INFLEQTION, INC.

Neutral-Atom Quantum: The Full-Stack Platform Bet, The Sensing Bridge, and Whether a $550M Cash Cushion Can Buy Enough Runway for Computing Revenue to Arrive Before the Market Loses Patience

1. Corporate Profile & The Between-Measurement Platform Thesis

Infleqtion is a full-stack quantum technology company generating real government revenue from deployed sensing and timing hardware today, while building toward fault-tolerant quantum computing advantage on a publicly committed roadmap. The investment question is whether the $550M cash cushion raised through the February 2026 SPAC listing is sufficient runway for computing revenues to scale before the market discounts the duration risk entirely.

Infleqtion designs and builds quantum computers, precision sensors, and quantum software for governments, enterprises, and research institutions. The founding science, the ability to cool individual atoms to temperatures a fraction above absolute zero and trap them with laser light, is the physical substrate on which every product Infleqtion has ever built rests.

The platform thesis rests on a specific claim about neutral atoms: that they are, in management’s phrase, nature’s ideal qubit. Unlike superconducting qubits, which require cooling to temperatures near absolute zero and are manufactured on chips with fixed connectivity, neutral atoms are identical in nature and can be arranged and rearranged in real time by laser fields.

This reconfigurability, combined with room-temperature trapping chambers and native all-to-all qubit connectivity, gives neutral-atom platforms theoretical scalability advantages that the company argues will compound as qubit counts grow. The same physics that produces high-fidelity quantum computing also produces the precise timekeeping and radio-frequency sensing capabilities that currently account for approximately 75% of Infleqtion’s revenue.

This dual-market structure distinguishes Infleqtion from every other publicly traded quantum pure-play. IonQ, Rigetti, D-Wave, and Quantum Computing Inc. each derive substantially all revenue from computing-adjacent activities, cloud access fees, professional services, or quantum annealing. Infleqtion derives the majority of its revenue from deployed sensing and timing hardware, primarily under national security contracts with the US Department of Defense, DARPA, NASA, and allied government agencies. That revenue base exists today, at scale sufficient to sustain operations at a modest but accelerating clip, and is financed separately from the computing roadmap.

The central tension in the investment case is temporal. Sensing revenue is real and growing but small relative to a market capitalisation implying a large computing premium. Computing revenue is near zero today but is the basis for the valuation multiple the company carries. Management’s stated position, that sensing and timing provide the revenue bridge while the computing roadmap matures, is strategically coherent, but it requires investors to hold duration risk across a 2026-2030 commercialisation window during which capital markets may reprice the sector multiple several times.

2. The Neutral-Atom Platform: Physics, Products & Technology Readiness

The neutral-atom modality offers room-temperature operation, native qubit reconfigurability, and all-to-all connectivity, properties that translate directly into scalability and cost advantages at high qubit counts. Infleqtion’s product portfolio spans four hardware categories and two software platforms, all built on the same underlying physics, which produces both technical synergies and concentrated technology risk if neutral atoms fail to scale as projected.

Why neutral atoms

The qubit modality question, which physical system provides the best path to fault-tolerant quantum computing, is the most consequential open debate in the industry. The four dominant approaches in commercial use are: superconducting qubits (IBM, Google, Rigetti), trapped ions (IonQ, Quantinuum), photonic qubits (PsiQuantum), and neutral atoms (Infleqtion, QuEra, Pasqal). Each modality has distinct tradeoffs across fidelity, coherence time, scalability, and cost of operation.

Superconducting qubits operate at millikelvin temperatures requiring expensive dilution refrigerators, and their connectivity is fixed by chip topology. Trapped-ion systems achieve very high gate fidelities and long coherence times but face scalability challenges as the number of ions in a trap increases, because motional coupling becomes more complex. Photonic systems offer room-temperature operation and high-speed gates but require deterministic photon-photon interactions that have proven technically difficult to engineer at scale.

Neutral atoms offer a different tradeoff profile. Individual atoms of elements such as rubidium or caesium are cooled by lasers to microkelvin temperatures and suspended in configurable arrays by optical tweezers or holographic traps. Because every neutral atom of a given element is physically identical, neutral-atom qubits are intrinsically uniform, eliminating the fabrication variability that afflicts superconducting chip production. The trapping chamber itself operates at or near room temperature, removing the refrigeration infrastructure cost. And because atoms can be physically rearranged within the trap by reconfiguring the optical tweezer array, neutral-atom systems support all-to-all connectivity rather than being constrained to nearest-neighbour gates as in fixed-topology architectures.

The primary vulnerability of neutral atoms has historically been gate speed: Rydberg-based two-qubit gates, while achieving high fidelity, operate on microsecond timescales that are slower than superconducting gates. Infleqtion’s most recent disclosure, a 99.73% two-qubit controlled-Z gate fidelity on the Sqale platform, addresses the fidelity dimension specifically. Gate fidelity matters more than gate speed in the fault-tolerance race because higher fidelity reduces the number of physical qubits required per logical qubit, the ratio that determines when fault-tolerant computing becomes economically viable.

Product portfolio

Infleqtion’s commercial product portfolio spans four hardware categories and two software layers. The hardware products are organised around the sensing-timing-computing continuum.

Sqale is the company’s flagship quantum computing platform. As of March 2026, Infleqtion delivered the UK’s only operational 100-physical-qubit quantum computing system to the National Quantum Computing Centre at Oxford, making Sqale the first neutral-atom platform of that scale deployed in a national facility. The Sqale system achieved 12 logical qubits in FY2025, ahead of the original roadmap, and management has committed to 30 logical qubits by end-2026 and 100 by 2028. The 100 logical qubit threshold is management’s stated estimate for the point at which quantum computing begins to address transformative applications in materials science, drug discovery, and cryptography.

Tiqker is the company’s quantum optical clock product, designed for precision timekeeping in GPS-denied and contested environments. Atomic clocks are among the most commercially mature quantum technologies, with established procurement channels across defence, telecommunications, and financial services. Tiqker positions Infleqtion in the precision timing market with a platform that is already generating revenue under government contracts, with a commercial partnership announced with Safran for precision timing applications.

Sqywire is a quantum radio-frequency receiver that exploits the sensitivity of Rydberg atoms to external electric fields. The product is capable of receiving RF signals without emitting, a capability with immediate national security applications in passive signals intelligence and communications monitoring. Traditional radar and RF systems must emit signals to detect their environment, making them detectable. A passive quantum RF receiver changes that equation. Sqywire is currently sold primarily under government research and development contracts.

The inertial navigation product line, marketed under the Exaqt brand, targets GPS-denied navigation for aerospace, submarine, and autonomous vehicle applications. Quantum inertial sensors exploit atom interferometry, the quantum wave nature of atoms, to measure acceleration and rotation with precision exceeding classical systems by orders of magnitude. The addressable market includes military platforms that cannot rely on GPS in contested or denied environments, as well as space vehicles where GPS signals are unavailable.

On the software side, Superstaq is the company’s quantum computing control and optimisation platform. It functions as a compiler and middleware layer that enables quantum circuits written once to be deployed across multiple hardware backends, NVIDIA CUDA-Q, IBM Quantum, and Infleqtion’s own Sqale QPU, maximising hardware utilisation and enabling hybrid quantum-classical workflows. Superstaq’s write-once, target-all architecture gives it relevance beyond Infleqtion’s own hardware, making it a potential revenue source in cloud-based quantum access markets regardless of which hardware modality wins the long-term technology race.

CML (Classical Machine Learning enhancement) software is built on quantum physics principles and is designed to amplify AI performance on classical GPU hardware today, without requiring a quantum computer. The product targets data centres and AI infrastructure operators who want performance improvements available immediately. CML is an early-stage commercial product; its revenue contribution to FY2025 results is not separately disclosed.

