INNVENTURE, INC.

Disruptive Conglomerate: Platform Value, Execution Risk, and the Accelsius Inflection

1. Corporate Profile & The Create-and-Operate Thesis

Innventure sits outside every standard investment category. It is an industrial growth conglomerate that identifies, licenses, seeds, and operates companies built around breakthrough technologies sourced from multinational corporations. The model has produced one public exit at a 26.8x return for early investors and three companies in active commercial development. Understanding what Innventure is, and what it is not, requires setting aside venture capital, private equity, and holding company frameworks entirely and evaluating it on its own structural terms.

The company’s stated purpose is to build companies with target enterprise values of at least one billion dollars by commercialising technologies that multinational corporations have developed but chosen not to bring to market independently. This commercialisation gap is real and structural. Large corporations generate substantial research and development output that frequently remains unutilised because the commercialisation pathway requires a different organisational model, a different risk tolerance, and a management team with a different incentive structure than exists inside the originating corporation. A technology that is too small to move the needle for a fifty-billion-dollar MNC may be the foundation of a billion-dollar independent company with the right commercial execution.

Innventure’s value proposition to the MNC is a structured and risk-shared pathway to realising value from stranded IP without bearing the full commercialisation burden. To Innventure’s shareholders, the proposition is exposure to a portfolio of early-stage industrial companies built on validated, IP-protected technology foundations rather than raw scientific hypotheses. The MNC’s prior investment in the technology de-risks the scientific development stage; what remains is commercialisation risk, which Innventure’s management team and shared services infrastructure are designed to manage across multiple simultaneous operating companies.

The four companies: An operational map

The company’s operating history encompasses four launched businesses. PureCycle Technologies was seeded in 2015 using polypropylene recycling technology licensed from Procter and Gamble. Innventure invested under ten million dollars at inception and took PureCycle public through a deSPAC transaction in Mar 2021 at a post-money valuation of 1.2 billion dollars, generating a 26.8x return on invested capital for early investors by management’s disclosure.

Innventure no longer holds an economic interest in PureCycle. The post-listing trading history of PureCycle as an independent company, which has significantly declined from its deSPAC peak, is not Innventure’s performance, but it is the relevant context for assessing whether Innventure’s model reliably produces sustained public market value creation or point-in-time liquidity events. Both interpretations are analytically supportable; the honest position is that one completed exit is insufficient statistical evidence for either conclusion.

AeroFlexx, a sustainable liquid packaging company using P&G-derived technology, was launched in 2018. As of Q1 2026, AeroFlexx has generated six consecutive quarters of commercial revenue across the pet, baby, industrial, personal care, and household product categories, and has announced a global partnership with Aveda, the Estee Lauder-owned professional hair care brand. AeroFlexx operates a manufacturing facility in West Chester, Ohio, and is preparing to conduct a direct capital raise at the operating company level to fund production line expansion.

Accelsius Holdings LLC, a two-phase direct-to-chip liquid cooling company built on Nokia Bell Labs technology, was launched in May 2022 and is the dominant near-term value driver in the portfolio. Accelsius closed a 65 million dollar Series B in Jan 2026 led by Johnson Controls and is now independently capitalised. Refinity Olefins LLC, which intends to convert mixed plastic waste into drop-in chemical intermediaries using technology from VTT Technical Research Centre of Finland, was launched in 2024 and is at pilot validation stage. The four businesses collectively represent three sectors, a breadth that management characterises as risk diversification and critics characterise as operational complexity at sub-scale.

The shared services model and its economics

Innventure operates across its portfolio through a shared services structure under which the parent provides accounting, finance, legal, human resources, and IT support to each operating company. This structure keeps the operating companies lean during the early development phase and allows Innventure to amortise a single professional infrastructure across multiple businesses. The theoretical economic advantage is clear: a single CFO, a single legal team, and a single IT infrastructure serving three companies cost less than three sets of those functions.

The practical risk is equally clear: shared services create dependencies that can create bottlenecks, and the material weaknesses in internal controls identified in the FY2025 audit (insufficient accounting staffing, inadequate IT general controls, and lack of segregation of duties) are a direct consequence of the shared services model being understaffed relative to the compliance obligations of a public company.

The strategic direction is for the shared services dependency to decline as operating companies mature. Accelsius is now independently capitalised and is developing its own management infrastructure as it scales. AeroFlexx and Refinity are both preparing for direct capital raises that would come with expanded investor governance requirements and, in due course, the need for standalone financial reporting capability. Each transition toward operating company independence reduces the scope of the parent’s shared services obligation and, in principle, reduces parent G&A expenses over time.

The financial logic of the create-and-operate model

The economic logic of Innventure’s model rests on three structural advantages over conventional venture capital.

First, the technology sourcing discipline reduces the scientific validation cost: when an MNC has already spent tens or hundreds of millions of dollars in R&D to develop a technology to pilot or commercial-validation stage, Innventure’s licence cost is a fraction of the development investment, it is paying for access to a pre-validated asset rather than funding the validation itself.

Second, the shared services model reduces the overhead cost of early-stage operating companies: a single set of corporate functions serving three businesses costs less per business than three independent sets of functions, which extends the effective runway of each operating company’s capital.

Third, the create-and-operate orientation, building toward long-term operating company value rather than the earliest available exit, creates the conditions for compounding returns that venture capital’s fund-cycle constraints frequently prevent.

The model’s economic vulnerability is equally structural. The front-loading of costs, capital must be deployed to develop operating companies before those companies generate the revenue that justifies the investment, creates a prolonged cash consumption period that must be funded externally.

In a private context, this funding comes from venture capital with defined investment timelines; in a public context, it comes from equity markets that price the stock daily and demand near-term evidence of progress. The tension between a model designed to create value over a seven-to-ten-year horizon and a public market that evaluates performance quarterly is the fundamental source of the volatility and the valuation discount that characterise INV’s trading history since the deSPAC listing. Resolving that tension requires demonstrating commercial milestones, specifically Accelsius revenue, quickly enough to give public market investors the evidence they need to hold through the long-duration value creation arc.

2. The DownSelect Architecture: How Innventure Sources and Builds Companies

The quality of Innventure’s future pipeline depends entirely on the quality of its technology sourcing discipline. The DownSelect methodology is the company’s proprietary framework for screening MNC-held technologies. Its criteria and limitations are the prerequisite for assessing whether the current three-company portfolio is a reliable sample of what the model can produce, or a partial expression of a methodology still being refined through experience.

Innventure’s DownSelect process is a staged screening methodology designed to identify technologies held by large corporations that meet a specific commercialisation opportunity profile. The primary quantitative threshold is a target enterprise value of at least one billion dollars for the resulting business. This threshold narrows the universe of candidate technologies sharply: it requires a combination of market size, unit economics, scalability, and competitive differentiation that most MNC-held orphan technologies do not simultaneously possess. Management applies the billion-dollar criterion at the outset rather than after initial investment, which forces a discipline around addressable market estimation before resources are committed.

The secondary DownSelect criteria include intellectual property protection quality, the technology must be patentable or already patent-protected to create a defensible market position that justifies the commercialisation investment, and technology readiness level. Innventure targets technologies that have been developed to the point where the primary residual risk is commercial execution rather than scientific feasibility.

This is the critical risk transfer that the MNC relationship enables: when Nokia Bell Labs has spent years developing a two-phase cooling technology internally, the scientific validation has been funded by Nokia’s R&D budget. What Innventure acquires is the right to take a technically validated technology and build a commercial business around it, absorbing the go-to-market risk rather than the fundamental research risk.

