Delcath Systems Inc.

Scaling Liver Therapy into an Oncology Platform

Purpose of the Analysis

This isn’t about today’s valuation, it’s about owning a scalable oncology platform before the market realizes it’s no longer just a device story.

This report presents a comprehensive, long-term investment thesis on Delcath Systems Inc. The objective is not to value the business on current revenues, but to analyze the structural, technological, and strategic characteristics that may enable Delcath to evolve from a niche FDA-approved therapy into a scalable procedural platform in liver-directed oncology.

Rather than offer a short-term valuation view, this analysis investigates Delcath’s therapy platform, business model, leadership, regulatory positioning, commercial ramp, and long-term clinical expansion strategy. The intent is to frame the investment not around price targets or volatility windows, but around platform durability, procedural adoption, and strategic optionality.

Delcath represents a distinct type of opportunity, one where risk is high, but the potential rewards are nonlinear and grounded in tangible, platform-level leverage. This thesis is meant to provide the foundation for building long-term conviction.

Table of Contents

Corporate Profile

Founding & Evolution

Company Overview

Management & Leadership

Business Model & Commercial Strategy

Therapy Platform & Core Products

Indications & Pipeline Expansion Strategy

Market Opportunity

Regulatory & Reimbursement Dynamics

Competitive Positioning & Differentiation

Clinical Risk & Executional Challenges

Biotech Operating Context

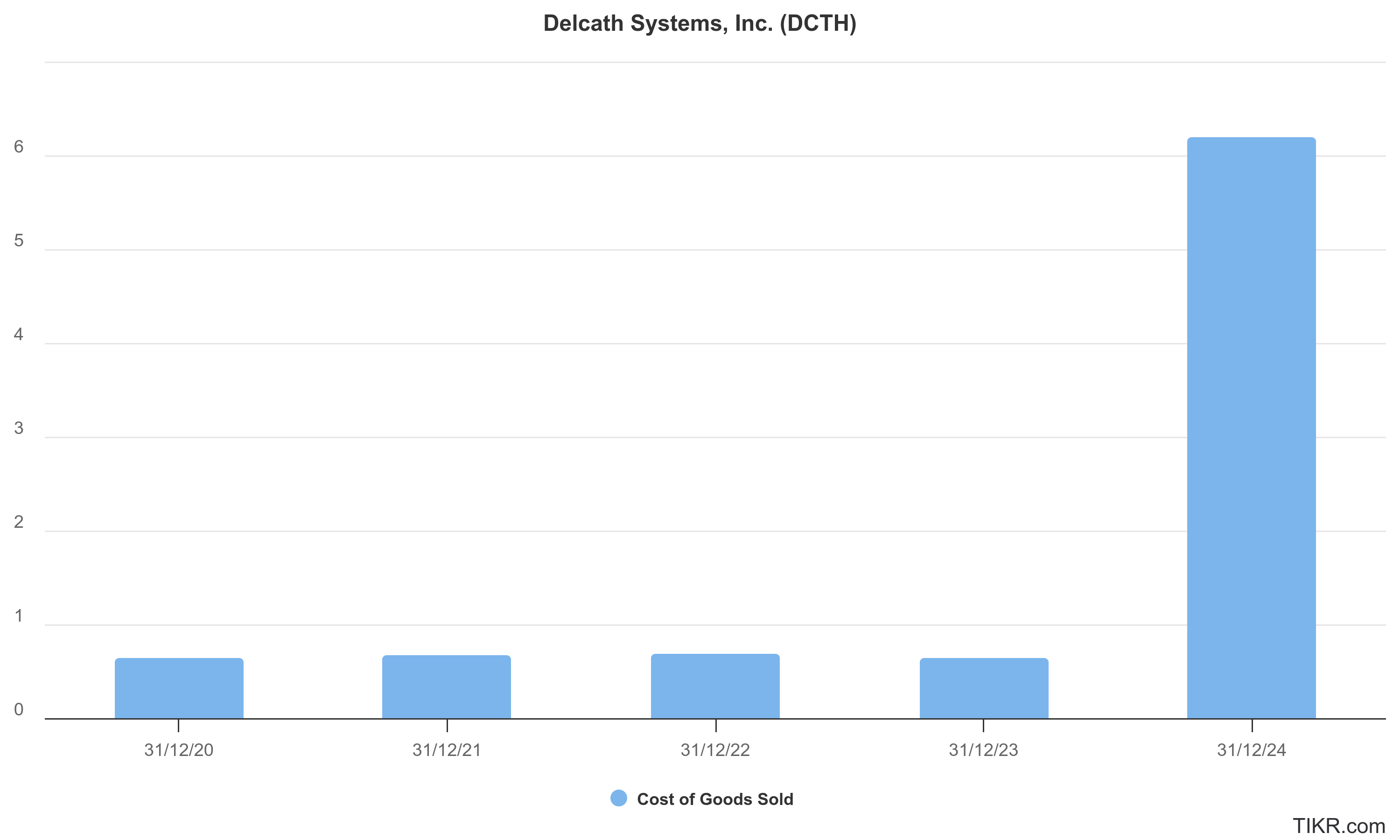

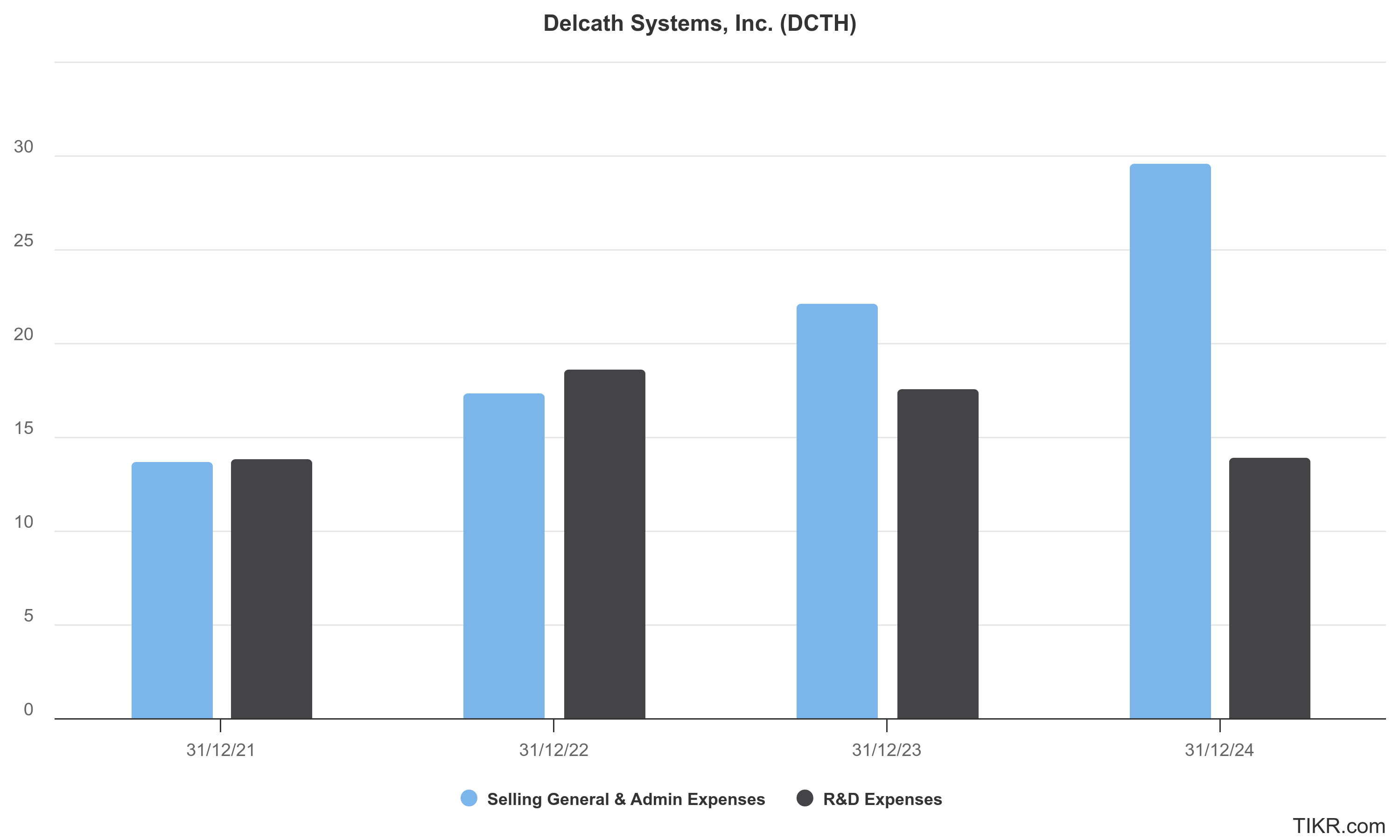

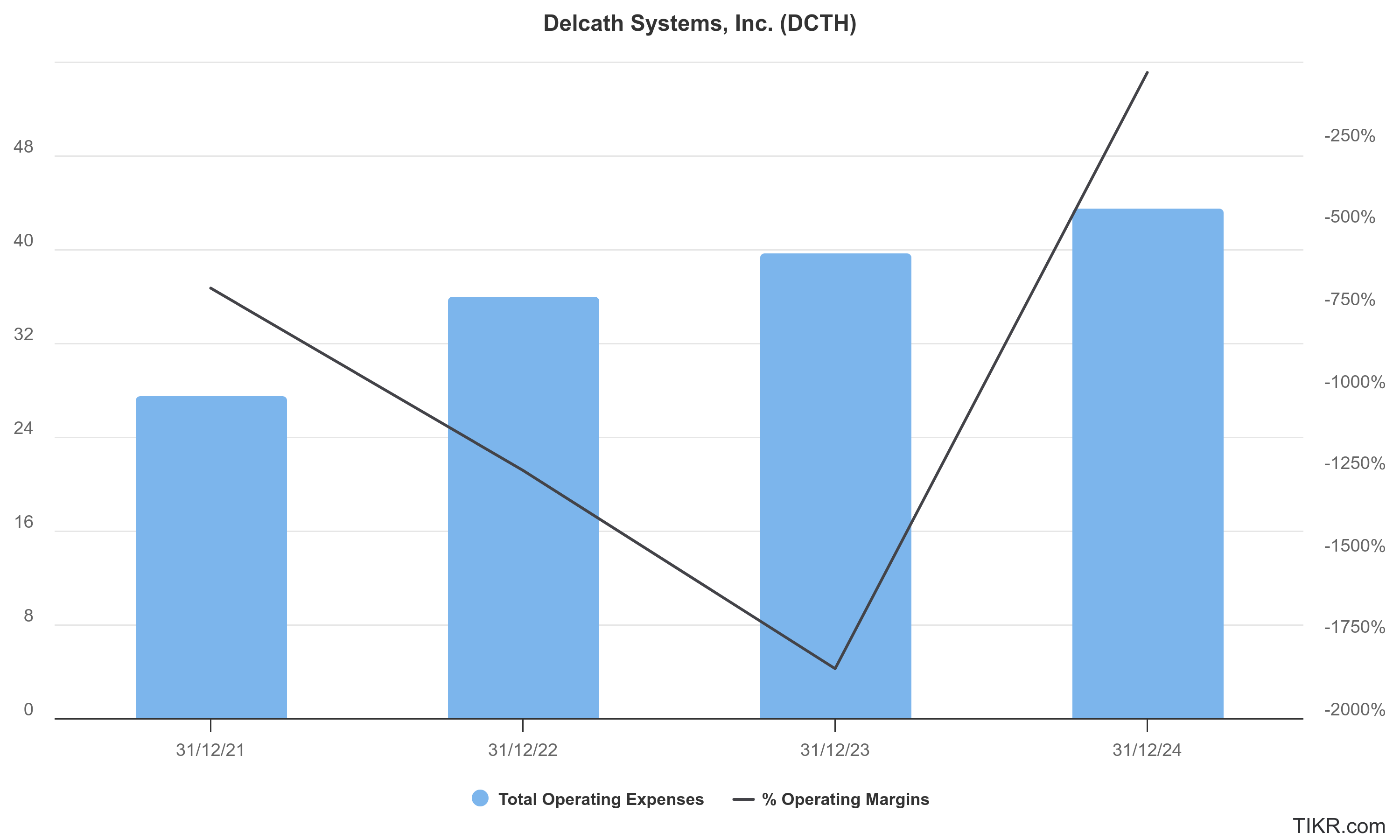

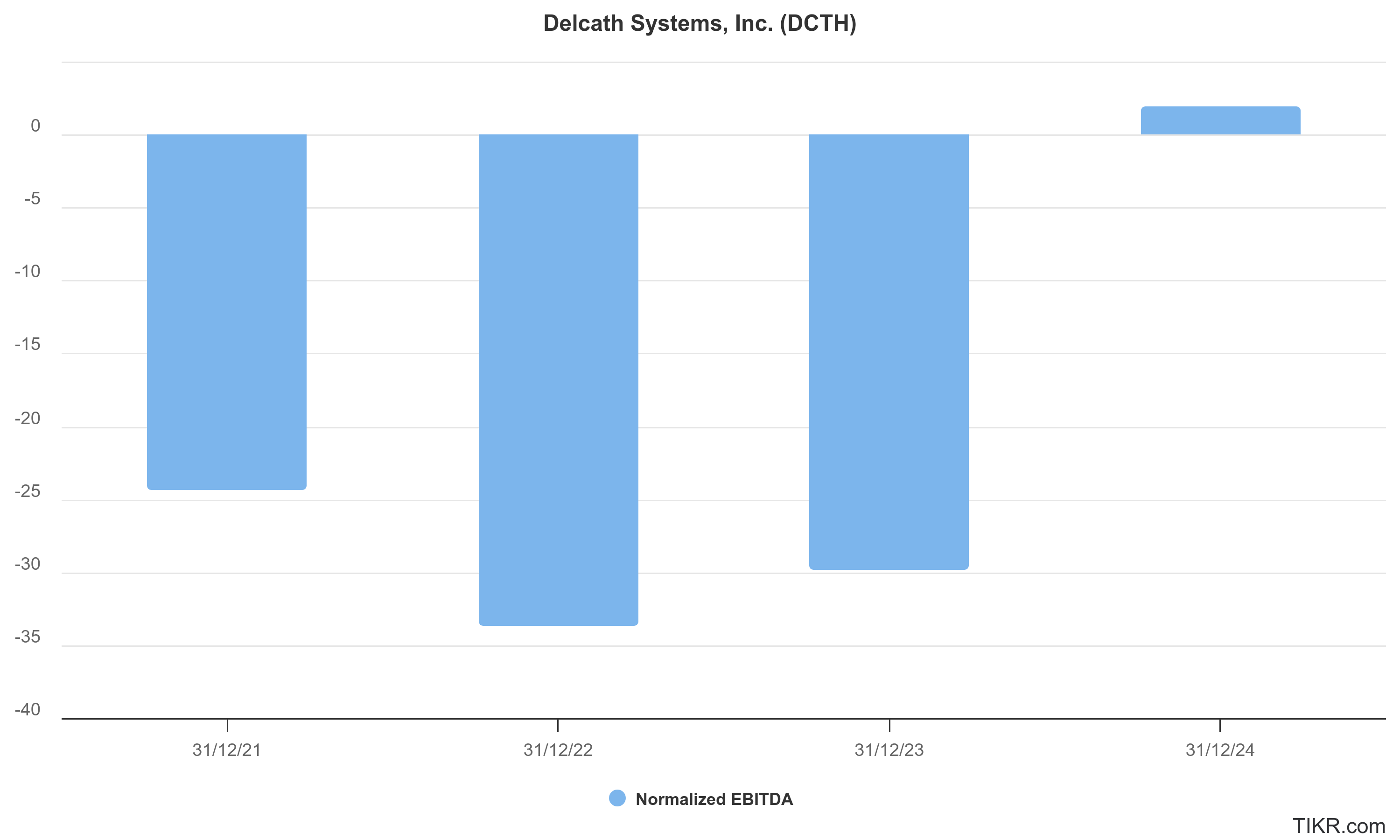

Financial Profile & Capital Allocation

Long-Term Strategic Outlook

Opinion & Target View

Conclusion

Acknowledgements & Disclaimer

1. Corporate Profile

Delcath Systems Inc (NASDAQ: DCTH) is a specialty pharmaceutical company focused on developing and commercializing innovative oncology therapies, primarily through its proprietary drug delivery platform designed to target liver cancers. Their business model centers on advancing breakthrough treatments that improve efficacy while minimizing systemic side effects, aiming to address significant unmet medical needs in oncology.

