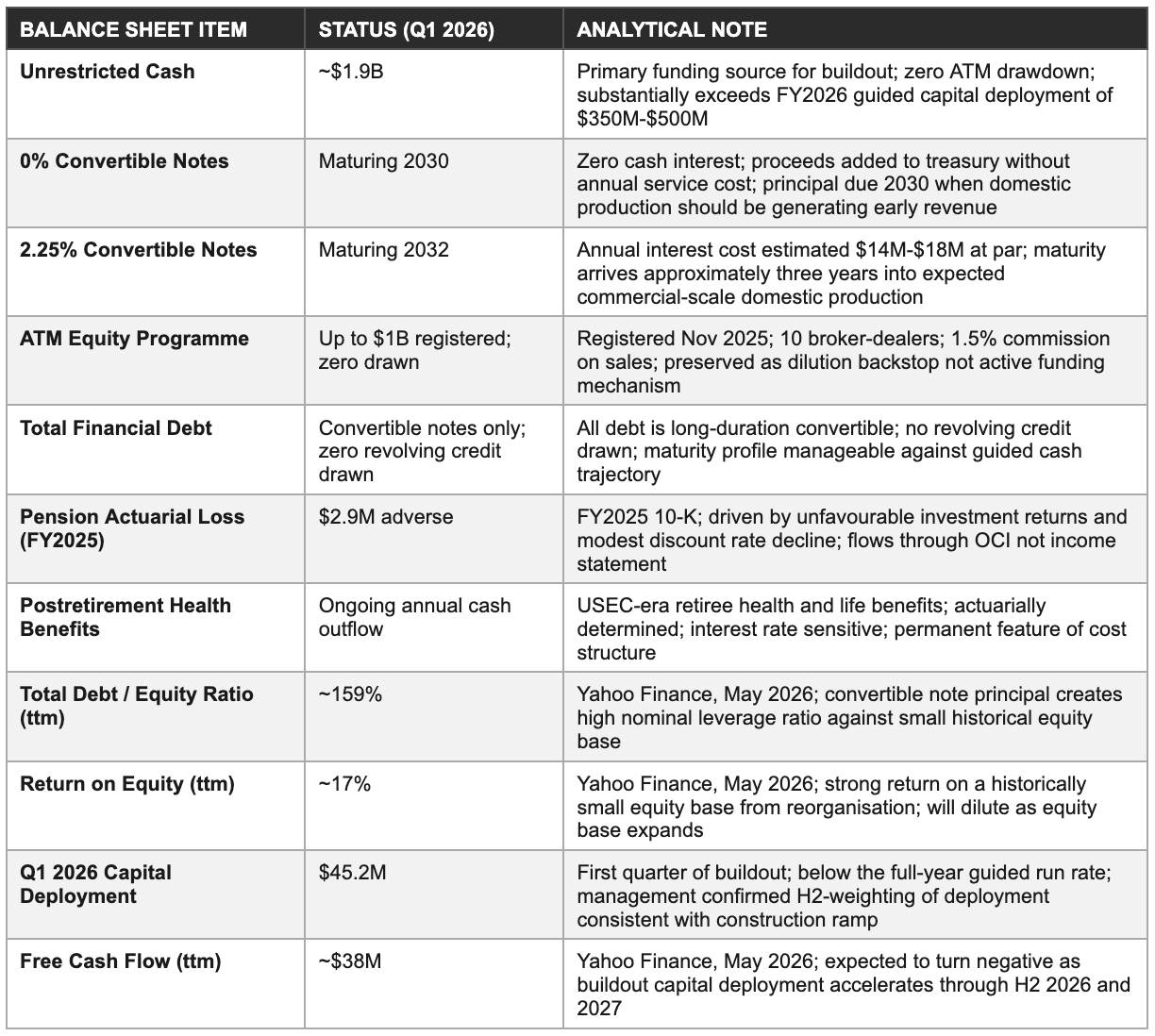

Centrus entered the commercial buildout phase with approximately $1.9 billion in unrestricted cash and zero drawn on its $1 billion at-the-market equity programme. That liquidity position is what makes the investment case viable: it provides multi-year runway to fund the Piketon and Oak Ridge programmes without immediate recourse to the capital markets regardless of near-term execution delays. The structural complexity comes from two directions: a convertible note structure with maturities in 2030 and 2032 that arrive before the enrichment programme reaches full commercial scale, and a legacy pension and postretirement benefit obligation inherited from USEC that represents a permanent cash drain on a business only recently achieving consistent profitability.

How the $1.9 Billion cash position was built

The $1.9 billion unrestricted cash balance as of March 2026 is the product of three concurrent capital actions executed over the twelve months preceding the buildout launch. The first and most important was operating cash generation from the LEU segment: the margin between the 2018-vintage TENEX contract purchase price and the current utility resale prices generated positive operating cash flow in FY2025, the third or fourth consecutive year of LEU segment profitability since the reorganisation. T

he operating cash generation has been augmented by the SWU price appreciation dynamic described in Section 7: higher utility resale prices on fixed-schedule delivery contracts contracted in 2022 to 2024 converted to cash as deliveries occurred, generating operating cash flow that accumulated in the treasury.

The second capital action was the issuance of 0% Convertible Notes in late 2025. Zero-coupon convertible instruments carry no cash interest obligation, the entire proceeds are available for capital deployment without any annual debt service cost reducing the cash reserve. The zero-coupon structure is particularly valuable in the context of the buildout: during the two to three years when capital deployment is at peak and operating cash flow is declining as the TENEX contract phases toward expiry, the absence of annual interest payments on the 0% notes preserves cash that would otherwise be consumed by debt service. The principal amount of the 0% notes determines the magnitude of the 2030 maturity event; the full disclosure appears in the 10-K and 10-Q filings available on SEC EDGAR.