A third criterion is MNC strategic alignment: the MNC must be willing to license or transfer the technology under terms that allow Innventure to build a genuinely independent business without conflicting channel obligations, downstream royalty structures that impair the unit economics, or reversion rights that undermine investor confidence in the operating company’s asset base.

Negotiating these terms requires the MNC to accept that Innventure’s value creation approach, long-term operation and eventual public market exit, is aligned with the MNC’s interest in realising value from the stranded technology. The terms of each license are not publicly disclosed, which creates a due diligence gap for external investors: the specific royalty rates, license durations, and reversion conditions that govern each operating company’s technology rights are material to the long-term value of each business and are not available in public filings.

Why the MNC relationship is structurally different from founder-pitch venture

The MNC relationship provides a set of advantages that pure-play venture studios sourcing founder-generated ideas do not possess. When a corporation with the research infrastructure of Procter and Gamble or Nokia has developed a technology to a stage of maturity sufficient for Innventure to license it, the scientific risk has been substantially pre-absorbed by the MNC’s existing budget.

The technology has been tested in a lab environment, assessed against internal development priorities, and typically reviewed by engineers who have identified both its potential and its limitations. This prior evaluation means that Innventure is not betting on a founder’s intuition about a scientific hypothesis; it is betting on a commercial execution thesis for a technology that already works at laboratory or pilot scale.

The MNC relationship also creates commercial advantages that extend beyond the technology licence itself. When Accelsius sources cooling technology from Nokia Bell Labs, the Nokia association, and Nokia’s willingness to collaborate with the resulting company, provides a form of credibility in enterprise conversations that a founder-led startup with equivalent technology but no institutional provenance would not possess.

The Johnson Controls and Legrand investments in the Accelsius Series B are the clearest illustration: two global industrial infrastructure companies committed capital to an Innventure-incubated company, providing not just funding but market validation, supply chain access, and sales channel leverage that accelerates the commercial ramp in a way that purely financial investment would not.

DownSelect limitations and pipeline sustainability

The DownSelect process has three structural limitations that are analytically important. First, the process depends on Innventure’s ability to maintain access to MNC technology portfolios, which in turn requires a track record of successful exits that MNC counterparties find credible. The PureCycle deSPAC at 1.2 billion dollars is Innventure’s reference case for MNC conversations; as long as the deSPAC exit is understood as the relevant performance metric, it remains a compelling reference. Accelsius’s 665 million dollar Series B valuation provides a more recent and still-active data point that is free of the post-listing ambiguity of the PureCycle case.

Second, the DownSelect process creates an inherently slow pipeline cadence. Innventure has launched four companies in approximately nine years, a frequency of roughly one every two to three years. At any given time, the number of operating companies at active commercial development is therefore small, currently three, which concentrates execution risk in a way that larger and more mature industrial conglomerates do not face. If any of the three current businesses fails to achieve commercial scale within its capital runway, there is limited portfolio diversification at the operating level to absorb the impact.

Third, the selection effect implicit in the process deserves explicit attention. Technologies that MNCs have developed but chosen not to pursue commercially are, by definition, technologies that internal corporate evaluation has deprioritised. In many cases this deprioritisation reflects resource allocation decisions rather than a negative technology assessment, the technology is viable but too small or too distant from the core business to justify the corporation’s attention.

In some cases, however, internal deprioritisation reflects a genuine judgment that the commercial economics are insufficient, the market timing is wrong, or the competitive landscape is too challenging. Innventure’s DownSelect discipline is designed to distinguish between these two categories, but the distinction is not verifiable from outside the process.

The DownSelect process as a competitive barrier

From a competitive moat perspective, the DownSelect process creates a sourcing advantage that is difficult for others to replicate quickly. Innventure’s access to MNC technology portfolios is built on relationships that have been developed over nine years of operating history, validated by the PureCycle exit and the Accelsius commercial trajectory.

A new entrant attempting to replicate the create-and-operate model would need to independently establish credibility with MNC technology licensing teams, a process that requires demonstrated exits rather than just capital. The PureCycle deSPAC at 1.2 billion dollars is Innventure’s primary credential in those conversations, and it is the kind of outcome that takes years to replicate.

The barrier is not insurmountable, a well-capitalised competitor with a credible founding team could establish MNC relationships over three to five years. But the lead that Innventure’s existing relationship network provides is a genuine competitive advantage in sourcing the technologies that feed its model. The specific MNC relationships that produced Accelsius (Nokia), AeroFlexx (P&G), and Refinity (VTT and Dow) represent years of technology licensing negotiation, collaborative development, and commercial structuring that cannot be replicated simply by identifying the same technologies in an MNC’s portfolio.

The institutional knowledge of how to structure a technology licence that allows an independent company to succeed while protecting the MNC’s interests is itself a form of intellectual capital that compounds with each transaction.