By leveraging a unique technology that isolates and delivers high-dose chemotherapy directly to the liver, Delcath promises to offer new hope for patients with difficult-to-treat liver malignancies, positioning itself as a potential leader in targeted cancer therapies. For investors, the company represents a high-growth opportunity driven by clinical progress and expanding market potential within a critical segment of cancer treatment.

2. Founding & Evolution

This isn’t just a biotech turnaround, it’s the revival of a platform that’s spent two decades quietly solving one of oncology’s most intractable procedural problems.

Delcath Systems was founded with a singular goal: to transform how liver cancers are treated. Unlike traditional chemotherapy, which circulates through the entire body, Delcath aimed to deliver ultra-targeted, high-dose chemotherapy directly to the liver while sparing the rest of the body from toxic exposure.

The founding insight, that the liver’s unique vasculature could be isolated, treated, and reconnected in a single intervention, was both technically ambitious and clinically promising. It implied not just better cancer control, but potentially a better quality of life. In a field notorious for brutal trade-offs, Delcath’s proposition was simple: treat harder, harm less.

The company’s roots trace back to the late 1990s, when early prototypes of its percutaneous hepatic perfusion (PHP) system were in development. Initial years were focused on engineering a catheter-based delivery system that could perfuse the liver with high-dose melphalan while simultaneously filtering the blood to prevent systemic toxicity.

By the early 2000s, Delcath entered early clinical testing and regulatory engagement, positioning itself more as a “device-enabled pharma company” than a conventional oncology biotech. The dual identity, drug + device, would shape both its opportunities and obstacles in the years to come.

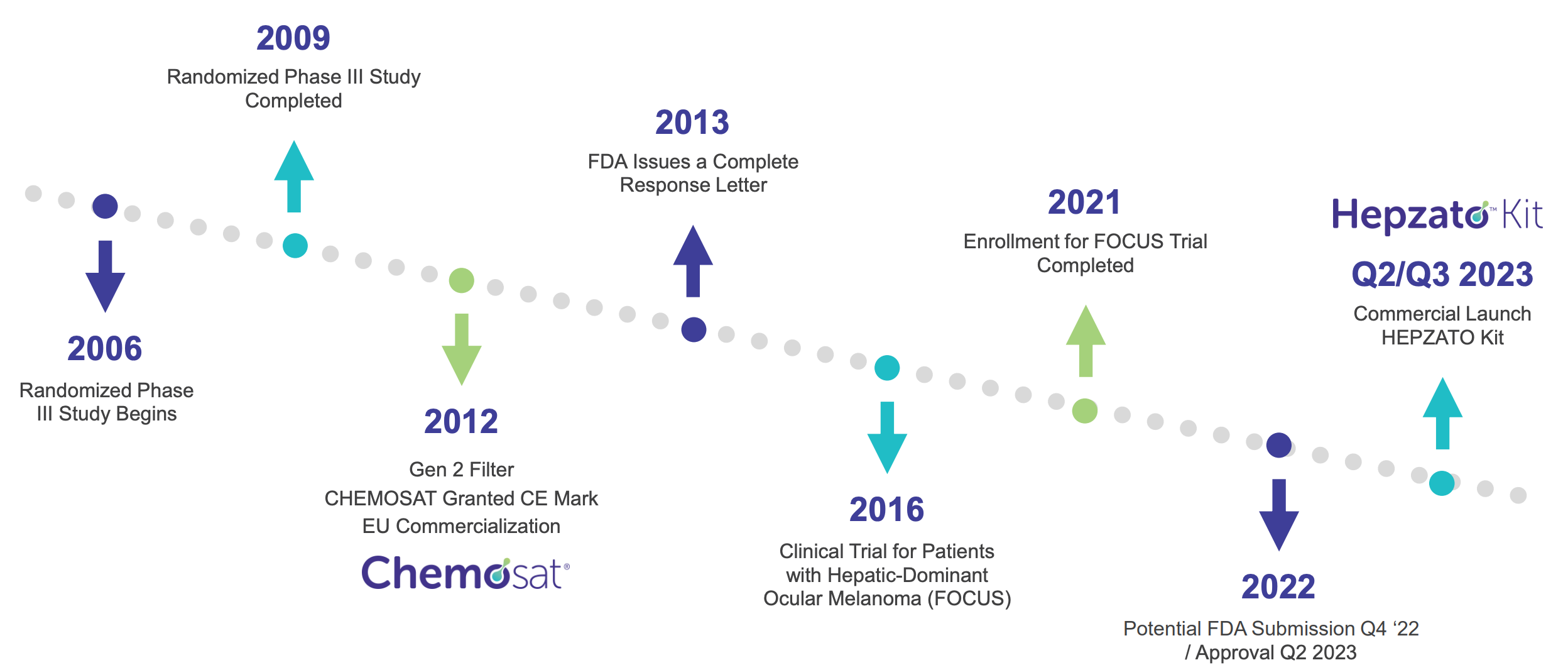

After nearly a decade of iterative development, Delcath gained European CE Mark approval in 2011 for its CHEMOSAT Hepatic Delivery System to treat liver-dominant tumors, primarily ocular melanoma metastases. But while this approval opened the door to European commercialization, it became clear that widespread adoption would be hampered by real-world hurdles: the procedure was complex, reimbursement systems were fragmented, and initial efficacy data were promising but not practice-changing.

In the U.S., the company struggled with the FDA, failing to secure approval in earlier attempts due to insufficient data and questions around safety profiles. By the mid-2010s, Delcath entered a prolonged period of retrenchment, share dilution, and strategic reassessment.

A major turning point came under the leadership of Gerard Michel, who was appointed CEO in 2020. Michel brought a pragmatic, execution-focused approach shaped by prior experience at Vericel and other healthcare companies. Under his tenure, Delcath pivoted away from pursuing narrow, niche approvals and instead set its sights on broader indications with real commercial potential.

The company refined its procedure, updated safety protocols, and launched the FOCUS trial, a pivotal study targeting metastatic uveal melanoma. In August 2023, Delcath finally secured FDA approval for HEPZATO KIT (a modernized version of the PHP system), marking a long-awaited regulatory milestone. For investors, this was more than a clinical win, it was a credibility restoration.

What followed was arguably Delcath’s most important strategic shift to date: the transition from an R&D-heavy medtech platform to a commercial-stage oncology company with a viable revenue engine and future pipeline optionality.

The initial U.S. launch of HEPZATO for ocular melanoma with liver metastases is only the beginning. Delcath is now enrolling a Phase 3 trial (the ALIGN study) in colorectal cancer liver metastases, a vastly larger indication. Management’s target is clear, to create a platform that delivers liver-targeted chemotherapy across multiple solid tumors, scaling commercial infrastructure along the way.

In a biotech landscape littered with failed pivots and shallow pipelines, Delcath’s persistence is notable. Its 25-year journey has been slow, nonlinear, and often frustrating. But its progress is now compounding. With FDA approval in hand, a commercial plan underway, a next-gen delivery system expected by 2025, and clear signals of clinical utility, Delcath stands on the verge of inflecting.

The company’s history is not just one of scientific innovation, but of strategic endurance, a case study in surviving long feedback loops and emerging with a product that might finally deliver what the original vision promised.

3. Company Overview

What if one FDA-approved procedure could redefine how we treat liver metastases across multiple tumor types?

Delcath Systems occupies a unique place in oncology: a platform company whose value isn’t in molecule discovery, but in how chemotherapy is delivered. This section explores the company's therapeutic focus, product mechanism, commercial strategy, and why its procedural approach to liver tumors may unlock broader clinical and financial leverage than traditional biotech models allow.

What Delcath does: Precision chemotherapy for liver tumors

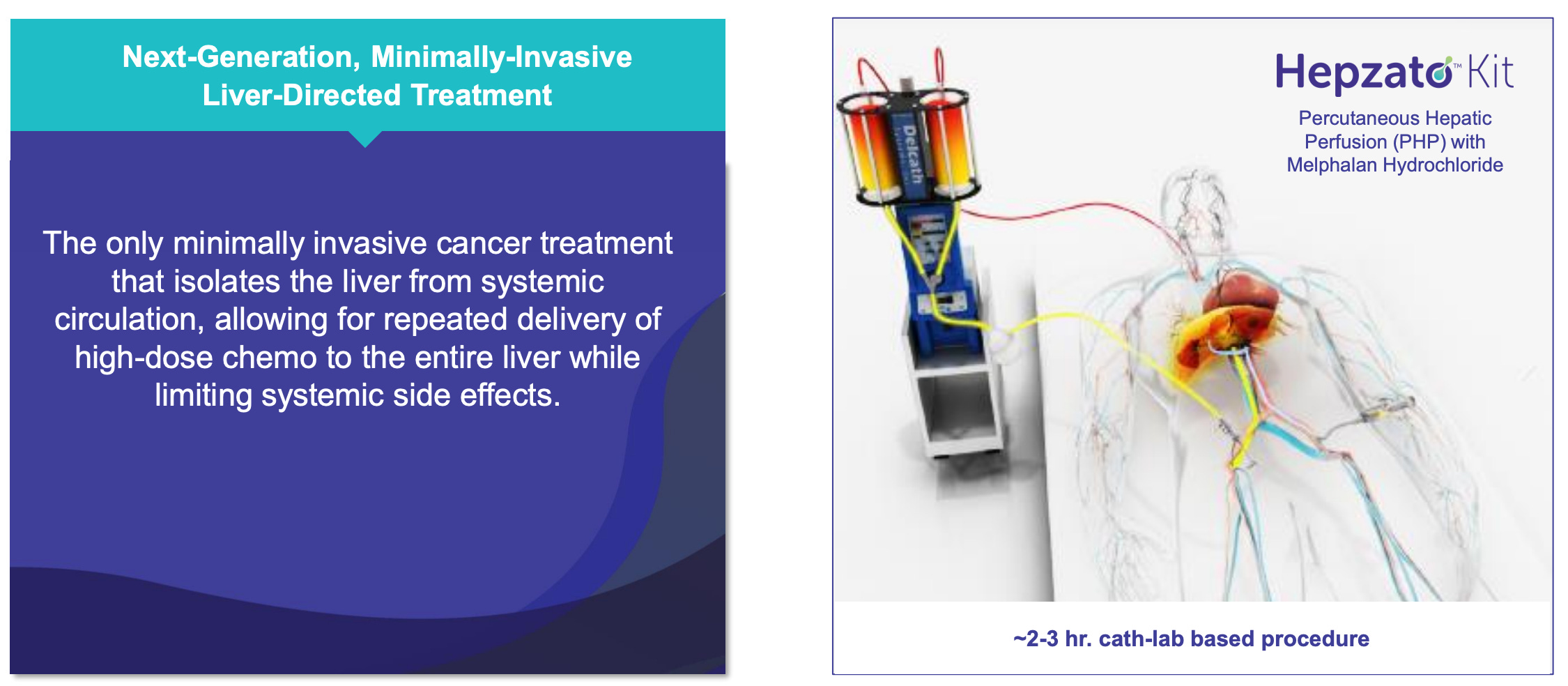

Delcath Systems Inc. is a U.S.-based oncology company that has developed and now commercializes a targeted drug delivery platform for liver-dominant cancers. Its flagship product, the HEPZATO KIT, enables physicians to deliver high-concentration chemotherapy directly to the liver, isolated from systemic circulation, through a procedure known as percutaneous hepatic perfusion (PHP). This approach allows for significantly higher drug exposure to liver tumors compared to systemic administration, while minimizing collateral toxicity to the rest of the body.

The treatment is not continuous, but episodic and repeatable, administered in a hospital setting under the supervision of interventional radiologists, oncologists, and perfusion teams. It integrates drug (melphalan), device (a dual-balloon catheter system), and filtration (extracorporeal hemofiltration) into a single therapeutic procedure. The HEPZATO KIT was approved by the FDA in August 2023 for the treatment of metastatic uveal melanoma (mUM) with liver metastases, a narrow but high-need indication that served as the company’s clinical and regulatory beachhead.

Delcath is not a traditional biotech developing a pipeline of molecules, nor is it a contract manufacturer or service provider. It operates as a procedure-driven oncology platform: a company whose core value lies in enabling hospitals to treat hepatic tumors more effectively by offering a regionally concentrated, FDA-cleared solution that is both reimbursable and clinically differentiated.

