GORILLA TECHNOLOGY GROUP INC.

From Smart-City Integrator to AI Infrastructure Landlord: Assessing Whether a Credibility-Discounted Pivot Can Close the Gap Between a Multi-Billion-Dollar Pipeline and a Sub-$200 Million Revenue Base

1. Corporate Profile & The Strategic Pivot Thesis

The question this report keeps returning to is simple to state and hard to answer: has Gorilla Technology become an AI infrastructure company, or has it become very good at describing itself as one. The answer determines whether the multiple investors are being asked to pay reflects a business already under way or a narrative still ahead of its financial statements.

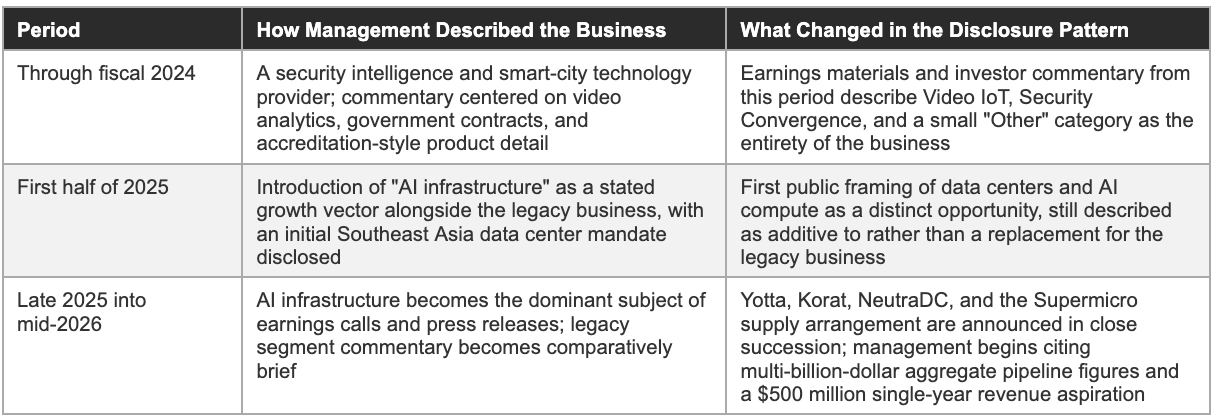

For most of its history the company built and sold video analytics, IoT security, and what it calls smart-city solutions, security convergence appliances, video intelligence platforms, and operational technology security, sold primarily to government and quasi-government buyers: police and criminal investigation agencies, transport authorities, port operators, and airport operators. The company reports its historical business across three segments, Video IoT, Security Convergence, and Other, a structure inherited from its 2022 listing and still in use in its most recent annual filing.

Beginning in 2025 and accelerating sharply through the first half of 2026, management’s public description of the business shifted. Where Gorilla had described itself as a security intelligence and smart-city technology provider, it began describing itself as a builder and operator of AI data center and GPU compute infrastructure, principally through a relationship with Yotta Data Services in India, a planned 200-megawatt campus in Korat, Thailand, and colocation capacity secured with NeutraDC in Indonesia.

Capital allocation followed the language: the company raised a $107 million convertible note in the second quarter of 2026 specifically to fund GPU purchases, hired more than 100 employees and contractors during 2026 to support infrastructure delivery according to management’s own count, and structured its most recent earnings call almost entirely around AI infrastructure milestones rather than the legacy security business.

The scale mismatch between the AI infrastructure narrative and the AI infrastructure financial statements is the defining feature of Gorilla’s investment case in mid-2026. Management has guided full-year 2026 revenue to a range of $160 million to $200 million, and separately described the Yotta relationship alone as supporting a potential annualized revenue base of more than $500 million once GPU compute and associated infrastructure services are both running, a figure the chief executive has used to argue that a $500 million revenue year is achievable for the company as a whole in 2027. The $500 million figure is best read as management’s own aspiration: it depends on hardware deliveries that had not yet occurred at the time of the most recent earnings call, on a single counterparty relationship, and on associated infrastructure services that are not yet contracted with the same specificity as the hardware deployment itself.

The legacy business deserves equal billing rather than treatment as an afterthought. Based on management’s own framing of segment mix at the upper end of 2026 guidance, AI data center and digital infrastructure revenue would represent 60% to 70% of revenue only at the $200 million end of the guided range, which implies the historical Video IoT and Security Convergence segments still account for the majority of revenue actually being recognized today, even as they receive a minority of management’s public attention.

Any assessment of Gorilla has to hold both businesses in view at once: a legacy security and smart-city integrator with a small number of government counterparties and a multi-decade operating history, and a newly announced AI infrastructure platform with billions of dollars in disclosed deal value and a fraction of that value yet converted into recognized revenue.

The market context behind the pivot is genuine even where the company’s own scale within it is not yet proven. India’s data center and AI compute capacity has been widely described, across industry and government commentary, as constrained relative to demand, with power availability and import logistics for high-end GPUs acting as binding constraints on how quickly any single operator, Gorilla included, can stand up capacity. Thailand and Indonesia occupy a comparable position a tier down in scale: both have stated national ambitions around digital infrastructure and both have a smaller existing base of hyperscaler-grade data center capacity than markets such as Singapore or Japan.

A real, underserved market does not by itself establish that a specific, thinly capitalized entrant will capture a durable share of it, and the demand backdrop behind the pivot is accordingly not the part of the story that calls for the most skepticism.

Execution, financing, and counterparty concentration are where the skepticism belongs, and they occupy the remainder of this report.

How management’s public narrative has shifted

2. Leadership, Capital Markets History & The Short-Seller Controversy

Three separate short sellers targeted Gorilla inside a fourteen-month window, each pointing at a different facet of the same underlying concern: that a company built around government security contracts learned to talk like a Silicon Valley infrastructure story faster than its disclosures kept pace. Sorting out which claims were substantiated, which were denied, and which remain unresolved is a precondition for valuing the stock rather than the story.

Jay Chandan has served as Chairman and Chief Executive Officer of Gorilla since the company’s mid-2022 listing, having chaired the special purpose acquisition company that brought Gorilla to the public market. The combination of sponsor and operating executive in one person removes a layer of independent deal scrutiny that a traditional listing process would otherwise apply to a company’s own pipeline disclosures, and it means the same individual who negotiated the terms of Gorilla’s public listing has also been the primary public voice behind the pipeline and backlog figures discussed throughout this report.

Bruce Bower was appointed interim Chief Financial Officer in the third quarter of 2024, following the prior Chief Financial Officer’s abrupt departure that quarter, and has since become the company’s permanent Chief Financial Officer, delivering the financial commentary on the company’s most recent earnings calls.

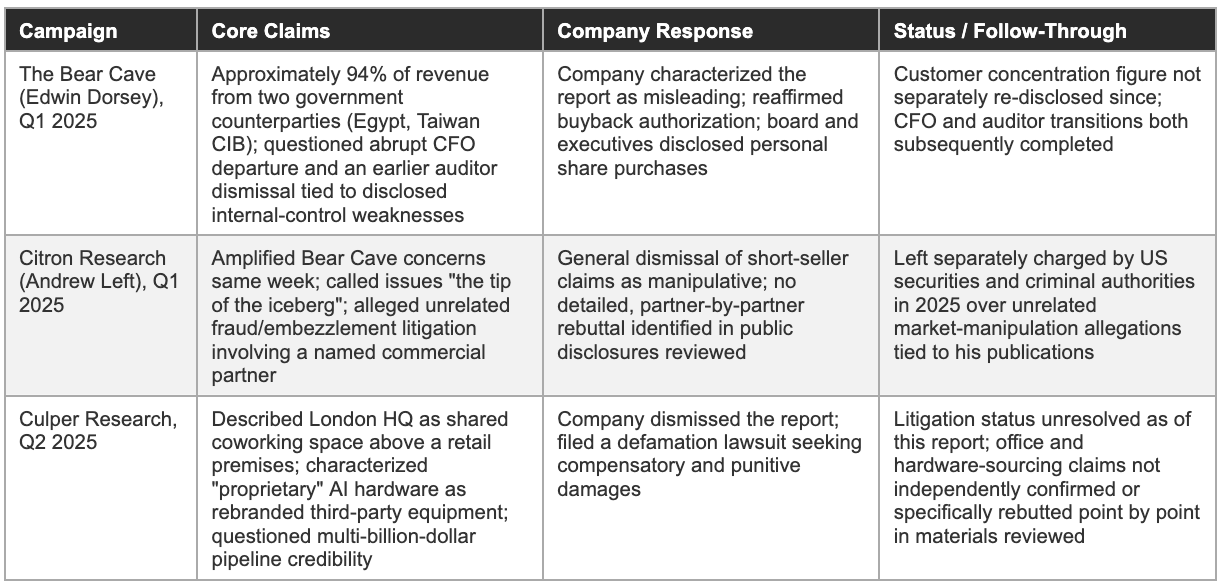

The first public short-seller report arrived in the first quarter of 2025 from Edwin Dorsey’s The Bear Cave, following a roughly tenfold increase in Gorilla’s share price over the preceding six months. The report’s central factual claim was that approximately 94% of Gorilla’s revenue derived from two customers, the government of Egypt and Taiwan’s Criminal Investigation Bureau, and it raised questions about the Chief Financial Officer departure and the earlier auditor dismissal.

Citron Research, run by Andrew Left, amplified the report the same week, calling Gorilla’s issues “the tip of the iceberg” and separately alleging that one of Gorilla’s announced commercial partners carried unrelated fraud and embezzlement litigation in Brazil.

A second, more detailed report followed roughly six weeks later from Culper Research, which described Gorilla’s London headquarters as a shared coworking address above a retail premises rather than a dedicated corporate office, characterized the company’s “proprietary” AI hardware as rebranded third-party desktop computers and cameras available commercially for a fraction of Gorilla’s stated cost, and questioned the credibility of the company’s multi-billion-dollar pipeline disclosures.

The company’s specific response to the buyback and insider-purchase signals it raised in 2025 is worth a closer, separate look, since a stated intention to buy back shares or a disclosed executive purchase carries different evidentiary weight depending on its scale and follow-through. Gorilla reaffirmed an existing share buyback authorization in the wake of the short-seller reports and pointed to disclosed purchases of shares by board members and executives, including the chief executive, as a signal of management’s own confidence in the business.

The dollar scale of those purchases relative to management’s overall equity stake, and the degree to which the buyback authorization was actually utilized rather than simply reaffirmed, were not detailed with enough granularity in the materials reviewed for this report to independently assess how large a signal either action represents; both are consistent with, but do not on their own prove, the confidence management has publicly expressed.

Gorilla’s response across all three campaigns followed a consistent pattern: public statements characterizing the reports as misleading or manipulative, reaffirmation of an existing share buyback authorization, public statements from board members and the executive team regarding personal share purchases, and, in the case of the Culper Research report, a defamation lawsuit seeking compensatory and punitive damages.

The company has also pointed out, accurately, that Andrew Left was separately charged by United States securities and criminal authorities in 2025 over allegations of market manipulation connected to his publications on other companies, a fact the company is entitled to raise and one investors should weigh on its own terms rather than treat as a blanket answer to every claim made by every short seller who has examined Gorilla.

Short-seller campaign chronology

None of the three reports has been definitively validated or invalidated by an independent regulatory finding as of mid-2026, and an investor evaluating Gorilla has to sit with that ambiguity rather than resolve it artificially in either direction. Some of the specific, checkable claims, the registered office description and the customer concentration figure in particular, can be verified independently over time through corporate filings and site visits, and the absence of a detailed, line-by-line company rebuttal of the more granular allegations leaves an unusually wide gap between what has been alleged and what has been specifically addressed.

Two further developments in 2026 are worth tracking under the same lens, not because either is alarming on its own but because both extend the company’s footprint beyond its core competency at exactly the moment investors are still working out whether that core competency itself, security integration turned infrastructure hosting, is being executed credibly.