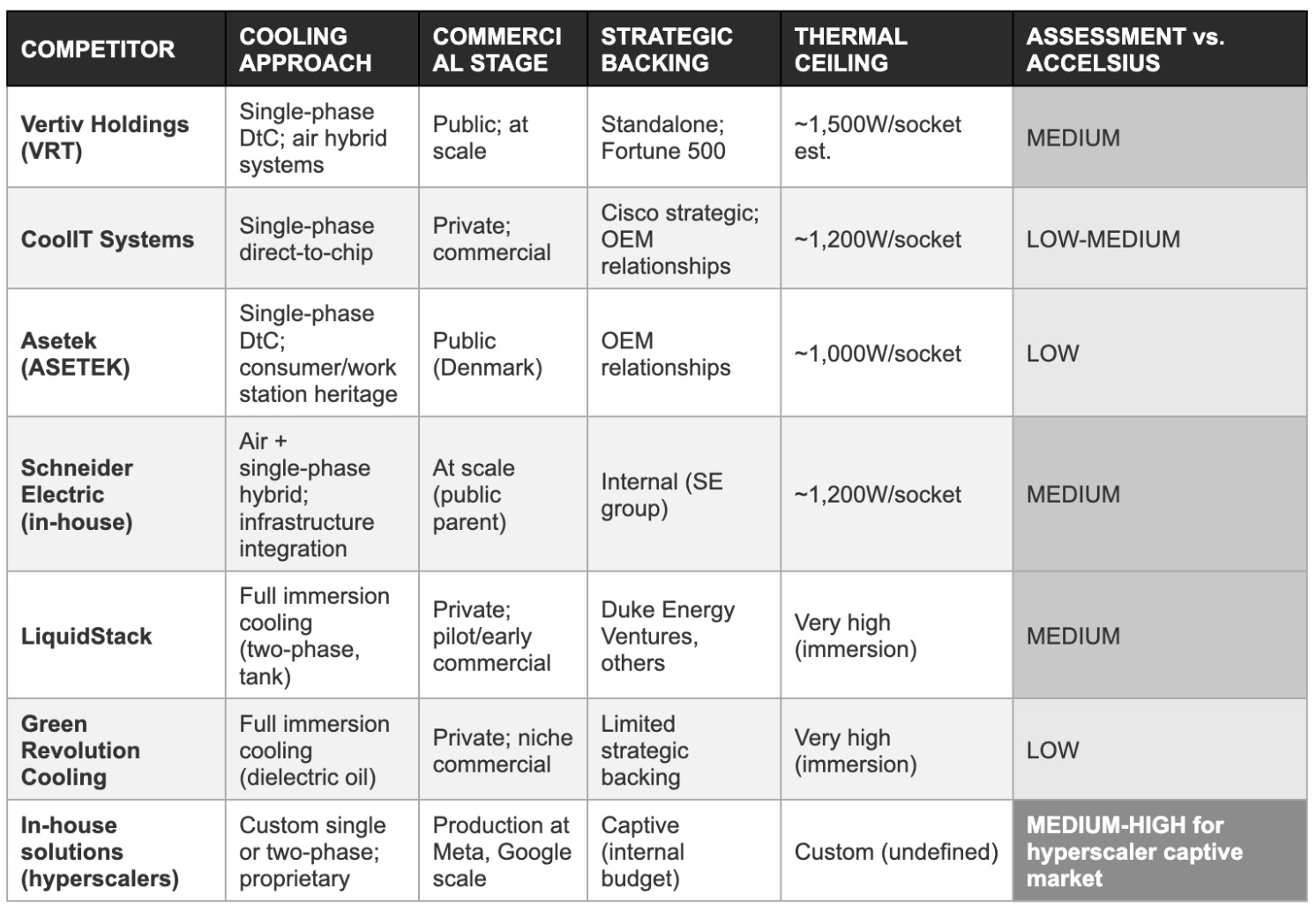

3. Accelsius: The AI Cooling Thesis and the Commercial Inflection

Accelsius is the investment thesis at Innventure as of mid-2026. The $50 million in Q1 2026 bookings against a full-year 2025 revenue base of $1.6 million represents a potential commercial step-change of the kind that either validates the entire create-and-operate platform model or exposes the gap between a strong sales pipeline and the operational capability to convert it. Everything else in the Innventure portfolio is analytically secondary to the resolution of that question over the next two to three quarters.

The technology: Why two-phase matters

Accelsius was founded by Innventure in May 2022 using two-phase direct-to-chip liquid cooling technology originally developed at Nokia Bell Labs. The core product line, the NeuCool platform, uses a dielectric coolant, a fluid that does not conduct electricity and is therefore safe in proximity to sensitive computing hardware, which is circulated directly to the surface of each processor chip. At the chip surface, the coolant is allowed to undergo a phase transition from liquid to vapour.

This phase change is the physical basis of the technology’s thermal performance advantage: the heat energy absorbed during the liquid-to-vapour transition (the latent heat of vaporisation) is substantially larger than the heat energy that can be absorbed by raising the temperature of a liquid without a phase change, which is the mechanism by which all single-phase liquid cooling systems operate.

The practical consequence is that a two-phase direct-to-chip system removes significantly more thermal energy per unit volume of coolant circulation than a single-phase system, and does so at a more stable chip-surface temperature because the coolant boils at a fixed temperature rather than accumulating heat continuously as it travels from inlet to outlet.

Accelsius has tested its NeuCool technology to thermal removal capacities exceeding 4,500 watts per socket, a threshold that represents more than six times the thermal design power of a current-generation consumer GPU and is well above the specifications of the highest-performance AI accelerators currently in production. Single-phase direct-to-chip systems have demonstrated effective thermal management at up to approximately 1,200 to 1,500 watts per socket in production deployments, which covers a wide range of current AI workloads but leaves a meaningful performance gap at the density frontier.

The NeuCool IR150, launched at the NVIDIA GTC conference in Apr 2026, represents the most recent product evolution, the industry’s first integrated rack for two-phase liquid cooling, designed to simplify the deployment of two-phase cooling at the rack level rather than requiring custom-engineered coolant distribution infrastructure for each deployment. The IR150 launch broadened the addressable deployment base from custom-engineered greenfield installations to a more standardised rack-level product, which reduces the barriers to adoption for data center operators who want the thermal performance of two-phase without the engineering overhead of a bespoke installation.

The market forcing function

The relevance of Accelsius’s thermal performance envelope has increased sharply with successive AI GPU generations. Current-generation NVIDIA B200 and GB200 accelerators draw on the order of 700 watts per GPU; rack configurations combining multiple GPUs with networking and storage infrastructure are producing rack-level heat densities that have already exceeded the practical limits of conventional air cooling and are approaching the limits of single-phase liquid cooling in the densest configurations.

Published industry forecasts project that liquid cooling penetration of AI data center infrastructure will expand from a minority of deployments today to the majority within two to three years, driven by the thermal requirements of the continued AI infrastructure buildout rather than by any technology push from the cooling industry.

The data center liquid cooling market overall is projected to grow at a compound annual rate exceeding twenty percent through the end of the decade, with premium two-phase systems commanding a price and margin advantage over single-phase alternatives that is justified by the superior thermal performance and zero-water architecture.

For data center operators, the selection of a cooling technology is not an isolated procurement decision, it determines the maximum rack power density achievable in a given physical footprint, which in turn determines how much AI compute can be deployed per unit of data center real estate. In a period when data center land and power availability are the binding constraints on AI infrastructure expansion, the ability to deploy denser compute in a given footprint has a direct financial value that makes premium cooling economics straightforward to justify.

Commercial progress and the bookings inflection

Accelsius generated 1.6 million dollars in revenue in FY2025, growing 433% from its FY2024 base. The Q1 2025 through Q3 2025 trajectory was characterised by Accelsius transitioning from proof-of-concept deployments to initial production orders, with a strengthening pipeline and the progression of the Series B fundraising process that culminated in the Jan 2026 close. The $50 million in Q1 2026 bookings represents the conversion of pipeline to commercial commitments, a qualitatively different stage from the proof-of-concept deployments that generated the 2025 revenue.

The DarkNX agreement, announced in connection with the Mar 2026 milestone update, commits to the deployment of NeuCool technology across a new 300 megawatt AI data center campus in Ontario, Canada. Management described this as the largest planned two-phase direct-to-chip deployment to date, and the scale is significant: at 300 megawatts, the DarkNX campus is a major greenfield data center project, and the selection of Accelsius as the cooling infrastructure vendor for the entire facility represents the kind of design-win that generates multi-year recurring revenue as the campus is built out in phases. The 65 megawatt initial phase and subsequent 65 megawatt second phase described in management conference commentary imply a phased revenue recognition profile rather than a single lumpy delivery.

The 3-year master purchasing agreement signed in Mar 2025 with a global thermal management company to white-label Accelsius’s liquid cooling solution for resale to that company’s end customers and channel partners is a distribution relationship that provides a secondary revenue pathway beyond direct data center operator sales. White-label agreements of this type function as a capital-efficient channel extension: the channel partner’s existing sales force and customer relationships carry Accelsius’s technology into conversations that Accelsius would not independently be positioned to access at its current commercial scale.

The bookings-to-revenue conversion

The central analytical question for Accelsius in 2026 is the timeline and rate of bookings-to-revenue conversion. Bookings represent commercial commitments from customers but do not generate recognised revenue until the product is delivered and accepted.

For a hardware company deploying specialised cooling infrastructure into greenfield data center facilities, the delivery and acceptance cycle involves multiple sequential dependencies: component procurement, assembly and quality testing at the Austin production facility, logistics to the customer site, civil engineering coordination for the coolant distribution infrastructure, integration with the data center’s power and networking systems, commissioning and performance validation, and formal customer acceptance. Each step can be delayed independently, and the cumulative effect of moderate delays across multiple steps can push revenue recognition by a quarter or more.