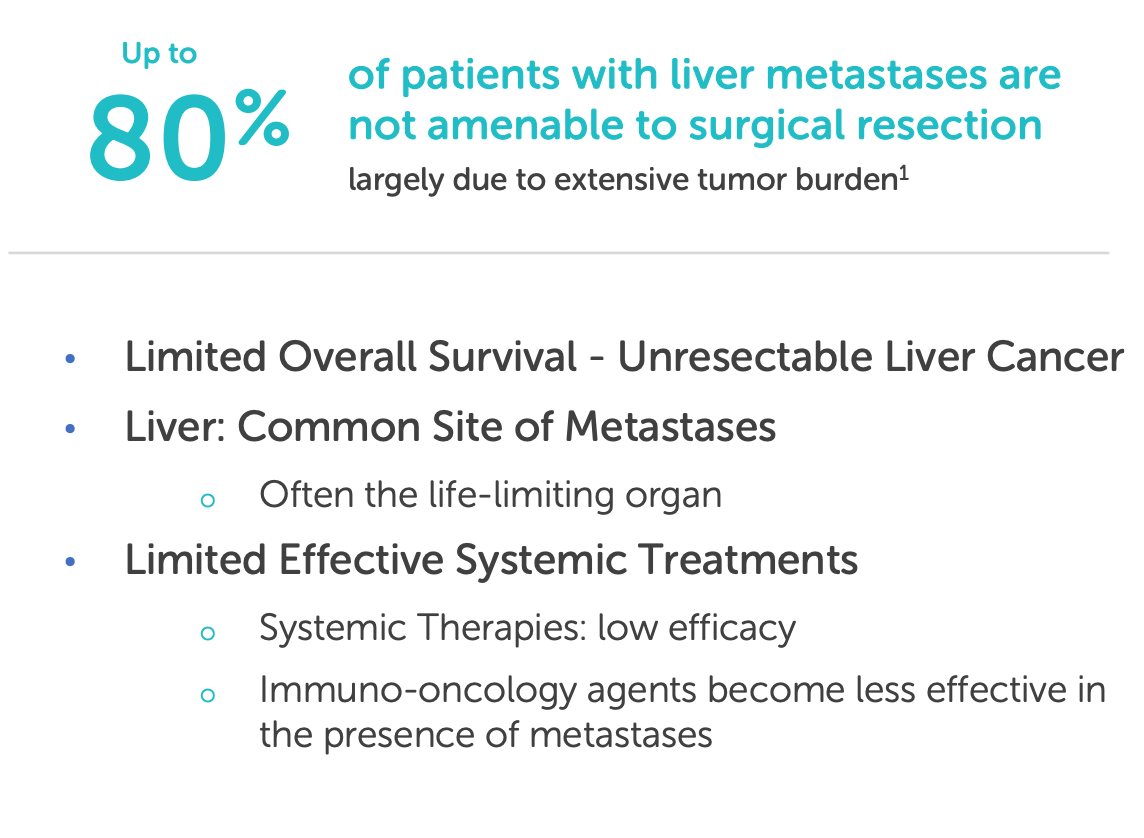

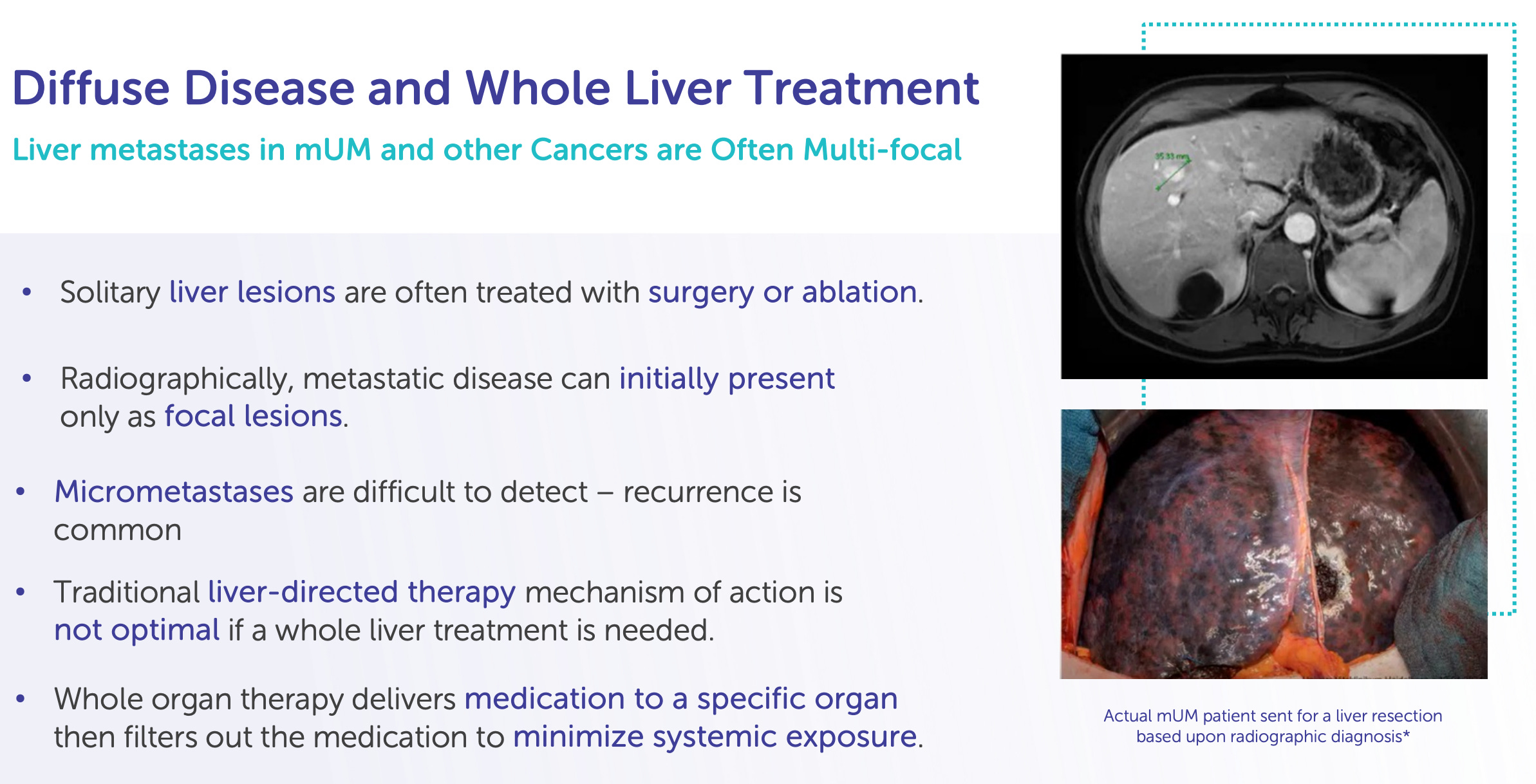

The problem: Liver-dominant metastases are a therapeutic dead zone

The liver is a frequent site of metastasis for multiple solid tumors, including colorectal cancer, ocular melanoma, cholangiocarcinoma, breast cancer, and pancreatic cancer. Yet systemic chemotherapy has long struggled to control liver-predominant disease due to two critical constraints: dose-limiting toxicity and heterogeneous drug delivery. Despite decades of innovation in systemic oncology, the liver remains one of the most challenging organs to treat effectively, particularly when the disease is confined to it but otherwise manageable.

For many of these patients, curative surgery is not an option, and systemic therapies offer poor hepatic control. In metastatic uveal melanoma (Delcath’s lead indication), over 90% of patients will have liver metastases as the dominant or sole site of spread, yet immune checkpoint inhibitors and small molecules have yielded limited responses. Even in colorectal cancer, where systemic options exist, patients with liver-only disease often experience hepatic progression long before other organs are affected.

The result is a mismatch between disease burden and therapeutic targeting: a liver-predominant cancer treated by whole-body drugs, often resulting in either underdosing the tumor or overdosing the patient.

The solution: A regionally targeted, systemically controlled platform

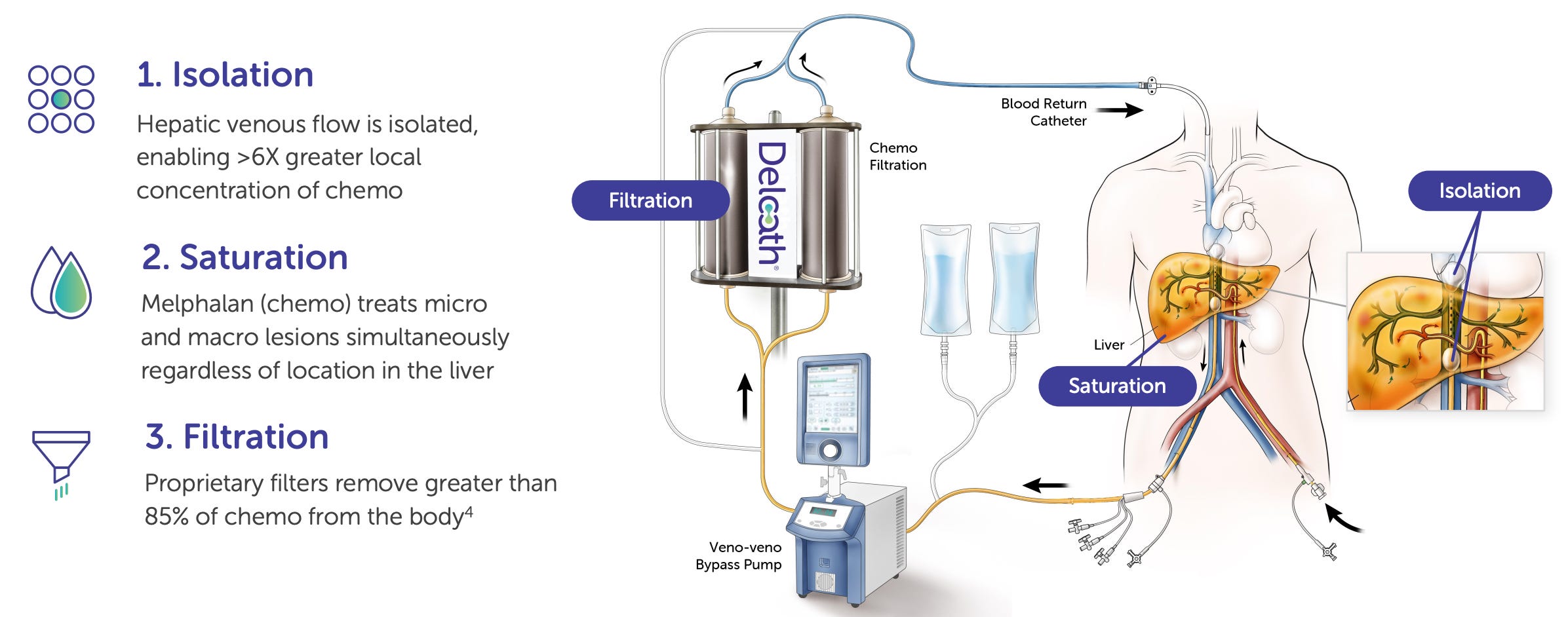

Delcath’s HEPZATO KIT is designed to solve this problem by isolating the liver during treatment, delivering a 3-5x higher localized dose of chemotherapy (melphalan), and filtering the blood before it reenters the general circulation. This is achieved via a sophisticated dual-balloon catheter that temporarily separates hepatic circulation from the systemic bloodstream, connected to an extracorporeal circuit that performs real-time hemofiltration.

The underlying mechanism is both mechanical and pharmacological: instead of discovering new drugs, Delcath is redistributing the pharmacokinetics of an existing one. Melphalan, a well-characterized alkylating agent, is used in high concentration within the liver for maximal tumoricidal activity, a practical application of “dose intensity by anatomy.” Once perfused, the drug is filtered out through a charcoal-based filter system to reduce systemic exposure. The net effect is a super-therapeutic dose to the liver, with subtherapeutic systemic levels.

This creates a unique therapeutic index: one that allows liver tumors to be targeted aggressively, while avoiding the hematologic or gastrointestinal toxicity that would otherwise occur at such doses. The technology has evolved over two decades and is now a fully integrated drug-device therapeutic platform regulated under the FDA’s NDA pathway. While the concept is not new, Delcath is the first to bring it to full regulatory and commercial fruition in the U.S. for cancer treatment.

Where Delcath stands today: Post-approval, early commercial phase

As of mid-2025, Delcath has completed the transition from a pre-revenue development-stage company to a commercial-stage oncology platform. The FDA approval of the HEPZATO KIT in August 2023, based on data from the FOCUS trial in metastatic uveal melanoma, represented the company’s first major regulatory milestone and has enabled its initial market launch in select U.S. academic and cancer centers.

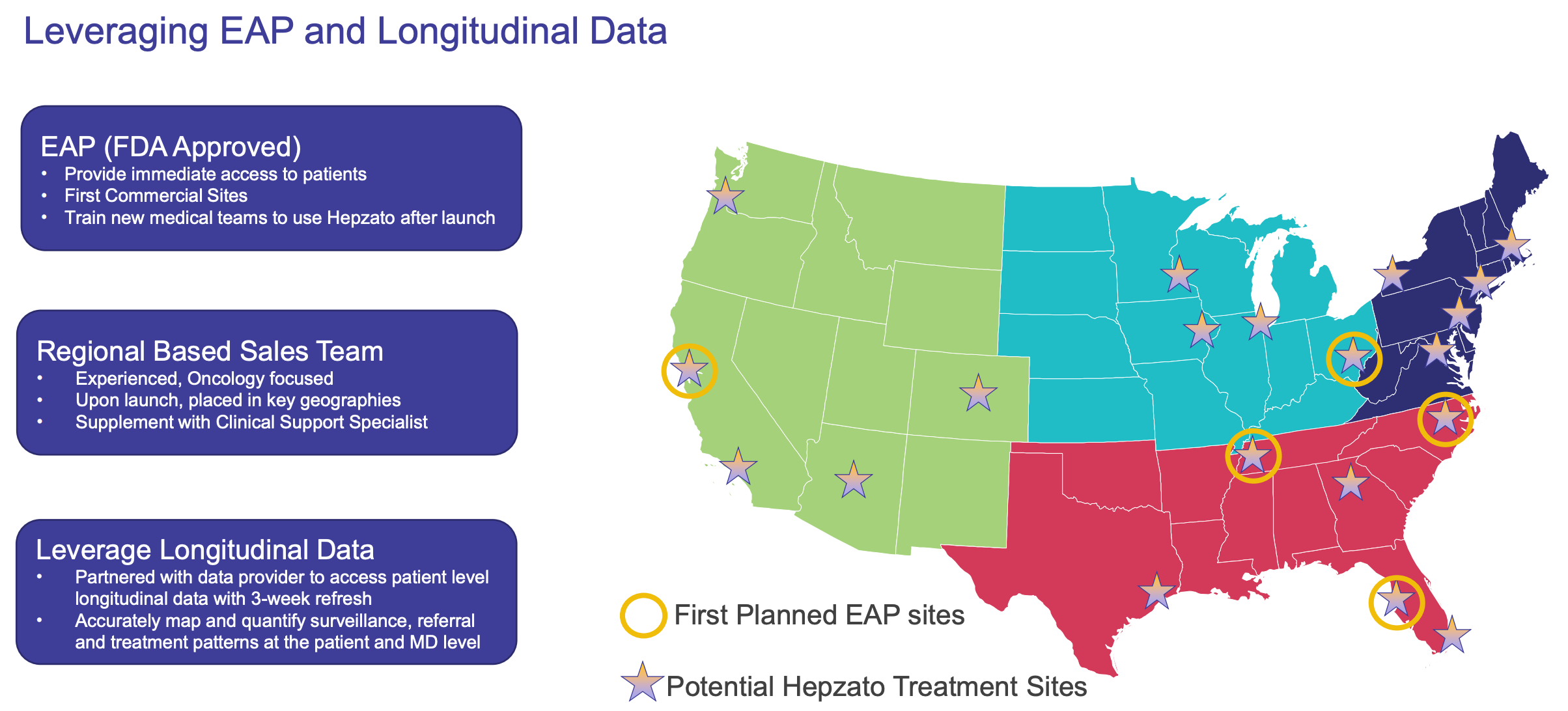

The company is now actively training physicians, onboarding institutions, navigating reimbursement dynamics, and building out field support, a classic early launch phase. Though adoption is expected to be measured given the complexity of the procedure and rare nature of the current indication, Delcath has already secured Category I CPT code assignment and is working toward broad payer coverage. Early demand signals from major liver oncology centers (e.g. MD Anderson, Memorial Sloan Kettering, Thomas Jefferson) suggest latent enthusiasm for liver-directed therapies that address gaps in current practice.

On the R&D front, the company is advancing the ALIGN Phase 3 trial in colorectal liver metastases (CRLM), which represents a vastly larger commercial opportunity. Enrollment is underway, and top-line data are expected in 2026 or early 2027. If successful, HEPZATO could become a standard of care for CRLM patients with unresectable, liver-dominant disease, a group that numbers tens of thousands annually in the U.S. alone.

Delcath has also begun development of a next-generation delivery system intended for commercial release in 2025. This upgraded kit will feature improved filtration efficiency, simplified setup, and increased operator consistency, all aimed at reducing procedural burden and expanding accessibility beyond top-tier interventional oncology centers.

At present, Delcath remains pre-profit, but is guiding toward cash flow break-even by 2027-2028, contingent on uptake in uveal melanoma, expansion into CRLM, and adoption of the next-gen kit. Cash runway and recent capital raises suggest a 2-3 year operational buffer, sufficient to navigate the commercial ramp and fund key clinical programs.

Strategic significance: A platform built for expansion, not a single indication

For long-term investors, the importance of Delcath lies not in its current revenue base, but in its positioning as a platform for liver-directed oncology. The company’s core value is its ability to deliver repeatable, liver-specific chemoperfusion across multiple tumor types and patient populations. With a single infrastructure and procedure, it can address liver metastases from colorectal, breast, pancreatic, ocular melanoma, and even primary liver tumors like iCCA and HCC, all of which share a common limitation: systemic drugs underperform in the liver.

Moreover, Delcath is entering this market at a time when interventional oncology is gaining momentum. Procedures like SIRT (Y90 radioembolization), TACE (chemoembolization), and ablation are increasingly integrated into cancer care pathways, but none offer what Delcath does: full-dose, systemically filtered chemotherapy in a repeatable, modular protocol. In this sense, Delcath is carving out a new niche that merges surgical precision with systemic pharmacology.

The timing also matters. Payers and physicians are increasingly focused on value-based oncology, therapies that meaningfully extend survival while minimizing toxicity and cost. Delcath’s therapy, though procedural, is potentially cost-saving when compared to extended systemic regimens that require months of therapy with modest hepatic control. Its product is hospital-based, high-margin, and structured for procedural billing, similar in reimbursement dynamics to SIRT or TAVR, offering durable pricing power and clinical integration.

In short, Delcath is not just a company with a device or a drug. It is a platform oncology company with a path to multiple indications, an addressable market in the billions, and a business model that, if executed properly, offers long-term revenue durability with margin expansion as procedure volumes scale.

Delcath is building more than a product, it’s constructing a procedure-based oncology platform. Its HEPZATO KIT represents the fusion of pharmacology, interventional technique, and hospital-based care, wrapped in a reimbursable, FDA-approved framework.

As the company expands indications and refines its delivery system, the core mechanism, liver-isolated chemoperfusion, remains central to its moat. For long-term investors, the real bet isn’t on one disease or product cycle. It’s on Delcath’s ability to scale a fundamentally new way of treating metastatic cancer where it lives.

Understanding the company’s strategic position sets the stage for evaluating the leadership team tasked with executing it.

4. Management & Leadership

In biotech, technology gets headlines, but leadership builds value. Delcath’s edge is execution, and its team is built to scale.

In the world of oncology platform companies, technical elegance is only as valuable as the team tasked with operationalizing it. For Delcath, the leadership bench is not just functional, it’s strategic. This section evaluates the management team not simply by credentials, but by fit: how each executive maps onto the company’s commercial, clinical, operational, and financial inflection points.

From CEO Gerard Michel’s capital discipline to Dr. Vukovic’s clinical rigor and Kevin Muir’s sales execution, Delcath’s leadership is arguably its most undervalued asset. In a sector riddled with scientific promise but executional fragility, this is a team built for precision, not just potential.

Gerard Michel - Chief Executive Officer

In biotech, especially in complex platforms that straddle device, drug, and procedure, the most important decision is often not the science , it's the steward. Executional failure, not scientific failure, is the dominant cause of value destruction in small-cap therapeutics companies. And in Delcath Systems, that execution rests on one person: Gerard Michel. He did not invent the technology, nor did he lead the early trials, but in a very real sense, he is the reason Delcath is now investable.

Michel is not a visionary scientist. He is not a capital-markets promoter. He is, by every measure, an operator, and Delcath is a company that needed exactly that. This is a story about fit: a 25-year-old platform technology finally matched with a CEO who understands what it takes to convert an elegant concept into commercial momentum. For long-term investors, Michel is not just part of the investment case, he is its operational core.