The third capital action was the November 2025 registration of an at-the-market equity offering programme providing up to $1 billion in Class A common stock issuance capacity through ten designated broker-dealers at a 1.5% commission on actual sales. As of Q1 2026, zero shares had been sold under the ATM programme. Management’s decision to register but not draw on the ATM programme reflects a capital strategy of preserving dilution capacity as a backstop rather than an active funding mechanism.

Registering the ATM programme at the time of the capital raise and convertible note issuance signals to the market that additional equity capacity exists without committing to dilution at any specific price. The practical effect is that institutional investors know Centrus could issue up to $1 billion in equity at relatively low friction cost if needed, which provides a form of implicit capital assurance that reduces the probability of a liquidity crisis scenario in the bear case.

The convertible note maturities: A 2030 decision point

The two convertible note instruments create financing decision points within the buildout horizon that are independent of the operational execution risks. The 0% Convertible Notes maturing in 2030 present the earlier and more significant challenge. Under the base case timeline, the first commercial cascade at Piketon comes online in the second half of 2029 and begins generating domestic production revenue in late 2029 or early 2030.

The 2030 note maturity arrives approximately six to twelve months after first domestic production commences, a period when the domestic revenue stream is real but nascent, when Orano-sourced brokerage is providing transitional revenue at compressed margins, and when the company has been consuming its cash buffer through two to three years of peak buildout capital deployment. The adequacy of the cash position and operating cash flow to address the note maturity at that specific moment, without issuing dilutive equity at a price that may reflect buildout execution uncertainty, is the central financial risk question in the 2029 to 2030 horizon.

The 2.25% Convertible Notes maturing in 2032 present a more manageable challenge under the base case. By 2032, domestic enrichment should be in its second to third year of commercial operation under the base case timeline, with multiple cascades potentially online and the Technical Solutions task order largely deployed. The annual interest cost of approximately $14 million to $18 million (estimated from the 2.25% coupon applied to a plausible principal amount) is manageable against the operating cash generation that should be visible by 2032.

The risk concentrates in a scenario where the buildout is delayed into 2031 and the 2032 notes arrive before domestic production has established a stable revenue base, a risk that is addressed by the bear case analysis in Section 13 but does not warrant being rated as a primary concern in the base case.

The legacy pension: A structural cost embedded in the business

The USEC Chapter 11 reorganisation left Centrus with two legacy benefit obligations that are permanently embedded in the company’s cost structure: a defined benefit pension plan covering USEC-era employees and eligible retirees, and a postretirement health and life benefit plan for the same covered population. Both obligations are actuarially determined, their present values depend on assumptions about participant mortality rates, benefit escalation, investment returns on pension assets, and the discount rate applied to project future liabilities back to present value.

The FY2025 10-K disclosed a net actuarial loss of $2.9 million driven by a combination of unfavourable pension asset investment returns during 2025 and a modest reduction in the discount rate assumption, which increases the present value of future benefit obligations. This actuarial loss is recorded through Other Comprehensive Income rather than flowing through the income statement, which means it does not affect reported net income but does reduce the book value of equity and represents a real economic deterioration of the company’s financial position.

The annual cash outflow for pension benefit payments and postretirement health and life benefits is disclosed in the operating section of the cash flow statement. These payments represent legal obligations to retirees who earned benefits during active service under USEC and cannot be reduced unilaterally. In the context of the $1.9 billion cash balance, the pension and postretirement cash obligations are not existential, they are a second-order cost item. The significance is their permanence and their sensitivity to macroeconomic variables outside management’s control.

If the Federal Reserve were to reduce interest rates materially in response to an economic slowdown during the 2026 to 2029 buildout period, the discount rate used to calculate pension obligations would decline, increasing the present value of future liabilities and the required annual contribution to maintain funded status. This scenario, a recession that simultaneously reduces enrichment demand, SWU prices, and discount rates, would create adverse pressure on multiple financial metrics at the same time, illustrating why the pension obligation is worth monitoring even when it appears manageable in isolation.

9. Competitive Landscape: The Enrichment Oligopoly and the HALEU Window

Centrus currently holds below 1% of global commercial enrichment capacity and yet occupies the most strategically valuable position in the domestic U.S. enrichment market. That apparent paradox resolves when competition is framed correctly: the relevant question is who will supply the domestic enrichment capacity that U.S. utilities must source from non-Russian suppliers beginning in 2028. Centrus’s first-mover advantage is real, licensed, and operational.

The global enrichment oligopoly: Why entry takes decades

Uranium enrichment is among the most concentrated industrial sectors in the global economy, and the concentration is structurally embedded rather than the result of anticompetitive behaviour. Four entities (Rosatom/TENEX, Urenco, Orano, and CNNC) control virtually all global SWU production capacity, and the barriers to entry are high enough that no new commercial-scale enrichment facility has been built in the Western world since the existing oligopoly was established. The technology barrier is the most fundamental: gas centrifuge enrichment is the only economically viable enrichment technology, the competing gaseous diffusion technology having been retired globally as uneconomical.

Each of the existing producers controls proprietary centrifuge technology that is classified as a national strategic asset and is not available for commercial licensing or technology transfer to new entrants. Urenco’s centrifuge designs are governed by the 1970 Treaty of Almelo and cannot be exported to non-treaty parties. Russia’s centrifuge technology is state property subject to export controls. China’s similarly. The American Centrifuge is the only domestically originated centrifuge technology that the United States can manufacture and deploy without dependence on foreign state permission.