Management has explicitly cited supply chain constraints as a factor affecting revenue timing, which is a direct acknowledgment that the conversion timeline is not fully within Accelsius’s control. The specific supply chain risks in a two-phase dielectric cooling system include the dielectric coolant itself (a specialised fluid with a limited supplier base), the heat exchanger assemblies that interface between the coolant and the chip package, and the custom manifold and distribution piping that delivers coolant to each server rack. The Jan 2026 Series B proceeds are in part intended to fund supply chain investment, including component inventory build-ahead and potential supplier qualification expansions that would reduce single-source dependency.

The management target of reaching a 100 million dollar annual revenue run-rate at Accelsius by year-end 2026 and achieving operating cash flow positivity at the subsidiary level by the same date implies a revenue recognition cadence that is heavily back-weighted to the third and fourth quarters of 2026. If the DarkNX Phase 1 deployment and several additional bookings-from-Q1 convert to revenue in Q3 and Q4 2026, the full-year result could approach or exceed the 100 million dollar annualised target without requiring Q1 or Q2 revenue to be transformatively large.

Accelsius competitive position

The two-phase direct-to-chip cooling segment is occupied by a small number of players at various stages of commercial maturity. The competitive table below assesses the most relevant alternatives across the dimensions that matter in enterprise data center procurement decisions.

4. AeroFlexx and Refinity: Complementary Platforms, Independent Capital Paths

AeroFlexx and Refinity address different markets, carry different risk profiles, and are at materially different commercial stages. Both are being positioned for direct capital formation outside the Innventure parent balance sheet, a structural transition that, if successfully executed, would release the parent from funding obligations that currently represent a material fraction of its cash burn.

AeroFlexx: Sustainable liquid packaging with six quarters of revenue

AeroFlexx was launched in 2018 using flexible packaging technology sourced from Procter and Gamble. The company manufactures a proprietary sustainable liquid packaging format, a flexible, air-cushioned pouch designed to replace rigid plastic and glass containers in consumer and industrial liquid product categories. The format’s environmental proposition is that it uses materially less plastic by weight than conventional rigid containers, is lighter for transportation (reducing shipping emissions and cost), and is designed to be recyclable through standard flexible film recycling streams that rigid plastic and glass are not eligible for.

The commercial traction is the most tangible evidence of product-market fit in the Innventure portfolio outside of Accelsius. Six consecutive quarters of revenue recognition across the pet, baby, industrial, personal care, and household categories establish that AeroFlexx’s format has cleared the buyer evaluation threshold at multiple independent brand owners operating in different product categories. Revenue growth has been constrained by production line capacity rather than by customer demand, a constraint that creates a visible and investment-addressable bottleneck, which is a preferable position to demand-side uncertainty.

The Aveda global partnership, announced in Q1 2026, is the highest-profile commercial milestone AeroFlexx has achieved. Aveda is the Estee Lauder-owned professional hair care brand, known for its premium environmental positioning and global distribution through professional salons and retail. Estee Lauder companies collectively operate extensive global supply chains for liquid personal care products, and an Aveda partnership creates a potential pipeline into broader Estee Lauder brand relationships if the Aveda rollout demonstrates the format’s performance at global scale. The eleeo brands partnership for the Boogie Bubbling Vapor Bath product, announced separately, adds a consumer baby care reference that expands the brand portfolio into a category with significant premium packaging sensitivity.

AeroFlexx’s West Chester, Ohio production facility operates the initial commercial line, which was installed with a nameplate design capacity of over 50 million units per year. Two additional production lines were planned to be launched during 2025, expanding total capacity to over 150 million units annually at nameplate. The capital intensity of packaging line installation means that revenue growth is directly limited by line availability, and the Aveda global rollout requires production capacity that a single-line facility cannot deliver at scale. The direct capital raise that AeroFlexx is preparing will be directed in part toward production line expansion and working capital for the Aveda ramp. The ability to raise that capital at a valuation that is accretive to Innventure’s current implied holding value is the key execution variable for AeroFlexx in 2026.

The competitive environment for AeroFlexx is the established flexible packaging industry, where Amcor, Sealed Air, Mondi, and Berry Global operate at scales orders of magnitude larger than AeroFlexx and maintain longstanding relationships with the brand owners that AeroFlexx is targeting. AeroFlexx’s differentiation is the proprietary air-cushion format, which provides structural protection for liquid products in a form factor that established suppliers do not equivalently offer. The competitive risk is that the larger players develop equivalent formats if the market opportunity justifies the investment, a risk that scales with AeroFlexx’s commercial success and the visibility it generates in the industry.

Refinity: Advanced chemical recycling at pilot validation stage

Refinity was launched in 2024 using fluidised-bed conversion technology licensed from VTT Technical Research Centre of Finland, supplemented by a collaboration agreement with The Dow Chemical Company. The technology converts minimally sorted, low-cost mixed plastic waste into drop-in chemical intermediaries, specifically olefin gases including ethylene and propylene, and hydrocarbon liquids such as naphtha substitutes, that feed directly into the existing petrochemical supply chain.

The design premise is that by accepting mixed plastic waste with minimal pre-sorting requirements and producing outputs that are directly compatible with existing crackers and polymerisation facilities, Refinity eliminates the two most significant commercial barriers to advanced chemical recycling: feedstock quality requirements and output integration costs.

The VTT technology has been validated at bench and pilot scale. Refinity disclosed in early 2026 that it had successfully demonstrated conversion of real-world plastic waste, producing one metric tonne of hydrocarbon outputs at yields in the sixty to seventy percent range with minimal char byproducts. The pilot demonstration used real mixed plastic waste rather than laboratory-grade feedstock, which is commercially significant: many advanced recycling technologies demonstrate attractive yields on clean, well-characterised feedstock but underperform when exposed to the contamination, variability, and composition uncertainty of real-world waste streams. The completion of a real-waste pilot validates the technology past one of the most common failure points in the advanced recycling development pathway.

Refinity has filed patent applications protecting proprietary reactor designs and is developing the engineering design for its first commercial demonstration, expected to be located at a partner facility. The Dow collaboration agreement provides a potential off-take pathway for Refinity’s output, though the agreement is not a binding purchase commitment and the economic terms are not publicly disclosed. The commercial demonstration engineering design is a necessary precursor to attracting the direct capital raise that Refinity requires to progress to commercial scale, and the timeline for that demonstration is not publicly committed.

The fundamental commercial risk for Refinity is the gap between pilot-scale validation and commercial-scale economics. Advanced chemical recycling technologies have a consistent historical pattern of demonstrating strong pilot performance that proves difficult to replicate at the throughput rates, feedstock variability conditions, and continuous operation requirements of commercial scale.

The fluidised-bed reactor technology at the core of Refinity’s process is an established industrial technology used in petroleum refining and petrochemical production, which provides more confidence in commercial scalability than technologies that require novel reactor engineering. However, applying fluidised-bed technology to mixed plastic waste, a feedstock with more variable composition and thermal properties than petroleum fractions, introduces engineering challenges that the pilot demonstration has partially but not fully resolved.

5. Capital Structure, Dilution Mechanics, and the Going-Concern Shadow

Innventure’s capital structure is the most material analytical variable for existing shareholders. The going-concern qualification, the SEPA with Yorkville, the S-3 shelf registration, the history of equity-funded operating losses, and the material weaknesses in internal controls collectively create a dilution and transparency risk profile that is central to any honest valuation assessment. Understanding the mechanics is the prerequisite for evaluating what a share of INV actually represents at any given trading price.