Technology readiness

Infleqtion’s products span a wide range of technology readiness levels that investors must disaggregate. The sensing and timing products are deployed hardware generating contracted revenue. They are not laboratory prototypes. The Sqale quantum computing platform, at 100 physical qubits and 12 logical qubits, is in the transition zone between research-grade and early-commercial hardware. It is operational in a national facility but has not yet demonstrated the logical qubit count at which commercial advantage over classical computing becomes routine. The 100-logical-qubit milestone targeted for 2028 is the threshold management identifies as transformative; the gap between today’s 12 and tomorrow’s 100 represents the primary technology execution risk in the investment case.

Management’s comparison of Infleqtion’s strategy to NVIDIA’s early approach is instructive. NVIDIA’s GPU was originally marketed for graphics before the CUDA software stack revealed its broader applicability to scientific computing and, eventually, AI training. Infleqtion is pointing its neutral-atom platform at near-term sensing and timing markets while building the computing roadmap toward applications that do not yet exist commercially. The analogy is apt in structure; whether it holds in outcome depends on whether the neutral-atom modality achieves commercial advantage before competing hardware approaches do.

3. Business Model Architecture: Contract Economics & the Path to Commercial Revenue

Infleqtion’s current revenue model is government-contract funded hardware and software development, a fundamentally different economic structure from recurring subscription software. Gross margins are contract-specific and project-dependent rather than predictable at a platform level. The transition from government-funded development to commercially priced product licensing is the most consequential business model event in the company’s forward history, and it has not yet occurred at meaningful scale.

Revenue structure today

Infleqtion generates revenue through three primary mechanisms. Development contracts, under which government agencies fund the development of specific quantum capabilities, are the largest revenue category. The company receives milestone-gated payments upon delivery of defined technical outputs. These contracts include cost-plus and fixed-price structures common in defence procurement, and they are governed by the Federal Acquisition Regulation framework, which imposes compliance overhead but also provides contractual revenue certainty for the duration of each award.

Product sales of deployed sensing and timing hardware, including Tiqker clock systems, Sqywire RF receivers, and inertial navigation components, constitute the second revenue category. These are one-time capital sales with the associated gross margin variability of hardware businesses. Management has stated that the long-term gross margin target for the sensing product line is price parity with classical alternatives on a performance-adjusted basis, implying continued margin pressure in the near term as quantum sensing hardware remains at low production volumes.

Software and cloud access fees, primarily through the Superstaq platform, are the third and smallest revenue category. Superstaq’s cloud quantum access business is early-stage; the revenue contribution in FY2025 is not separately disclosed. The long-term gross margin target for the software business, management has referenced semiconductor-comparable margins as the eventual target, is meaningfully higher than the hardware lines, making software mix shift the primary lever for gross margin expansion over time.

The revenue bridge thesis

Management’s stated commercialisation sequence is explicit: sensing and timing revenue provides the economic bridge that finances the computing roadmap without requiring the company to return to capital markets for operational funding. The logic depends on two things holding simultaneously. First, sensing contract wins must continue to grow at a rate sufficient to offset operating cash burn, or at minimum to reduce the net cash consumption below the pace that would exhaust the $550M treasury before computing revenues arrive. Second, the computing roadmap must deliver logical qubit milestones on schedule, because each delay extends the duration risk that the market must price.

CEO Matthew Kinsella’s stated revenue mix trajectory, approximately 75% sensing in FY2025 bookings moving toward 50/50 sensing-computing as large computing contracts are won, then shifting rapidly toward computing once commercial advantage is demonstrated, provides the framework for forward revenue modelling. The bookings mix moving toward 50/50 in FY2025 is significant because bookings lead revenue by the duration of contract delivery cycles, typically 12 to 36 months for government R&D contracts. A 50/50 bookings split in FY2025 implies that computing-related revenue could represent a materially larger share of total revenue by FY2027 than the current 25% share suggests.

Unit economics of government contracts

Government quantum technology contracts carry economics that differ from both software subscriptions and commercial hardware sales. Cost-plus contracts reimburse allowable development costs plus a defined fee, providing revenue but limited gross margin expansion potential. Fixed-price development contracts transfer cost overrun risk to Infleqtion but allow for higher margins if work is executed below the fixed price. The company’s improving operating loss trajectory, from $(53M) in FY2024 to $(35.3M) in FY2025, reflects both revenue growth and cost discipline rather than unit economics improvement of the kind that characterises software businesses.

The long-term economic transformation of the model requires transition from single-use government development contracts to repeating product sales or cloud access subscriptions that carry higher gross margins and lower incremental cost to serve. That transition is beginning at the sensing layer but has not yet occurred at the computing layer, where Sqale access today is primarily provided under research and development arrangements rather than commercial pricing.

The gross margin profile of the business as it exists today is not separately disclosed by product line in available public filings. The company has targeted semiconductor-comparable gross margins as its long-term aspiration, which in the semiconductor industry context implies 50-65% on hardware and 70%+ on software. The current blended gross margin, implied from available revenue and cost of revenue figures, we estimated to be at 20-35%, consistent with a hardware development business at early production volumes. The path to semiconductor-comparable margins requires both scale and mix shift toward software and cloud access.

4. Capital Position & Dilution Overhang

The February 2026 SPAC transaction delivered a $550M+ cash balance that eliminates near-term funding risk, but it also created a complex capital structure with 10.4M exercisable warrants, 121.8M shares registered for resale by selling security holders, and a $1.11B shelf registration filed in late April 2026. Each of these elements represents real or potential dilution that investors must price explicitly.

Capital position

The combined effect of the SPAC trust, the PIPE financing, and Legacy Infleqtion’s existing cash resulted in a pro forma cash balance exceeding $550M against zero debt, as disclosed on the Q4 2025 earnings call. At a FY2025 operating cash burn of approximately $24M, the current treasury theoretically provides more than twenty years of runway at the pre-public burn rate, a figure management has cited as evidence of the company’s capital adequacy.

The more relevant comparison is the expected post-public burn rate, which will be higher due to increased compliance, personnel, and commercialisation investment. At a normalised post-public burn of $35-45M per year, which we estimate as a reasonable base case given the $40M revenue base and guided operating cost structure, the cash position still provides 12-16 years of runway.

The practical significance of the cash position extends beyond solvency assurance. Enterprise procurement of quantum technology, whether by government agencies or commercial customers, increasingly involves counterparty financial due diligence, because buyers of quantum systems must commit to multi-year integration and operation relationships. A vendor with $550M in cash and zero debt occupies a distinctly different risk category for procurement committees than a vendor burning capital toward a funding deadline. This financial credibility is a competitive asset in enterprise sales conversations that the balance sheet alone cannot fully capture.

Dilution overhang

The capital position is the good news. The dilution structure is more complex and requires explicit investor attention. Four categories of dilution overhang exist.

First, 10,350,000 public warrants and 75,000 private warrants are exercisable for common stock at $11.50 per share. These warrants were issued in connection with Churchill Capital’s own IPO and converted into Infleqtion warrants at the SPAC closing. If all warrants are exercised for cash, the company receives approximately $119.9M in additional proceeds, which is economically positive, but existing shareholders experience dilution of approximately 4.8%. Given the current trading range of $11-17 per share, warrant exercise is economically rational for holders when the share price exceeds $11.50, which encompasses much of the trading range since listing.