The capital barrier compounds the technology barrier. A commercial centrifuge enrichment facility requires an initial investment measured in billions of dollars, multi-year construction timelines, and a sustained operating period before it generates sufficient revenue to recover its capital cost. The economics are not attractive to private capital without the assurance of long-duration utility supply contracts, and long-duration utility contracts are not available without a demonstrated track record of reliable enrichment operation, which requires having already built the facility.

The government capital that DOE has committed through the $3.4 billion enrichment programme is the mechanism for breaking this financing circularity, it provides the initial capital that enables construction, which enables the operating track record, which enables utility contracting, which enables commercial revenue. Without government seed capital, the Western enrichment expansion required by the Russian import ban could not proceed on the timeline the legislation requires.

The HALEU market: A first-mover opportunity with a closing window

The HALEU competitive landscape is structurally different from conventional LEU because HALEU production does not yet exist in Western commercial supply at any scale. Every potential Western HALEU producer is essentially starting from approximately the same point in 2025 to 2026, with Centrus distinguished by being the only one that has actually produced HALEU in the United States under regulatory oversight and delivered it to a customer.

This operating track record, limited in volume but unique in regulatory and operational history, is the moat that makes Centrus’s HALEU position durable in the near term. Competitors cannot purchase this track record; they can only accumulate it through their own production history, which takes time regardless of capital invested.

The HALEU competitive window is real but narrowing. Urenco USA’s conditional regulatory authorisation for enrichment to 10% U-235 at its New Mexico facility could be extended toward commercial HALEU production if the company chooses to invest in the additional processing capabilities required. Orano’s conditional HALEU development plans, if funded and executed, could produce commercial quantities in the 2029 to 2031 timeframe. General Matter’s DOE contract, if executed successfully, adds another potential Western source.

The competitive question for Centrus is whether it can establish commercial relationships with advanced reactor fuel programmes during the 2027 to 2031 window when it is the only or primary available domestic HALEU source, creating long-term supply agreements that lock in customer relationships before the competitive market becomes more crowded.