The going-concern qualification

Innventure’s auditors, WithumSmith+Brown PC, who replaced BDO as audit firm in Aug 2025, issued a going-concern explanatory paragraph in the FY2025 audit report. The qualification notes substantial doubt about the company’s ability to continue as a going concern without additional financing. The going-concern designation reflects the mathematical gap between the company’s operating cash consumption of approximately 80.7 million dollars in FY2025 and its year-end cash position of 65.4 million dollars, even accounting for the 40 million dollar registered direct offering completed in Jan 2026, the consolidated cash position provides a runway measured in months at 2025 burn rates.

The going-concern qualification has multiple consequences beyond the obvious solvency concern.

First, it complicates enterprise customer sales conversations: large data center operators and packaging brand owners conducting vendor due diligence now routinely request financial stability evidence, and a going-concern qualification requires active management in those conversations.

Second, it affects the terms on which Innventure can access capital markets, equity issuances during periods of going-concern uncertainty carry implicit discounts relative to issuances by financially stable companies, because investors require compensation for the risk of being diluted in a potential distress financing.

Third, it constrains the governance optionality available to management: pursuing a strategic transaction, a spin-off, or an alternative structure for one of the operating companies becomes more complex when the parent entity is operating under a going-concern qualification.

The Yorkville SEPA: Mechanics and dilution impact

The Standby Equity Purchase Agreement with YA II PN Ltd. (Yorkville) is the primary at-will dilution mechanism in Innventure’s capital structure. Under the SEPA, Innventure may from time to time request that Yorkville purchase newly issued shares at a price determined by either 95% of the daily volume-weighted average price during a one-day pricing period, or 97% of the lowest daily VWAP during a three-consecutive-trading-day pricing period, at Innventure’s election depending on the advance notice type submitted.

The mechanism is structurally dilutive because each draw issues shares at a discount to market, and the discount compounds across multiple draws over time. Shareholders who do not participate in the issuances experience proportional dilution in their ownership percentage without any compensating participation in the capital raised.

Approximately 66.6 million dollars of SEPA capacity remained available as of the most recent S-3 filing. This represents a significant source of additional capital but also a significant source of potential share supply. If Innventure draws the full remaining SEPA capacity at a market price near recent trading levels, the share count could increase by tens of millions of shares, representing a material dilution of existing shareholders.

The SEPA is not guaranteed, it is subject to conditions including that the shares issued do not exceed the exchange cap (generally 20% of outstanding shares without shareholder approval), but within those constraints, it represents a powerful tool for management to raise capital without requiring a formal underwritten offering or investor roadshow.

6. The Activist Dimension

The Commonwealth Asset Management Schedule 13D and the Ascent Capital investor letter represent two distinct but reinforcing shareholder pressure events that have pushed Innventure’s governance, capital allocation strategy, and management structure into public disclosure. The company’s response has been constructive rather than defensive, and several structural improvements have followed. Whether those improvements are sufficient to close the gap between asset value and equity value is the open governance question heading into the second half of 2026.

Commonwealth Asset Management filed a Schedule 13D in Feb 2026, disclosing ownership above the five percent disclosure threshold and signalling activist intent toward Innventure’s strategy and governance. Innventure responded with a formal statement reiterating its long-term value creation strategy and its commitment to engaging constructively with all shareholders. The response was measured and did not disclose the substance of Commonwealth’s communications, but the public statement and the subsequent governance announcements suggest that Commonwealth raised concerns about the pace of operating company self-sufficiency, the parent-level G&A burden, and the board’s independence composition.

A subsequent Schedule 13D/A from Ascent Capital contained a detailed investor letter arguing that Accelsius is the single best-managed pure-play public exposure to two-phase direct-to-chip liquid cooling available in the public markets and that the corporate structure, a pre-revenue conglomerate parent with a going-concern qualification, is the primary obstacle between the share price and the value of the Accelsius asset.

Ascent argued that the market is materially mispricing Innventure relative to the Accelsius Series B valuation, noting that if Accelsius alone carries a post-money valuation of 665 million dollars at the Series B, and Innventure’s market capitalisation has periodically traded below that level, the market is effectively attributing negative value to AeroFlexx, Refinity, and the platform itself, a position that is difficult to sustain if Accelsius is genuinely worth its Series B valuation.

The activist thesis implicit in both filings is the sum-of-parts discount: Innventure’s corporate structure is creating a holding company discount rather than a conglomerate premium, and the mechanism for closing that discount is either simplifying the structure or demonstrating commercial execution that reduces the parent-level risks that justify the discount. Innventure’s management has not publicly endorsed a structural simplification, the stated strategy remains to operate multiple companies within the conglomerate model and reach consolidated cash flow positivity by 2028, but the governance improvements announced in response to the activist engagement suggest that management understands the source of the discount and is taking addressable steps to reduce it.

7. Financial History and the Development-to-Revenue Transition

Innventure’s financial statements do not resemble those of a commercial-stage company because Innventure is not yet a commercial-stage company in any conventional sense. Separating the non-cash accounting events from the operating cash consumption, and understanding the specific drivers of each line item, is the prerequisite for forming a view on what the business actually costs to run and what trajectory it needs to follow to reach financial self-sufficiency.

Revenue: Early traction at pre-scale

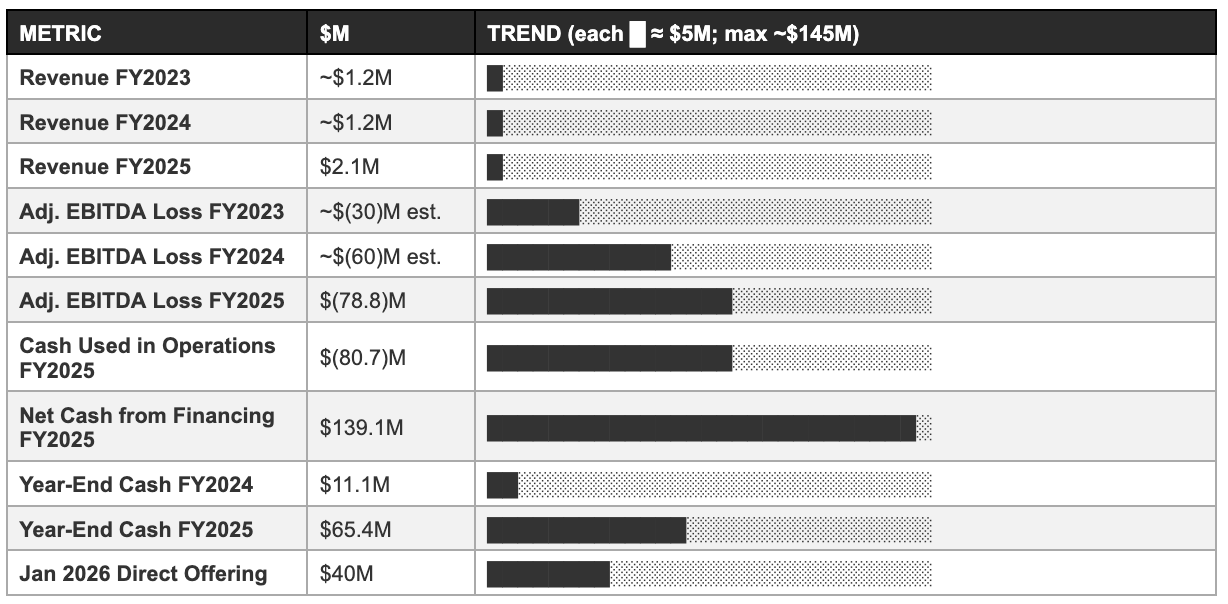

Total revenue grew from approximately 1.2 million dollars in FY2024 to 2.1 million dollars in FY2025, a 75% increase that reflects early commercial traction at Accelsius, where segment revenue grew 433% to 1.6 million dollars as the company transitioned from laboratory deployments to initial production orders, and continuing revenue from AeroFlexx. Refinity generated no revenue in FY2025 as it remains at the pre-commercial technology validation stage.