Second, 121,829,432 shares of common stock were registered for resale by selling securityholders pursuant to the S-1 filed in March 2026. These shares include the PIPE shares (12.7M), Founder Shares held by the Churchill Sponsor (10.4M), Legacy Infleqtion holder shares registered for resale (98.4M), and other categories. The registration itself does not trigger selling, but it removes the lockup and regulatory barrier to selling for a population of shareholders whose shares were originally issued at or below $10.00. Shareholders who received shares in the PIPE at $10.00 hold near-money shares relative to current trading prices; Legacy Infleqtion holders whose shares were issued in the merger at the deal’s implied valuation may hold shares at a significantly higher average cost, reducing near-term selling incentive for that cohort.

Third, the company filed a $1.11 billion shelf registration for common stock in April 2026, described publicly as related to an employee stock ownership programme. The shelf provides financial flexibility and signals that management is thinking about equity-based compensation at a scale consistent with the company’s market capitalisation. The filing itself is not indicative of an imminent public offering.

Fourth, 31,059,533 options and restricted stock units outstanding as of closing represent additional potential dilution from employee compensation. At a weighted exercise price below current trading prices for a portion of this pool, option exercise dilution will accrue over the vesting horizon.

The net dilution picture, taken in total, is manageable but not trivial. Investors purchasing shares at current prices are buying into a capital structure where up to 10.4M warrant shares, plus options and RSUs over 31M shares, represent future dilution that is partially offset by the cash proceeds received upon warrant exercise. The selling securityholder overhang is the component most likely to create near-term price pressure if holders seek liquidity.

5. Government Relationships & National Security: The Revenue Foundation

Approximately 70% of Infleqtion’s FY2025 revenue came from US government sources, with national security applications as the primary use cases. The government customer base is real, growing, and provides the revenue bridge that management describes as financing the computing roadmap. The concentration risk is equally real: a shift in defence budget priorities or a programme cancellation could materially impair near-term revenue without advance warning.

Customer base and contract history

Infleqtion’s government customer base spans the full spectrum of US national security agencies and allied government entities. The US Department of Defense is the largest single customer category. DARPA has funded multiple Infleqtion programmes including, most recently, the April 2026 HARQ award of $2M to develop Multistaq, a heterogeneous quantum software platform.

The Department of Energy’s ARPA-E awarded $6.2M in March 2025 for quantum-enhanced energy grid optimisation. NASA awarded $17M in September 2025 for space-based quantum sensing. The US Army awarded $2M in December 2025 for secured AI positioning at the edge. The UK government, through the National Quantum Computing Centre, contracted the delivery of the Sqale 100-physical-qubit system deployed in March 2026.

The customer relationship with In-Q-Tel, the venture capital arm of the US intelligence community, is a structural indicator of government confidence in Infleqtion’s technology. In-Q-Tel invests in technologies that address critical intelligence community needs; its investment in Infleqtion predates the public listing and signals that the technology has cleared the classified assessment process that the intelligence community applies to dual-use quantum technologies.

The disclosed customer list, which in public materials includes NASA, DARPA, SAIC, Lockheed Martin, and the Department of War across named relationships, represents a procurement network that took nearly two decades to build and that cannot be replicated quickly by a new entrant. Each government quantum contract requires security clearance processes, compliance certification, and programme review cycles that extend well beyond commercial procurement timelines. The barriers to entry in the government quantum channel are institutional and time-based rather than purely technological.

National security applications

The specific applications Infleqtion addresses in the national security market have immediate, near-term relevance that differentiates them from speculative future computing applications. GPS-denied navigation is an operational requirement that the US military is actively procuring solutions for, given the demonstrated ability of adversaries to jam or spoof GPS signals in contested environments. Infleqtion’s quantum inertial sensors based on atom interferometry provide navigation accuracy that degrades much more slowly than classical inertial systems during GPS denial, making them operationally superior in exactly the environments that current and near-future conflicts are expected to feature.

Quantum RF sensing addresses a related national security priority. Electronic warfare and signals intelligence operations increasingly depend on detecting adversary communications without revealing the presence or location of the detector. A passive quantum RF receiver that can detect signals without emitting provides a structural stealth advantage in signals intelligence operations. This capability is not a future aspiration; it is the basis for existing development contracts.

Precision timing for critical national infrastructure is the third near-term national security application. GPS-based timing signals, on which much of modern infrastructure depends, are vulnerable to jamming and spoofing attacks. Quantum optical clocks of the Tiqker type provide timing accuracy and holdover characteristics that would allow critical infrastructure to maintain synchronisation through GPS disruption events. The addressable market for infrastructure-grade quantum clocks extends from defence to utilities, financial exchanges, and telecommunications carriers.

Government funding concentration risk

The concentration of revenue in government customers is both the business’s current strength and its most acute operating risk. US defence budgets are subject to continuing resolution cycles, programme priority shifts, and, most recently, the structural uncertainty introduced by the Department of Government Efficiency’s review of federal spending. A significant reduction in quantum technology R&D funding would create immediate revenue pressure that the $550M cash balance could absorb but that would impair the bridge revenue thesis.

The FY2026 guidance of $40M is not publicly broken down by contract category, but given the FY2025 mix of approximately 70% US government revenue, any material disruption to government contract activity would put the guided trajectory at risk. The government contract pipeline that management has referenced as exceeding $300M is a useful indicator of demand health, but pipeline figures represent pursued opportunities rather than awarded contracts, and conversion rates in government procurement are inherently uncertain.

The mitigation to concentration risk is the diversification trajectory that the bookings mix data already suggests. The shift from 75% sensing (predominantly government) toward a 50% computing bookings share implies that computing contracts, which include both government-sponsored research (DARPA, DOE) and emerging commercial relationships (NVIDIA, JPMorgan, the Illinois Quantum and Microelectronics Park), are growing as a share of new business. If that mix shift continues, the effective government revenue concentration will decrease over time even if the absolute government revenue figure grows.

6. The Computing Roadmap: Logical Qubit Milestones & the 2028 Promise

Management has committed to a specific, publicly observable logical qubit roadmap with quarterly checkpoints: 30 logical qubits by end-2026, 100 by 2028, and 1,000+ by 2030. Execution ahead of the original schedule on the first two milestones, 2 logical qubits in 2024 and 12 in 2025, provides credibility for the near-term target. The gap between 12 and 100 logical qubits is where the commercial computing thesis is won or lost.

The logical qubit roadmap

Logical qubits are the fault-tolerant computational units that quantum error correction produces from multiple physical qubits. The ratio of physical qubits required to produce one reliable logical qubit is the primary determinant of when practical quantum computing becomes possible. At today’s error rates, superconducting systems typically require hundreds to thousands of physical qubits per logical qubit. Infleqtion’s 99.73% two-qubit gate fidelity implies a lower overhead ratio than lower-fidelity systems, meaning fewer physical qubits are needed to achieve the same number of reliable logical qubits.

At 12 logical qubits from a 1,600-physical-qubit array, Infleqtion’s current overhead ratio is approximately 133:1, a figure that will need to improve substantially to reach 100 logical qubits from the planned physical qubit count of roughly 40,000 (the Sqorpius architecture target).

The FY2025 delivery of 12 logical qubits was achieved ahead of the original 2025 schedule, which is the strongest single data point supporting the credibility of the FY2026 and FY2028 targets. The milestone was independently validated by academic publications, including joint work with NVIDIA demonstrating the world’s first materials science application using logical qubits. In September 2025, Infleqtion demonstrated a logical architecture uniting motion and in-place entanglement, and executed the world’s first quantum decryption using logical qubits, technical achievements with direct commercial relevance in the cryptography sector.