From strategy to the field: A career built on cross-disciplinary competence

Michel’s resume reads less like that of a typical biotech founder and more like that of a turnaround architect. With over 30 years of experience across biopharma, medtech, and corporate strategy, he has spent his career navigating complexity, both scientific and organizational. From early roles at Wyeth and Lederle Labs in sales and marketing, he transitioned to Booz Allen Hamilton, where he advised healthcare companies on commercial strategy and product development.

The most formative stretch of his career came in the C-suite of three mid-stage biopharma companies, NPS Pharmaceuticals, Biodel Inc., and Vericel Corporation, where he combined financial oversight with corporate development. At NPS, he helped reshape the pipeline and prepare the company for its eventual $5.2B acquisition by Shire. At Biodel, he worked through the economic and regulatory challenges of diabetes therapeutics. But it was at Vericel where Michel arguably earned his operator credentials.

At Vericel, Michel served as CFO from 2014 to 2020, where he played a central role in the company’s turnaround. He helped lead the acquisition of MACI, a marketed autologous cell therapy from Sanofi, and then restructured the company around this newly acquired commercial asset. Under his financial and operational leadership, Vericel shifted from R&D burn to revenue-generating growth, achieving break-even operations and building a high-margin niche around regenerative orthopedics. The stock rose over 1,000% during his tenure, not because of a pipeline breakthrough, but because of commercial execution and capital discipline.

The Delcath challenge: A company in search of a builder

When Michel took over Delcath in October 2020, the company had spent two decades developing a novel, but underutilized, therapy: regional chemoperfusion for liver tumors. The technology had earned CE Mark approval in Europe years earlier, and had shown promising but inconsistent results across academic centers. Yet Delcath had failed repeatedly to obtain U.S. FDA approval, burned investor trust with dilution, and suffered from a lack of clear commercial identity. It was, by most accounts, a company in search of structure, a scientific asset looking for an operator.

Michel inherited a platform with clinical data, but no market. Trials had been run but not harmonized. Payers didn’t understand the therapy. Physicians had to be trained from scratch. There was no CPT code, no formulary status, no field team, and a skeptical investor base. In short, it was a classic biotech limbo: too complex to fail outright, too fragmented to scale.

Michel brought a pragmatic re-foundation. He revised clinical strategy around a single, high-probability approval path: metastatic uveal melanoma (mUM), a rare cancer that nearly always metastasizes to the liver and lacks a systemic standard of care. This gave Delcath a clear regulatory narrative. He completed the FOCUS trial, engaged the FDA directly under the NDA pathway, and ultimately secured HEPZATO KIT approval in August 2023, the company’s first U.S. approval in over 20 years of existence.

Strategic clarity: From rare disease to procedural oncology platform

But Michel’s value to Delcath goes beyond the approval itself. His true contribution is strategic: re-framing Delcath not as a rare disease company, but as a procedural oncology platform. Under his leadership, Delcath is no longer a single-indication play. It is a system. And like all systems, it is built to scale.

The HEPZATO KIT now forms the commercial backbone. The ALIGN Phase 3 trial in colorectal liver metastases (CRLM) offers a clear expansion path into a multi-billion-dollar market. The next-generation delivery system, expected in 2025, will reduce friction at the procedure level, allowing more centers to come online. Michel is building a company that doesn't win by discovery, it wins by deployment.

This structure fits Michel’s style. He is not a biotech storyteller. In public communications, he focuses on center onboarding, CPT code integration, procedure training, and payer engagement. His earnings calls read more like operator briefings than capital raises. That sobriety has helped rebuild investor confidence in a platform many had written off.

Capital stewardship: A rare discipline in small-cap biotech

One of the most underappreciated aspects of Michel’s leadership is his capital discipline. Delcath under his tenure has avoided the kind of chronic dilution that often plagues clinical-stage biotech. In fact, despite achieving a U.S. FDA approval and initiating a Phase 3 trial, Delcath has remained lean: management headcount is modest, SG&A has scaled only in line with launch, and the company maintains tight control over cash burn. Michel has raised capital only when value inflection points justified it, and at better terms.

Moreover, Michel has built a non-promotional culture. There is no excessive use of stock-based compensation. No marketing fluff. No pie-in-the-sky projections about pan-cancer applications or AI-driven oncology. Just a clear, grounded thesis: train physicians, grow procedure volume, expand indications, improve the kit, reinvest in pipeline.

This approach is rare. In a sector where "platform" often means "perpetual pre-revenue optionality," Michel is building the opposite, a revenue-engineered system with defined economics, gross margin visibility, and a commercial moat rooted in procedural proficiency. It’s a model that may take longer, but has fewer points of failure.

Central to the thesis: Betting on execution, not just science

Ultimately, what makes Michel indispensable to the Delcath investment case is not that he believes in the platform, but that he knows how to run it. In platform therapeutics, particularly in interventional oncology, the CEO is often the business model. You’re not just betting on the science. You’re betting on a human system that can manage clinical data, payer relationships, procedure training, regulatory nuance, and logistics, simultaneously.

Delcath’s future depends on scaling a complex, high-value therapy through a fragmented and conservative U.S. hospital system. That’s not a scientific problem. It’s an execution problem. And Michel has done it before, at Vericel, at NPS, and now, step by step, at Delcath.

Investors searching for asymmetric biotech returns often chase the next molecule. But Delcath is different. The asymmetry here lies in executional inflection, the conversion of a long-languishing technology into a repeatable commercial engine. In that sense, Gerard Michel is not just a CEO. He is the de-risking mechanism for the entire investment thesis.

Executive Leadership Team

Martha S. Rook, PhD - Chief Operating Officer

Dr. Martha S. Rook brings over 25 years of technical and operational leadership spanning academic research, diagnostics, and biologics manufacturing, a background that positions her uniquely well to navigate the complexity of Delcath’s drug-device combination platform. Before joining Delcath in 2024, Dr. Rook served as Chief Technical Operations Officer at insitro, a machine learning-driven drug discovery company, where she led cross-functional responsibilities including quality systems, laboratory operations, project management, and research infrastructure.

Prior to that, she held the same title at Sigilon Therapeutics, where she oversaw the analytics, manufacturing, supply chain, and quality for a combination biologic-device product, giving her direct experience with regulatory, CMC, and logistics challenges similar to Delcath’s. Her earlier tenure at MilliporeSigma spanned 13 years, culminating in her role as Vice President and Head of Gene Editing & Novel Modalities, where she built and led a business unit supporting cell and gene therapy workflows from R&D to GMP manufacturing.

At Delcath, Dr. Rook serves as Chief Operating Officer, responsible for overseeing the company’s transition from clinical-stage to full commercial operations. Her role spans core technical functions, including manufacturing, supply chain, CMC strategy, quality systems, and commercial readiness, and she plays a pivotal role in scaling the HEPZATO KIT from a single-site launch product to a repeatable, high-throughput oncology procedure across U.S. and potentially ex-U.S. markets.

As the company prepares to roll out a next-generation delivery system in 2025, Rook is central to streamlining the procedure workflow, ensuring manufacturing robustness, and harmonizing supply chain logistics, all while maintaining the strict quality controls necessary for FDA-regulated combination products. Her operational oversight is especially critical as Delcath increases its site activation cadence and seeks to standardize treatment delivery in complex hospital settings.

Delcath’s business model depends on repeatable, procedure-based therapy delivery, a structure fundamentally different from oral drugs or infused biologics. Every treatment requires precise execution across hospital systems, making operational reliability a core source of value, not just a back-end function. In this context, the COO role becomes highly strategic. Dr. Rook’s background with combination products, supply chain scale-up, and biologic-device integration gives her direct leverage over Delcath’s ability to execute consistently across a growing network of oncology centers.

As Delcath moves toward broader market penetration, particularly with the anticipated launch of its next-generation delivery system in 2025, her leadership will be critical in reducing procedural friction, improving throughput, and ensuring that hospitals view HEPZATO not as a complex outlier but as a standardizable, system-ready intervention. For a platform whose long-term value hinges on adoption, reproducibility, and device-driven scalability, her function is not just operational support, it is core to the company’s go-to-market engine.

David Hoffman - General Counsel, Corporate Secretary & Chief Compliance Officer

David Hoffman brings more than two decades of legal and regulatory expertise in the biotechnology sector, with a particular focus on commercial-stage companies operating in highly regulated therapeutic categories. Before joining Delcath, he served as Associate General Counsel and Chief Compliance Officer at Vericel Corporation, where he oversaw all legal and compliance functions as the company transitioned from clinical stage to commercial operator in the regenerative medicine space.

His work supported the market growth of autologous cell therapies and biologics, product categories that, like Delcath’s offering, required extensive physician training, patient-specific logistics, and payer engagement. Earlier in his career, Hoffman advised a range of life sciences firms on commercial law, risk management, and regulatory structure, giving him a versatile foundation across legal domains critical to high-growth biotech companies.

At Delcath, Hoffman holds a multifunctional leadership role encompassing general counsel responsibilities, corporate governance as Secretary, and oversight of compliance as the company scales its commercial footprint. His day-to-day remit includes contract strategy, regulatory risk, intellectual property, compliance protocols, and oversight of interactions with payers, providers, and hospital systems, all essential elements of Delcath’s growth phase.

With the HEPZATO KIT now FDA-approved and commercially available in the U.S., Hoffman’s legal and compliance architecture must support site onboarding, field team operations, and interactions governed by Sunshine Act, Stark Law, and anti-kickback statutes. He also manages board governance matters and plays a key role in aligning legal operations with the company’s broader strategic, clinical, and commercial objectives.

This role is particularly important for Delcath because the company operates in a procedure-based therapeutic model, where the line between drug, device, and service can be blurry, especially in the eyes of regulators. Every site activation, reimbursement discussion, or physician training interaction carries regulatory and legal implications that require rigorous oversight.

Additionally, as Delcath prepares to expand into new indications and potentially enter ex-U.S. markets, Hoffman’s experience at Vericel, guiding a similarly complex therapy through commercialization, offers immediate strategic relevance. His presence helps de-risk Delcath’s compliance profile at a time when the company is building commercial velocity and engaging directly with hospital systems, making his role a critical enabler of scalable, audit-ready growth.

Vojislav “Vojo” Vukovic, MD, MSc, PhD - Chief Medical Officer

Dr. Vojo Vukovic brings to Delcath over two decades of senior leadership in oncology drug development, with a career spanning early- to late-stage clinical trials, regulatory engagement, medical affairs, and strategic indication planning. His experience is both broad and deep: he has served as Chief Medical Officer or Senior Vice President of Clinical Development at multiple oncology-focused biotechs including Aileron Therapeutics, Taiho Oncology, and Synta Pharmaceuticals, where he led the advancement of various novel therapies across solid tumors and hematologic malignancies.

His academic background includes an MD from the University of Sarajevo, followed by an MSc in radiation biology and a PhD in tumor biology from the University of Toronto, a training path that has given him scientific fluency across both mechanistic oncology and translational development. A frequent contributor to oncology literature and active member of major professional societies including ASCO, AACR, ASH, and ESMO, Dr. Vukovic brings with him a respected voice in the cancer research community and a track record of global clinical leadership.

As Chief Medical Officer at Delcath, Dr. Vukovic is responsible for overseeing all clinical development activities, including trial design, regulatory strategy, medical monitoring, and physician engagement, as well as long-term indication planning for the HEPZATO platform. He leads the medical strategy behind the ongoing ALIGN Phase 3 trial in colorectal liver metastases (CRLM) and is a key architect of the clinical rationale for expanding the platform into other liver-dominant cancers such as intrahepatic cholangiocarcinoma (iCCA), hepatocellular carcinoma (HCC), and potentially breast and pancreatic metastases.

In addition to his role in clinical trial execution, he plays an important cross-functional role in medical affairs, helping to shape physician education, investigator-initiated studies, and treatment center engagement, all of which are essential to building procedural adoption in the interventional oncology community.

For Delcath, the CMO role is more than clinical trial oversight, it’s about narrative leadership and clinical franchise building. The company’s platform relies not just on FDA approvals, but on sustained evidence generation across tumor types and procedural standardization across institutions.

Dr. Vukovic’s ability to communicate the hepatic-directed treatment rationale to both regulators and practicing oncologists is key to driving indication expansion and ensuring that each clinical program is designed for regulatory clarity, payer relevance, and physician uptake. In a company where commercial growth will depend on real-world clinical traction and a multi-indication label strategy, Dr. Vukovic’s presence provides scientific credibility and strategic rigor, making him a vital pillar in Delcath’s long-term oncology roadmap.

Kevin Muir - General Manager, Interventional Oncology

Kevin Muir brings over 20 years of sales and marketing leadership in the biotherapeutics and interventional medtech sectors, with deep domain expertise in commercializing complex, procedure-based therapies. Prior to joining Delcath, he served as Director of U.S. Sales for the Interventional Oncology business at BTG, where he was instrumental in the market success of TheraSphere, a Yttrium-90 (Y90) radioembolization platform used in the treatment of liver cancer.

TheraSphere, like Delcath’s HEPZATO KIT, required physician education, site onboarding, logistical coordination, and payer alignment, giving Muir direct operational experience in navigating the commercial hurdles of liver-directed, minimally invasive oncology interventions. His earlier roles included Director of Sales at ClearFlow Inc. and Aragon Surgical, as well as leadership positions at Kensey Nash, Kyphon, and Genzyme Biosurgery, where he built regional and national sales organizations targeting both hospital-based and outpatient markets.

At Delcath, Muir leads all commercial operations related to the HEPZATO KIT and future platform therapies, with a specific focus on hospital engagement, sales force development, and interventional oncology center activation. He is tasked with building the field team responsible for training, adoption, and procedural throughput, ensuring that institutions not only purchase the therapy, but are equipped to administer it effectively.

His remit includes center of excellence development, physician relationship management, sales enablement infrastructure, and feedback loops with the clinical and operations teams to inform rollout priorities. Given the procedural nature of HEPZATO, which requires cross-functional coordination across radiology, oncology, perfusion, and pharmacy, Muir’s role demands more than typical oncology drug commercialization. He must establish an ecosystem of repeat users, internal champions, and reimbursement pathways that can support durable product utilization.

This role is mission-critical for Delcath because the company’s revenue is procedure-based and site-driven, not broadly prescribed. Unlike small molecule oncology drugs, HEPZATO must be adopted hospital by hospital, and every additional treatment center represents a significant revenue opportunity and fixed-cost leverage point.

Muir’s specific experience at BTG scaling TheraSphere, which shares nearly identical clinical dynamics in hepatic oncology, gives him a precise playbook for growing Delcath’s footprint. His blend of medtech fluency, sales force leadership, and oncology commercialization makes him central to Delcath’s near-term inflection and long-term value realization. As adoption expands and the next-generation delivery system approaches, Muir will be responsible for turning a de-risked platform into a scalable, durable commercial franchise.

Sandra Pennell - Chief Financial Officer

Sandra Pennell brings over two decades of senior financial leadership across high-growth life sciences companies, with deep expertise in SEC reporting, capital markets execution, FP&A, and treasury operations. Her career includes leading finance organizations through periods of clinical development, public market volatility, and commercial scale-up, all highly relevant to Delcath’s current trajectory.

Prior to joining Delcath, Pennell served as Vice President of Finance at Invivyd, Inc., a publicly traded infectious disease therapeutics company, where she helped manage equity financing, regulatory filings, and operational budgeting in a rapidly evolving clinical landscape. Before that, she held the role of Vice President & Corporate Controller and Principal Accounting Officer at Vericel Corporation, where she played a key role during the company’s transformation from R&D-centric to a profitable commercial-stage enterprise.

At Delcath, Pennell is responsible for all finance and accounting functions, including financial reporting, audit and compliance, internal controls, capital structure strategy, investor relations support, and strategic resource allocation. She plays a cross-functional role in budgeting for the commercial rollout of HEPZATO, guiding investment decisions across sales force expansion, clinical trial resourcing, and next-gen platform development.

Importantly, she oversees the alignment of Delcath’s cost structure with its staged revenue plan, ensuring that operational scale-up remains capital-disciplined and ROI-focused. Her involvement in treasury and equity financing strategy positions her as a key interface with capital markets, responsible for maintaining the financial runway needed to execute the company’s commercial and clinical agenda without over-reliance on dilutive capital raises.

The CFO function is especially pivotal at Delcath given its position at the intersection of capital-intensive operations and high-margin procedure-based revenue. Unlike pure-play biotech models that live between inflection points, Delcath’s long-term viability depends on disciplined, sustained investment in both commercial and manufacturing infrastructure, without bloating SG&A ahead of revenue scale.