The board added a director nomination in the second quarter of 2026 specifically tied to AI infrastructure strategy, alongside an increased strategic investment in Astrikos.AI, a minority equity position in an artificial intelligence company rather than a controlled subsidiary. Separately, Gorilla obtained regulatory approval from the UK Financial Conduct Authority in the first quarter of 2026 to acquire Shackleton Finance, a step the company has described as paving the way for a financial services arm to be branded Gorilla Tech Capital.

A security integrator that is simultaneously building AI data centers, taking minority stakes in AI startups, and acquiring a regulated consumer finance business inside the same eighteen-month window is, at minimum, a company whose management attention is spread across more simultaneous initiatives than its current revenue base or balance sheet would typically support, and that breadth is worth weighing against the execution risk already identified in the AI infrastructure build-out itself.

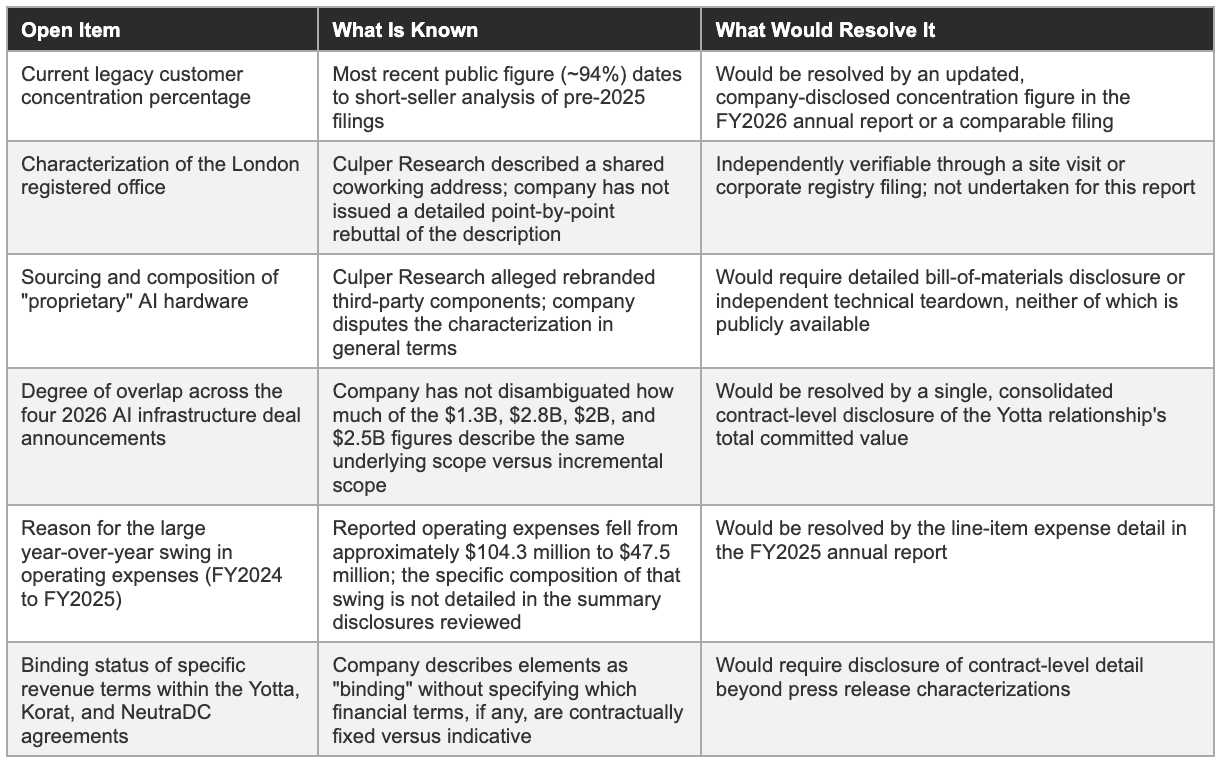

Open verification items

The table below catalogues the specific factual questions this report could not independently resolve using public information available as of mid-2026. None of these gaps should be read as a finding against the company; they are listed so a reader can track exactly which figures in this report rest on company self-disclosure versus independent confirmation, and can watch for the specific filing or disclosure that would resolve each one.

3. Business Model Architecture & Customer Concentration

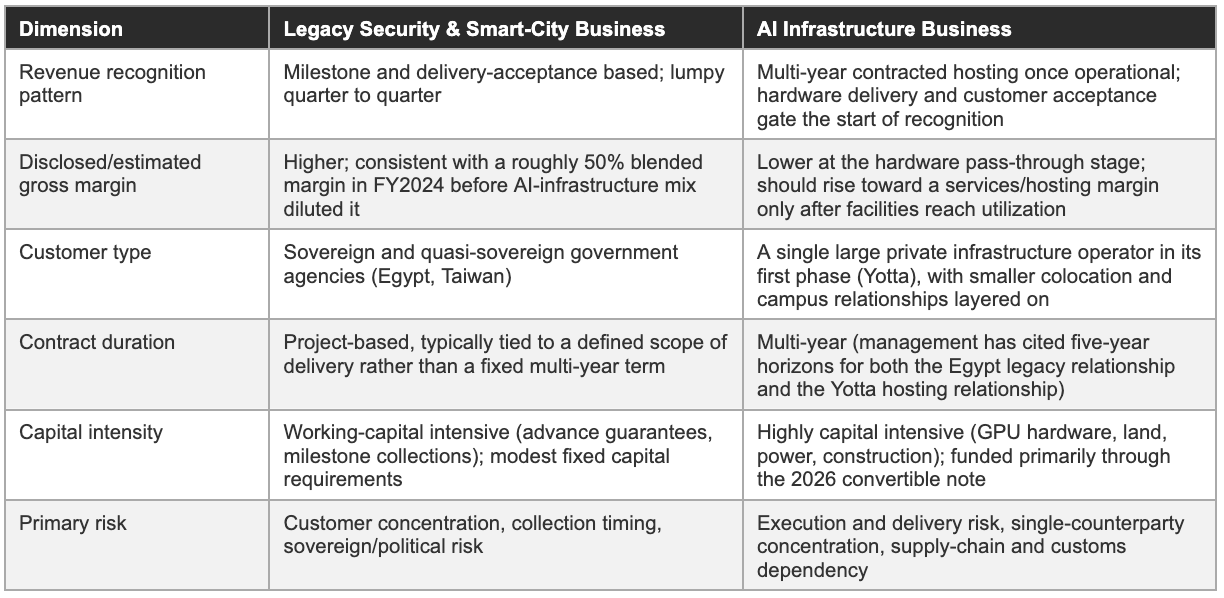

Gorilla today is best understood as two businesses sharing one income statement: a project-based security and smart-city integrator with a small, concentrated, largely sovereign customer base, and an emerging infrastructure-hosting business whose economics and customer concentration are still being formed in real time. Treating the combined entity as a single, coherent platform risks averaging away the very different risk each business carries on its own.

The legacy business sells security and smart-city technology, video analytics platforms, IoT security appliances, business intelligence software, and integration services, into long-cycle, project-based contracts with government and quasi-government buyers. Revenue recognition on these contracts is tied to project milestones and delivery acceptance rather than to a recurring subscription, which means revenue can be lumpy quarter to quarter even when the underlying relationship is durable; management’s own commentary about collecting overdue invoices from large customers and reducing advance payment guarantees in the first quarter of 2026 is itself evidence that working capital and collection timing have been a live operational issue on this side of the business.

The most specific public figure on customer concentration comes from the first short-seller report discussed in the previous section: approximately 94% of revenue derived from two customers, the government of Egypt and Taiwan’s Criminal Investigation Bureau, as of the period that report examined in early 2025. Gorilla has not, in the disclosures reviewed for this report, published an updated concentration percentage specific to its legacy business since that figure was raised, so the number above should be read as the most recently available public estimate rather than a current, company-confirmed figure.

What has changed concretely is the status of the Egypt relationship: management disclosed in its first-quarter 2026 results that advance payment guarantees tied to large customers fell from the tens of millions of dollars historically to approximately $45,000, and that the Egypt project had moved into final implementation with five years of recurring revenue expected once that phase completes. A concentration ratio in the low-to-mid nineties percent, even spread across a government counterparty with a long operating history, carries currency conversion risk, political risk, and payment timing risk that a diversified private-sector channel partner generally does not.

The AI infrastructure side of the business being assembled through 2025 and 2026 looks structurally different from the legacy model. Rather than selling finished software and integration services, Gorilla is positioning itself as an intermediary that sources GPU hardware, through arrangements such as the one disclosed with Supermicro for the India deployment, secures land, power, and colocation capacity, and then either hosts compute for a single large counterparty, Yotta in India, or leases data center capacity to enterprise customers through the NeutraDC colocation arrangement in Southeast Asia.

This sits closer to a capital-intensive infrastructure leasing or GPU-as-a-service model than to the project-based integration model that built the legacy business, with heavy upfront capital deployment for hardware and facilities, multi-year contracted revenue once operational, and an early-stage single-counterparty concentration risk that is arguably as acute as the legacy business’s two-customer concentration: as of mid-2026 the disclosed AI-infrastructure deal value is overwhelmingly tied to one relationship, Yotta, with the Thailand and Indonesia initiatives still in earlier stages of construction or capacity build-out.

Two businesses, side by side

The two business models carry different gross margin profiles, and the consolidated financial statements show it plainly. Reported gross margin compressed from roughly 50% in fiscal 2024 to roughly 33% in fiscal 2025 even as revenue grew by more than a third, consistent with a business mix shifting toward hardware-heavy delivery, GPU and server procurement, network equipment, data center build costs, that carries materially lower margin than the software-and-services-heavy legacy security business.

If the AI infrastructure business continues to grow faster than the legacy business, as both guidance and management’s public commentary suggest it will, the consolidated gross margin path investors should expect over the next several quarters is further compression, at least until the infrastructure assets reach utilization levels that allow services and recurring hosting revenue, which should carry a higher margin than the initial hardware pass-through, to become a larger share of the AI infrastructure segment’s own mix.

The company’s segment disclosure does not yet break the AI infrastructure activity out as its own reporting segment; it sits within or alongside the existing Video IoT, Security Convergence, and Other categories depending on the period and the specific filing, which limits how precisely an outside investor can separate legacy-business performance from AI-infrastructure performance using the financial statements alone.

This is a disclosure-design choice rather than a violation of any standard, and it is common for companies in the early stages of a new business line, but it does mean that the gross margin compression discussed above, and the revenue growth figures discussed in the next section, are consolidated numbers that blend two businesses with different unit economics, different customer concentration, and different growth trajectories.

A reporting structure that separated AI infrastructure into its own segment with its own revenue, cost of revenue, and capital expenditure would let investors test management’s claims about the new business’s economics directly; until that happens, the most reliable way to track the AI infrastructure business specifically is through the deal-level disclosures covered in the next section and the milestone tracker later in this report, rather than through the consolidated income statement.