Architecture evolution

In October 2025, Infleqtion disclosed a new architecture underpinning the next-generation Sqale system, designated Sqorpius, that targets 1,000+ logical qubits by 2030 using up to 40,000 physical qubits. The architecture combines individual qubit addressing, which Infleqtion pioneered, with dynamically reconfigurable atom arrays and a new optical tweezer control system. The company is incorporating chip-scale photonics into future systems which would dramatically reduce the size, weight, and cost of each quantum processor unit, enabling deployment outside laboratory settings and in data centre environments.

The chip-scale photonics programme is a research-stage activity. Its success is a prerequisite for the 1,000-logical-qubit target at affordable cost, because building 40,000 physical qubits using current table-scale laser infrastructure would produce a system too large and expensive for commercial data centre deployment. The photonics integration work is technically ambitious; comparable photonic integration programmes at other quantum companies have encountered multi-year delays. Investors should treat the 2030 target as indicative rather than contractually committed.

Illinois quantum and Microelectronics Park

The planned deployment of a 50+ logical qubit system at the Illinois Quantum and Microelectronics Park represents the most concrete near-term computing deployment milestone with commercial implications. The Illinois facility, co-developed with state and federal support, positions Infleqtion’s Sqale system alongside NVIDIA’s planned HPC infrastructure in a hybrid quantum-classical computing environment.

If executed, this deployment would produce the first commercially accessible Infleqtion quantum computing resource in a dedicated facility designed for enterprise and government users, distinct from the research-access model of the NQCC deployment. Revenue from this arrangement is not embedded in the FY2026 guidance.

CUDA-Q and the hybrid workflow opportunity

NVIDIA’s CUDA-Q platform for hybrid quantum-classical computing, and the NVQLink interface that Infleqtion demonstrated at GTC 2026, represent the near-term commercial computing revenue pathway. Under the NVQLink architecture, Infleqtion’s Sqale QPU connects directly to NVIDIA GPU clusters with ultra-low latency, enabling real-time quantum error correction handled by GPU compute and hybrid quantum-classical algorithm execution where each component handles the problem structure it is best suited for.

If this architecture is adopted by NVIDIA’s enterprise data centre customers, Sqale QPU access would become a line item in data centre procurement budgets rather than a separate government research programme. That transition is the inflection point for computing revenue at material scale.

7. Strategic Partnerships: NVIDIA, JPMorgan & the Commercial Ecosystem

Infleqtion’s partnership network with NVIDIA, JPMorgan, SAIC, and Lockheed Martin serves two distinct commercial functions: hardware-software integration that expands the addressable market for Sqale beyond government research, and enterprise use-case validation that allows the company to demonstrate quantum value in finance, energy, and defence applications before fault-tolerant computing is achievable. The partnerships are genuine but should be assessed against the absence of disclosed commercial revenue contribution from any of them in FY2025.

NVIDIA

The NVIDIA partnership is the most commercially significant in Infleqtion’s portfolio. Infleqtion and NVIDIA have co-published the world’s first demonstration of a materials science application using logical qubits, peer-reviewed work that appeared in the academic literature and establishes the scientific credibility of the collaboration. At NVIDIA GTC 2026, the two companies demonstrated Sqale QPU integration with NVIDIA’s HPC environment through NVQLink, a native quantum-classical interconnect that NVIDIA is building into its accelerated computing platform.

The commercial logic for NVIDIA is clear: as quantum computing matures, NVIDIA wants to be the classical computing layer that runs alongside quantum processors, the same position it occupies in AI relative to CPU compute. Infleqtion’s neutral-atom architecture, with its room-temperature operation and real-time error correction requirements, is a natural fit for GPU-accelerated error correction, because the classical compute needed to implement quantum error correction in real time is substantial and GPU-parallel in structure. Infleqtion is currently the only neutral-atom company featured in an NVIDIA booth at GTC, a selection that reflects technical partnership depth beyond a marketing relationship.

The absence of disclosed commercial revenue from the NVIDIA partnership in FY2025 is the relevant constraint on the bullishness that the partnership warrants. NVIDIA has not committed to a commercial QPU procurement, and NVIDIA’s investments in multiple quantum modalities simultaneously indicate that it is hedging across approaches rather than endorsing Infleqtion exclusively. The NVIDIA relationship is an enabling partnership, not a revenue commitment.

JPMorgan Chase

The JPMorgan collaboration, which produced an open-source quantum error correction library in May 2025 that reduces physical qubit requirements by an estimated 10-100x for certain circuit classes, is a technical validation of Infleqtion’s computing approach from one of the world’s most sophisticated quantum computing enterprise users. JPMorgan has an active quantum computing research programme that evaluates hardware for financial modelling, portfolio optimisation, and risk calculation applications. The publication of a jointly developed error correction library signals that the collaboration has progressed beyond early-stage evaluation into active algorithm development.

Financial services is one of the most credible near-term commercial markets for quantum computing, because the computational problems in options pricing, credit risk modelling, and portfolio optimisation have well-defined quantum algorithmic approaches that are already theoretically superior to classical methods at problem sizes reachable with fault-tolerant hardware. JPMorgan’s active engagement with Infleqtion’s hardware gives the company early access to the enterprise use cases that would anchor the first wave of commercial computing contracts.

SAIC and Lockheed Martin

The SAIC and Lockheed Martin relationships are defence-prime integrations that position Infleqtion’s sensing and timing products within larger defence platform programmes. Both companies are named in Infleqtion’s customer and collaborator disclosures, though the specific contract values and programme details are not publicly available given their national security nature. The significance of these relationships is distributional: defence primes like SAIC and Lockheed Martin have established procurement relationships with the entire US defence establishment and can integrate Infleqtion quantum sensors into larger platform contracts at a scale that Infleqtion could not access through direct government sales alone. If either company standardises on Infleqtion sensing components for a major platform programme, the revenue impact would be substantially larger than any single government development contract.