Competitive landscape table

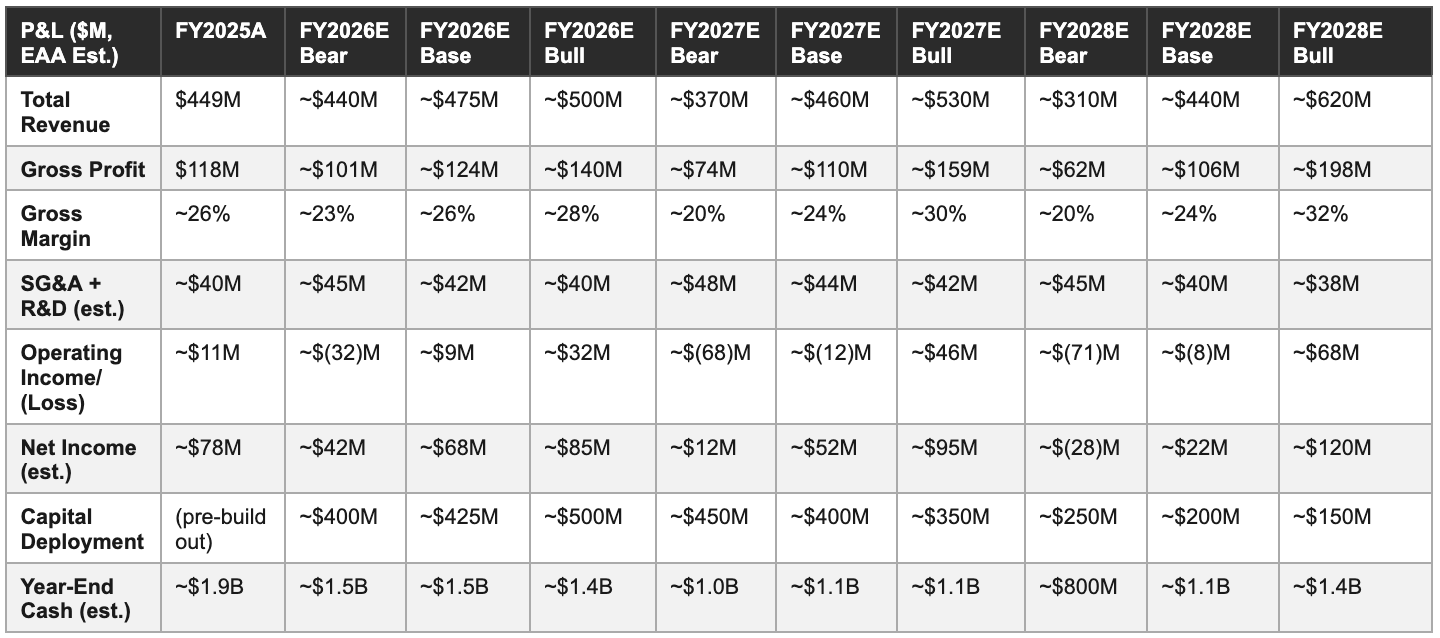

10. Forward Financial Model: Bear / Base / Bull Through FY2028

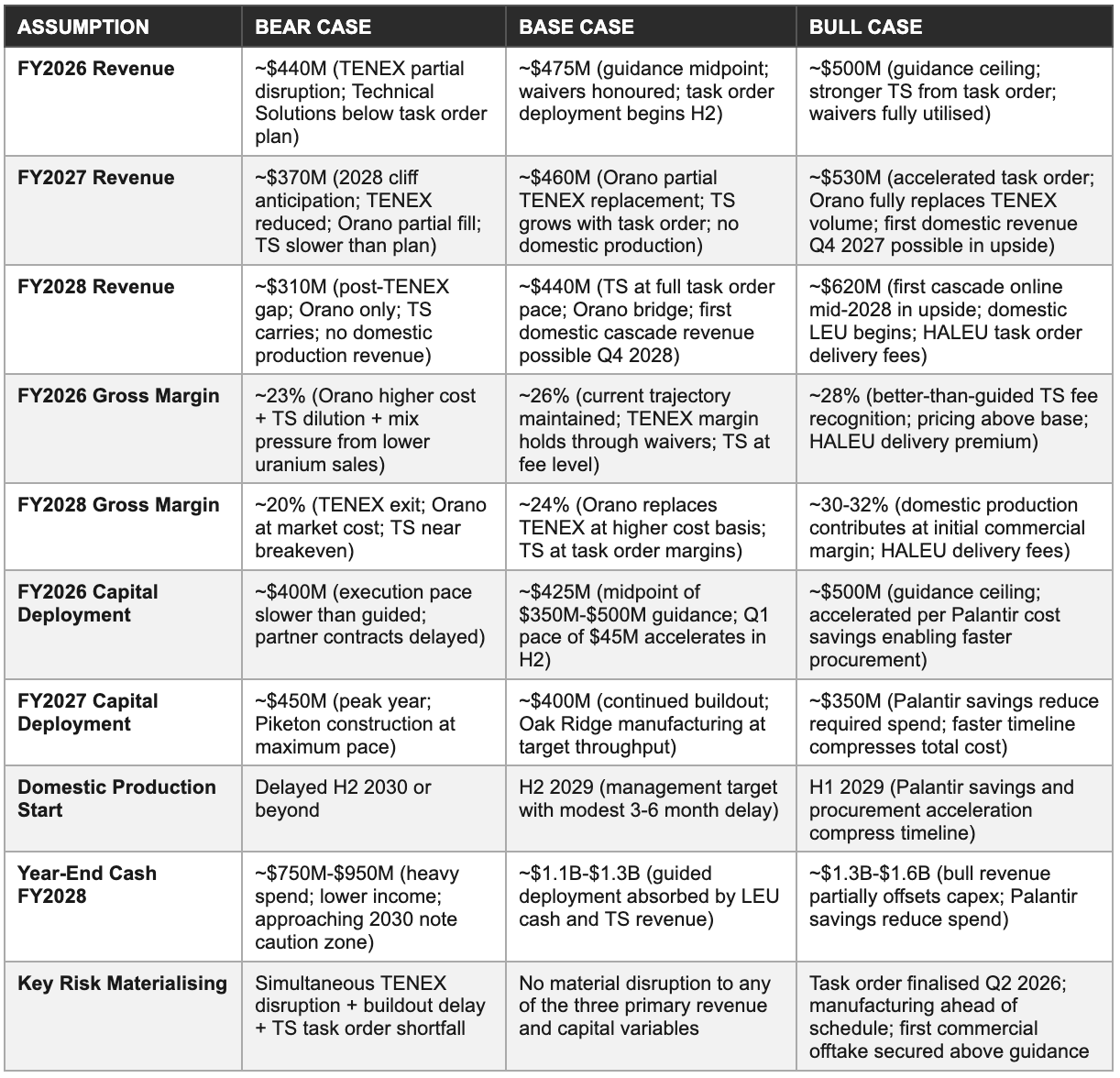

The three-scenario model addresses a business in structural transition: a profitable brokerage operation winding down as its primary cost-advantaged supply contract expires, a capital-intensive buildout consuming cash through 2029, and a government contract revenue stream growing as DOE appropriations deploy. The bear case is defined by the gap between TENEX expiry and domestic production that the Orano relationship alone cannot bridge. The base case requires TENEX contract integrity through 2028 and the 2029 first-cascade target to be met within one year of schedule. The bull case requires the buildout to accelerate relative to current guidance, producing domestic revenue before the full severity of the post-TENEX trough is felt.

Scenario assumptions

Three-year P&L projection

The 2027-2029 revenue trough: What it looks like and why it is not a distress signal

The revenue trajectories in all three scenarios exhibit a trough in FY2027 and FY2028 relative to FY2025 and FY2026. In the base case, FY2027 revenue of approximately $460 million reflects the beginning of the TENEX wind-down as the final year of waiver-covered deliveries completes, partially offset by growing Technical Solutions revenue from the DOE task order deployment. FY2028 in the base case sees LEU brokerage revenue fall materially as TENEX deliveries cease, with Technical Solutions carrying a larger share of the reduced total.

The revenue trough does not represent a business in distress, it represents a business at the peak of its capital deployment cycle in the year before its primary new revenue engine comes online. The analogy to other capital-intensive businesses in transition is useful: a pipeline company building a new trunk line will show lower free cash flow in the construction years and higher free cash flow once tariffs begin flowing.

The answer in the base case is yes: the $1.9 billion starting cash position, reduced to approximately $1.1 billion by end-FY2028 after capital deployment, retains sufficient buffer to address the 2030 convertible note maturity and fund the additional cascade additions required to convert the first-cascade proof of concept into commercial-scale revenue generation. The answer in the bear case is more qualified: the end-FY2028 cash of approximately $800 million to $950 million leaves less room for the 2030 note maturity and the continued buildout capital requirements of 2029, and creates a scenario where the ATM programme may need to be drawn to bridge the gap between the note maturity and the commercial revenue ramp.