4. The AI Infrastructure Build-Out: Yotta, Korat and the Supply Chain

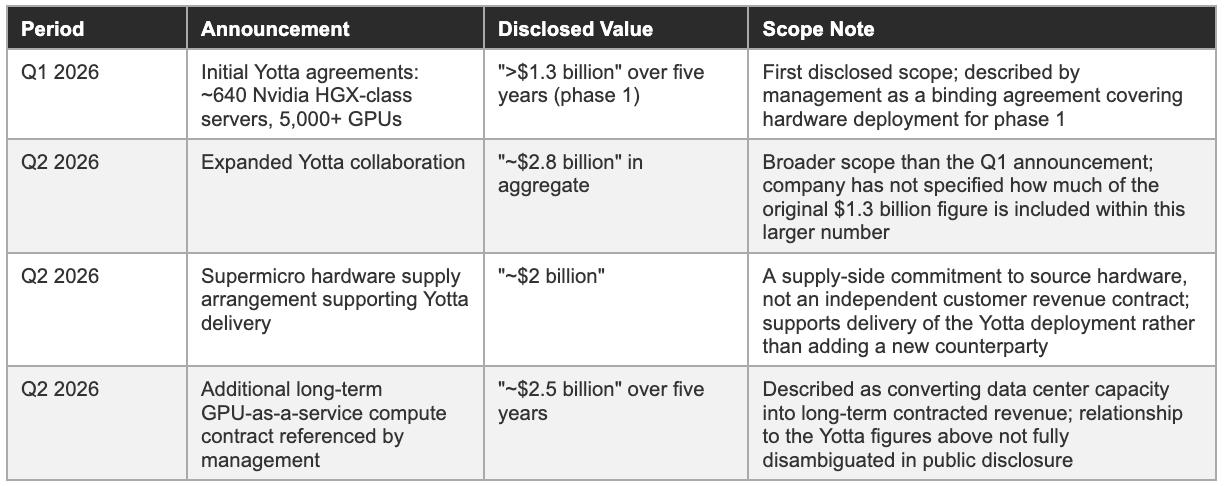

Every figure in this section originates from a company press release or an earnings call rather than from an audited contract filed with a securities regulator, and the distinction between a binding agreement, an expanded collaboration, and a value the company says a relationship “represents” matters more here than anywhere else in this report.

Gorilla’s relationship with Yotta Data Services in India was disclosed in stages across the first half of 2026. The company described signing agreements with Yotta in the first quarter of 2026 covering a deployment of approximately 640 high-performance Nvidia GPU servers, more than 5,000 graphics processing units in aggregate, which management said it expected to contribute more than $1.3 billion of revenue over five years once the first phase is fully deployed.

A further announcement in the second quarter of 2026 described an expanded collaboration with Yotta valued by the company at approximately $2.8 billion in aggregate, and a separate announcement the same quarter disclosed a roughly $2 billion hardware supply arrangement with Supermicro specifically to support the Yotta deployment’s delivery schedule.

The escalating figures across these three announcements, $1.3 billion, then $2.8 billion, then a further $2 billion supply arrangement, describe an expanding and partially overlapping scope of the same underlying relationship rather than three independent, additive sources of revenue; the company’s disclosures do not cleanly separate how much of the later, larger figures supersede the earlier ones as opposed to adding to them.

The escalating disclosed deal value: A closer look

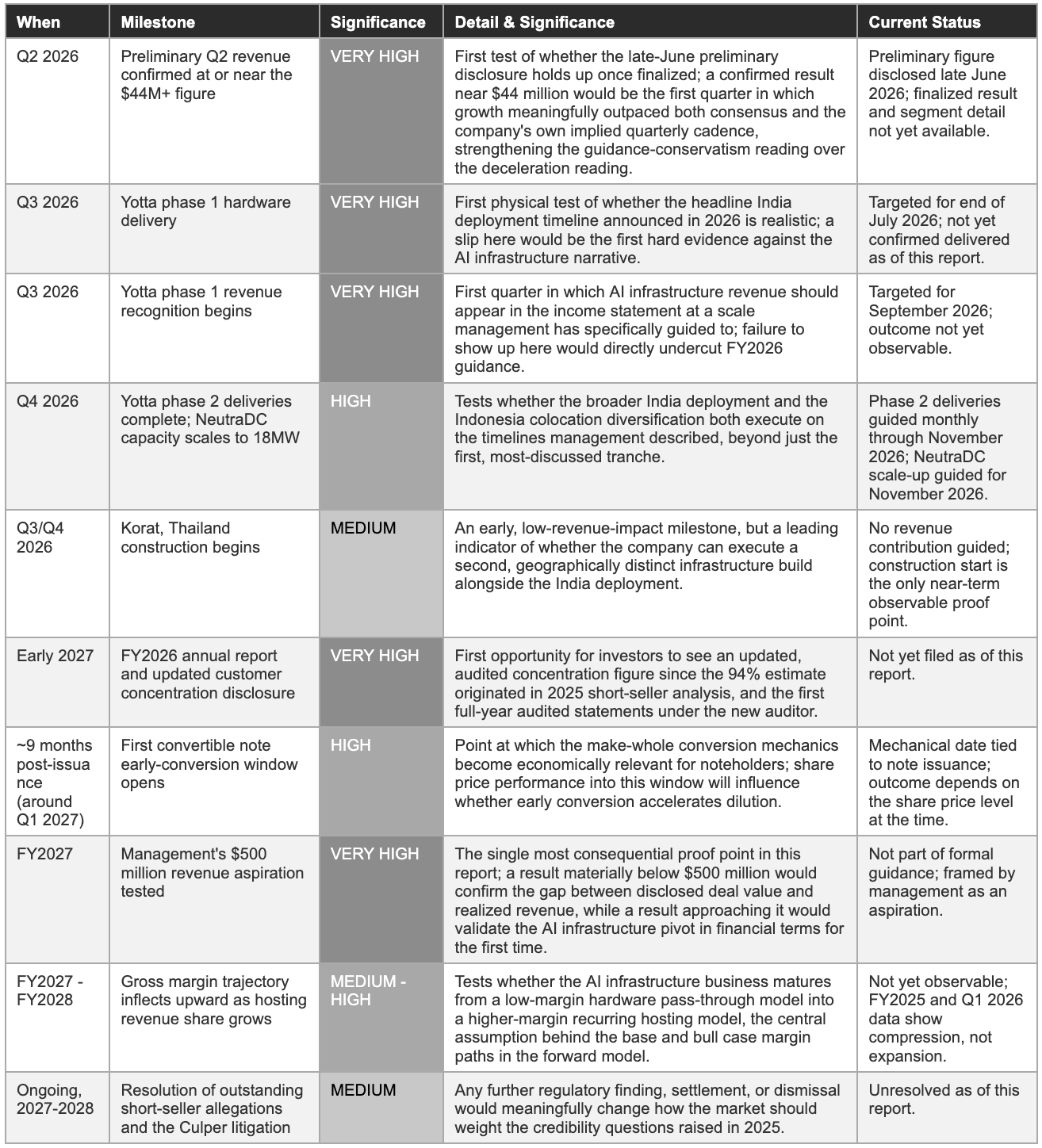

On the first-quarter 2026 earnings call, management described the delivery schedule in specific terms: the first phase of hardware delivery was targeted for the end of July 2026, with associated revenue recognition beginning in September 2026; a larger second phase was targeted to begin delivery at the end of August 2026 and continue on a monthly cadence through November 2026, with revenue recognition expected across the fourth quarter. As of the period covered by this report, none of these milestones had yet been reached, which means the entire revenue contribution from the Yotta relationship embedded in 2026 guidance and in management’s 2027 aspiration remains forward-looking and contingent on hardware arriving, being installed, and being accepted on the schedule management has described.

Gorilla announced plans in the second quarter of 2026 for a 200-megawatt AI data center campus in Korat, Thailand, with construction targeted to begin in the third or fourth quarter of 2026. This is an early-stage, multi-year infrastructure commitment; no revenue contribution from the Korat campus is embedded in current guidance, and the project’s progress depends on local permitting, power availability, and construction execution that sit largely outside Gorilla’s direct control as project sponsor.

Gorilla also disclosed an arrangement with NeutraDC in the second quarter of 2026 for an initial 5.5 megawatts of data center capacity in Southeast Asia, with capacity expected to scale to 18 megawatts by November 2026; management has indicated colocation revenue from this relationship should begin in the third or fourth quarter of 2026. The Indonesia and Thailand initiatives, taken together, read as the company’s attempt to diversify its AI infrastructure exposure beyond the single Yotta relationship, though both remain materially smaller in disclosed scale than the India deployment and both remain pre-revenue as of the most recent quarterly disclosure available.

Several of Gorilla’s announcements describe agreements as binding, and management has stated on earnings calls that guidance is built from contracted revenue rather than pipeline assumptions. A binding contract for hardware deployment carries a different commitment than a binding, multi-year revenue contract with defined pricing, volume, and termination terms, and the public disclosures reviewed for this report do not provide enough detail to confirm which specific elements of the Yotta, Korat, and NeutraDC relationships carry firm, enforceable revenue commitments as opposed to framework agreements describing an intended scope of work subject to further definitive documentation. Every dollar figure in this section should be read as management’s own characterization of deal value rather than as independently confirmed, audited contract value, with the realized revenue trajectory in 2026 and 2027 standing as the only reliable test of how much of the disclosed pipeline converts into cash.

Two further execution variables sit underneath the headline delivery dates and deserve explicit attention because they are largely outside Gorilla’s control.

The first is GPU allocation: Nvidia’s highest-demand data center chips remain supply-constrained globally, and a company of Gorilla’s size sourcing thousands of units through a named supply partner, Supermicro in this case, is dependent on that partner’s own position in the broader allocation queue rather than on a direct, negotiated allocation from Nvidia itself. A delay or reduction at the Supermicro level would flow through directly to Gorilla’s delivery schedule regardless of how well Gorilla itself executes on land, power, or staffing.

The second is customs and import logistics specific to India, where high-value electronics imports of this scale typically require duty classification, licensing, and customs clearance steps that can introduce delay independent of manufacturing or shipping timelines; the company’s own delivery targets, hardware arriving by the end of July 2026 and a second phase running through November 2026, leave limited buffer for either a supply-chain slip at the Supermicro level or a customs delay at the India border, which is part of why the milestone tracker later in this report treats the initial delivery date as a very high-significance, near-term observation rather than a routine operational update.

Yotta Data Services itself is worth a brief, separate characterization, since the credibility of the entire AI infrastructure thesis rests substantially on a single counterparty’s own ability to deliver its side of the relationship. Yotta is an Indian data center and cloud infrastructure operator, part of the Hiranandani Group, an established Indian real estate and infrastructure conglomerate, and has positioned itself publicly as a builder of sovereign AI compute capacity for the Indian market.

Yotta’s own scale and balance sheet have not been independently verified for this report in the same depth as Gorilla’s public filings, since Yotta is not itself a listed company subject to the same disclosure requirements; the relationship’s credibility therefore rests in part on the standing of its parent conglomerate and in part on Gorilla’s own characterization of the agreement’s terms, a degree of counterparty opacity that is itself worth weighing alongside the execution risks already discussed.

5. Capital Structure & Dilution Mechanics

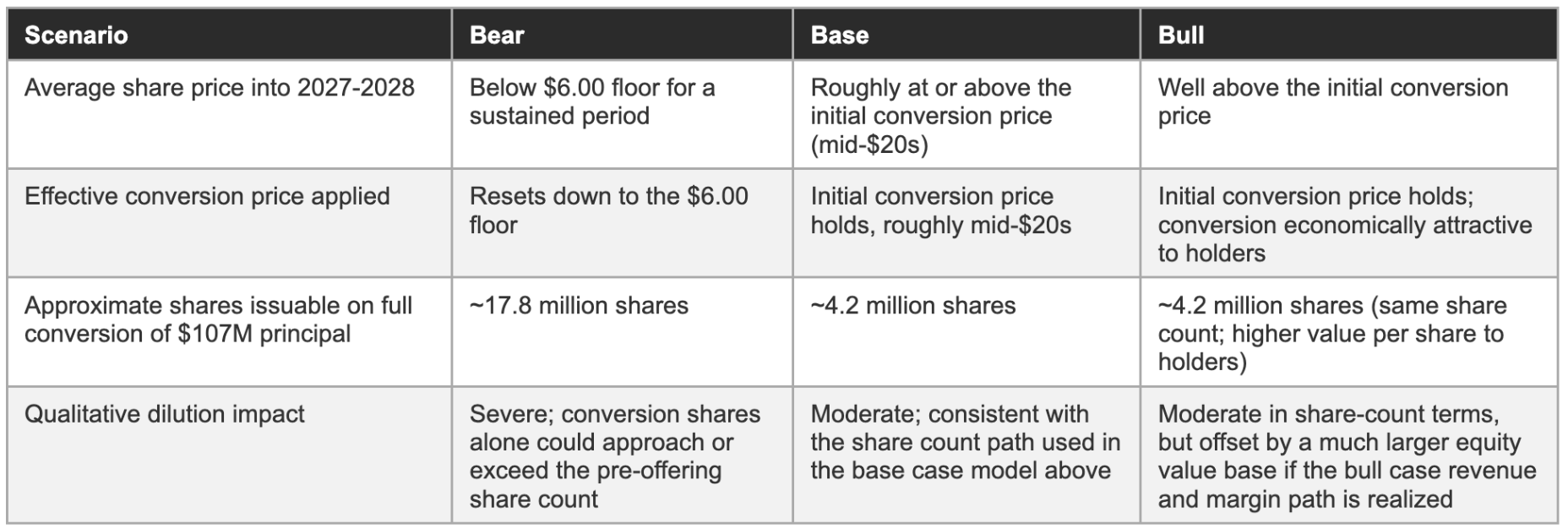

Building gigawatts of AI infrastructure costs real money up front, and Gorilla has chosen to fund that build-out with a financing instrument whose dilution profile is asymmetric: shareholders absorb most of the downside if the stock underperforms and share the upside only above a fixed conversion price. The mechanics of that instrument matter for modeling the share count an investor will actually own three years from now.