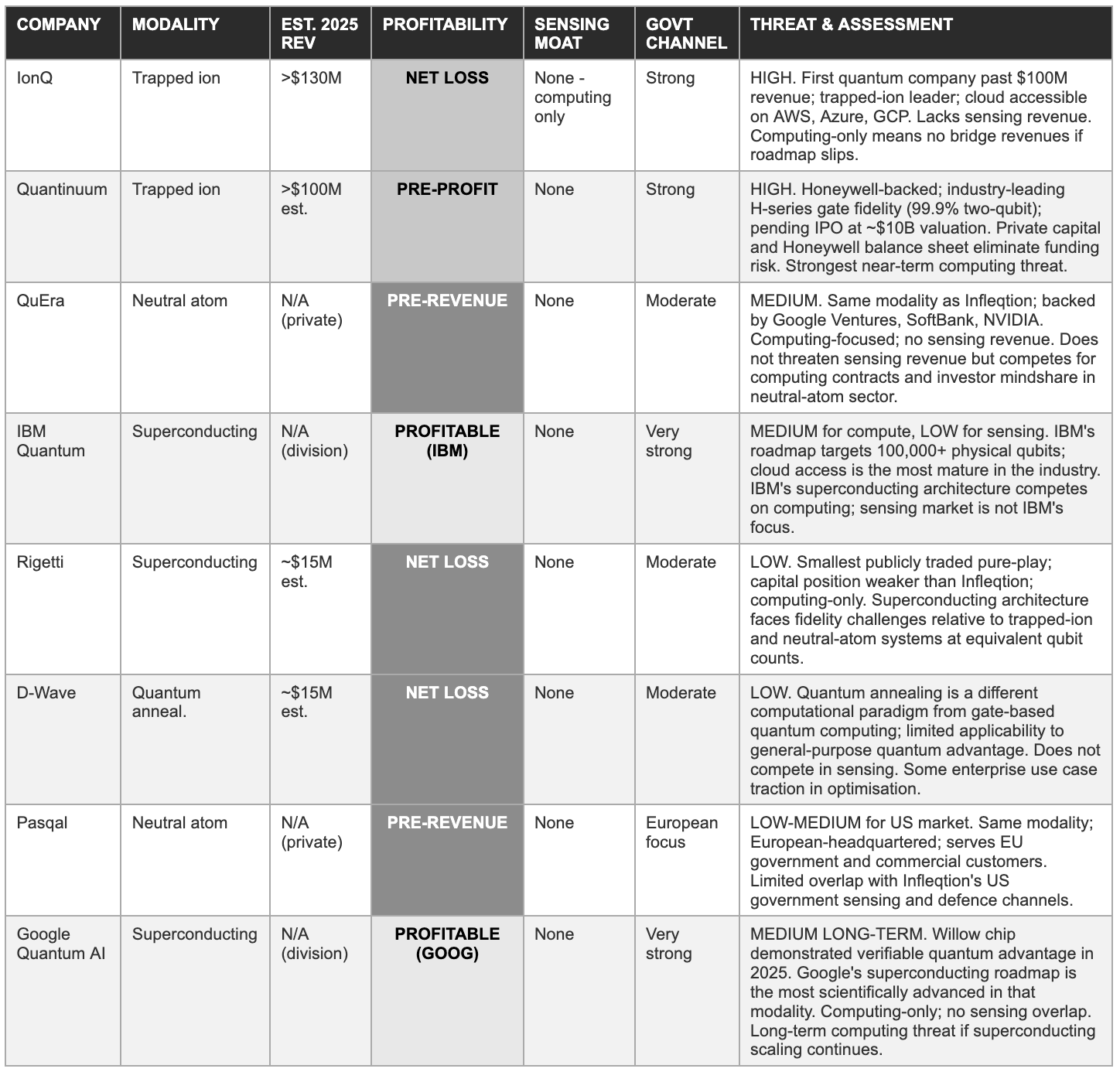

8. Competitive Landscape: Modality Wars & the Neutral-Atom Race

Six quantum pure-plays now trade on US exchanges, and the competitive landscape has bifurcated around two dimensions: modality (which physical qubit type wins the fault-tolerance race) and breadth (full-stack platform versus single-application focus). Infleqtion’s competitive position is strongest in neutral-atom breadth and government channel depth; it is weakest in computing revenue scale relative to IonQ and in commercial channel access relative to IBM and Google.

The competitive dynamic most relevant to Infleqtion’s near-term investment case is the distinction between computing-only peers and Infleqtion’s full-stack platform. Every publicly traded quantum pure-play derives substantially all revenue from computing-adjacent activities. Infleqtion derives the majority of revenue from sensing, which means that a delay in quantum computing commercialisation does not eliminate the company’s revenue base in the way it would eliminate the revenue base of Rigetti, D-Wave, or Quantum Computing Inc. This structural resilience is Infleqtion’s primary competitive differentiation at the business model level, and it is underappreciated by investors who frame the company purely as a quantum computing play.

The neutral-atom modality competition, between Infleqtion, QuEra, and Pasqal, is the dimension most likely to increase in intensity over the next two years. QuEra’s February 2025 convertible funding round of $230M, backed by Google Ventures, SoftBank, and NVIDIA, established it as the most heavily capitalised private neutral-atom competitor. QuEra’s approach, using atomic arrays with individual atom addressing, has produced impressive error correction demonstrations.

The technical distinction between QuEra’s and Infleqtion’s approaches is architectural detail that will be settled by performance benchmarks rather than by independent assessment. What is clear is that both companies will reach comparable logical qubit counts within similar timeframes, making differentiation on hardware performance alone insufficient. Infleqtion’s sensing revenue, government channel relationships, and Superstaq software differentiation are the competitive assets that matter when hardware parity is reached.