The answer in the bull case is comfortable: the accelerated revenue from early domestic production and the task order cost savings reduce cash consumption through FY2028 and enter the 2030 maturity horizon from a position of greater financial strength.

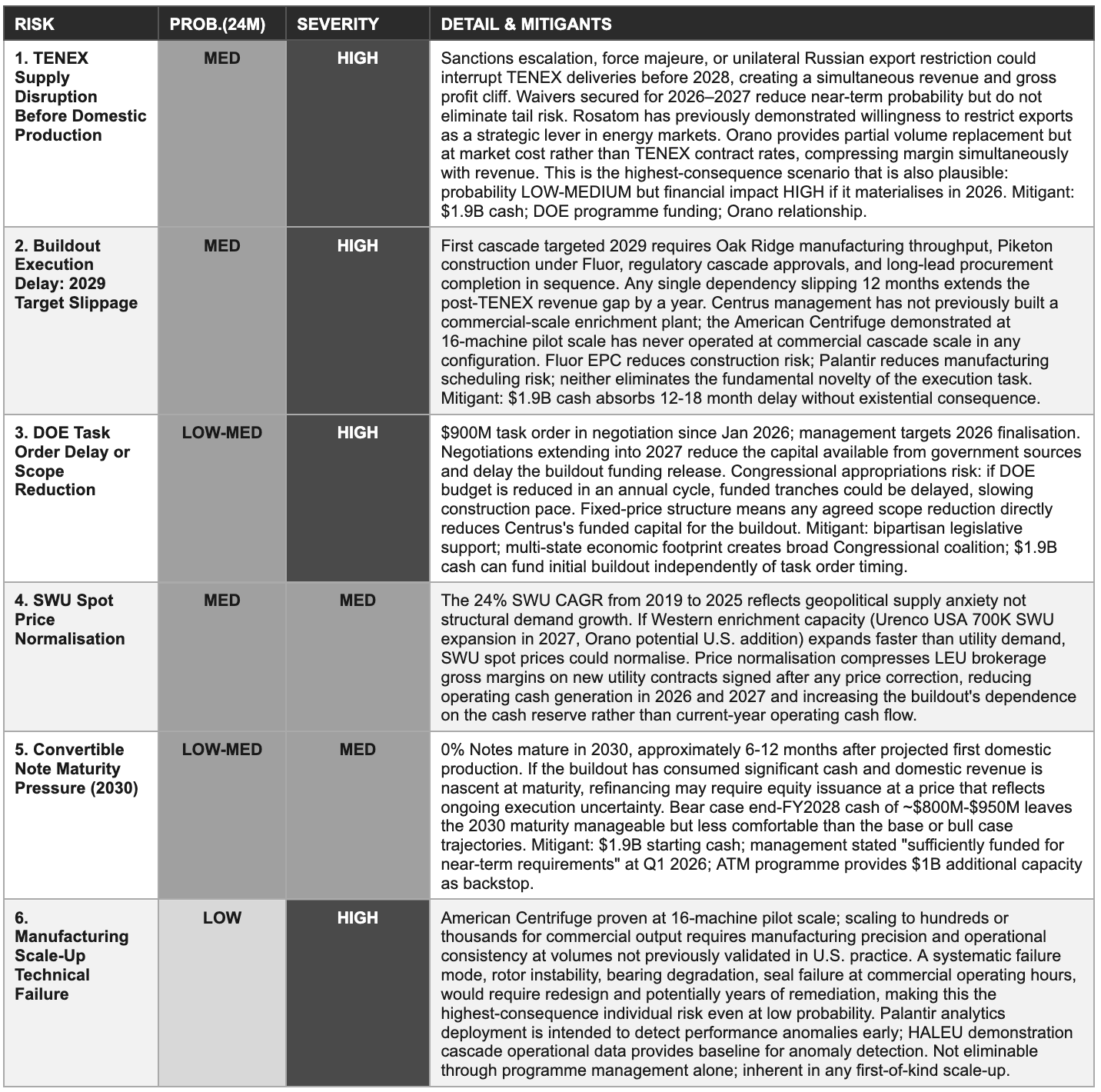

11. Risk Matrix

Each risk below is a specific variable whose outcome determines which of the three scenarios in Section 10 is realised. Probability reflects the likelihood of a significant negative outcome within 24 months; severity reflects the degree of long-term impairment if it materialises. Risks are ordered by the combined weight of both dimensions.