Pennell’s background at Vericel, which shares a similar trajectory as a once-early-stage therapeutic company that matured into a commercial platform, offers a valuable operational blueprint. Her approach to financial planning and risk management is essential to guiding Delcath through its transition phase, managing dilution risk, and ensuring that every capital deployment aligns with strategic growth levers. As Delcath moves into multi-indication expansion, Pennell will serve as the financial architect ensuring scalability, compliance, and capital efficiency across the platform lifecycle.

Delcath’s platform is complex, its market fragmented, and its therapeutic model demands precision across domains most biotechs never have to coordinate: device regulation, procedural training, hospital reimbursement, and real-world treatment execution. What sets Delcath apart is not just its innovation, but the architecture of the team tasked with scaling it.

From top to bottom, the company’s leadership reflects a rare coherence: operators with experience commercializing procedure-based therapeutics, managing regulatory ambiguity, and driving adoption one hospital at a time. For long-term investors, this is not a management team to tolerate, it is a strategic moat in its own right.

With the leadership in place, the next step is to assess how Delcath plans to translate its platform into a scalable, durable business.

5. Business Model & Commercial Strategy

This isn’t a pill you prescribe, it’s a platform you build. Delcath’s business model doesn’t follow biotech rules, and that’s exactly the point.

Delcath Systems is not a conventional biotech company monetizing molecular innovation through prescriptions or out-licensing. Instead, it operates a procedure-centric business model, in which revenue is generated each time a hospital administers its flagship therapeutic product, the HEPZATO KIT, as part of a structured interventional oncology treatment.

This model aligns more closely with medical device companies like Intuitive Surgical or Medtronic, or procedural therapeutic platforms like SIRT (Y90 embolization) or TAVR (valve replacement), than with traditional oncology drug developers.

The implications for investors are material: Delcath has the potential to scale high-margin, repeatable revenue by expanding treatment center access, increasing per-site utilization, and broadening its indication footprint, all while maintaining capital discipline and avoiding the linear SG&A ramp typically associated with multi-product pharmaceutical companies.

What Delcath sells: A high-value procedure packaged as a drug-device combination

At the center of Delcath’s business model is the HEPZATO KIT, an FDA-approved, proprietary system designed to administer high-dose melphalan hydrochloride directly to the liver via isolated perfusion, while simultaneously filtering the patient’s blood before it returns to systemic circulation. The system is classified as a drug-device combination product, comprising several integrated components:

A dual-balloon catheter system to isolate hepatic blood flow,

A precision-controlled extracorporeal hemofiltration circuit,

A high-concentration chemotherapy dose of melphalan,

Procedural disposables and supporting materials tailored for safe, repeatable use.

The product is delivered as a complete, single-use kit intended to be used during a structured interventional oncology procedure. This therapy is not administered through conventional pharmacy channels or as an outpatient infusion, it is delivered within a hospital’s interventional suite, typically by a multi-disciplinary team involving an interventional radiologist, perfusionist, anesthesiologist, and oncology staff.

Because the therapy is episodic, with most patients undergoing 2-4 treatment cycles per clinical protocol (or more in some cases), Delcath monetizes each procedure independently. That translates into multiple revenue events per patient and a built-in element of semi-recurring revenue within each treatment center. Importantly, the complexity of the procedure creates clinical and operational lock-in, once a center is trained, it is unlikely to churn or substitute another therapy, especially as procedural repetition improves staff efficiency and cost recovery.

How Delcath makes money: High ASPs, repeat utilization, and site-level revenue density

Delcath sells the HEPZATO KIT directly to hospitals and academic centers through specialty distribution or direct contracting, with the average selling price (ASP) estimated between $25,000 and $35,000 per procedure. The ASP reflects not only the therapeutic value of melphalan, but also the complexity and IP protection surrounding the delivery system. Gross margins are expected to exceed 70% at scale, consistent with high-end oncology procedures and minimally invasive interventional therapies.

The revenue model is tightly tied to site activation and patient throughput, not broad prescriber volume. This means the company's top-line growth is dependent on the number of operational centers and their procedural cadence, not traditional metrics like market share among oncologists or script volume. Once a site is trained and credentialed, it becomes a revenue-generating asset. Centers treating patients with hepatic-dominant cancers often have multiple eligible patients at any given time, enabling fast conversion from launch to recurring use.

Patients typically receive multiple treatments within a defined window, so per-patient lifetime value is high, particularly when considering the limited competition in mUM and future planned indications. Delcath also benefits from favorable economic incentives for hospitals, many of which seek to expand their interventional oncology service lines with procedures that are both clinically meaningful and reimbursable. HEPZATO offers both, and the company supports procedural adoption with clinical training, onsite technical support, and reimbursement navigation.

The business model allows for high revenue density per center. As sites gain experience, procedural cadence often increases, enabling more efficient staff utilization and consistent revenue streams. Early commercial rollout is focused on high-volume academic centers, where Delcath can maximize revenue per activation while building procedural champions that will aid in community center adoption over time.

Platform leverage: Multi-indication expansion without commercial duplication

Delcath’s most strategic commercial advantage lies in its platform leverage, the ability to expand into new indications without rebuilding its commercial, technical, or procedural infrastructure. Unlike small molecule drugs that require new salesforces, educational campaigns, or specialty pharmacies for every new label, HEPZATO is a modular procedure.

Once a hospital is trained to administer the therapy, that same team, catheter infrastructure, and billing protocol can be used across multiple indications, whether treating uveal melanoma, colorectal liver metastases, intrahepatic cholangiocarcinoma, or eventually hepatocellular carcinoma.

This gives the company an attractive non-linear growth curve: future trials and indications expand revenue not by opening new markets from scratch, but by deepening utilization within already-onboarded centers. For example, the ongoing ALIGN Phase 3 study in CRLM, which targets a 10-20x larger market than mUM, could unlock dramatically more revenue from existing centers that have already cleared the initial onboarding and training hurdle. Importantly, Delcath does not need to scale its SG&A in parallel, it can add new patient segments without replicating the cost structure.

This also contributes to the company’s procedural moat. Because physicians, administrators, and support staff invest time and resources to integrate HEPZATO into their practice, they are less likely to switch to alternatives, even if future competition enters the hepatic-directed therapy space. The company benefits from institutional inertia, procedural repetition, and clinical familiarity, all of which build network effects around each treatment center.

From a long-term strategy perspective, this model positions Delcath not just as a single-product company, but as a procedural oncology platform with multiple verticals and optionalities. As more data emerges, and as new indications are approved, the company can stack utilization across tumor types, enhancing both per-site economics and enterprise value without proportional increases in headcount or infrastructure.

Capital efficiency, monetization timeline, and strategic alignment

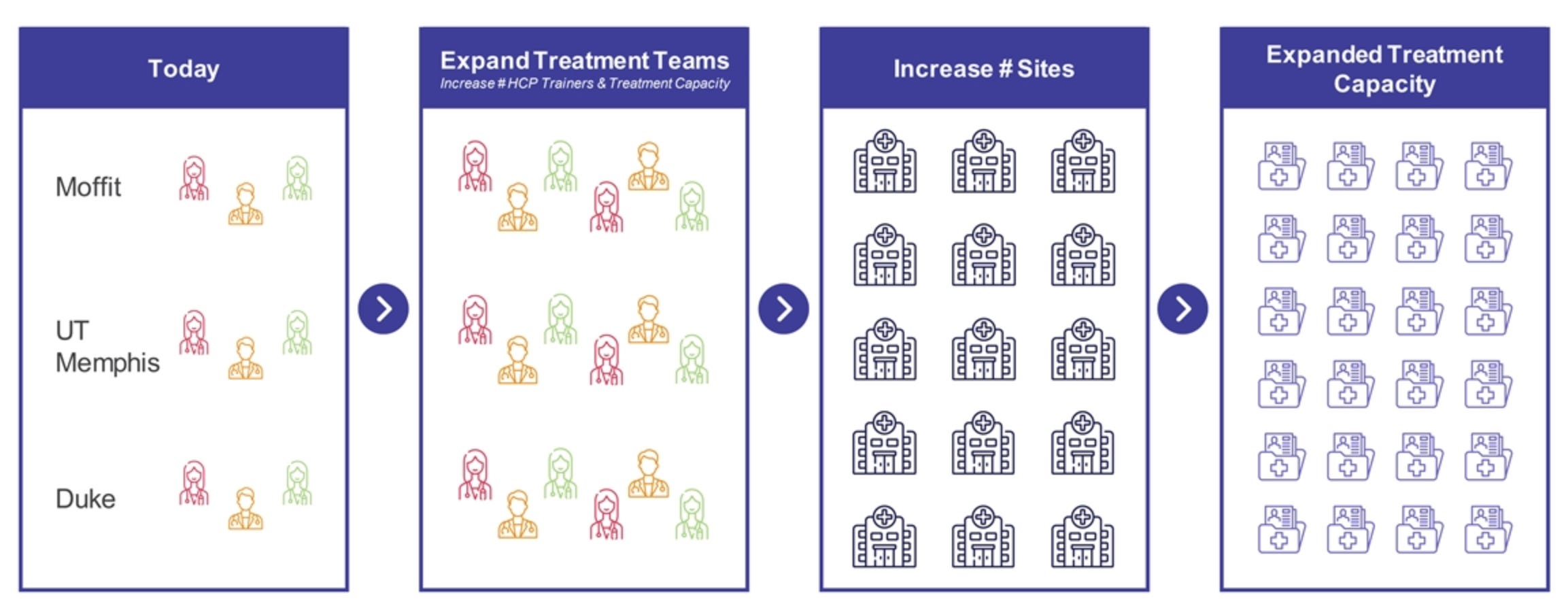

Delcath’s business model is not only margin-accretive and procedurally anchored, it’s also designed for time-sensitive monetization with capital-efficient scalability. The typical onboarding process for a new treatment center takes between 3 to 6 months, encompassing contracting, physician and staff training, and initial procedural support. Once live, these sites can begin administering HEPZATO immediately, creating a relatively fast conversion from site activation to cash-generating revenue.

Hospitals purchase the HEPZATO KIT either via direct sales agreements or through specialty distributors, and Delcath recognizes revenue upon shipment, simplifying working capital management. While individual contract structures can vary by institution, the pricing model is generally based on per-use kit purchases, not volume-based tiering or rebates, which helps preserve ASP integrity in the early launch phase.

Over time, Delcath expects this structure to support robust unit economics, especially as procedural frequency rises and operational support becomes more standardized. Importantly, Delcath is not building out a large field force to “push” product, instead, it is selectively targeting high-volume academic centers where procedural oncology infrastructure already exists, allowing each site to reach meaningful revenue contribution without extensive commercial lift.

Because each new indication can reuse the same sales infrastructure and clinical support pathways, Delcath gains multi-indication leverage, every new label expansion increases throughput per center, improving fixed cost absorption and expanding gross margin. Additionally, the company’s next-generation delivery system, expected in 2025, is designed to simplify procedural setup, shorten training cycles, and reduce variability, all of which should further compress onboarding time and increase per-site utilization, reinforcing both scalability and time-to-revenue compression.

In the long-term, this structure creates a business model with multi-layered operating leverage: (1) fixed costs amortized across growing procedural volume, (2) recurring use within centers as new patients enter treatment, and (3) platform stacking via additional indications using the same delivery hardware and clinical team.

When combined with a reimbursement architecture aligned to existing CPT codes and hospital workflows, the result is a commercial engine that scales predictably, supports high-margin growth, and aligns tightly with long-term investor interests. For a small-cap company transitioning from R&D to commercialization, this business model, anchored in procedure-driven, site-recurring revenue, provides a foundation not only for top-line expansion, but also for durable margin growth and platform-level strategic optionality.

Delcath’s business model is not just innovative, it’s structurally advantaged. By anchoring revenue to procedure volume rather than prescription flow, the company builds durable, high-margin, and site-recurring income with limited commercial overhead. Each new treatment center becomes a revenue node, each new indication a throughput multiplier.

With embedded training, procedural complexity, and reimbursement alignment, Delcath creates economic and operational stickiness that is difficult to displace. And because the platform is modular, expansion doesn’t require parallel cost scaling, it deepens utilization within the same footprint. For long-term investors, this isn’t a typical biotech curve. It’s a platform economics story, and one with real-world friction that translates into real-world defensibility.

To understand how value is captured, we must now examine the underlying products and platform driving that value.

6. Therapy Platform & Core Products

Delcath isn’t delivering a drug, it’s delivering control. Precision, protection, and platform scalability are built into every procedure.

Delcath’s product innovation centers around the HEPZATO KIT, a proprietary, FDA-approved drug-device combination therapy designed for regionally targeted delivery of high-dose chemotherapy to the liver. The product is not a drug in the conventional sense, nor is it a standalone device; rather, it is a highly engineered procedural system that integrates pharmacology, interventional radiology, and extracorporeal filtration into a unified clinical solution.

The therapeutic rationale is straightforward: by isolating the liver’s circulatory system and perfusing it directly with concentrated melphalan, physicians can achieve tumoricidal drug levels within the organ while minimizing systemic toxicity through blood filtration, a pharmacokinetic profile that cannot be replicated with systemic administration.

At the product level, the HEPZATO KIT includes:

A dual-balloon catheter system inserted via the femoral artery and vein, enabling blood flow isolation of the hepatic circuit.

A high-dose melphalan hydrochloride formulation optimized for intra-arterial infusion.

A custom extracorporeal filtration circuit, which removes 85-90% of the drug before blood re-enters systemic circulation.

Procedure-specific disposables (tubing, connectors, pumps) integrated into an operating kit that supports a single use.

A mobile, table-side CHEMOSAT system, in some markets, that supports circuit management (EU only).

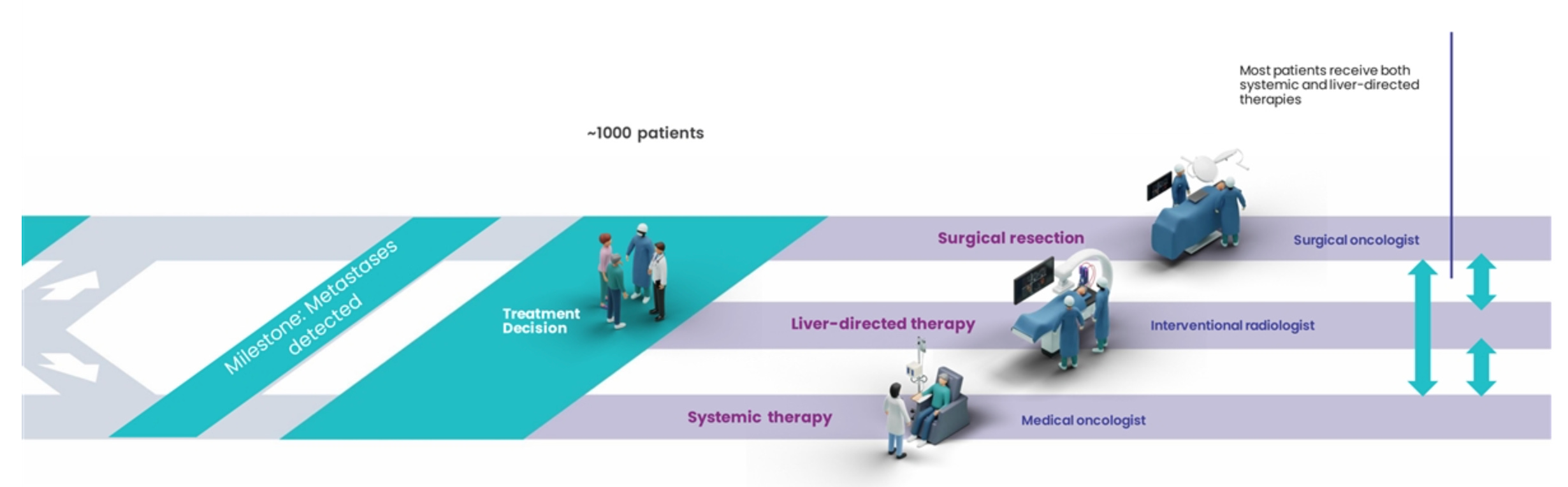

The delivery system is designed to be used in hospital interventional oncology suites under general anesthesia, with procedural support from perfusionists, interventional radiologists, anesthesiologists, and oncology staff. Each treatment session typically lasts several hours and is conducted on an inpatient or outpatient basis depending on institutional protocol. Patients may undergo multiple sessions, usually spaced 6-8 weeks apart.