These figures are genuine commercial revenues recognised against delivered products and services; they are not bookings, pipeline, or pro-forma figures. They are also immaterial relative to the operating cost structure: 2.1 million dollars in revenue against a 78.8 million dollar adjusted EBITDA loss means that revenue is covering approximately 2.7 cents of every dollar of operating expenditure, a ratio that must improve dramatically, and that the 2026 Accelsius revenue ramp is designed to begin addressing.

The FY2025 net loss and the goodwill impairment

The reported net loss of 475.4 million dollars in FY2025 is dominated by the 346.6 million dollar non-cash goodwill impairment. Goodwill was created at the time of the deSPAC transaction when the difference between the transaction price and the fair value of Innventure LLC’s identifiable net assets was capitalised as goodwill on the consolidated balance sheet.

When Innventure’s market capitalisation subsequently declined to levels that implied the total enterprise was worth less than the carrying value of its net assets, a consequence of the post-deSPAC multiple compression that affected virtually all 2023 and 2024 vintage deSPAC listings, the accounting standards required that goodwill be written down to its implied recoverable value, generating the 346.6 million dollar charge. The impairment is a balance sheet accounting event, not a cash outflow, and it does not affect Innventure’s ability to fund operations or the underlying value of the operating companies. It is, however, an accurate accounting reflection of the premium that the deSPAC transaction valuation embedded above the operating companies’ demonstrated commercial value at the time of listing.

Stripping out the goodwill impairment, the operating loss in FY2025 was approximately 128.8 million dollars, which aligns with the adjusted EBITDA loss of 78.8 million dollars after adding back depreciation, amortisation, and stock-based compensation. The cash used in operating activities of 80.7 million dollars is the most relevant measure of actual cash consumption for runway calculation purposes: it captures the real cash flow from the business’s operating activities without non-cash items that do not affect the company’s solvency position.

Cash position, financing history, and runway

Innventure ended FY2025 with 65.4 million dollars in cash and restricted cash, up from 11.1 million dollars at year-end 2024, entirely because of 139.1 million dollars raised through financing activities during the year. The Jan 2026 registered direct offering added a further 40 million dollars. The cumulative financing since the company’s founding through various venture capital raises, operating company direct raises, and parent-level equity issuances has exceeded 240 million dollars directed into the operating companies, as management has disclosed.

At the parent level, the January 2026 offering and the SEPA together provide capital access that extends the runway, but each draw comes at a dilutive cost to existing shareholders.

At the FY2025 operating cash consumption rate of approximately 80.7 million dollars per year, the consolidated cash position at year-end 2025 plus the January 2026 offering of 40 million dollars provides approximately 13 to 15 months of runway at unchanged burn rates, extending into late 2026 or early 2027. The critical variable is whether the Accelsius revenue ramp, the G&A reductions, and the AeroFlexx and Refinity direct capital raises collectively reduce the parent-level burn rate sufficiently in 2026 to extend the runway without requiring further dilutive parent capital raises. If the base case execution trajectory materialises, the parent burn rate should decline materially in the second half of 2026 as Accelsius moves toward operating cash flow positivity and reduces its need for parent capital.

Revenue and EBITDA progression - Unicode bar chart

8. Regulatory Environment and ESG Tailwinds Across the Portfolio

Each of Innventure’s three operating companies operates in a market where regulation and corporate sustainability commitments are acting as demand accelerants independent of the companies’ own commercial efforts. The tailwind is not a guarantee of commercial success, but it does mean that the addressable market for each operating company is structurally expanding as a result of policy and procurement dynamics that Innventure does not control and does not need to fund.

Data center energy regulation and liquid cooling adoption

The regulatory environment for data center energy consumption has moved from a background concern to a near-term operational constraint in the United States and Europe. The European Union’s Energy Efficiency Directive, which entered into force in 2023, requires data centers above a certain size to report energy efficiency metrics and is expected to establish mandatory efficiency standards in subsequent implementing regulations.

The United States Department of Energy has been directed by executive order to assess data center energy consumption and develop efficiency standards, and several U.S. states, including Virginia, which hosts more data center capacity than any other U.S. jurisdiction, have enacted or are advancing legislation that links data center development permits to efficiency benchmarks.

The practical effect of these regulatory developments on liquid cooling adoption is direct: liquid cooling, particularly two-phase systems, achieves a Power Usage Effectiveness (PUE) ratio, the ratio of total data center energy consumption to the energy delivered to computing equipment, that is materially better than air-cooled facilities. A conventionally air-cooled data center typically achieves a PUE of 1.4 to 1.6, meaning that 40 to 60 cents of every dollar of energy expenditure goes to cooling rather than computing.

A two-phase direct-to-chip cooled facility can achieve PUE ratios approaching 1.02 to 1.05, meaning that nearly all energy goes to computing. As regulators establish PUE thresholds for new data center permits, the business case for liquid cooling transitions from a technical performance argument to a regulatory compliance requirement, a fundamentally more durable demand driver than performance preference alone.

The water consumption dimension reinforces the regulatory argument. Conventional air cooling with cooling towers consumes significant quantities of fresh water, a resource that is increasingly regulated in drought-prone regions. Accelsius’s dielectric two-phase system is a zero-water architecture: the dielectric coolant is a closed-loop system with no water consumption and no wastewater discharge. In jurisdictions where water consumption permits for data centers are becoming a binding constraint on development, a zero-water cooling architecture is a procurement advantage that goes beyond energy efficiency.

Plastic waste regulation and AeroFlexx / Refinity demand drivers

Both AeroFlexx and Refinity benefit from the accelerating global regulatory trend toward extended producer responsibility and recycled content mandates for plastic packaging. The European Union’s Packaging and Packaging Waste Regulation, which entered the legislative process in 2022 and is advancing toward implementation, establishes mandatory recycled content thresholds for plastic packaging and bans certain single-use plastic formats.

In the United States, four states (California, Colorado, Maine, and Oregon) have enacted extended producer responsibility legislation that places the cost of plastic waste management on producers, creating a direct economic incentive for brand owners to shift toward packaging formats with lower waste management cost implications.

For AeroFlexx, the regulatory trajectory is a demand accelerant: brand owners who face extended producer responsibility fees on rigid plastic packaging have a direct economic incentive to evaluate the AeroFlexx format’s plastic weight reduction and recyclability advantages as a cost management tool rather than purely as an environmental positioning choice. The shift from voluntary sustainability commitment to mandatory compliance cost changes the buyer’s decision calculus in AeroFlexx’s favour, particularly for brand owners in the household, personal care, and pet care categories that are most exposed to extended producer responsibility obligations.

For Refinity, the regulatory environment creates both demand for its outputs and policy support for its operations. Chemical recycling outputs, specifically the olefins and naphtha substitutes that Refinity’s process produces, qualify as recycled content under most regulatory frameworks that mandate recycled content in plastics, because they are derived from post-consumer plastic waste rather than virgin petroleum feedstock.