Gorilla priced $107 million in aggregate principal amount of senior unsecured convertible notes in the second quarter of 2026, due in 2031, carrying a 7.50% coupon payable semi-annually in cash or, at the company’s election, in ordinary shares. Net proceeds after placement fees were approximately $102 million, earmarked specifically to fund GPU purchases tied to the AI infrastructure build-out. The initial conversion rate was set at approximately 39.24 ordinary shares per $1,000 of principal, implying an initial conversion price in the mid-$20s per share, a premium of roughly 17% to the share price at the time of pricing.

The notes include a periodic conversion-price reset mechanism alongside a stated floor of $6.00 per share below which the conversion price cannot reset further, and a separate make-whole provision that increases the conversion rate for holders who convert early, before a date in 2029, by an amount tied to the interest payments those holders would otherwise have received through that date.

A reset mechanism paired with a low floor means the dilution math on these notes is not fixed at the initial conversion price: if the shares trade meaningfully below that price for an extended period, the conversion price can reset downward, increasing the number of shares the company would need to issue to retire the notes through conversion rather than cash repayment. The notes also carry a call option for the company beginning in 2029 and customary repurchase rights for holders on certain corporate transactions.

The offering was led by Highbridge Capital Management, described by the company as a current institutional stakeholder in Gorilla. A financing arrangement led by an existing shareholder is not unusual in small-capitalization capital markets, where issuer size limits the pool of institutions willing to underwrite a convertible offering, though it does mean the pricing and structure of the notes were negotiated with a counterparty that already held an economic interest in the company’s equity performance, a dynamic worth weighing when assessing whether the terms, the conversion premium, the coupon, the floor, were struck at arm’s-length market terms.

The coupon itself is a smaller but still relevant dilution lever. At 7.50% on $107 million of principal, annual interest amounts to approximately $8.0 million; if the company elects to pay that interest in shares rather than cash, which the note terms permit, roughly 320,000 to 400,000 additional shares would be issued each year depending on where the shares are trading at each semi-annual payment date, an amount that is modest on its own but adds up over the note’s term to 2031 if the company consistently chooses the equity-settlement option to conserve cash during the AI infrastructure build-out.

Separately from the convertible notes, Gorilla disclosed in its most recent annual filing that restricted stock units granted in the first quarter of 2026 could generate stock-based compensation expense in the range of $20 million to $23 million for fiscal 2026, excluding any further expense from performance-based units tied to market conditions. Stock-based compensation of that size, against a revenue base in the $160 million to $200 million range, is a meaningful drag on reported profitability before accounting for the dilution from the shares those units eventually settle into, and it compounds the dilution math from the convertible notes rather than substituting for it.

Between the convertible note’s potential conversion shares, the disclosed restricted stock unit grants, and any further equity issuance the company may need if the AI infrastructure build-out requires more capital than current cash and note proceeds can fund, the fully diluted share count an investor should expect to own against in two to three years is likely to be measurably higher than the share count outstanding today. Building data center capacity is capital-intensive by nature, and convertible debt is a standard tool for funding it. The forward financial model later in this report accounts for a rising share count alongside rising revenue and earnings, and the bull case for the stock requires the underlying business to grow into the dilution rather than around it.

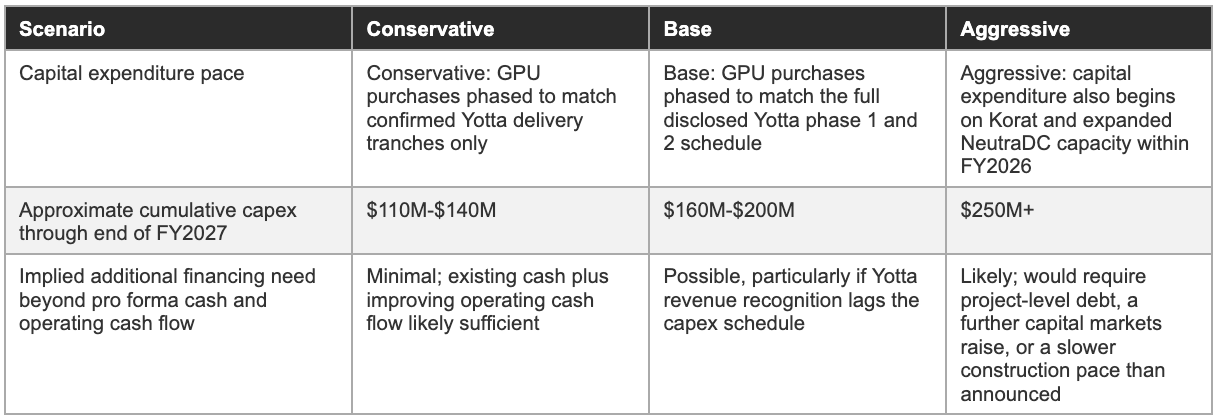

Cash runway under three capital expenditure paths

The pro forma cash position following the convertible note offering, combined with the planned pace of GPU purchases tied to the Yotta and broader AI infrastructure build-out, determines how much runway the company has before it needs to return to capital markets. The table below sketches three illustrative capital expenditure paths against the pro forma cash position discussed in the valuation section of this report, holding operating cash flow from the legacy business roughly flat at recent levels.

6. Financial History & The Guidance Credibility Question

Gorilla’s revenue has compounded quickly for three straight years, and on its own that fact would normally support a constructive view of the business. The complication is that profitability has not compounded alongside it, that guidance has been revised upward inside the same year it was issued, and that the gap between the size of the pipeline management describes and the size of the revenue base it actually guides to has widened rather than narrowed as the AI-infrastructure story has developed.

Reported revenue grew from roughly $65 million in fiscal 2023 to $74.7 million in fiscal 2024, an increase of approximately 15%, and then to $101.4 million in fiscal 2025, an increase of 35.7%, a clear re-acceleration that predates most of the AI infrastructure announcements and reflects growth in the legacy security and smart-city business as much as anything else. Growth accelerated further in the first quarter of 2026, with revenue of $28.2 million representing a 55% increase year over year, though half-year 2025 revenue had already grown 90% year over year off a smaller base, illustrating how volatile the year-over-year growth rate can look from one period to the next given the project-based, lumpy nature of legacy contract recognition.

The more important fact sits below the revenue line. Adjusted EBITDA was $19.1 million in fiscal 2025, essentially flat against $20.0 million in fiscal 2024, despite revenue growing by more than a third; adjusted net income similarly slipped from $21.2 million to $19.9 million over the same period. A business growing revenue 36% while adjusted profitability stays flat or declines is showing a different dynamic than the operating leverage usually associated with a scaling, software-and-services-driven growth story: the pattern lines up instead with incremental revenue coming from a lower-margin source than the existing base, consistent with the gross margin compression described in the business model section.

The pattern continued into the first quarter of 2026: revenue grew 55% year over year, but adjusted EBITDA swung from a positive $5.2 million in the first quarter of 2025 to a loss of $8.3 million in the first quarter of 2026, the first negative adjusted EBITDA quarter the company has disclosed since its 2025 turnaround narrative began. Reported operating losses in the first quarter of 2026 were considerably larger still, at $41.1 million, though management has attributed most of that figure to a $20.9 million stock-based compensation charge and an $18.9 million foreign-exchange loss, leaving an underlying operating loss closer to $1.2 million once both items are excluded.

The $8.3 million adjusted EBITDA loss already excludes stock-based compensation under the company’s own definition, so the swing from positive to negative adjusted EBITDA reflects a real increase in underlying operating costs tied to the AI infrastructure build-out rather than an accounting artifact alone.

The one unambiguously positive financial data point in the first quarter of 2026 was cash flow. Net cash from operating activities was a positive $6.6 million, an improvement of $17.3 million from the $10.7 million of cash used in operating activities in the first quarter of 2025, and the company ended the quarter with $98.4 million of cash and equivalents, up 373% year over year, with management specifically noting that advance payment guarantees tied to major projects had fallen from the tens of millions of dollars historically to approximately $45,000.

That improvement, collections from large legacy customers finally working their way through the balance sheet, is real and worth crediting on its own terms; it sits alongside, rather than resolves, the adjusted EBITDA deterioration described above, since cash collected from old project milestones and cash generated by new, profitable operations are not the same thing.

The quarterly shape of 2025 revenue is itself informative about how lumpy the legacy, project-based business remains even as the full-year growth rate looks smooth. First-quarter 2025 revenue was approximately $18.2 million, implied by management’s disclosure that first-quarter 2026 revenue of $28.2 million represented 55% year-over-year growth; first-half 2025 revenue of $39.3 million, up 90% year over year, implies second-quarter 2025 revenue of roughly $21.1 million.

Full-year 2025 revenue of $101.4 million then implies second-half 2025 revenue of roughly $62.1 million, more than half the full year’s total concentrated in the back two quarters, consistent with the project-based, milestone-driven recognition pattern described earlier in this report. Investors modeling 2026 should expect a similar back-half weighting, reinforced rather than offset by the Yotta delivery schedule, which itself concentrates anticipated revenue recognition in the third and fourth quarters of 2026.

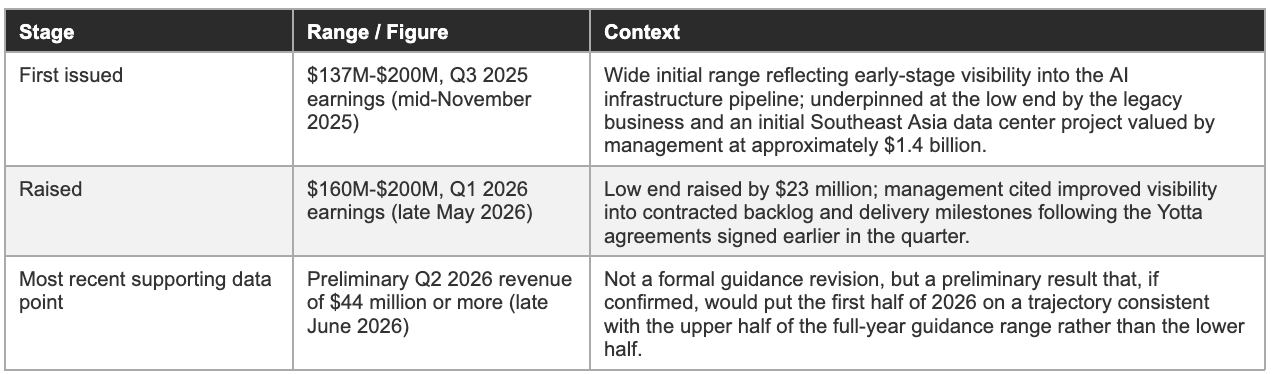

The most recent data point available at the time of this report is a preliminary disclosure, issued ahead of finalized quarterly results, that second-quarter 2026 revenue is projected to exceed $44 million, against a roughly $33 million analyst consensus estimate and against $21.1 million in the second quarter of 2025. A figure of that size would represent sequential growth of more than 55% from the first quarter of 2026 and more than 100% growth year over year, and management attributed the increase specifically to execution under active customer contracts and conversion of signed commercial commitments into recognized revenue, language that, if accurate, would mark the first quarter in which AI infrastructure-related delivery shows up in the topline ahead of the September revenue-recognition start date management had previously guided for the Yotta relationship specifically.