The mechanism: Pharmacokinetic engineering through mechanical isolation

The therapeutic logic behind the HEPZATO KIT lies in its ability to mechanically reshape the pharmacokinetics of chemotherapy. At its core, Delcath’s system enables regional isolation of the liver’s blood supply, allowing for the direct infusion of high-dose melphalan hydrochloride into hepatic circulation, followed by extracorporeal filtration of the blood before re-entry into systemic circulation. This addresses one of oncology’s oldest and most persistent tradeoffs: delivering a drug dose potent enough to kill tumors without exceeding systemic toxicity thresholds.

Unlike traditional chemotherapy regimens, where drug levels are diluted across the entire body and limited by systemic side effects, Delcath’s platform concentrates exposure where the disease resides, the liver, while removing excess drug before it circulates systemically.

Published pharmacokinetic data shows that hepatic drug exposure is increased by as much as 20-fold relative to systemic delivery, while systemic drug concentrations are reduced by 85-90% due to the filtration circuit. This allows for both higher efficacy at the site of disease and an acceptable safety profile, particularly in cancers where hepatic progression is the dominant cause of mortality.

From an engineering standpoint, the key innovation lies in how the system achieves this isolation and filtration in a repeatable, reproducible clinical setting. A dual-balloon catheter blocks the hepatic venous outflow while the arterial supply is cannulated for drug infusion. Blood is routed through a proprietary hemofiltration circuit, which uses a high-capacity charcoal filter to remove melphalan before blood is returned to the body via a separate catheter.

This entire process is controlled in real-time by a trained perfusionist and requires anesthesia, hemodynamic monitoring, and coordination across interventional radiology and oncology teams, a complexity that acts as both a barrier to entry and a durable procedural moat.

Crucially, this mechanism does not require a molecular breakthrough, it requires precise control of anatomy, circulation, and filtration, which Delcath has engineered into a commercially viable therapeutic workflow. The result is a form of regional chemotherapy intensification that cannot be achieved through conventional infusion methods, positioning HEPZATO as a unique and differentiated therapeutic approach within the interventional oncology landscape.

Product evolution: From device platform to integrated combination product

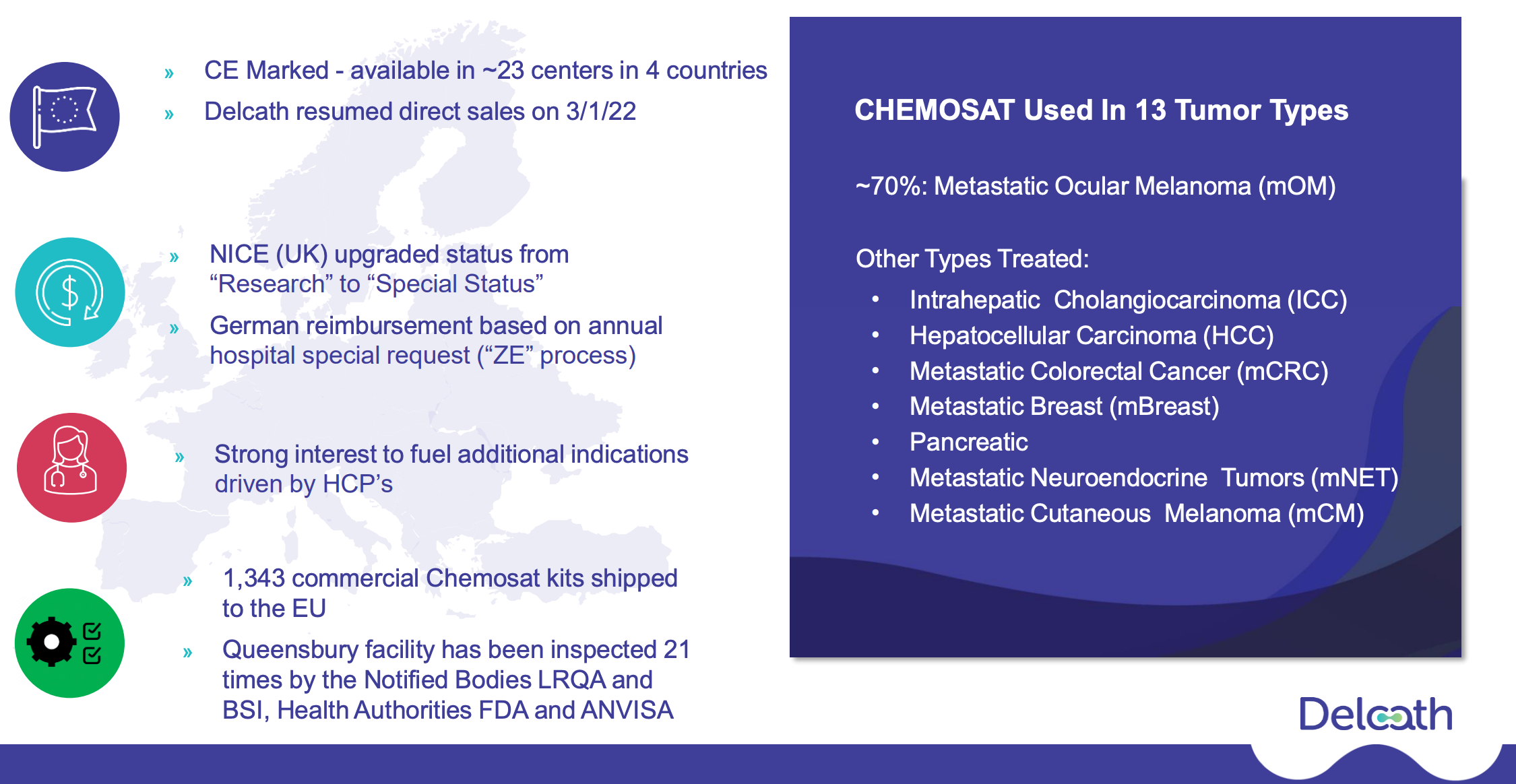

Delcath’s product strategy has evolved from a hardware-centric device offering (CHEMOSAT) to a fully integrated drug-device combination product (HEPZATO). This transition reflects both a maturation of the platform and a strategic decision to pursue higher regulatory defensibility, stronger economic capture, and improved clinical usability.

Originally introduced in Europe under the CE mark as a device-only system, CHEMOSAT required hospitals to source melphalan separately, which complicated logistics and limited Delcath’s pricing power and brand control. While the platform saw clinical uptake in Europe, the lack of drug integration and FDA clearance constrained commercial scale.

Recognizing these limitations, Delcath reoriented its U.S. strategy around a combination product regulatory pathway, leading to the development of the HEPZATO KIT, a packaged system that includes both the drug and device components under a unified label. This repositioning brought several strategic advantages:

It allowed for control over drug supply, quality, and labeling, ensuring consistency across procedures.

It enabled Delcath to pursue FDA approval under a New Drug Application (NDA), gaining regulatory exclusivity and a stronger IP position.

It simplified hospital adoption by reducing friction in procurement, pharmacy prep, and procedural planning.

The FDA approval of the HEPZATO KIT in August 2023 for patients with metastatic uveal melanoma marked the platform’s first U.S. commercial milestone. This version reflects multiple product refinements: catheter design improvements, streamlined disposables packaging, more standardized operator protocols, and integration with hospital procedural workflows. These changes reduce training time, procedural variability, and error risk, all essential for driving adoption in busy hospital environments.

Looking ahead, Delcath is developing a next-generation version of the delivery system, targeting a 2025 release. While details are limited, investor communications and product roadmaps suggest upgrades may include:

Automated pressure and flow monitoring to reduce operator burden.

Simplified circuit priming and setup, improving procedural turnaround.

Potential software integration for procedural guidance and analytics.

The intent is clear: to make HEPZATO more scalable, less manually intensive, and ready for broader adoption, including community-based oncology centers. In doing so, Delcath isn’t just improving usability, it’s enhancing the long-term operating leverage and install-base ROI of every treatment center onboarded.

IP, manufacturing, and product defensibility

Delcath’s product moat is protected by a hybrid of intellectual property, regulatory exclusivity, and procedural complexity, a structure that creates real barriers to entry and supports premium pricing. On the IP front, the company holds patents covering the catheter design, hemofiltration media, methods of use, and drug-device integration, many of which extend into the 2030s.

The combination product designation adds a further layer of protection, as any generic entrant would need to demonstrate equivalence not only in drug formulation but in procedural performance and filtration kinetics, a formidable hurdle, especially given the system’s engineering-specific clinical claims.

But the defensibility extends beyond IP. HEPZATO is fundamentally a procedural solution, not a passive drug or device. Its effective use requires specialized training, cross-disciplinary coordination, and infrastructure integration. Hospitals that invest in onboarding, including perfusion staffing, protocol approval, and pharmacy integration, build operational commitment that is not easily unwound. This creates a sticky install base, similar to surgical platforms or radiation systems, where switching costs and institutional inertia reinforce long-term utilization.

From a manufacturing standpoint, Delcath uses a contract manufacturing model, outsourcing production of both drug and device components while maintaining control over final kit assembly, packaging, and quality assurance. This approach limits capital intensity while allowing for scalable production as volume ramps.

As the company moves toward its next-generation system, opportunities for cost-of-goods optimization and logistics simplification are likely to improve gross margins, an important lever as revenue scales and margin expansion becomes a core driver of equity value.

The combination of proprietary components, clinical workflow lock-in, and regulatory complexity means that even with future competition in liver-directed therapy, Delcath is structurally advantaged as the first mover with an FDA-approved, clinically validated system. In oncology, where time-to-market, institutional trust, and procedural standardization are paramount, this type of integrated defensibility can support a decade or more of uncontested commercial runway.

Strategic significance: A scalable procedure, not a one-off product

HEPZATO’s importance to Delcath’s investment thesis goes well beyond its current approval in metastatic uveal melanoma. It is the cornerstone of a procedural oncology platform designed for multi-indication expansion. Because the therapy is delivered through the same physical infrastructure and clinical workflow regardless of tumor type, each newly approved indication can be layered onto existing sites with minimal additional training or cost. This makes the platform economically and operationally scalable, a key point of differentiation from traditional biopharma models.

For example, if a hospital is treating mUM patients with HEPZATO today, that same center could treat patients with colorectal liver metastases, intrahepatic cholangiocarcinoma, or hepatocellular carcinoma using the same catheter systems, filtration setup, perfusion staff, and billing pathways. This stacking of indications creates non-linear revenue growth, as per-site utilization increases without requiring new salesforce expansion, major product reconfiguration, or commercial reinvestment. As a result, HEPZATO is not a static SKU, it is a delivery franchise capable of addressing multiple high-value, high-burden hepatic cancers.

This structure enables Delcath to pursue a stepwise platform rollout, where each clinical and regulatory milestone builds upon the last, increasing ROI on both R&D and commercial infrastructure. It also positions the company favorably within hospital systems increasingly focused on procedural consistency, training efficiency, and bundled care pathways. The more indications that can be treated through a single procedural protocol, the more attractive the platform becomes for institutional adoption and payer integration.

Over time, the HEPZATO architecture could also support future innovations beyond melphalan. While the company’s current focus is on expanding indications for its existing therapy, the mechanical isolation and filtration principles could, in theory, be applied to other agents or even combination regimens. That optionality isn’t priced into current operations but represents a strategic long-tail for long-term investors betting on platform-level oncology infrastructure.

HEPZATO is more than Delcath’s first product, it’s the chassis for an entire procedural oncology platform. By engineering therapeutic intensity into a repeatable system, the company has created a franchise that can scale across cancers, institutions, and indications with minimal reinvention. Every new use case becomes a force multiplier, not a dilution of focus.

With strong IP, built-in clinical complexity, and high procedural stickiness, the platform is both protected and extensible. In a market dominated by molecules, Delcath offers something rarer: a mechanistically sound, operationally scalable, and economically durable approach to cancer therapy.

With the platform defined, attention turns to how it expands across clinical indications and market segments.

7. Indications & Pipeline Expansion Strategy

Delcath’s pipeline isn’t about new products, it’s about deepening value from the same platform, one indication at a time.

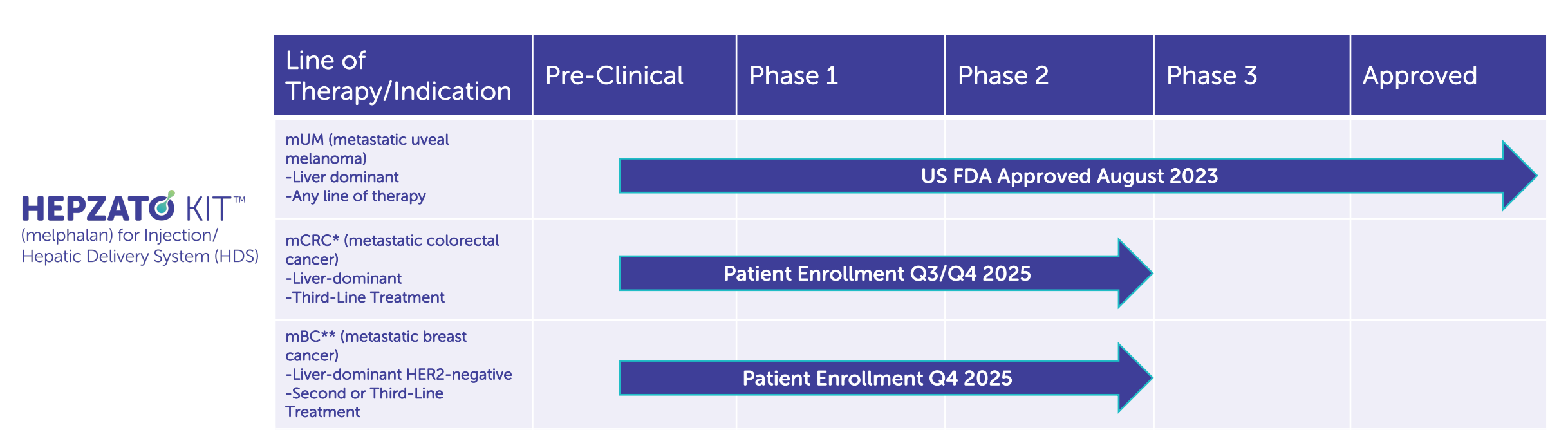

Delcath’s clinical and commercial strategy centers around the strategic layering of liver-dominant cancer indications onto a single procedural platform. With HEPZATO’s approval in metastatic uveal melanoma (mUM) as the foundational step, the company is executing a multi-year, indication-led expansion strategy targeting other high-burden, underserved liver cancers, including colorectal cancer liver metastases (CRLM), intrahepatic cholangiocarcinoma (iCCA), and hepatocellular carcinoma (HCC).

Each indication leverages the same treatment system, procedural workflow, and commercial footprint, enabling the company to scale utilization and revenue without proportionally scaling cost or infrastructure.

The clinical rationale across these indications is unified: in each case, the liver serves as the dominant site of progression and often the proximate cause of death. However, unlike solid tumors where systemic therapy can offer durable control, liver-dominant disease is frequently non-curable, poorly responsive to chemotherapy, and ineligible for resection or ablation. Delcath’s value proposition lies in its ability to deliver potent, liver-targeted cytotoxic exposure, addressing a clear therapeutic gap with precision and repeatability.

The sequencing of these indications is not opportunistic, it is engineered. Each step is meant to incrementally validate the platform across increasingly prevalent disease settings, growing the TAM while building procedural muscle, payer comfort, and clinical evidence. In this section, we explore the strategic and clinical logic of each target tumor type, its commercial relevance, and its role in the platform’s evolution.