Brand owners who are required to incorporate a percentage of recycled content into their plastic packaging can satisfy that requirement by purchasing resins made from Refinity’s chemical recycling outputs. The Dow collaboration agreement, if it progresses to a binding off-take arrangement, would position Refinity’s outputs within Dow’s resin supply chain, a pathway from Refinity’s plastic waste inputs to brand owner packaging compliance at scale.

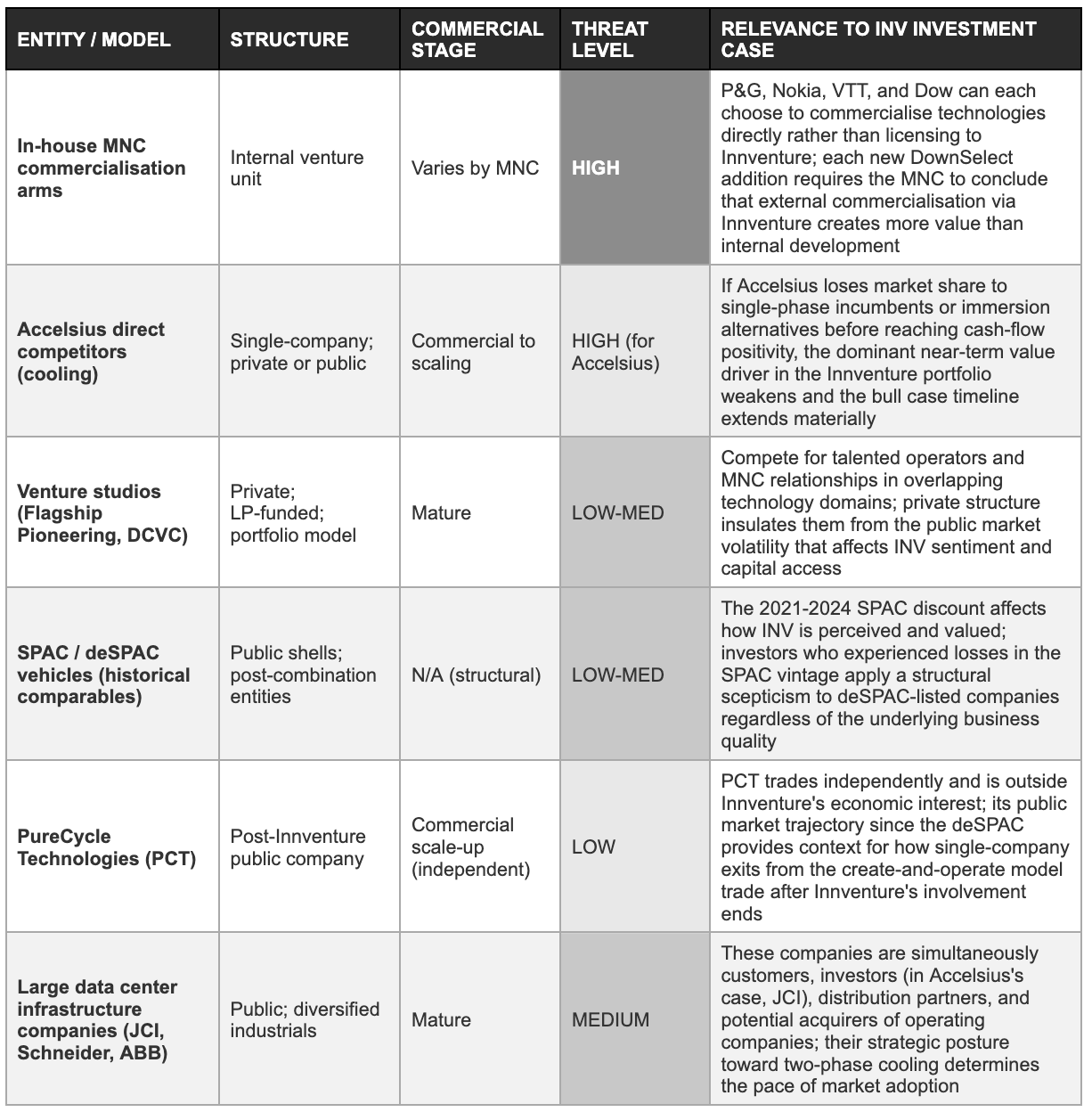

9. The Broader Competitive Landscape: Platform Comparables and Positioning

Innventure’s platform model, licensing MNC technology, seeding companies, and operating them toward independent public or private market exits, has no direct public market comparable. The closest reference points are industrial technology conglomerates, venture studios, and single-company pure plays in each operating company’s market. Each comparison illuminates a different aspect of how the equity should be priced.

At the platform level, Innventure describes itself as neither a venture studio nor a private equity roll-up, and the distinction is commercially important. The distinction from a venture studio is that Innventure sources technologies from established corporations rather than evaluating founder-generated pitches, a sourcing discipline that pre-filters for scientific validity at the cost of a slower pipeline cadence.

The distinction from private equity is that Innventure operates its portfolio companies as long-term assets rather than targeting return-of-capital events within a fixed fund timeline, which creates a different set of incentives for management and a different set of expectations for investors. Specifically, Innventure’s model is designed to allow operating companies to compound value over time rather than being sold at the earliest attractive opportunity, a positioning that management argues creates more value for shareholders but that requires patience from investors who are accustomed to private equity’s defined exit timelines.

Industrial conglomerates that operate multiple early-stage technology businesses simultaneously are typically private or subsidiary structures. There is no directly comparable publicly listed company that builds and operates early-stage industrial technology businesses across multiple sectors through a shared services model. This absence of comparables is both an opportunity and a risk: Innventure cannot benefit from comparable company multiple expansion, but it also cannot be anchored by comparable company multiple compression if its specific execution differentiates it from the general deSPAC or pre-revenue conglomerate category.