The figure remains preliminary and subject to quarter-end closing procedures as of this report, and it has not yet been accompanied by the segment-level or margin detail that would confirm how much of the beat is AI infrastructure-related versus legacy-business timing. It is, nonetheless, the most directly relevant near-term evidence available against the guidance credibility question this report raises throughout, and a confirmed result anywhere close to the preliminary figure would meaningfully strengthen the case that the 2026 guidance range understates rather than overstates what the business can deliver.

Gorilla’s full-year 2026 revenue guidance was raised in the first quarter of 2026 to a range of $160 million to $200 million, up from a previously disclosed low end of $137 million, with management citing improved visibility into contracted backlog and delivery milestones. Raising guidance after a strong quarter is, on its own, a favorable signal. The harder question is how to read the gap between that guidance and the figures management uses in the same breath to describe the company’s longer-term opportunity: a signed backlog and executable opportunity said to exceed $5 billion, with a further pipeline said to exceed another $5 billion, against guided 2026 revenue of, at the top end, $200 million.

For comparison, the company’s own rebuttal to short-seller criticism in early 2025 cited a backlog of $93 million; the jump from $93 million to a figure in excess of $5 billion inside roughly a year reflects the addition of the AI infrastructure deals discussed earlier in this report far more than it reflects organic growth in the legacy backlog, and a backlog figure that mixes signed contracts with an unspecified amount of executable opportunity is a lower-quality disclosure than a contractually committed order book broken out by counterparty and delivery date. The $5 billion-plus figure is best treated as a rough indication of the scale of opportunity management believes it is pursuing rather than a number that can be divided by a run-rate to produce a reliable revenue forecast.

FY2026 Guidance: A short history

One further item in the consolidated income statement deserves a note of caution rather than a confident explanation. Reported operating expenses fell from approximately $104.3 million in fiscal 2024 to approximately $47.5 million in fiscal 2025, a swing large enough on its own to be the single biggest driver of the improvement in reported net loss between the two years, alongside the revenue growth already discussed.

The summary disclosures reviewed for this report do not provide enough line-item detail to confirm what drove a swing of that size, whether a one-off charge or impairment inflated the 2024 figure, a one-off credit or reversal reduced the 2025 figure, or the change reflects a more mundane combination of normal cost discipline and currency effects. Until the FY2025 annual report’s full expense detail is reviewed against this question specifically, the operating expense trend should be treated as a meaningful open item rather than as confirmed evidence of structural cost discipline.

The single most useful piece of information that does not yet exist in public disclosure is a quarter, or two, in which actual Yotta-related revenue shows up in the income statement at a scale consistent with management’s own timeline. Until that happens, the most defensible reading of Gorilla’s financial history is that the legacy business has demonstrated real, if uneven, revenue growth and a recent improvement in cash collection, while the AI infrastructure business has demonstrated an ability to sign large headline agreements faster than it has demonstrated an ability to convert them into recognized revenue or sustained adjusted profitability.

7. Competitive Landscape & Technology Position

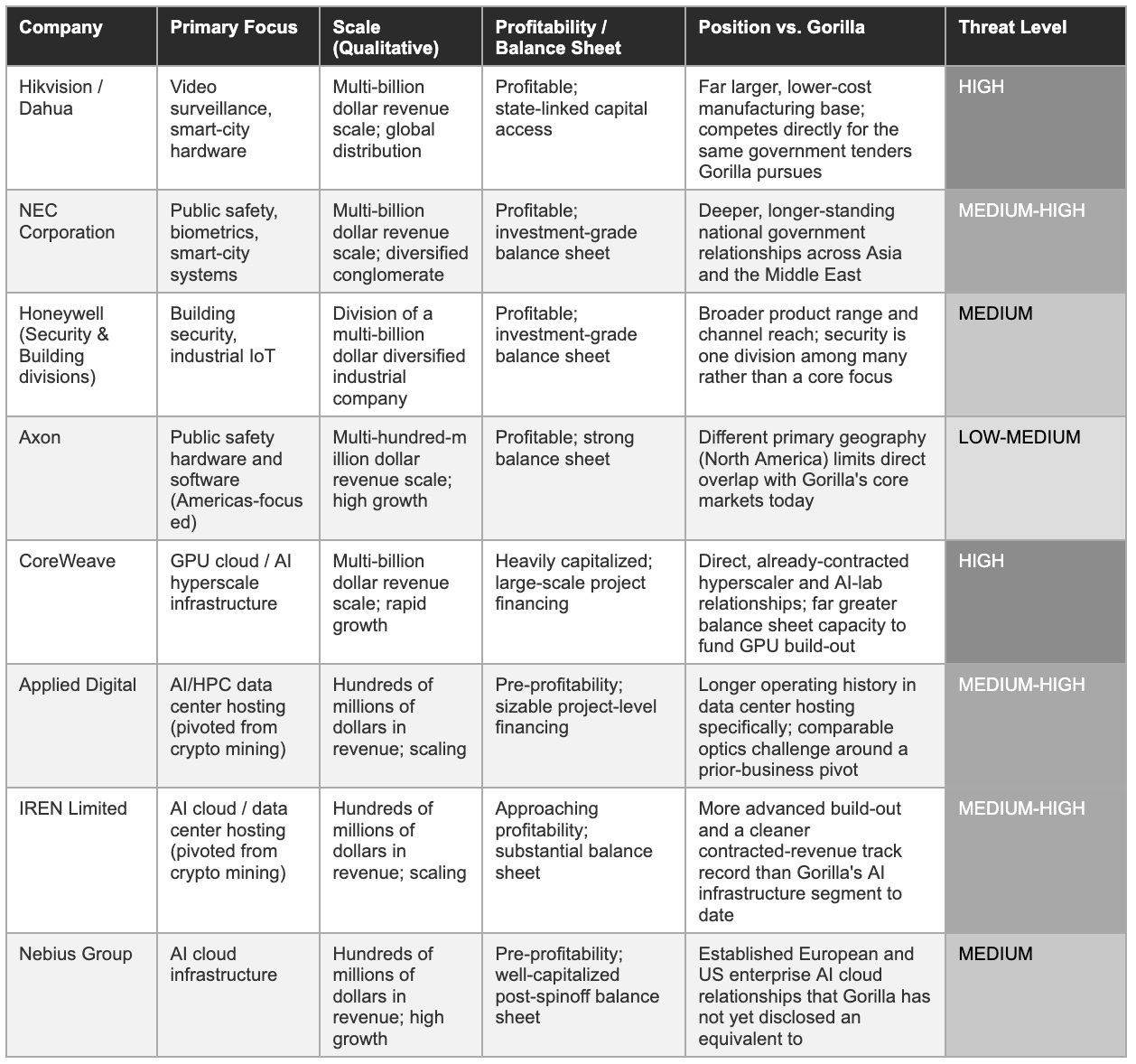

Gorilla competes in two markets that have almost nothing in common except that they currently report into the same income statement: a crowded, mature security and smart-city integration market dominated by far larger incumbents, and an even more crowded, better-capitalized AI infrastructure and GPU hosting market where Gorilla is a recent entrant with a fraction of the balance sheet its new competitors carry.

In security intelligence, video analytics, and smart-city integration, Gorilla competes against a mix of large, diversified incumbents, Hikvision, Dahua Technology, NEC Corporation, Idemia, and Honeywell’s building and security divisions, and more specialized public safety software vendors such as Axon and Genetec. Most of these competitors are larger than Gorilla by a wide margin, several carry more diversified customer bases across commercial and government channels, and several have deeper, longer-standing relationships with the kind of national government buyers Gorilla depends on for the bulk of its legacy revenue.

Gorilla’s competitive position in this market has rested historically on price and on relationships with specific government counterparties in Taiwan, Egypt, and a handful of other jurisdictions, rather than on a demonstrable technology advantage; the short-seller claims discussed earlier in this report, that Gorilla’s proprietary AI hardware is in substantial part rebranded third-party equipment, are consistent with a company competing primarily on integration and relationship rather than on differentiated underlying technology, a characterization Gorilla disputes.

The AI infrastructure and GPU hosting market Gorilla has entered includes well-capitalized, purpose-built competitors such as CoreWeave, Applied Digital, IREN, Core Scientific, and Nebius Group, several of which already carry multi-year, large-counterparty contracts generating disclosed revenue at a multiple of Gorilla’s current scale, balance sheets supported by far larger equity and debt raises, and, in some cases, direct relationships with major cloud and AI model providers that Gorilla has not disclosed.

Several of these competitors carry their own optics challenges of their own, more than one began as a cryptocurrency mining operation before pivoting to AI hosting, so Gorilla’s pivot narrative is not unique within the sector; it is smaller, less capitalized, and earlier in converting announced capacity into contracted, billed revenue than the more established names in the group.

Gorilla’s structural disadvantage in the AI infrastructure market is straightforward to describe. Scale and access to capital are the primary competitive variables in GPU hosting, since the underlying hardware is broadly the same Nvidia silicon available to any well-funded buyer, and the main differentiators are the cost of capital used to acquire it, the speed of securing power and land, and the credibility of the counterparty relationships needed to sign long-duration hosting contracts. A $107 million convertible note funds a fraction of the gigawatts of capacity that better-capitalized neocloud competitors are deploying with billion-dollar-scale project financing, and Gorilla’s single-counterparty concentration in India compares unfavorably with competitors that have diversified their hosting customer base across multiple large enterprise and hyperscaler relationships.

The capital-intensity gap is large enough to put in concrete terms. Industry cost estimates for a modern AI data center campus, covering construction, power infrastructure, and GPU hardware together, commonly run from roughly $10 million to $15 million per megawatt of critical IT load, depending on chip generation and power density. Against that range, a single 200-megawatt campus such as the one Gorilla has announced for Korat could require on the order of $2 billion to $3 billion of cumulative capital across construction and equipment phases, a figure that dwarfs the $107 million the company has raised to date and implies that the bulk of the capital for Korat specifically, beyond an initial development phase, has yet to be sourced, whether from project-level debt, a joint-venture structure, or further capital markets issuance not yet disclosed.

Gorilla has not disclosed a patent portfolio, a proprietary chip design, or another defensible technology asset that would differentiate its AI infrastructure offering from a well-funded competitor assembling similar Nvidia-based server racks; the company’s stated value proposition rests on integration speed, relationships with local partners in India, Thailand, and Indonesia, and the ability to source hardware through arrangements such as the Supermicro supply agreement, rather than on technology a competitor could not replicate given sufficient capital. This is a meaningfully different position from a company protecting a multi-year evidence base or a regulatory accreditation stack, and it means Gorilla’s primary defense against competitive displacement in AI infrastructure is execution speed on the deals already signed, rather than a moat that compounds with time.

Competitive positioning across both markets

The split in the table above is itself the clearest illustration of Gorilla’s competitive position: against legacy security peers, the threat comes from scale and relationship depth rather than technology; against AI infrastructure peers, the threat comes from capital access and contracted-revenue maturity rather than geography. Gorilla is not positioned as the technology leader in either market, and its competitive argument in both cases rests on being faster, more locally embedded, or more willing to pursue specific government and emerging-market relationships than larger, more conservative competitors.