Metastatic Uveal Melanoma (mUM): Foundational proof of concept and controlled market entry

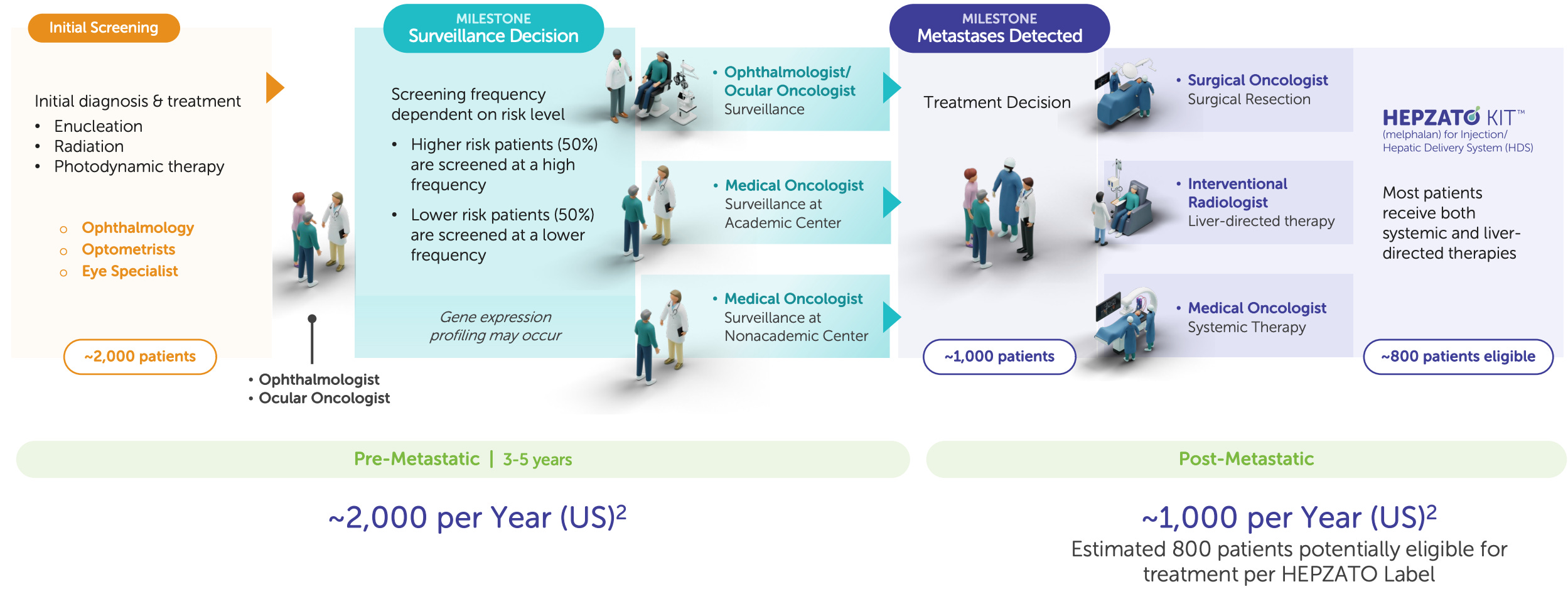

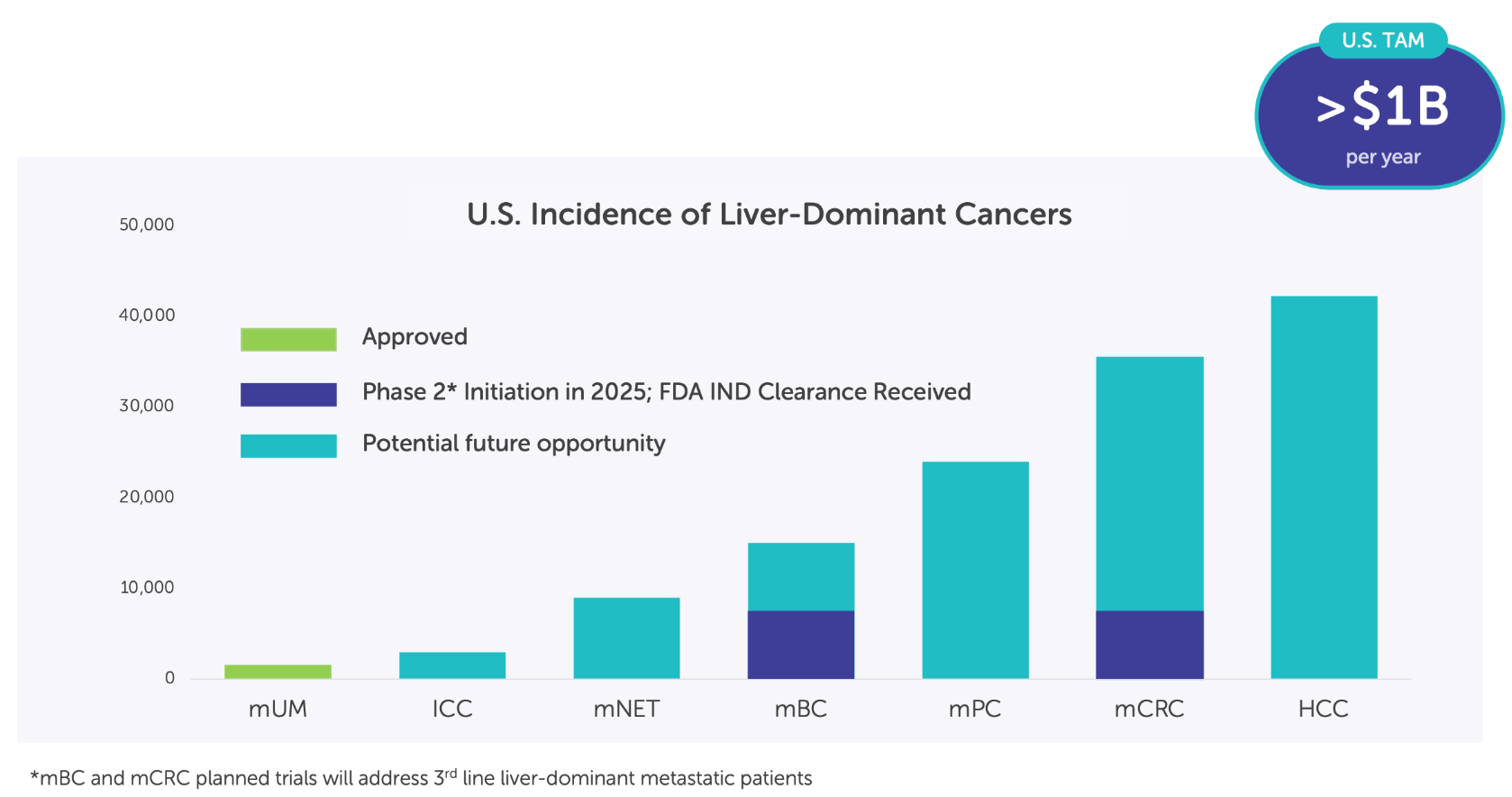

Delcath’s first FDA-approved indication, metastatic uveal melanoma (mUM), is more than a regulatory milestone; it is a strategic test bed for platform deployment, commercial refinement, and procedural adoption. With approximately 1,000–1,200 new cases per year in the U.S., mUM represents a small but highly concentrated oncology market, with most patients referred to a limited number of academic centers specializing in rare ocular cancers. More than 90% of metastatic spread occurs in the liver, making mUM uniquely suitable for a liver-directed therapy such as HEPZATO.

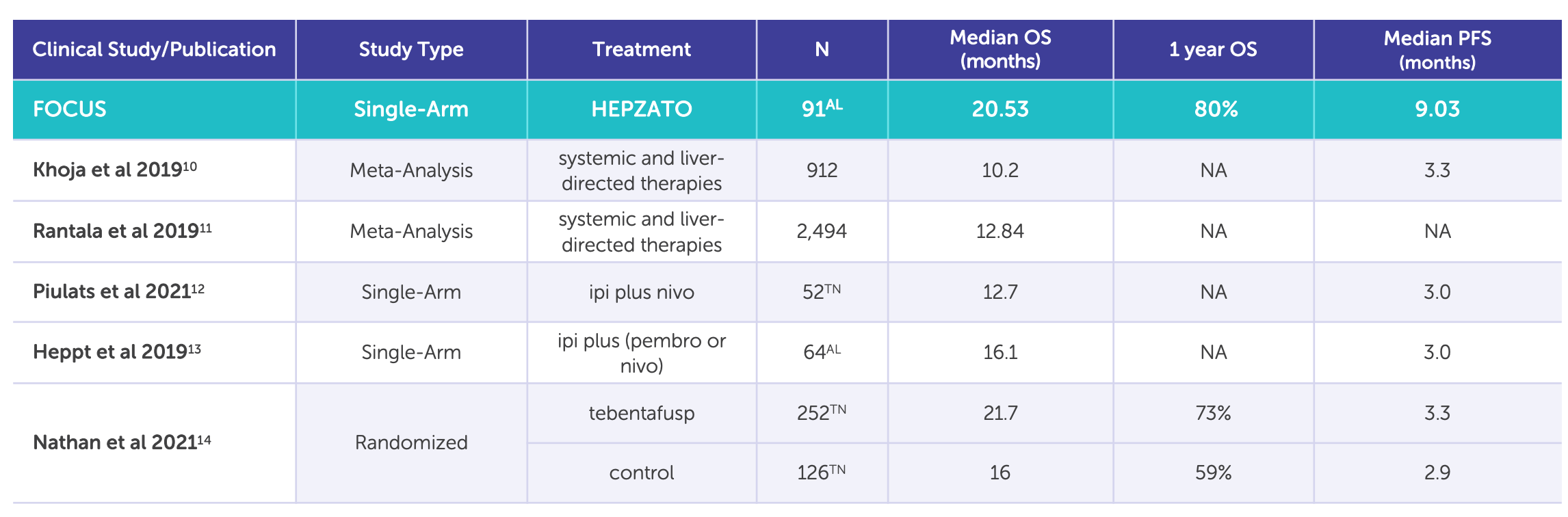

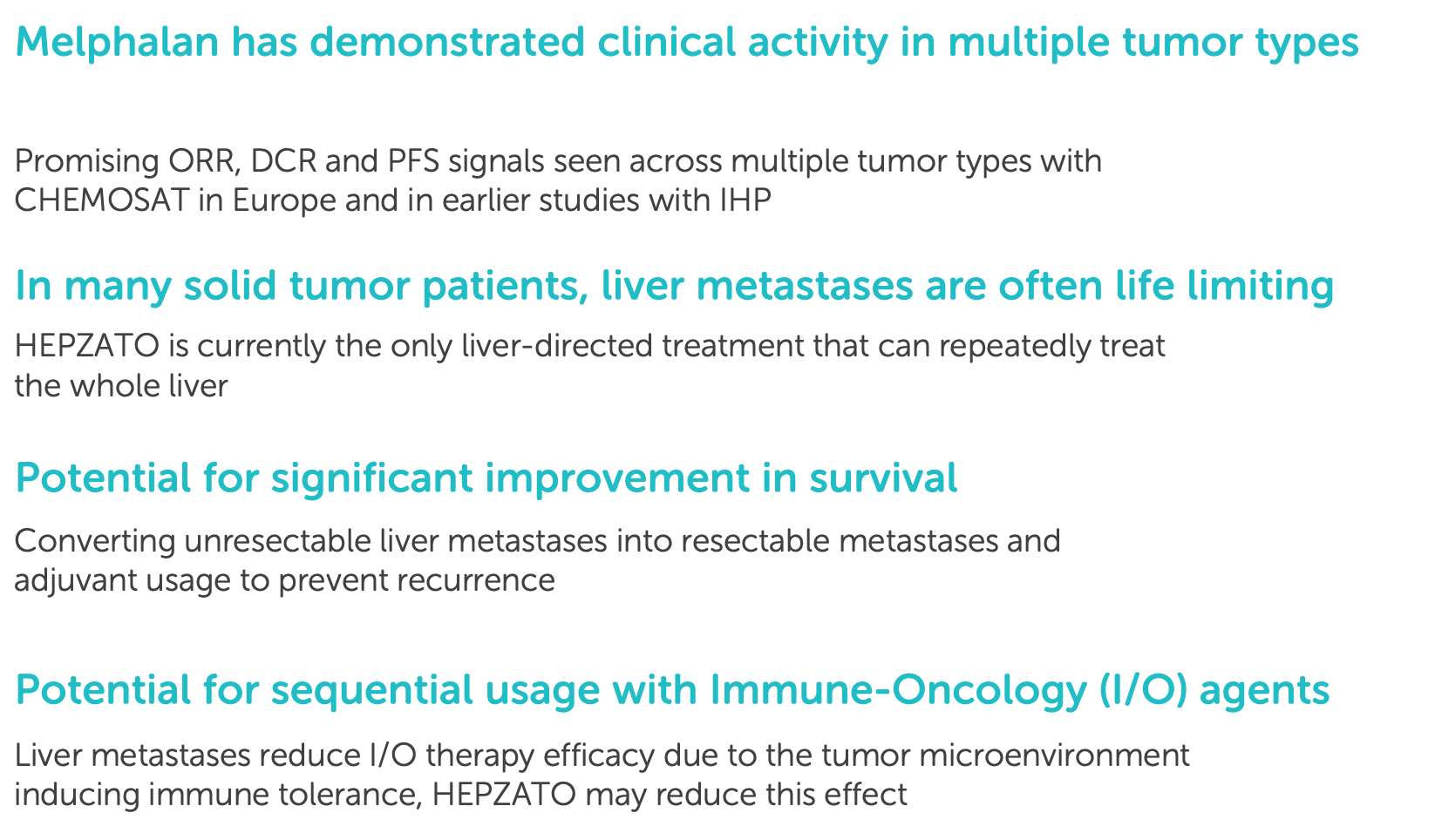

Delcath’s Phase 3 FOCUS trial (single-arm, multi-center) demonstrated that HEPZATO achieved a 36.3% objective response rate (ORR), a disease control rate of 73.8%, and a median hepatic progression-free survival (hPFS) of 8.1 months. These results were achieved in heavily pre-treated patients with no other liver-directed therapeutic options and minimal response to systemic checkpoint inhibitors. The FDA approved the HEPZATO KIT in August 2023, marking the first time a percutaneous hepatic perfusion (PHP) system was approved as a drug-device combination product for solid tumor treatment in the U.S.

From a commercial perspective, mUM allows Delcath to refine its go-to-market model in a low-volume, high-specialization setting. Most patients are funneled to major academic centers, reducing sales force requirements and concentrating onboarding efforts. The procedures are reimbursed under existing hospital frameworks, and the rarity of the disease often justifies institutional investment in specialized treatments.

Importantly, mUM centers frequently treat other complex solid tumors, particularly metastatic colorectal and cholangiocarcinoma, which means that early procedural investments are reusable across future indications.

Also, mUM provides the company with initial revenue visibility, clinical validation, and payer touchpoints that will support broader expansion. The importance of mUM lies not in its market size but in its strategic optionality, it serves as a regulatory foothold, procedural pilot, and reputational wedge into a market that values clinical differentiation.