9. Financial History & The Revenue Scaling Question

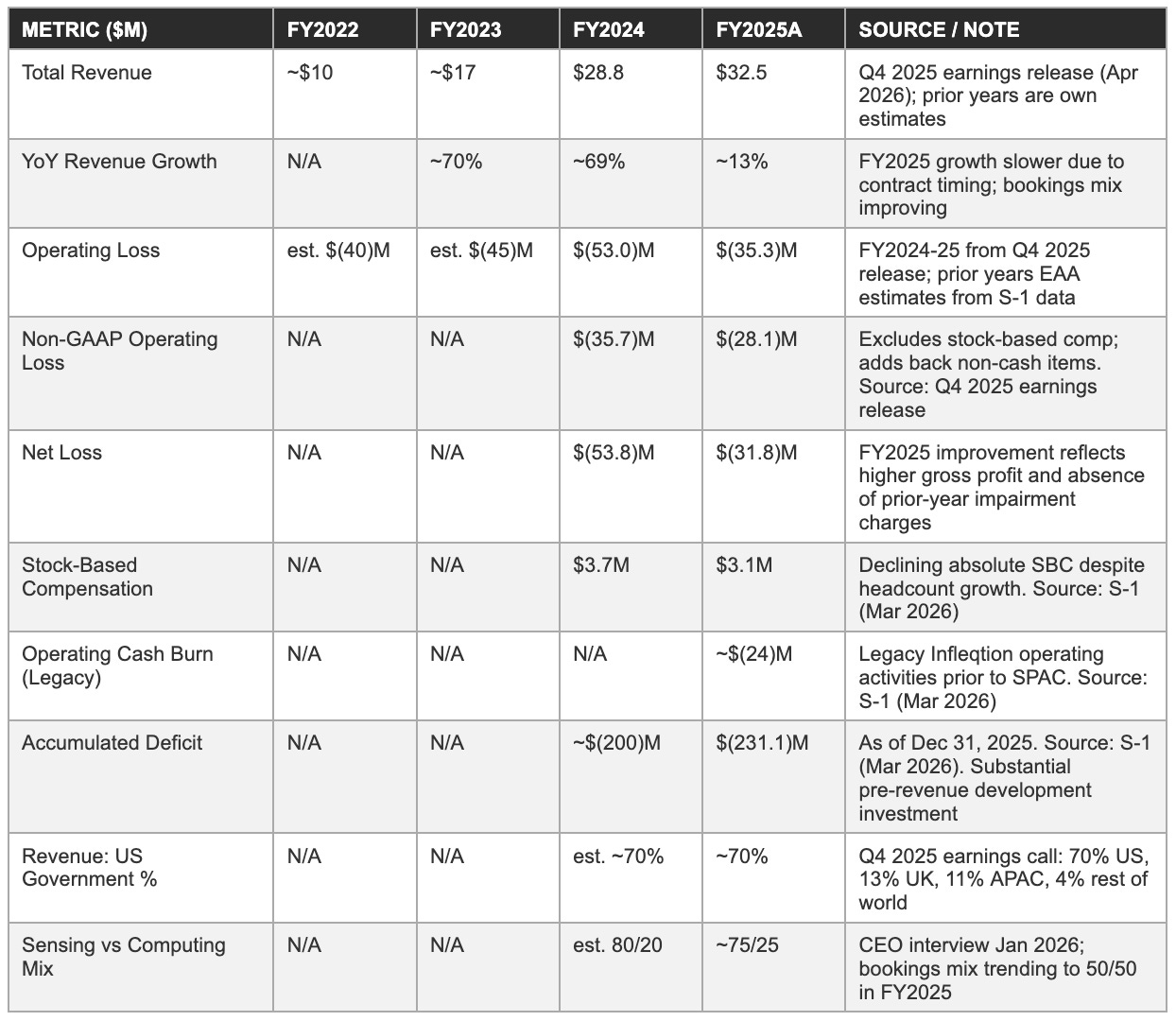

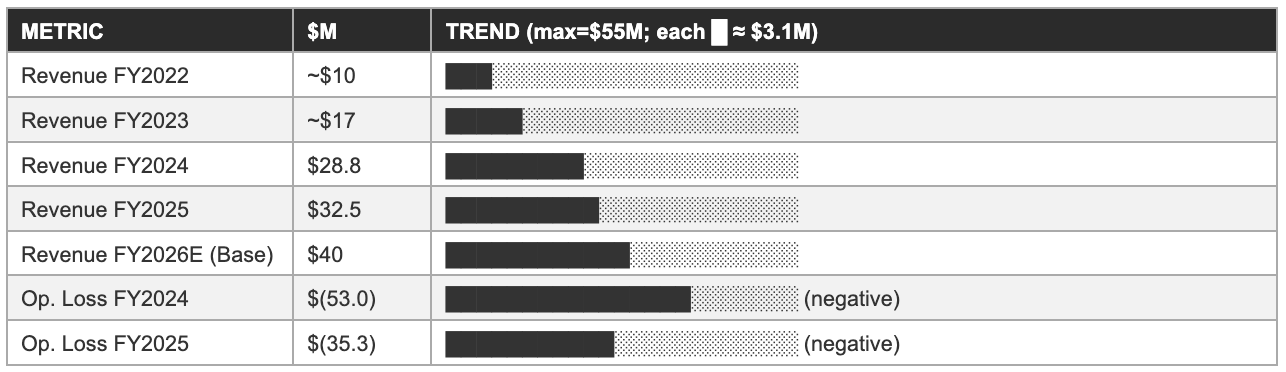

Revenue grew from approximately $10M in FY2022 to $32.5M in FY2025, a compound annual growth rate of roughly 48% over three years. Operating losses narrowed from $(53M) in FY2024 to $(35.3M) in FY2025, reflecting both revenue growth and cost discipline. The company guided to $40M in FY2026, implying 23% growth, a deceleration in percentage terms that reflects both the expanding base and the absence of large computing contracts in the near-term revenue pipeline.

Revenue growth: Visual comparison

The revenue deceleration

FY2025 revenue growth of approximately 13%, from $28.8M in FY2024 to $32.5M in FY2025, is the data point that deserves explicit scrutiny, because it represents a sharp deceleration from the 69% growth rate in FY2024. Management’s explanation centres on contract timing: large government contracts are milestone-gated, and the FY2025 revenue recognised reflects the completion cycle of contracts initiated in prior years rather than a reduction in new business activity. The bookings trajectory, not the revenue recognition schedule, is the forward indicator.

Management’s statement that FY2025 included approximately $50M of booked and awarded business, against $32.5M of recognised revenue, implies a revenue backlog that will accrete into FY2026 and FY2027 recognition. If accurate, the $40M FY2026 guidance is not simply a 23% growth target; it is the floor of a recognition schedule supported by already-committed contracts. The risk to the guidance is contract modification or programme cancellation rather than new business shortfall.

The $40M guidance carries one additional characteristic that is strategically significant: it is the first revenue guidance number Infleqtion has issued as a public company. Unlike companies with multi-year public track records of guidance construction, there is no established pattern of conservative guidance culture to draw on. FY2026 will be the year that establishes, or fails to establish, the management team’s credibility on forward revenue communication, making the Q2 and Q3 2026 quarterly reports the most important near-term observable data points in the investment case.

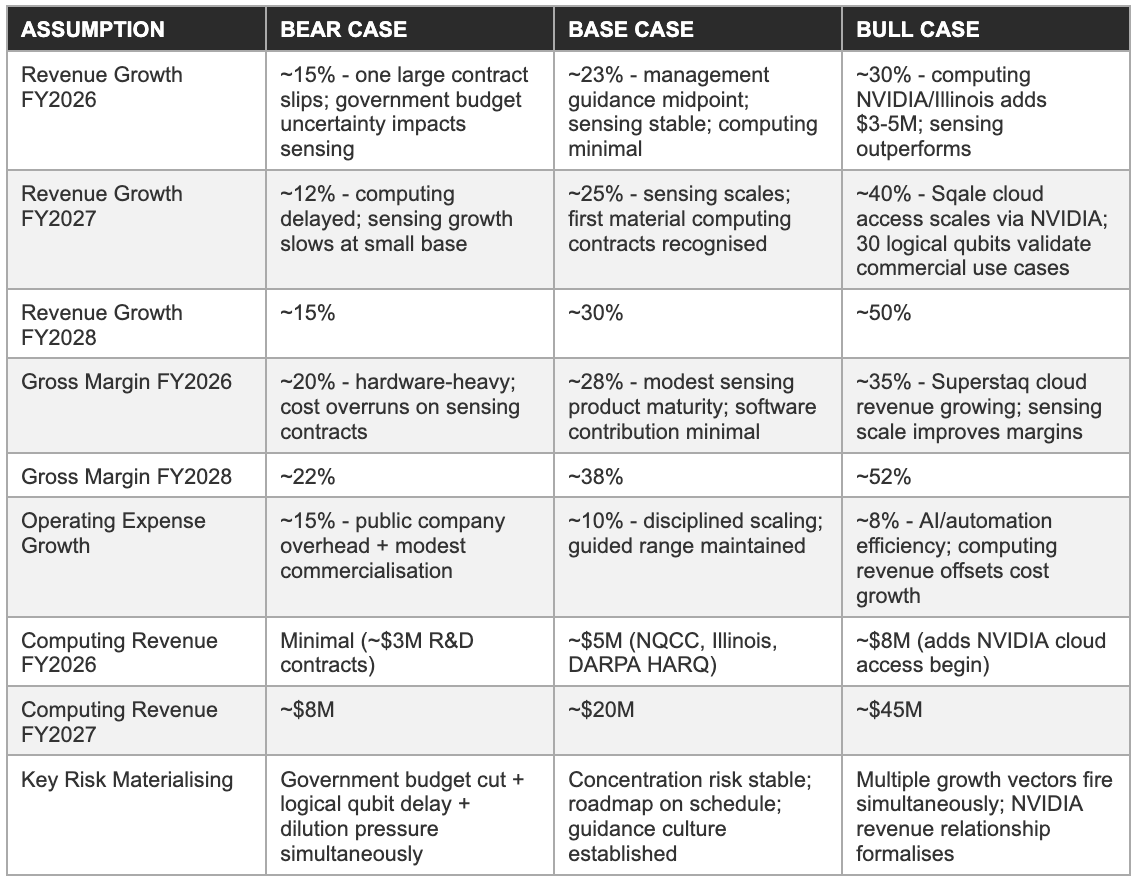

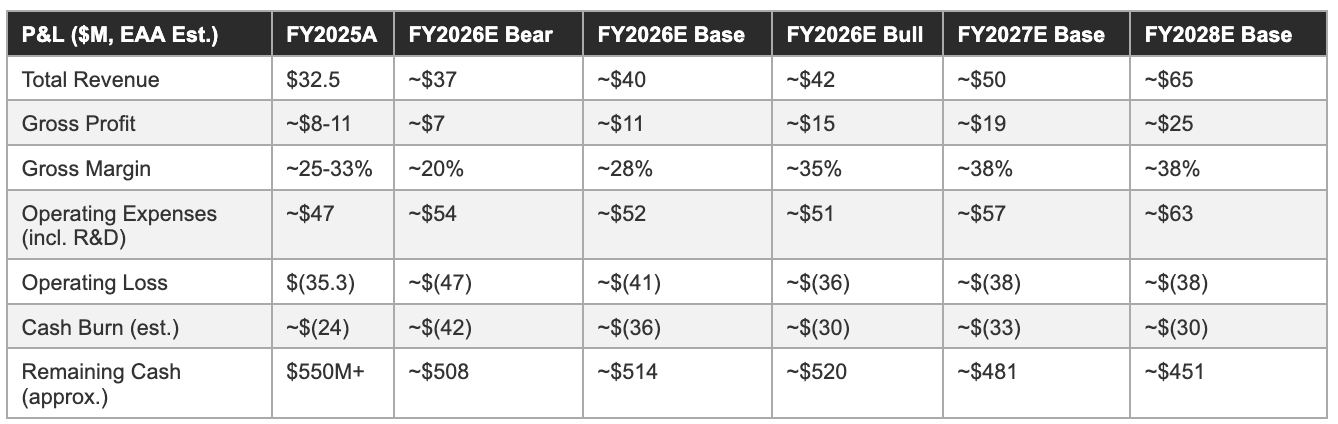

10. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios below are anchored to management’s FY2026 guidance of approximately $40M revenue and are extended through FY2028. Computing revenue is excluded from the FY2026 base case consistent with management’s guidance framing.