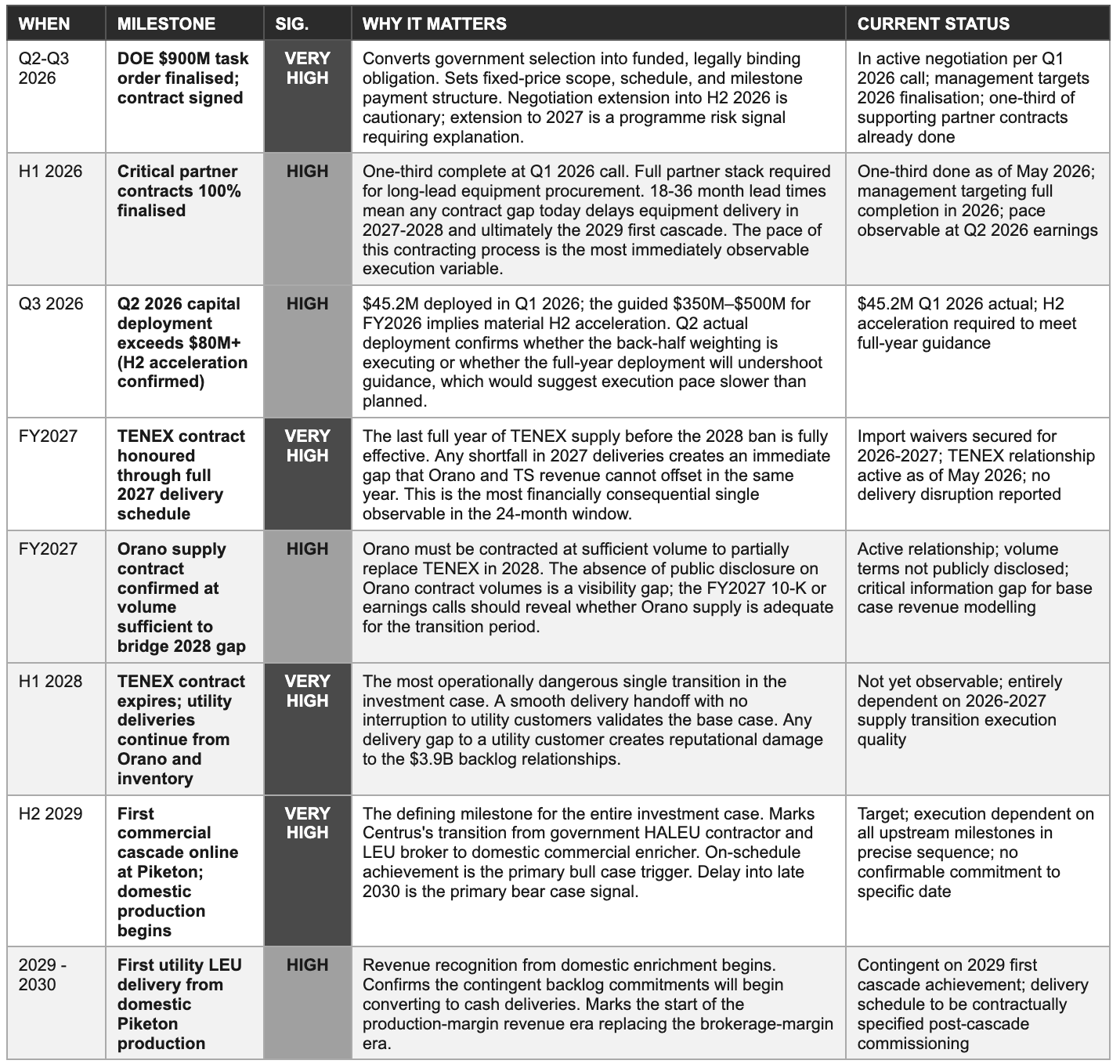

12. Milestone Tracker

The milestones below are the specific observable proof points distinguishing the base case from the bear and bull cases across the 2026 to 2030 horizon. The two highest-stakes near-term observations are the DOE task order finalisation and the FY2027 TENEX delivery record; everything else is secondary until those two variables are resolved. The scorecard condenses the analytical conclusions from the preceding twelve sections into a single-reference framework.

Milestone Tracker: 2026-2030

13. Investment Scorecard & Opinion: Bull, Base, and Bear Cases

What follows is the analytical view as of May 2026. The bull case requires believing that an industrial programme forty years in development can be executed on a three-year timeline by a management team that has not previously built at this scale, supported by a government counterparty that has not previously funded domestic enrichment at commercial scale.

The bull case: Four pillars

The first pillar is the HALEU monopoly window. Centrus is the only U.S.-operational HALEU producer with a demonstrated track record and an NRC licence. The DOE has formally selected Centrus for a $900 million HALEU expansion task order. The NNSA has declared intent to sole-source certain enrichment without competitive bidding. These positions are regulatory and operational, competitors cannot occupy them regardless of capital invested on any near-term timeline.

The window represents a three-to-five year period in which Centrus is the practical monopoly domestic supplier to a market that is legislatively mandated to transition away from Russian supply. The commercial value depends on how quickly advanced reactor deployments materialise and how effectively Centrus converts the government HALEU mandate into commercial utility contracts at pricing above production cost.

The second pillar is balance sheet strength qualitatively different from any prior attempt at this programme. The $1.9 billion unrestricted cash position, zero ATM drawdown, and zero-coupon 2030 notes provide financial runway through the most capital-intensive period without requiring immediate market access. The USEC predecessor failed partly because it was executing the same programme from a chronically stretched balance sheet that had no capacity to absorb construction delays or cost overruns.

The current Centrus balance sheet can absorb a twelve-month buildout delay and a 20% cost overrun without approaching a capital constraint, a statement that USEC could not make at any comparable stage. This capital adequacy changes the risk profile of the programme in a fundamental way: the consequence of execution delays shifts from existential to expensive, and from expensive to manageable.

The third pillar is the policy permanence of the demand catalyst. The Prohibiting Russian Uranium Imports Act requires Congressional action to reverse. The bipartisan political consensus behind domestic nuclear energy, driven by energy security, clean power generation, and advanced manufacturing employment in multiple swing states, is as durable as any energy policy environment in the current political landscape.

The DOE’s $3.4 billion sector-wide enrichment commitment, the NNSA’s operational dependency on domestic enrichment, and the multi-state economic footprint of the buildout programme create a policy architecture that is more durable than a single administration’s preference. The practical risk to the programme is delay rather than reversal, and the cash buffer is designed specifically to absorb the delay risk.