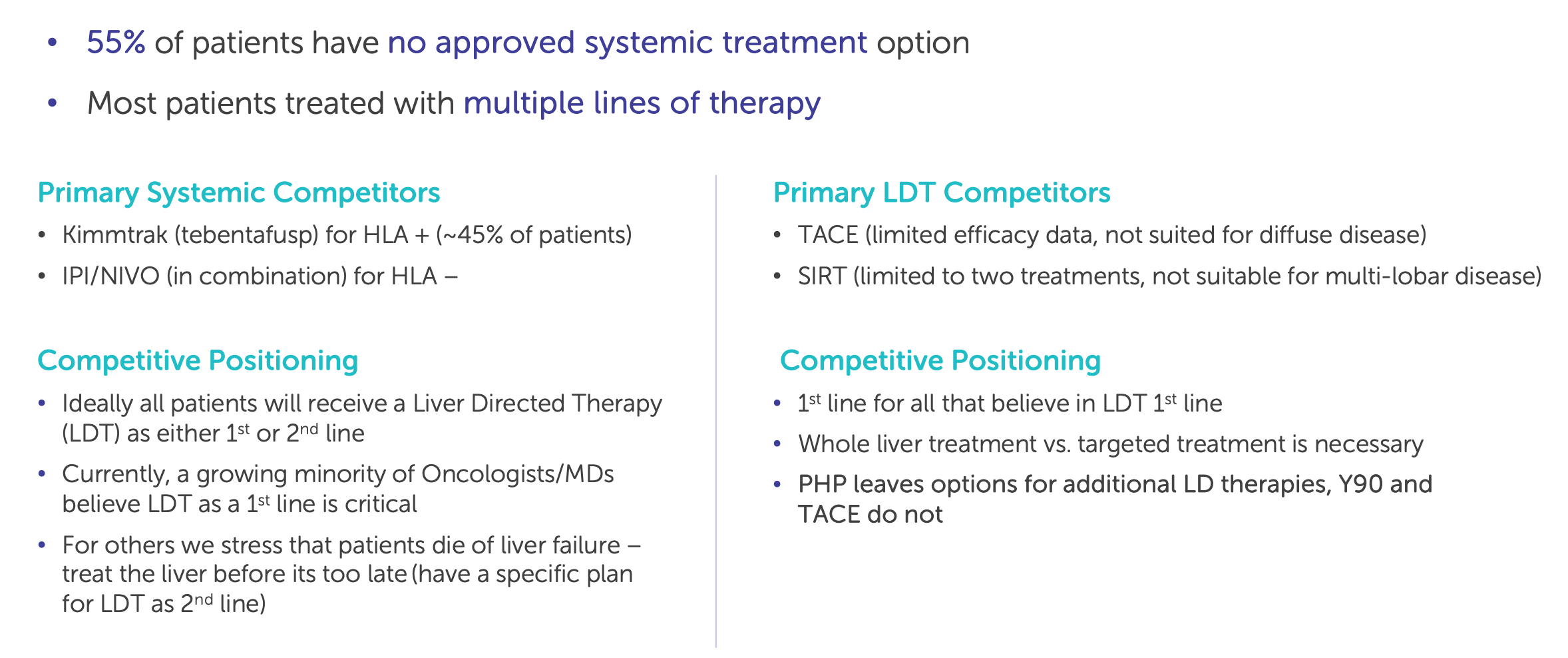

Colorectal Liver Metastases (CRLM): The pivotal growth catalyst

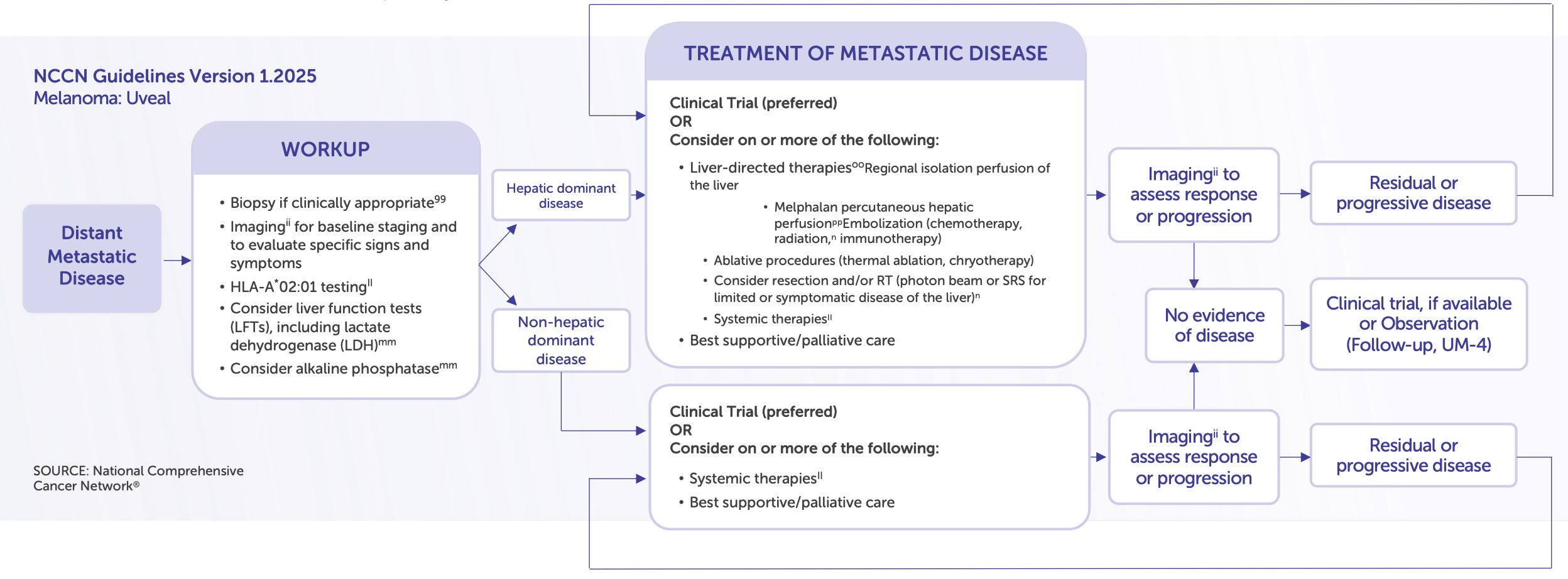

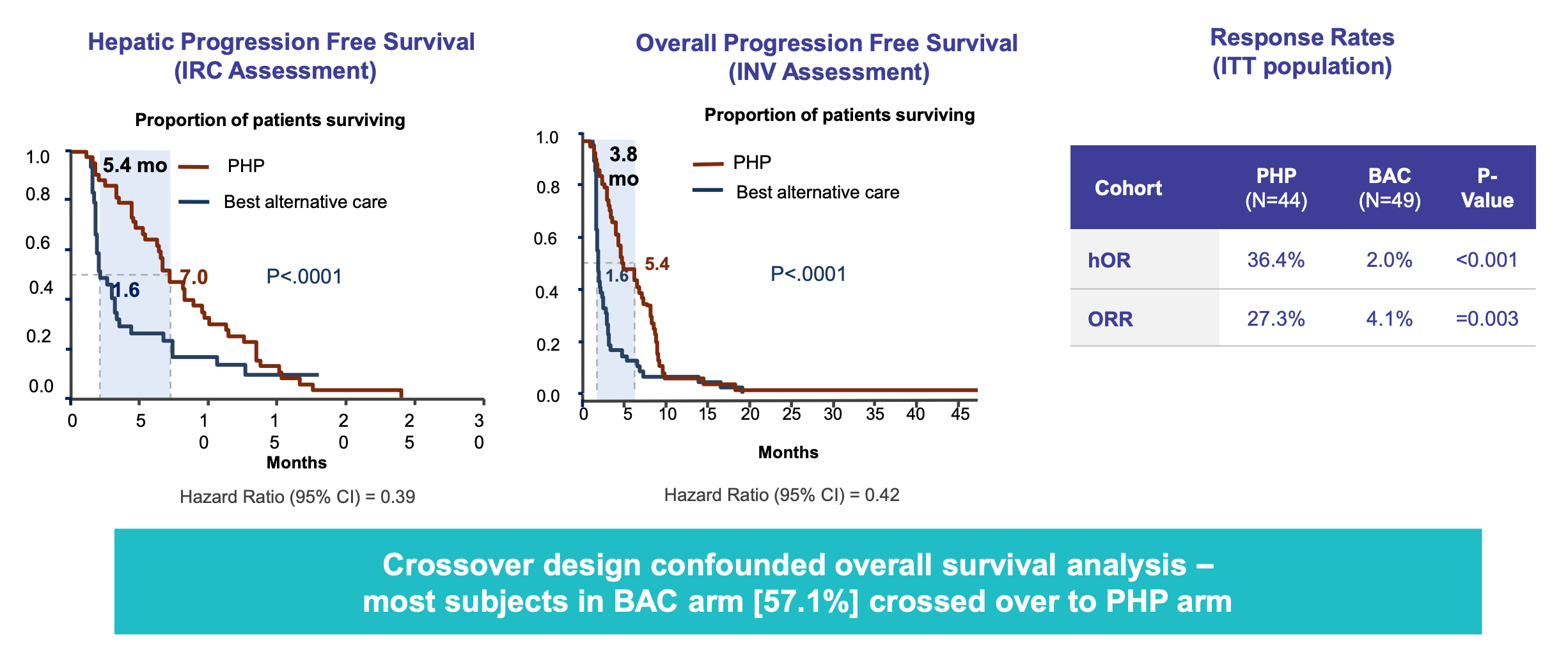

If mUM was Delcath’s foot in the door, colorectal cancer liver metastases (CRLM) represent the key to unlocking platform-scale commercial potential. Colorectal cancer is the second-leading cause of cancer death in the U.S., and approximately 50% of patients eventually develop liver metastases. Among these, a large subset present with unresectable, liver-dominant disease that cannot be treated with surgery or ablation, and who have already progressed on standard chemotherapeutic or targeted regimens. In this setting, there is currently no liver-directed therapy with demonstrated survival benefit, creating a significant unmet need that Delcath is well-positioned to address.

The company’s ongoing Phase 3 ALIGN trial is enrolling patients with third-line liver-dominant CRLM. The study is designed to compare HEPZATO KIT to physician’s choice of best alternative care (typically FOLFIRI, trifluridine-tipiracil, or regorafenib), using hepatic progression-free survival (hPFS) as the primary endpoint and overall response rate and overall survival as key secondaries. Notably, the trial is powered to detect clinically meaningful differences in hepatic disease control, which has emerged as a validated proxy for overall outcomes in this patient population.

From a platform economics perspective, CRLM is transformative. The U.S. addressable population for third-line liver-dominant CRLM is estimated at 10,000-15,000 patients annually, an order of magnitude larger than mUM. Moreover, treatment sites for CRLM are often the same academic centers already activated for mUM, allowing Delcath to layer additional revenue per center without requiring incremental field buildout. Even modest penetration in this indication could support triple-digit revenue growth, with attractive gross margins and minimal SG&A expansion.

Beyond the numbers, CRLM validates the broad utility of the platform. If Delcath can show that its system improves liver disease control in one of the largest solid tumor indications, it will fundamentally reposition the company from an orphan-disease niche player to a mainstream procedural oncology business. The top-line readout is expected in 2026, making this trial the single most important clinical catalyst for the platform in the next 24-36 months.

HCC and iCCA: Optionality-rich expansion into broader hepatic oncology

Following CRLM, Delcath is targeting expansion into intrahepatic cholangiocarcinoma (iCCA) and hepatocellular carcinoma (HCC), two aggressive primary liver cancers where local progression drives morbidity and mortality. Both diseases are characterized by late-stage diagnosis, limited surgical candidacy, and suboptimal response to current systemic therapies.

While agents such as durvalumab (in HCC) and FGFR inhibitors (in iCCA) have modestly improved outcomes in subsets of patients, local control remains a major challenge, especially when tumors are refractory or confined to hepatic lobes.

In HCC, the challenge is greater: checkpoint inhibitors and tyrosine kinase inhibitors (TKIs) are now standard of care, but only a subset of patients experience durable response. Delcath’s system could theoretically be used in early-intervention, locoregional control, or as a second-line approach for patients with partial response.

However, the presence of competing liver-directed modalities (e.g. TACE, Y-90) and a more complex systemic-treatment backdrop make HCC a higher-risk, higher-uncertainty target. For this reason, Delcath appears to be approaching HCC cautiously, with trial timing and design yet to be finalized.

For iCCA, Delcath is currently designing a clinical development strategy that may begin with a Phase 2 basket trial, focusing on patients with unresectable, liver-confined disease who have failed first-line gemcitabine–cisplatin regimens.

Given the small patient population and lack of direct procedural competitors, iCCA represents a clinically high-need, low-competition indication that could be brought to market with relatively low trial cost and operational complexity. Preliminary feasibility studies, along with prior experience in similar perfusion protocols, suggest strong clinical rationale.

Strategically, both iCCA and HCC extend the clinical relevance and commercial breadth of the platform. Importantly, they do so without requiring any hardware changes. The same HEPZATO catheter, filtration system, and procedural setup can be used for all indications, making these programs essentially incremental revenue unlocks rather than new product lines. Over time, they also enhance Delcath’s positioning as a go-to platform for hepatic oncology interventions, a space with limited innovation and high hospital willingness to adopt specialized procedures.

Strategic indication sequencing: Platform economics by design

Delcath’s indication sequencing is not simply a function of clinical feasibility, it is a carefully staged platform development plan, designed to optimize regulatory de-risking, commercial compounding, and capital efficiency. Each step along the indication roadmap is chosen for its ability to validate new aspects of the platform while supporting increased utilization of existing infrastructure.

mUM proves that the system can be safely implemented, reimbursed, and scaled in a real-world setting.

CRLM is the commercial breakout, the first large-market test of platform utility and payer viability.

iCCA/HCC extend the platform horizontally into additional tumor types and broaden the clinical utility of the system.

Future potential expansions (e.g., breast, NETs, or pancreatic liver metastases) offer long-tail optionality without platform redesign.

This sequencing creates a compounding flywheel: each new indication increases site-level ROI, improves revenue per procedure suite, and deepens Delcath’s procedural moat. It also allows for reimbursement harmonization across tumor types, enhancing payer relationships and supporting the case for bundled or platform-based contracting models in the future.

From an investor’s standpoint, this structure enables a rare combination of clinical development leverage and commercial reusability, every R&D dollar has the potential to expand multiple revenue lines, and every new label expansion increases throughput without increasing commercial overhead. In a capital-constrained biotech environment, this stackable ROI profile is a distinguishing strength.

Delcath’s expansion strategy is not about breadth for its own sake, it’s about compounding utility across a stable, high-barrier platform. With each new indication, the company is not just unlocking more patients, it’s increasing the throughput and economic density of every center it serves.

The result is a rare biotech profile: capital-efficient growth, infrastructure reuse, and procedural entrenchment that deepens over time. This is not a pipeline of molecules, it’s a pipeline of leverage. And if the clinical data holds, Delcath won’t need to rebuild itself for each new market. It will just need to keep the system running.

Each new indication adds strategic weight, but it only matters if the market opportunity is large and accessible.

8. Market Opportunity

Delcath isn’t chasing tumor types, it’s building a procedural monopoly on the liver, one indication at a time.

To understand Delcath’s commercial potential, you have to think anatomically, not categorically. This is not a company going after discrete tumor types with separate pipelines, it’s a platform designed to dominate a single organ that plays a central role in the progression of countless solid tumors: the liver.

By anchoring its model in a repeatable, liver-specific therapy, Delcath is turning a fragmented oncology market into a unified procedural opportunity. This section breaks down how the company’s TAM is constructed not by chasing diseases, but by treating the place where they converge.

A liver-centric view of oncology: Why Delcath’s addressable market is structurally unique

The liver is one of the most frequent and consequential sites of metastatic spread for solid tumors. It is also the primary origin for some of the most aggressive cancers globally. This biological reality creates a uniquely centralized opportunity for Delcath: a therapy platform focused entirely on liver-directed oncology. The company’s proposition is not limited to a single tumor type, but rather to a shared clinical condition, liver-dominant disease, that occurs across many oncologic settings.

What makes this attractive from an investment standpoint is the procedural unification of a fragmented oncologic burden. Delcath is not developing separate solutions for each cancer subtype; it is building a system that targets the liver as a disease nexus, regardless of the primary tumor.

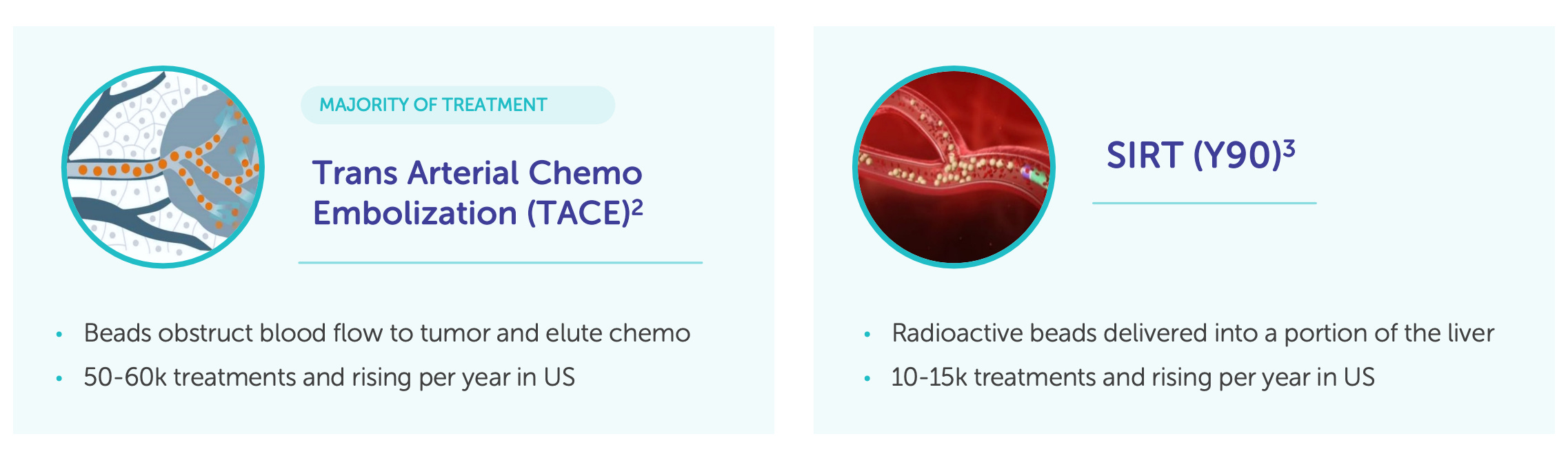

This anatomical focus creates a structurally unique addressable market. Solid tumor metastases to the liver are common in colorectal, breast, pancreatic, gastric, neuroendocrine, and ocular cancers. In fact, in colorectal cancer alone, more than 50% of patients develop liver metastases. Despite this, therapeutic solutions specifically optimized for liver control are extremely limited.

Conventional systemic chemotherapies have poor hepatic targeting and are often discontinued due to systemic toxicity. Local therapies such as transarterial chemoembolization (TACE) and radioembolization (Y-90) exist, but are either limited to certain anatomical distributions or restricted by patient liver function.