Three-year P&L projection

The cash runway analysis is the most important output of the financial model at this stage of the company’s development. Under the base case, cumulative cash consumption through FY2028 is approximately $99M, leaving a treasury in excess of $450M even after three years of scaled operations. Even under the bear case, cumulative burn through FY2028 is approximately $150M, leaving $400M in cash, a position that eliminates dilutive capital raise necessity through at least FY2031 at sustained bear-case burn rates.

The cash cushion is not merely a solvency buffer; it is the primary strategic asset that allows Infleqtion to pursue a patient commercialisation strategy rather than being forced into premature revenue recognition through underdeveloped commercial pricing.

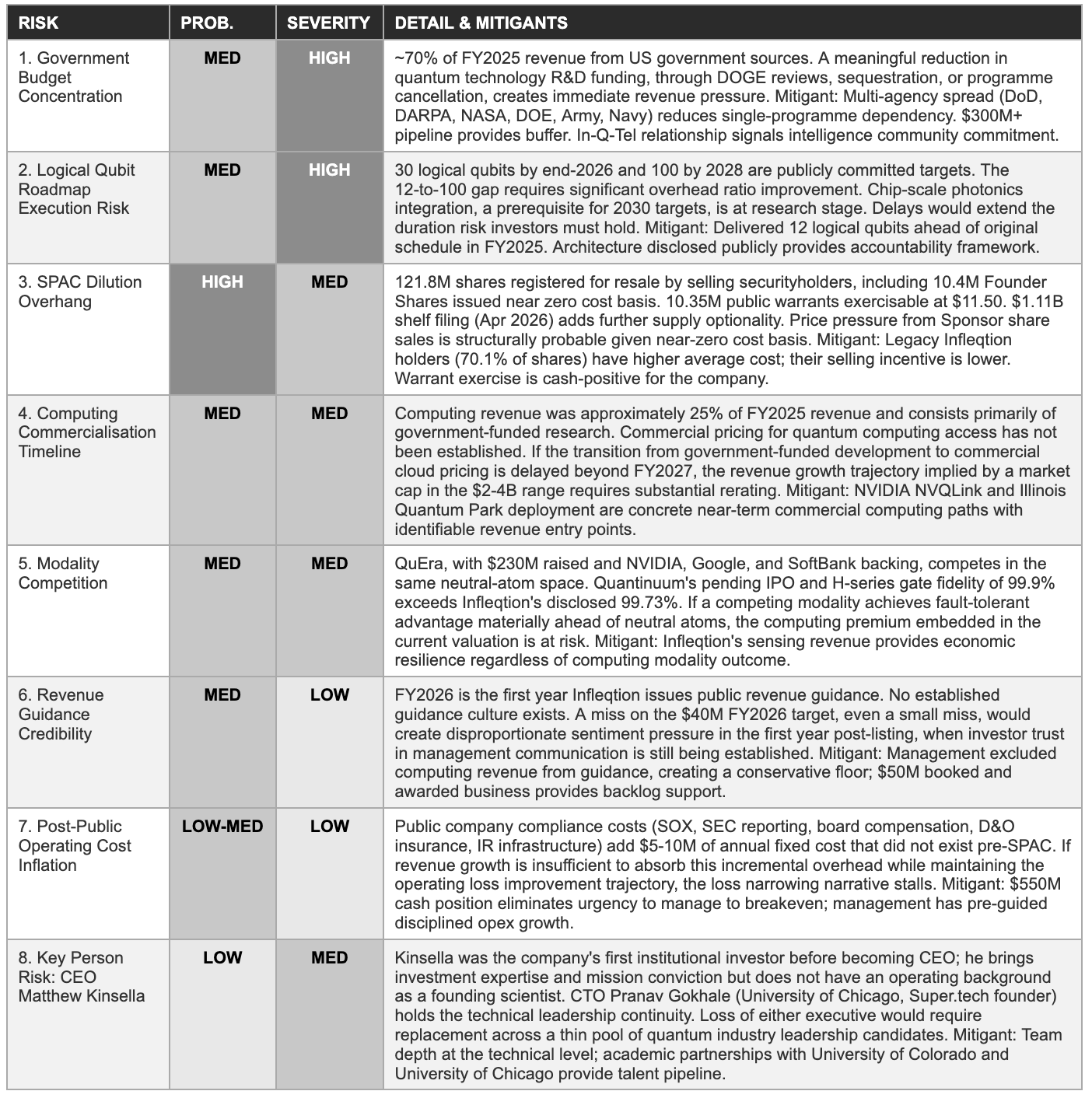

11. Risk Matrix

Each risk below represents a specific variable whose resolution determines which of the three scenarios in Section 10 is realised. Probability reflects the likelihood of a materially negative outcome within 24 months. Severity reflects the degree of impairment to the long-term investment thesis if the risk materialises. Risks are ordered by the combined weight of both dimensions.

12. Milestone Tracker: What to Watch 2026-2028

Management’s stated priorities for 2026, 30 logical qubits, computing revenue initiation, sensing contract growth, and continued operating loss improvement, translate into a set of observable proof points. The two highest-stakes near-term data points are the Q2 2026 earnings report (the first public quarterly result) and the end-2026 logical qubit delivery. Everything else is secondary until those are resolved.