That can be a workable strategy for a company of Gorilla’s size, smaller, focused entrants have taken share from larger incumbents in security integration before, but it places a higher burden on execution and counterparty management than a strategy built around a defensible technology or evidence moat would, and it leaves less room for error if either the legacy government relationships or the new AI infrastructure counterparties prove harder to manage than disclosed.

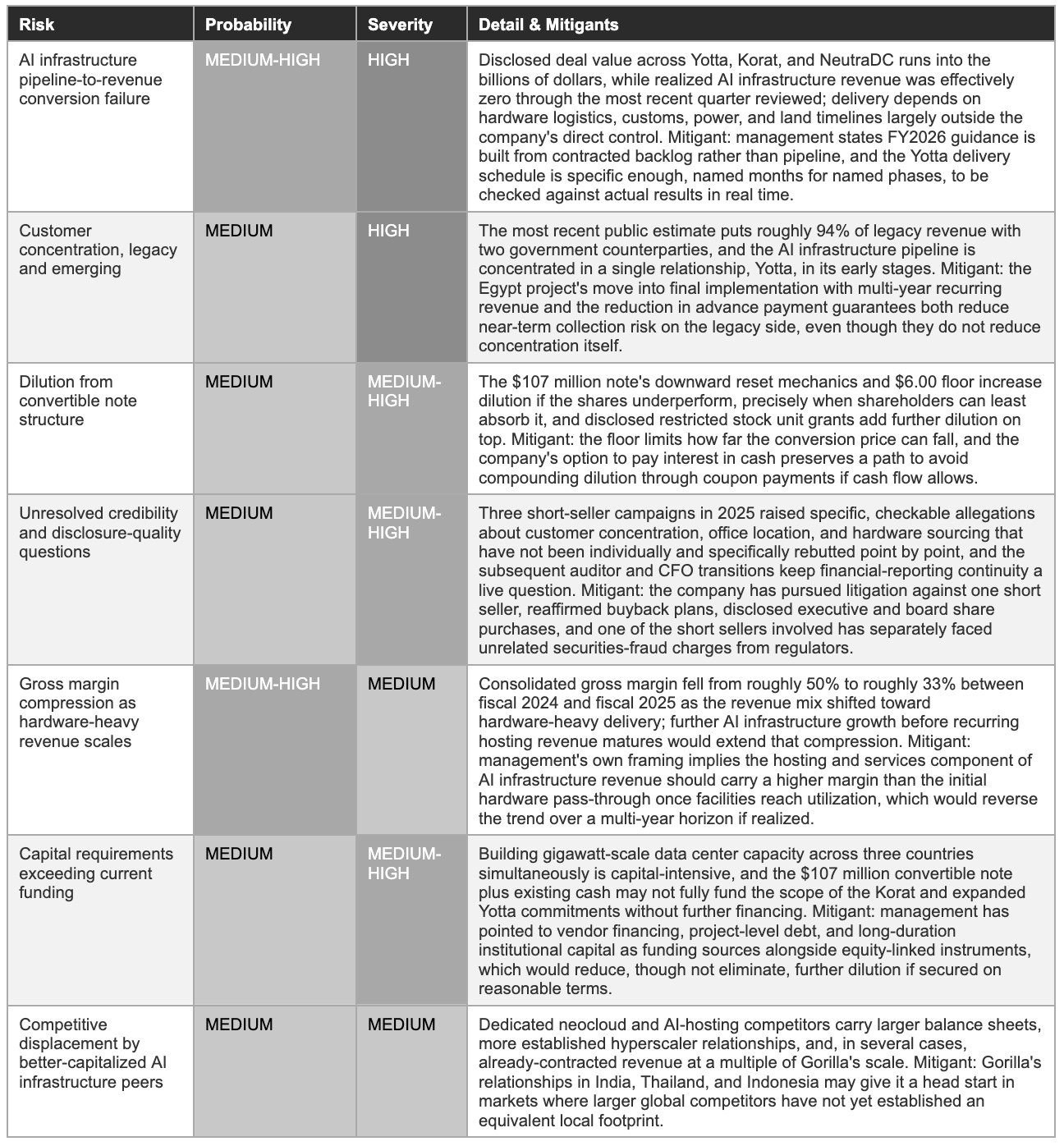

8. Risk Matrix

Each risk below is a variable whose resolution over the next twelve to twenty-four months will determine which of the scenarios in the forward financial model comes closest to realized. Probability reflects the likelihood of a materially negative outcome within that window; severity reflects the degree of lasting damage to the investment case if it occurs.

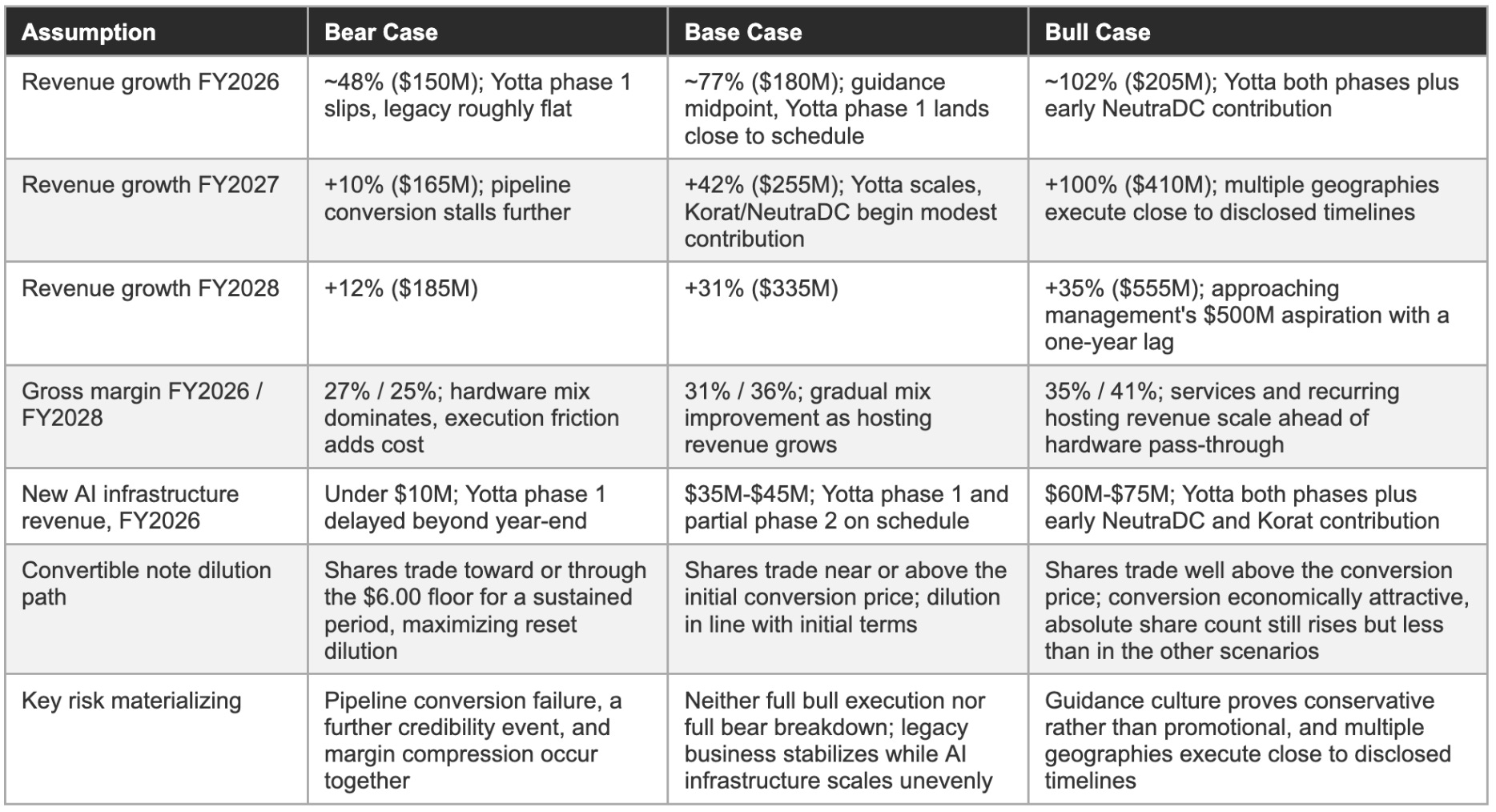

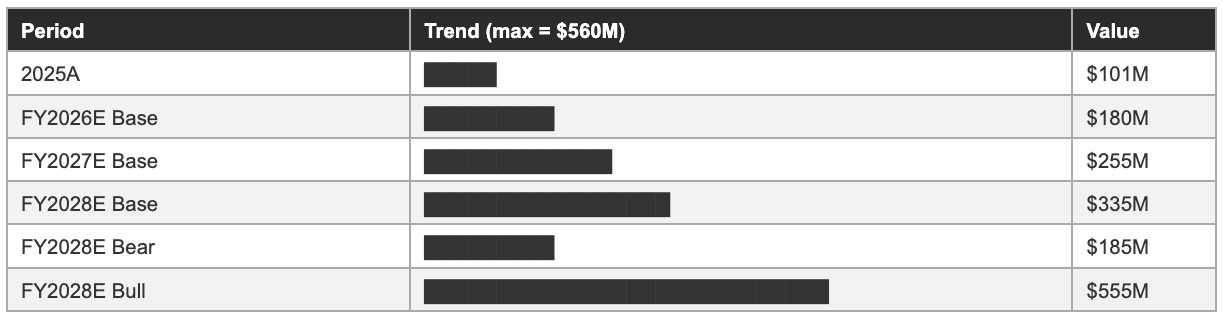

9. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios below start from management’s own FY2026 guidance range and diverge sharply by FY2028 based on a single underlying question: how much of the disclosed AI infrastructure deal value converts into recognized revenue, and at what margin, over the next three years.