The fourth pillar is the utility backlog as evidence of commercial conviction expressed in contractual form. The $3.9 billion total backlog signed by utility customers is not guaranteed revenue, but it is powerful evidence that the customers Centrus has served for decades have pre-committed to domestic enrichment supply at a scale that validates the commercial logic of the buildout. Utilities sign decade-long supply commitments with counterparties they consider reliable and programmes they consider realistic. The utility backlog is the market’s revealed preference for domestic enrichment, expressed commercially before the first domestic SWU has been produced. It validates the demand side of the equation even as the supply side remains subject to execution risk.

The bull case does not require Centrus to dominate global enrichment. It requires Centrus to be the preferred U.S.-owned domestic enrichment source for a market that has legislatively eliminated the principal alternative supplier. That is a substantially more achievable condition than building a globally competitive enrichment business from zero capital.

The base case: Execution without acceleration

The base case is that management delivers on FY2026 guidance of $450 million to $500 million in revenue, the TENEX contract is honoured through its full 2028 term with waivers intact, the DOE task order is finalised during 2026, and the first commercial cascade at Piketon comes online approximately on the 2029 schedule, perhaps the second half of 2029 rather than the first half, reflecting the normal tendency of complex first-of-kind industrial projects to slip modestly from optimistic initial targets.

Under these conditions, FY2027 and FY2028 revenue reflects the TENEX wind-down and the Orano partial replacement, with Technical Solutions revenue growing as the task order is deployed, before domestic enrichment revenue begins its ramp in 2029 and 2030. The cash position remains adequate through the trough: starting from $1.9 billion, absorbing $350 million to $425 million per year of capital deployment, and generating declining but positive operating cash flow from the LEU segment through 2027, the base case end-FY2028 cash position of approximately $1.1 billion is sufficient to address the 2030 convertible note maturity without additional capital market access under normal refinancing conditions.

The base case at the current trading range midpoint of approximately $200 to $260 per share does not offer exceptional returns, it represents guidance that the market has already partially priced in at the range midpoint. The investment thesis for a base-case-only investor rests primarily on the option value embedded in the bull case scenarios: GLP-1 companion analogies aside, the first successful domestic cascade delivery in 2029 is the catalyst that converts the stock’s narrative from “execution risk discount” to “domestic infrastructure asset premium,” a re-rating that could be material regardless of whether revenue surprises on the upside. The base case is essentially an underwrite of the downside protection, the $1.9 billion cash buffer and the utility backlog provide a floor, while the bull case provides the upside.

The bear case: The three-way squeeze

The bear case is defined by the simultaneous materialisation of three independent risks: TENEX delivers below the contracted schedule in 2026 or 2027 due to sanctions escalation or logistics disruption; the DOE task order negotiation extends materially or its scope is reduced; and the Piketon first cascade slips to 2030 or beyond due to manufacturing throughput shortfalls or construction complications. Each of these individually is manageable with the $1.9 billion cash buffer.

The compound scenario, all three materialising in the same 24-month window, creates a revenue cliff (TENEX reduced, domestic production not started) combined with capital pressure (reduced government funding, higher buildout costs) that challenges even the $1.9 billion starting position if the compound duration extends through 2030 and 2031.

The 23.7% short interest as of May 2026 indicates that a meaningful portion of the institutional market is assigning non-trivial probability to the bear case or to an intermediate outcome worse than management guidance. Short sellers in this name are primarily expressing a view about execution risk and the adequacy of the capital buffer against a compound adverse scenario, concerns that are legitimate and that the bull case evidence does not eliminate.

The $1.9 billion cash buffer materially reduces the probability that the bear case becomes an existential solvency event, Centrus could absorb the three-way squeeze scenario without filing for bankruptcy, but a multi-year revenue gap and capital consumption above guidance would suppress the share price toward the lower end of the 52-week range or below, creating a painful outcome for investors at current prices even without a liquidity crisis. The distinction between a painful bear case and an existential bear case is precisely the cash buffer, and maintaining that buffer through disciplined capital deployment and conservative management of the fixed-price task order cost is the most important near-term management imperative.

The fourth specific bear concern is the institutional precedent from the programme’s history. The American Centrifuge absorbed more than a billion dollars in combined capital over two decades under USEC without reaching commercial scale. Every prior programme generation produced optimistic timelines and then missed them. The current management team has a better track record on the HALEU demonstration phases, but the demonstration phases are qualitatively different from commercial build: they involve a defined small number of machines, a defined government client, and a cost-plus economic structure that removes the cost overrun risk that a fixed-price commercial build introduces.

Investors who weight this prior appropriately will assign a wider distribution to the 2029 timeline estimate and a higher probability to the 2031 to 2032 scenario than management’s guidance implies. The question if the current trading range already compensates for it, which at the lower end of the 52-week range it arguably does.