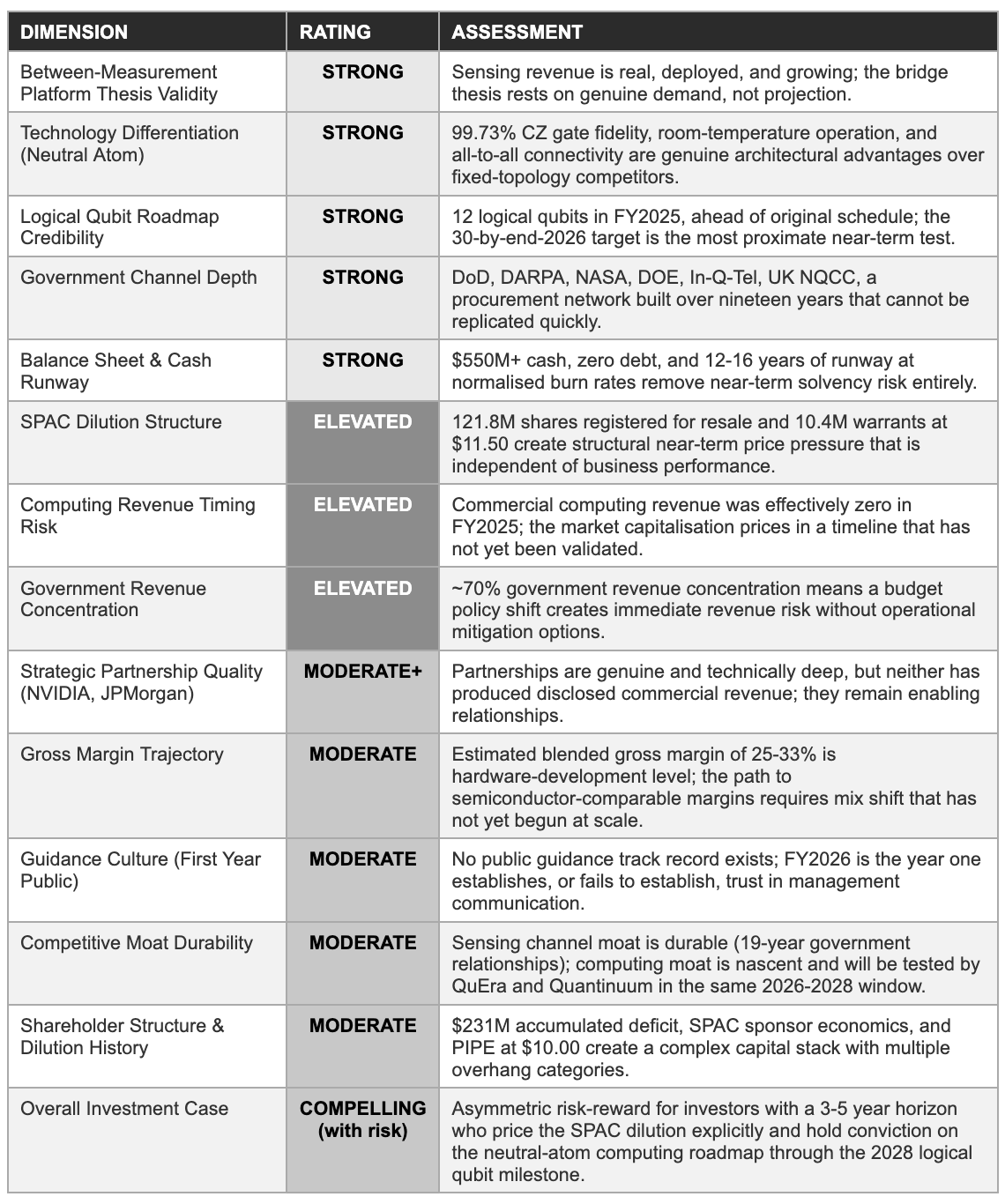

13. Investment Scorecard & Opinion: Bull, Base & Bear Cases

The following is our own view as of May 2026, not an investment recommendation, but an attempt to present the bull, base, and bear cases with equal analytical weight. At a market capitalisation implying a multiple of 60-90x trailing revenue on a pre-profit business, the burden of proof sits firmly with the bull case, and that case requires specific, observable outcomes within a defined window.

Investment scorecard

The bull case: Three pillars

The first pillar is the revenue bridge. Infleqtion’s sensing and timing business is a rare asset in the quantum sector: a quantum technology business generating $32.5M of revenue from deployed hardware in FY2025 with a 70% government customer base, a 230-patent portfolio, and a 19-year track record of delivery. This revenue base does not disappear if quantum computing takes longer than expected to commercialise. It continues to grow, continues to finance operations from the existing cash treasury, and continues to build the government channel relationships that will serve as the procurement network for commercial quantum computing when that market materialises.

The second pillar is the technical roadmap execution record. Delivering 12 logical qubits ahead of schedule in FY2025, installing the UK’s only operational 100-physical-qubit system in March 2026, and demonstrating the world’s first materials science logical qubit application with NVIDIA are not marketing claims — they are peer-reviewed, independently verified technical milestones. A company that delivers technical milestones ahead of schedule, on a specific and publicly committed roadmap, provides the kind of observable proof points that justify holding duration risk through a multi-year commercialisation window.

The third pillar is the balance sheet. With $550M+ in cash and zero debt, Infleqtion can afford to be patient with commercial pricing, invest in the chip-scale photonics programme without capital market pressure, and weather a government budget disruption without existential consequences. In a sector where counterparty solvency is now a procurement screening criterion, the treasury is itself a competitive asset.

The bear case: Three concerns

The first concern is the valuation implied by the market capitalisation. A market capitalisation in the $2-4B range on $32.5M of trailing revenue implies a revenue multiple of 60-120x, a range that embeds a specific commercial computing timeline that has not been validated. If computing revenue does not reach $50-100M by FY2028, which is the base and bull case assumption, the implied multiple at that revenue base is still demanding relative to comparable-stage technology companies. The SPAC listing mechanism, which typically prices at a premium to private round valuations, may have imported a valuation from the peak of the 2021-2022 quantum enthusiasm cycle that the current market would price more conservatively absent the SPAC mechanics.

The second concern is the dilution overhang’s independence from business performance. The 121.8M shares registered for resale, the 10.4M warrants, and the $1.11B shelf registration create price pressure mechanisms that activate regardless of whether the business is performing well. A Sponsor holder whose shares were received at near-zero cost has an economically rational incentive to sell at any price above minimal thresholds, irrespective of the company’s technical progress. This structural pressure is most acute in the 12-24 months following listing, precisely the period when investors who purchased at listing prices are waiting for the first evidence of computing revenue.

The third concern is the absence of a comparable successful outcome in the quantum sector to calibrate expectations. No pure-play quantum company has yet transitioned from government-funded research revenue to large-scale commercial computing revenue. IonQ is the furthest along on this transition, past $100M in annual revenue, but the commercial computing portion of that revenue remains modest relative to the total. Infleqtion’s path to $1B+ in annual revenue requires outcomes that have no precedent in the industry, at a timeline that the market is being asked to price today. The bear case is not that neutral-atom quantum computing fails; it is that it succeeds, but on a timeline measured in 8-12 years rather than 3-5, and that the current multiple cannot be sustained through the intervening period.

The bottom line

The investment case for Infleqtion at current prices is fundamentally a duration trade: the business has real technology, real revenue, and real cash, but the multiple requires a computing commercialisation timeline that has no precedent. The bull case is asymmetrically large; the path to it requires specific, observable milestones to arrive on schedule; and the SPAC dilution structure creates near-term price pressure that is independent of those milestones.

Investors who can model the dilution explicitly, hold through a 3-5 year commercialisation window with conviction on neutral-atom physics, and treat the $550M cash position as the duration insurance it is, are taking a calculated bet on a genuinely differentiated technology company at a genuinely demanding multiple.

Sources

This report has been prepared by EAA Partners from publicly available information as of May 2026. Primary sources: Infleqtion Q4 2025 earnings release and conference call (Apr 2026, Business Wire / Yahoo Finance transcript); S-1 Registration Statement (Mar 2026, SEC EDGAR); SPAC Form 425 (Feb 2026, SEC EDGAR); 10-K Annual Report (Mar 2026, SEC EDGAR via ir.infleqtion.com); DARPA HARQ contract press release (Apr 2026, Business Wire); NQCC 100-qubit delivery press release (Mar 2026, Business Wire); NVIDIA GTC 2026 NVQLink announcement (Mar 2026, Business Wire); Infleqtion 2026 revenue guidance press release (Apr 2026, Business Wire); Churchill Capital Corp X Form 424B3 (Mar 2026, SEC EDGAR); CEO Matthew Kinsella interview, Sherwood News (Jan 2026); Morningstar, Robinhood, and TradingView for market data; Stocktwits and StockTitan for SEC filing summaries; The Quantum Insider and Quantum Zeitgeist for competitive landscape data.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Infleqtion, Inc. (NYSE: INFQ) or any other security. All information is sourced from publicly available materials believed to be reliable as of May, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.