Model assumptions

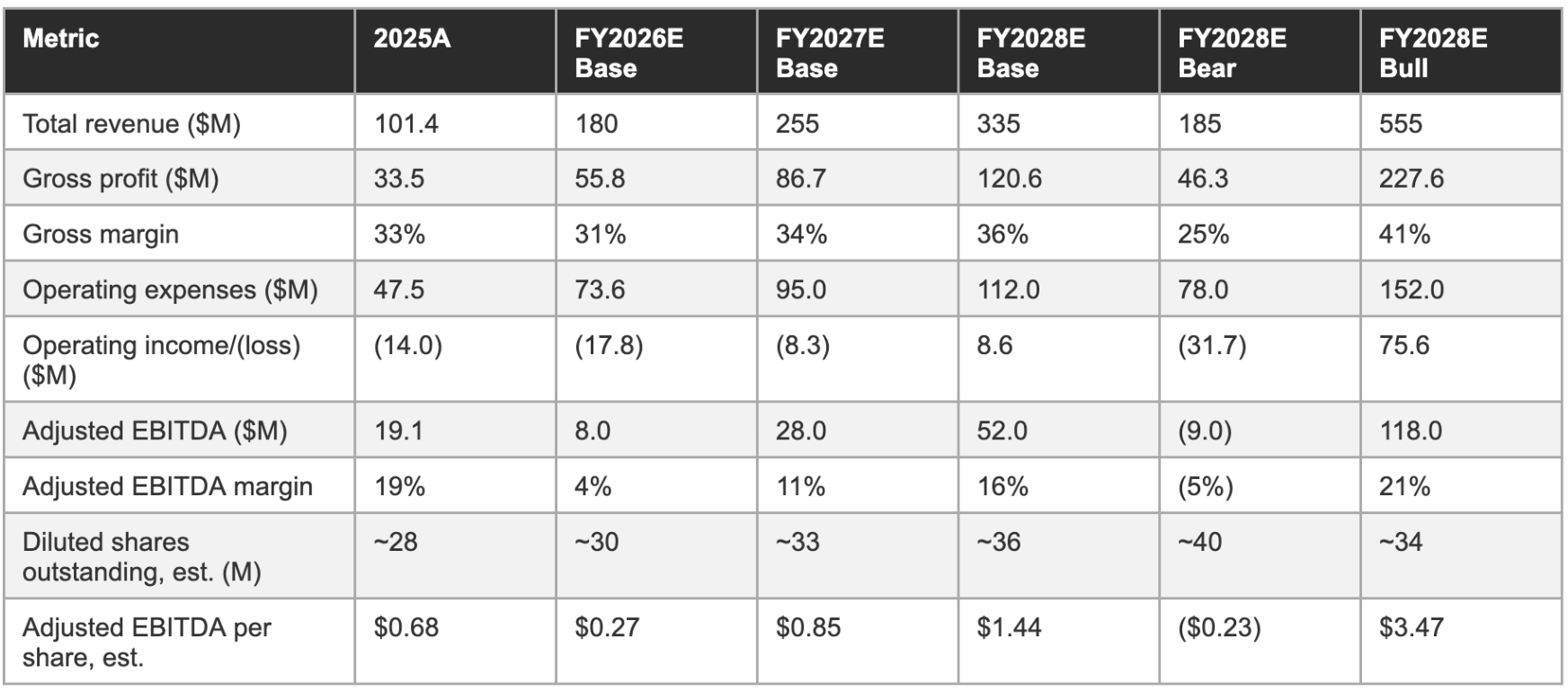

Three-year P&L projection

Convertible note dilution sensitivity

Revenue trajectory: Visual comparison

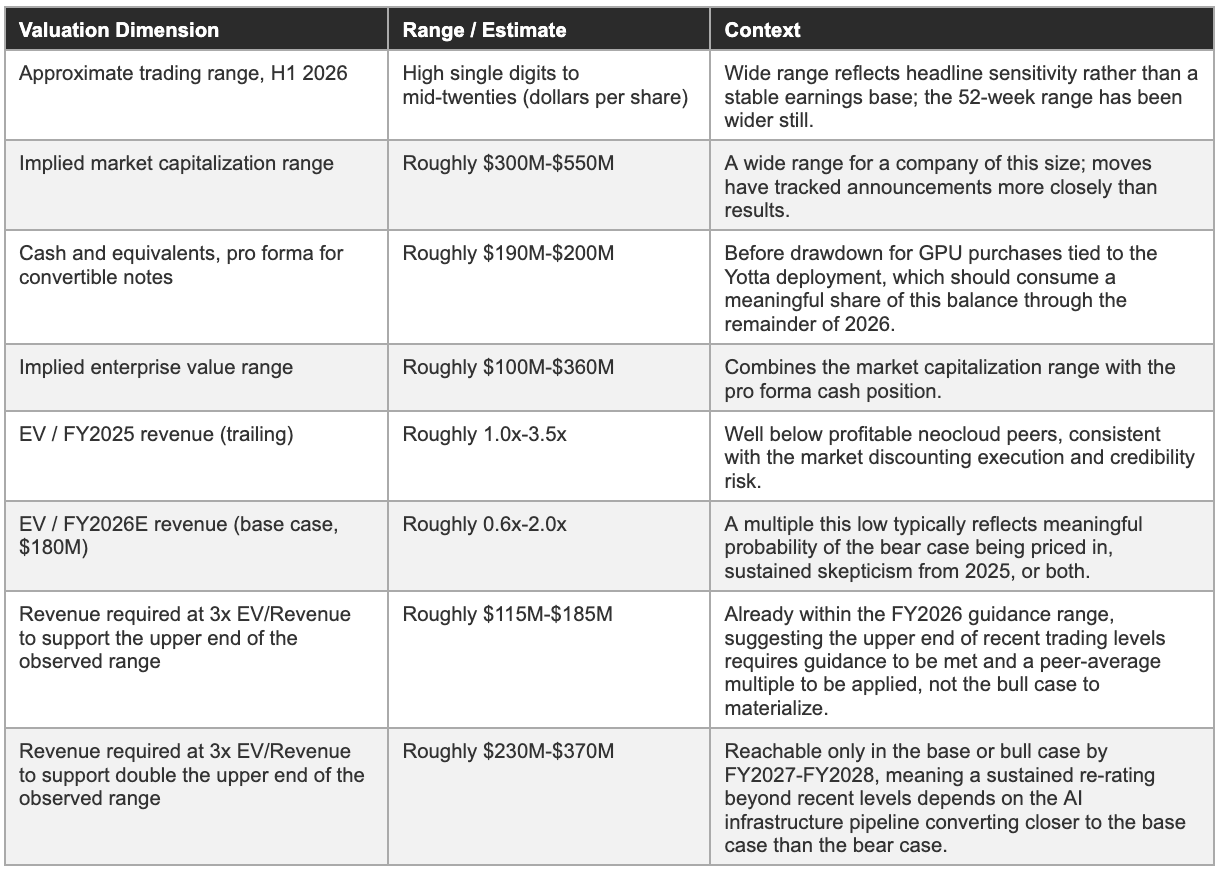

10. The Implied Valuation Question

Shares have moved on headlines as much as on financial results over the period covered by this report, which makes any single point-in-time valuation figure a poor anchor. The more useful exercise is to ask what revenue and margin combination the recent range of trading levels actually requires, and to check that requirement against the scenarios built in the preceding section.

Shares have traded across a wide range through the first half of 2026, broadly between the high single digits and the mid-twenties on a dollar basis, implying a market capitalization range of roughly $300 million to $550 million across that period rather than a single stable figure. A range that wide for a company of this size reflects how sensitive the valuation has been to headline-driven sentiment, short-seller campaigns, AI infrastructure announcements, and the convertible note pricing, rather than to a stable, slowly evolving earnings base.

Cash and equivalents stood at $98.4 million at the end of the first quarter of 2026, before the $107 million convertible note closed; pro forma for that offering’s roughly $102 million of net proceeds, cash approached $190 million to $200 million ahead of any drawdown for GPU purchases tied to the Yotta deployment, a balance that should fall meaningfully over the second half of 2026 as capital expenditure ramps. Combining the market capitalization range above with this cash position implies an enterprise value range of roughly $100 million to $360 million, again wide enough that a single point estimate would understate the genuine uncertainty in how the market is pricing the business.

Against FY2025 revenue of $101.4 million, that enterprise value range implies a trailing multiple of roughly 1x to 3.5x revenue; against the FY2026 base case of $180 million, the forward multiple compresses to roughly 0.6x to 2.0x. Both figures sit well below the multiples that profitable, well-capitalized neocloud peers have commanded, and a multiple this low typically signals that the market is pricing meaningful probability of the bear case, continued skepticism following the 2025 short-seller campaigns, or both.

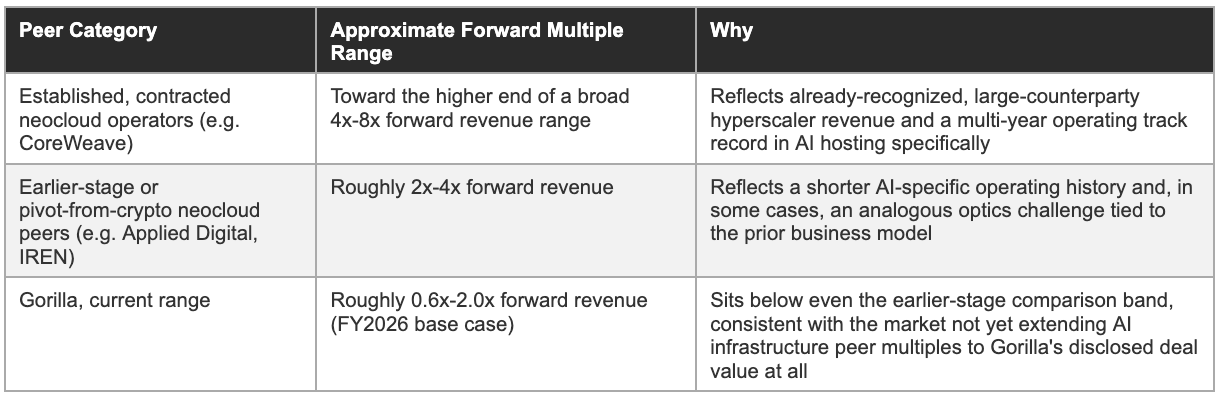

The peer set discussed in the competitive landscape section is a useful, if imperfect, cross-check. Established neocloud and AI infrastructure operators with contracted, already-recognized hyperscaler revenue have traded at multiples toward the higher end of a broad 4x to 8x forward revenue range, while earlier-stage, less-contracted, or optics-challenged peers in the same group have traded closer to 2x to 4x.

Gorilla’s current multiple sitting below even that lower, earlier-stage comparison band is consistent with a market that has not yet extended AI infrastructure peer multiples to Gorilla at all, treating the company’s disclosed deal value as largely unpriced until it shows up in recognized revenue. That gap is precisely what the bull case requires to close: not a re-rating to match CoreWeave or Nebius, but a re-rating to match the lower end of the range earlier-stage, similarly sized peers have achieved once their own contracted revenue became observable.

Peer multiple reference points

Valuation framework

If the Yotta relationship alone reaches the more than $500 million annualized revenue base management has described, and the broader business is valued at a discount to dedicated neocloud peers given Gorilla’s smaller scale and credibility overhang, perhaps 2x to 4x forward revenue rather than the 4x to 8x multiples better-capitalized peers have commanded, the implied valuation would represent a substantial increase from recent trading levels. The probability of that specific outcome, a single relationship reaching $500 million of annualized revenue inside roughly eighteen months of the agreements being signed, is the crux of the bull case.

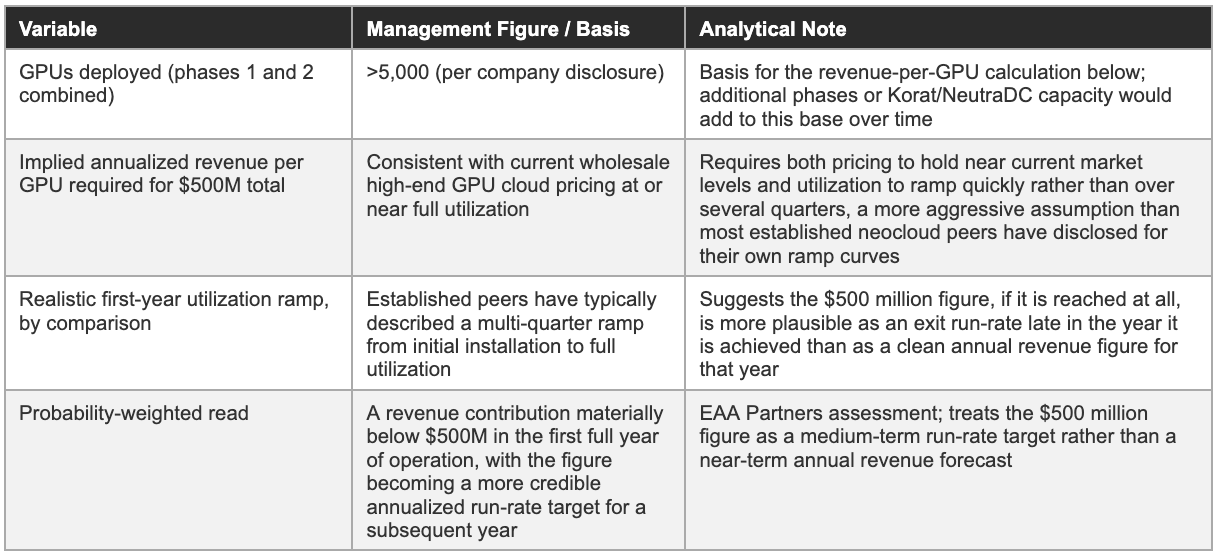

What the $500 million aspiration requires

Breaking management’s own $500 million figure down into its component assumptions is a useful discipline, since the number is repeated frequently enough in public commentary that it risks being treated as a target rather than as a calculation. A $500 million annualized run-rate from the Yotta relationship alone, at the blended per-GPU hosting economics implied by the disclosed hardware scope, more than 5,000 GPUs across the two announced phases, would require monthly hosting revenue per GPU in a range consistent with prevailing wholesale GPU cloud pricing for high-end Nvidia accelerators, multiplied by a utilization rate management has not separately disclosed.