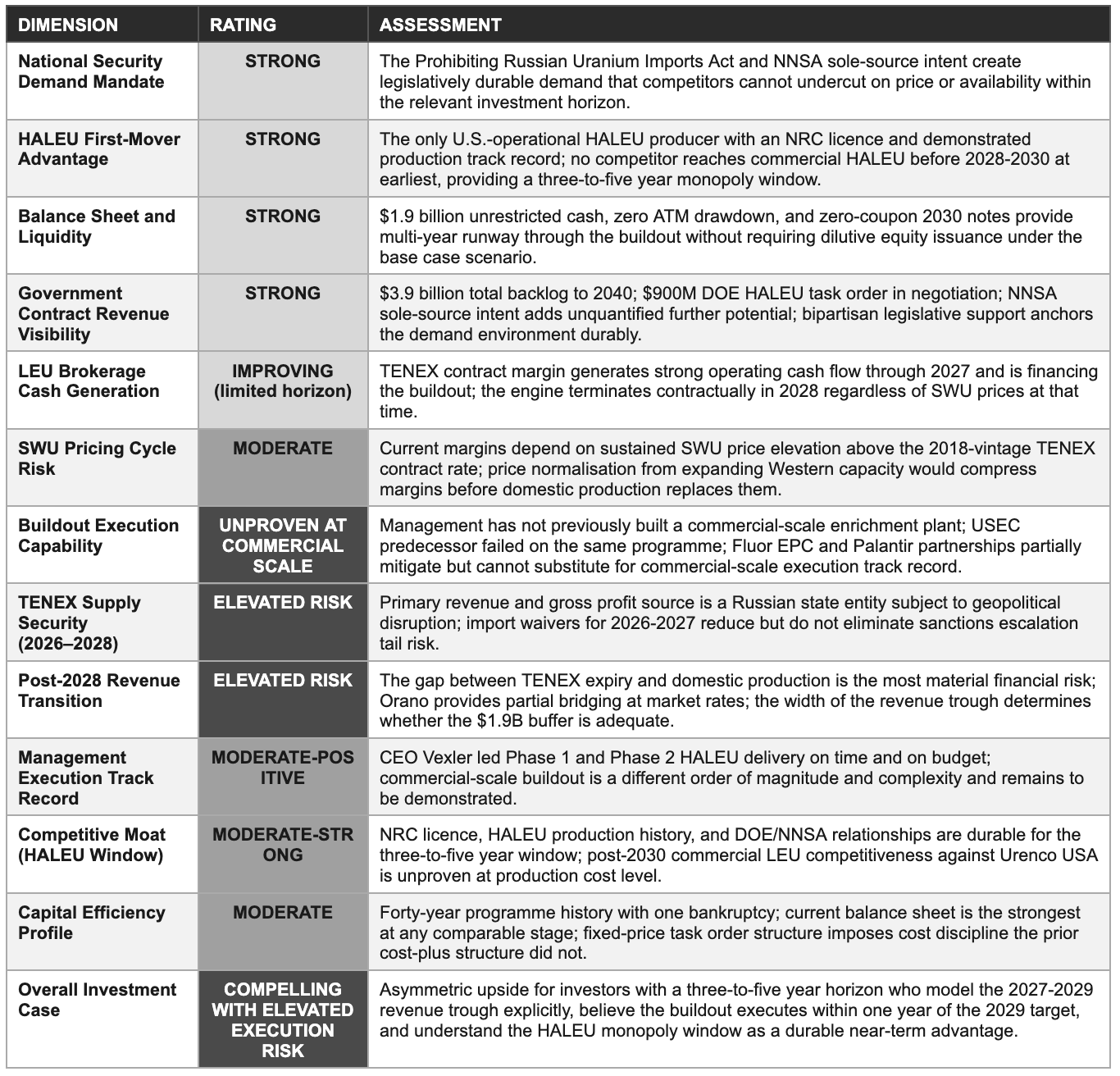

Investment scorecard

The bottom line

Thirteen sections of analysis converge on the same conclusion: Centrus Energy holds an industrially unique position that the market has oscillated between pricing as a domestic monopoly infrastructure asset and pricing as an execution-risk industrial long shot. Both framings contain truth, and both are supported by evidence rather than sentiment. The HALEU monopoly window, the legislative demand mandate, the utility backlog, and the $1.9 billion cash buffer are real advantages that competitors cannot replicate on any timeline shorter than three to five years.

The forty-year development history, the TENEX supply cliff, the post-2028 revenue trough, and the absence of commercial-scale enrichment execution precedent in the current management team are real risks that the balance sheet buffer softens but cannot eliminate.

The investment discipline required to own Centrus at current prices involves four commitments: a multi-year holding horizon of at least three to five years; an explicit model of the 2027 to 2029 revenue trough that resists reading the $3.9 billion backlog as uninterrupted revenue visibility; an honest probability-weighted assessment of whether the buildout executes within two years of the 2029 target; and conviction that the bipartisan policy environment supporting domestic nuclear fuel independence is more durable than a single administration cycle.

Investors who meet all four conditions, and who have sized the position appropriate to the execution risk, may find that the current trading range provides an unusual entry point into the only domestic uranium enrichment infrastructure build of commercial scale attempted in the United States since the Cold War era. The narrative shift that converts the stock from execution-risk discount to domestic infrastructure premium will be observable, the 2029 first cascade is the catalyst, but the price at which investors establish exposure will be determined in the months and quarters before that milestone, not after it.

Sources

All information is sourced from publicly available materials believed to be reliable as of May 2026. Primary sources include: Centrus Q4 2025 earnings release (Feb 2026, PRNewswire); Centrus Q1 2026 earnings release and 8-K (May 2026, SEC EDGAR); Q4 2025 earnings call transcript (Feb 2026); Q1 2026 earnings call transcript (May 2026); company 10-K filed Feb 2026 (SEC EDGAR); company 10-Q filed May 2026 (SEC EDGAR); DOE press releases (Jan 2026); Centrus press releases (Sep 2025, Dec 2025, Jan 2026, Apr 2026, May 2026); Morningstar (May 2026); Yahoo Finance (May 2026); StockTitan (May 2026)

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Centrus Energy, Corp. (NYSE: LEU) or any other security. All information is sourced from publicly available materials believed to be reliable as of May, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.