At full utilization and pricing toward the higher end of the current market range, the GPU count disclosed for phase one and two combined could plausibly support an annualized revenue figure in the hundreds of millions of dollars, which is directionally consistent with management’s own figure. The two assumptions doing the most work, full utilization from the point of installation rather than a multi-quarter ramp, and pricing holding at current levels rather than compressing as GPU cloud capacity expands industry-wide, are both more optimistic than what most established neocloud operators have disclosed about their own ramp curves, where utilization typically builds over several quarters rather than reaching full capacity immediately upon hardware delivery.

Implied outcome table

11. Milestone Tracker: 2026-2028

The milestones below translate the analytical questions raised throughout this report into specific, observable proof points. The Yotta delivery and revenue milestones in the second half of 2026 are the two highest-stakes near-term observations; most of what follows in this report depends on how those two resolve.

12. Opinion & Investment Perspective: Bull, Base & Bear Cases

What follows is an attempt to give the bull and bear cases equal space and equal scrutiny. A story built this heavily on announced deal value deserves at least as much skepticism as enthusiasm, and a stock that has already moved sharply on headlines deserves a clear-eyed view of what would need to go right, and wrong, from here.

The bull case: Four pillars

The first pillar is real, observable improvement in the legacy business’s working capital profile. Operating cash flow turned positive in the first quarter of 2026, advance payment guarantees on major projects fell from the tens of millions of dollars to roughly $45,000, and the Egypt project moved into final implementation with five years of recurring revenue expected once that phase completes. None of this depends on the AI infrastructure pivot succeeding, which makes it a genuine, independent positive in the investment case rather than a story contingent on Yotta.

The second pillar is an early position in three large, underserved AI compute markets. India, Thailand, and Indonesia represent significant AI compute demand relative to current local supply, and Gorilla’s relationships with Yotta, NeutraDC, and Thai authorities give it a contracted or quasi-contracted position in those specific markets ahead of larger global neoclouds establishing comparable local footholds. Converting even a fraction of the disclosed deal value into revenue would represent substantial percentage growth off the company’s small existing base.

The third pillar is management’s stated discipline around guidance construction. The 2026 guidance raise was explicitly tied to contracted backlog rather than pipeline assumptions, and CFO commentary has repeatedly emphasized that framing. If that discipline holds through the Yotta delivery milestones in the second half of 2026, the gap between guidance and realized revenue should narrow rather than widen, a different pattern from the backlog and pipeline commentary discussed in the financial history section.

The fourth pillar is optionality across three separate geographies rather than dependence on one. Even though Yotta in India represents the overwhelming majority of disclosed AI infrastructure deal value today, the Korat campus in Thailand and the NeutraDC relationship in Indonesia give the company two additional, smaller-scale paths to AI infrastructure revenue that do not depend on the same counterparty, the same national customs regime, or the same power grid as the India deployment. A company with only the Yotta relationship would be a single-counterparty bet in the purest sense; a company executing reasonably well across two of its three disclosed AI infrastructure initiatives, even if the largest one slips, would still show a credible, diversifying growth path that the market has not yet given the company credit for.

The bear case: Four concerns

The first concern is an unresolved credibility deficit. Three short-seller campaigns, an auditor change, and a CFO transition combine into a pattern of disclosure-quality questions that have not been individually resolved. A single additional negative disclosure event, a further auditor change, a delayed annual filing, or a missed Yotta milestone, would land on a stock already trading substantially on faith in announced-but-unrealized deal value, with asymmetric downside.

The second concern is that the AI infrastructure pivot has layered a new concentration risk on top of the old one rather than replacing it. The legacy two-customer concentration, approximately 94% of revenue from Egypt and Taiwan’s Criminal Investigation Bureau, was a known, long-standing risk. The Yotta relationship in India introduces a different but comparably acute single-counterparty concentration on the AI infrastructure side, while adding execution risk, land, power, customs, hardware logistics, that a pure software and integration relationship did not carry.

The third concern is dilution embedded directly in the financing structure. The convertible note’s reset and floor mechanics, combined with the disclosed restricted stock unit grants, mean even a successful execution scenario delivers a meaningfully larger share count by FY2028 than exists today, and a less successful scenario, with the stock underperforming and triggering downward resets, compounds dilution at precisely the moment shareholders can least afford it.

The fourth concern is that management’s own attention and the company’s capital are being spread across more simultaneous initiatives than the current revenue base would typically support. Three AI infrastructure geographies, a minority stake in an AI startup, and a newly approved consumer finance acquisition are each individually defensible as opportunistic moves, but taken together they describe a management team pursuing breadth at a moment when the market’s primary question is whether the company can execute reliably on its single largest, most time-sensitive commitment, the Yotta delivery schedule in India. Execution risk tends to compound rather than average across simultaneous initiatives, and a company this size has a smaller margin for error managing five fronts at once than a larger, better-capitalized peer would.

The base case sits between these two narratives rather than averaging them. It assumes the legacy business continues its recent pattern of improved collection and modest, uneven growth, that the Yotta relationship delivers on a schedule running somewhat behind management’s stated timeline but well ahead of the bear case’s near-total slippage, and that the convertible note’s dilution lands closer to its initial terms than to its floor because the equity story, while unresolved, has not collapsed. Under that base case, the preliminary second-quarter 2026 revenue figure and the original Yotta delivery and revenue-recognition dates in the third and fourth quarters of 2026 are the specific events most likely to move the stock toward one narrative or the other before the next annual report is filed.

The combination of a real, cash-generating legacy business and a still-unproven AI infrastructure pipeline produces a wider range of plausible outcomes for Gorilla over a three-year horizon than for most companies of comparable size. The credibility questions raised over the past year mean that wide range should be treated as a feature of the investment case to underwrite explicitly, weighing the bull and bear pillars above on their own merits, rather than as a temporary overhang to wait out.

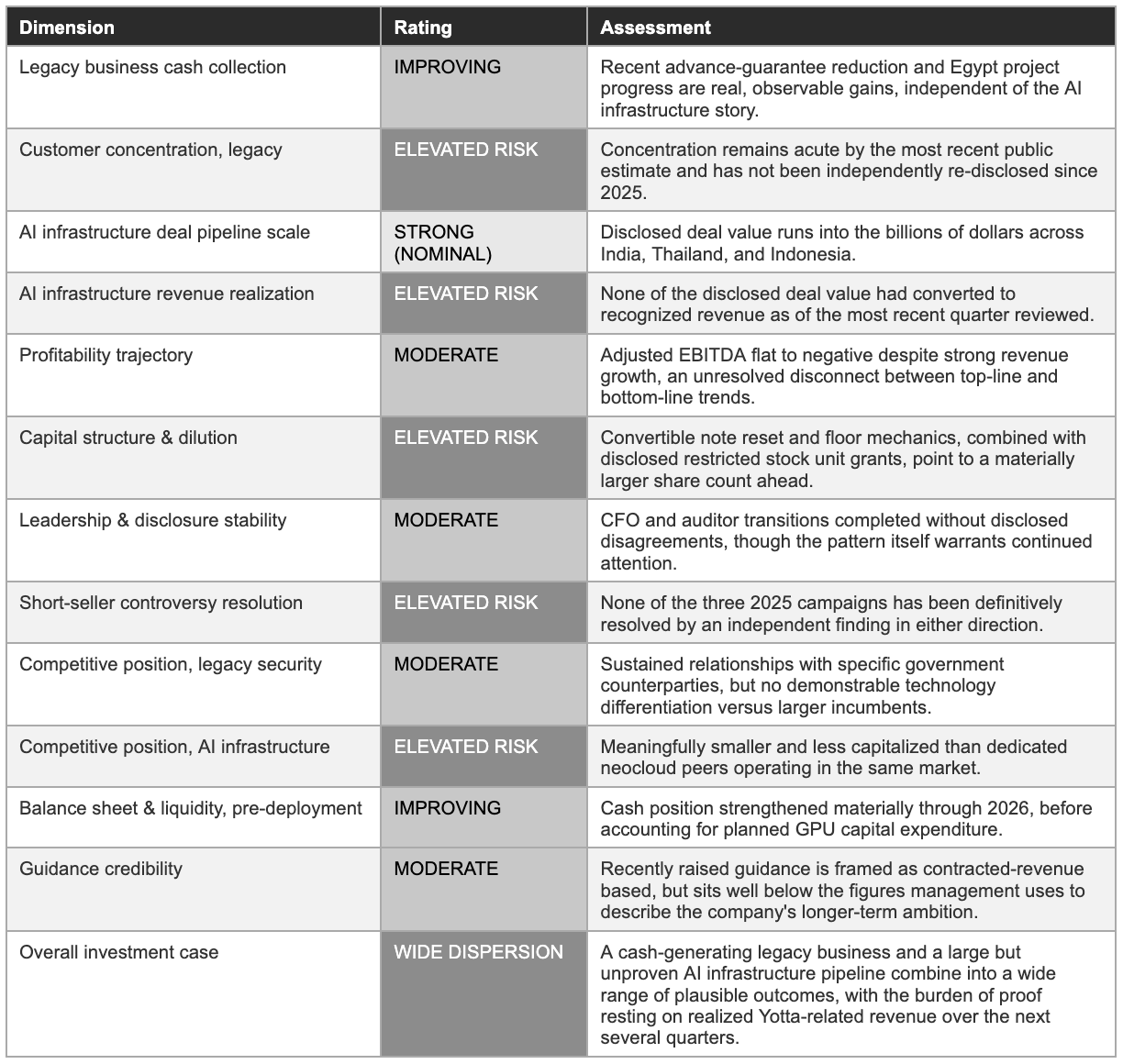

13. Investment Scorecard & The Bottom Line

The scorecard below distils the preceding twelve sections into a single reference frame. The dispersion across dimensions is unusually wide for a company of this size, real strength in cash collection and early market position sits next to real, unresolved questions about concentration, dilution, and disclosure, and that dispersion is itself the most important single conclusion of this report.

The bottom line

Gorilla in mid-2026 is two businesses at very different stages of proof. The legacy security and smart-city business has a long operating history, a recent improvement in cash collection, and a customer concentration problem that has not gone away. The AI infrastructure business has an enormous disclosed pipeline, a fast-growing headcount and capital commitment behind it, and effectively no realized revenue to show for it yet. The credibility questions raised by three separate short-seller campaigns in 2025 have not been individually resolved, and the financing structure chosen to fund the AI infrastructure build-out adds dilution risk on top of execution risk rather than instead of it.

None of this means the pivot will fail. The geographies Gorilla has targeted are large and underserved, the relationships it has signed are specific enough to be checked against a real calendar of delivery dates over the next two years, and the legacy business’s improved cash collection gives the company more room to absorb delays than its income statement alone would suggest. It does mean that the case for owning the stock today rests on a forecast rather than a result, and that the next several quarters of Yotta-related delivery and revenue data, not further announcements of additional billions of dollars in deal value, are what should move an investor’s view from here.

Sources

This analysis is based exclusively on publicly available information as of mid-2026. Primary sources include Gorilla Technology Group’s Q1 2026 results release and earnings call commentary, FY2025 annual report (Form 20-F), Form 6-K current reports covering the convertible note offering and auditor change, company press releases regarding the Yotta, Korat, NeutraDC, and Supermicro arrangements, and short-seller reports from The Bear Cave, Citron Research, and Culper Research together with the company’s public responses to each. Analyst price targets and consensus figures referenced are drawn from third-party financial data aggregators. All specific figures are sourced to these materials unless explicitly identified as an own estimate.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Gorilla Technology Group Inc. (NASDAQ: GRRR) or any other security. All information is sourced from publicly available materials believed to be reliable as of July, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.