Platform-level competitive and structural assessment

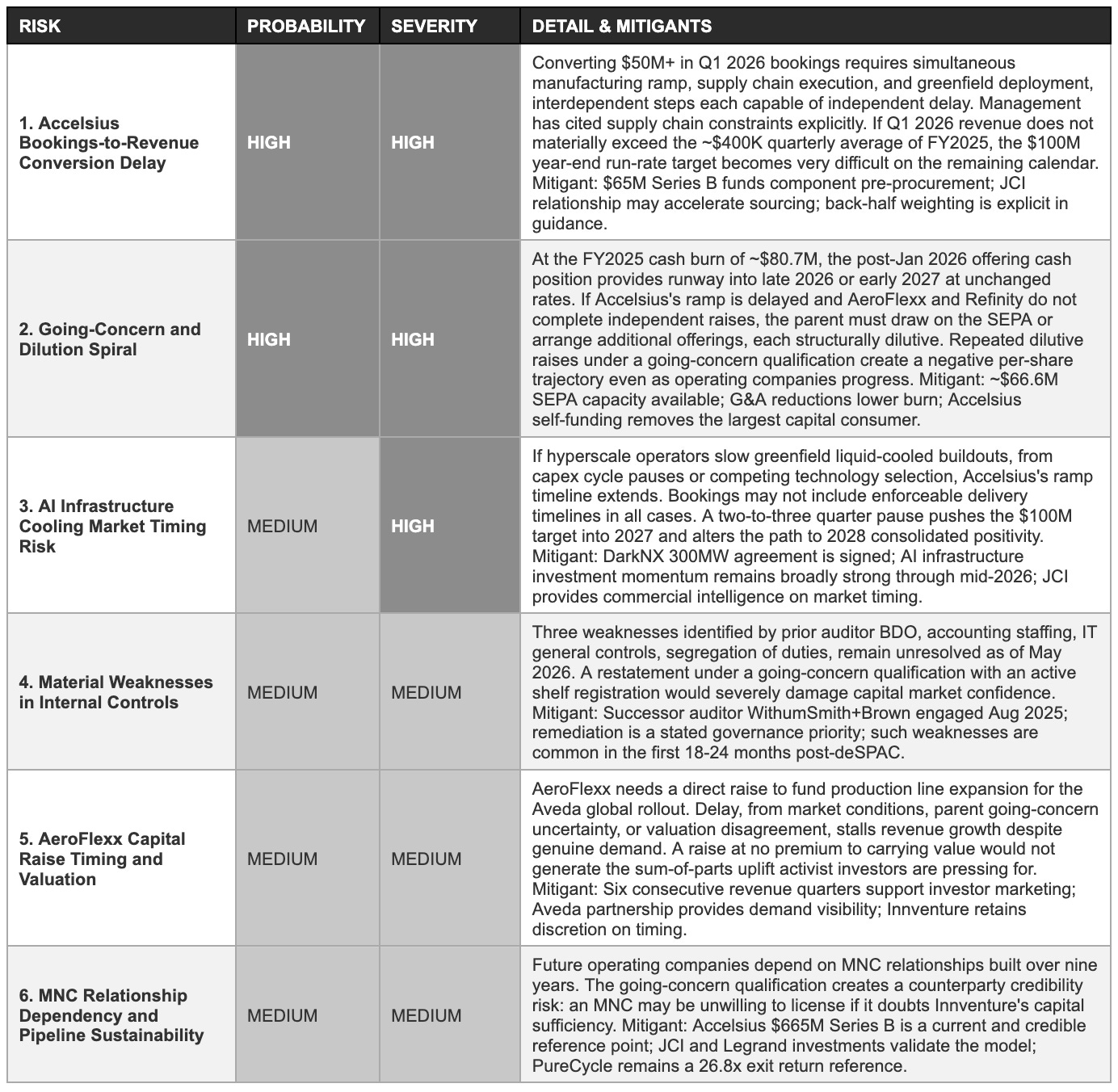

10. Risk Matrix

Each risk below identifies a specific variable whose resolution determines which of the three forward scenarios described in Section 10 materialises. Probability reflects the likelihood of a significant negative outcome within 24 months; severity reflects the degree of long-term impairment to the investment case if the risk materialises fully. Risks are ordered by the combined weight of both dimensions. Mitigants are presented where they exist, but the existence of a mitigant does not eliminate the risk, it defines the conditions under which the risk is bounded.

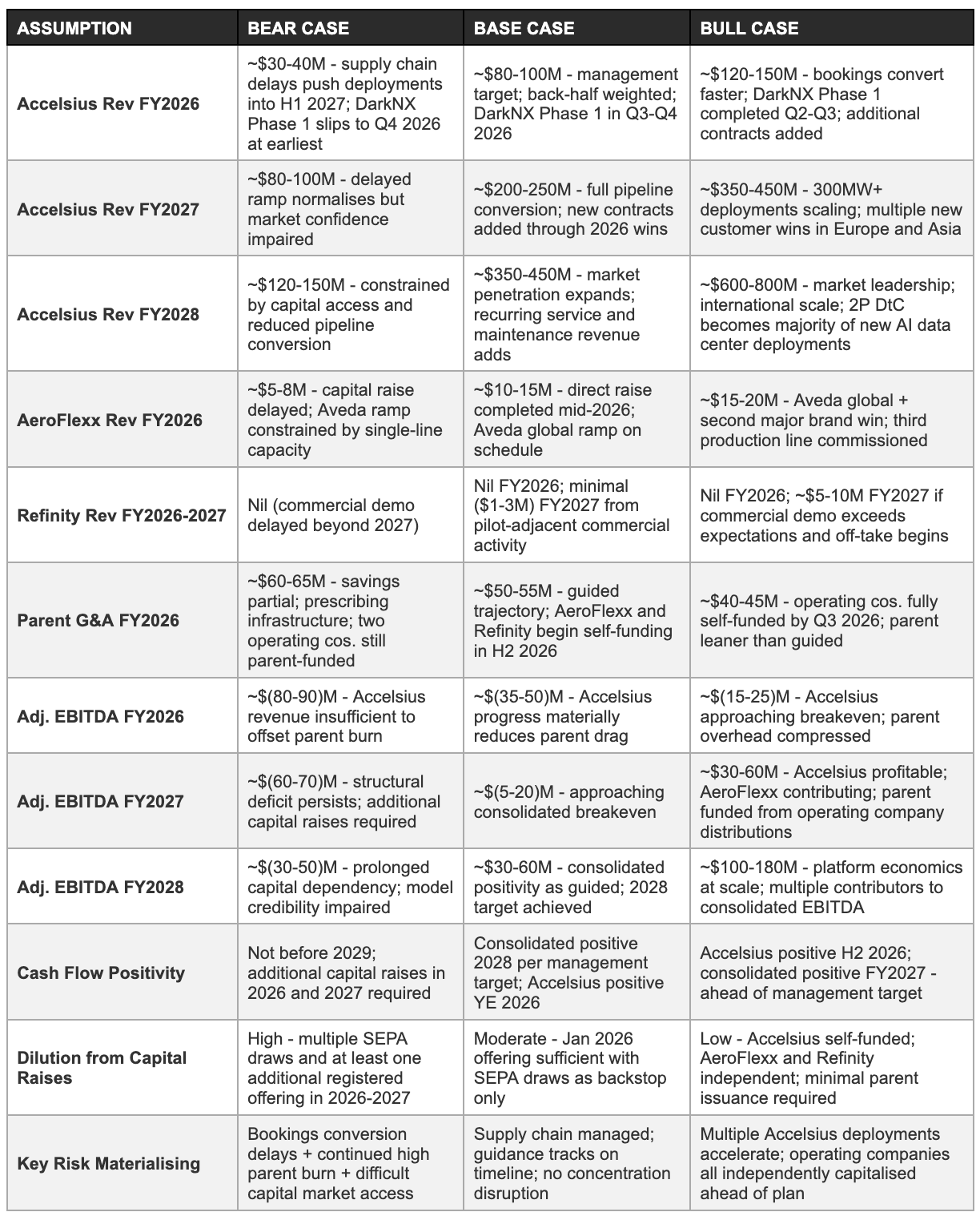

11. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios below are anchored to management’s disclosed targets, with the base case reflecting those targets, and then stress-tested against the two most important unresolved variables: Accelsius revenue conversion rate and parent-level cash consumption.

Model construction and key assumptions

The model is constructed in three layers. The Accelsius layer drives the majority of the revenue variance across scenarios and is the dominant variable in the consolidated outcome. The AeroFlexx layer is assumed to grow at rates consistent with production line capacity expansion, with the bear case reflecting a delayed capital raise and the bull case reflecting an accelerated Aveda global rollout.

The Refinity layer contributes no revenue in FY2026 across all scenarios and modest revenue in FY2027 only in the bull case, reflecting that commercial demonstration success and a direct capital raise are prerequisites for commercial revenue at Refinity. The parent G&A layer is modelled under three different compression trajectories depending on the pace of operating company self-sufficiency.

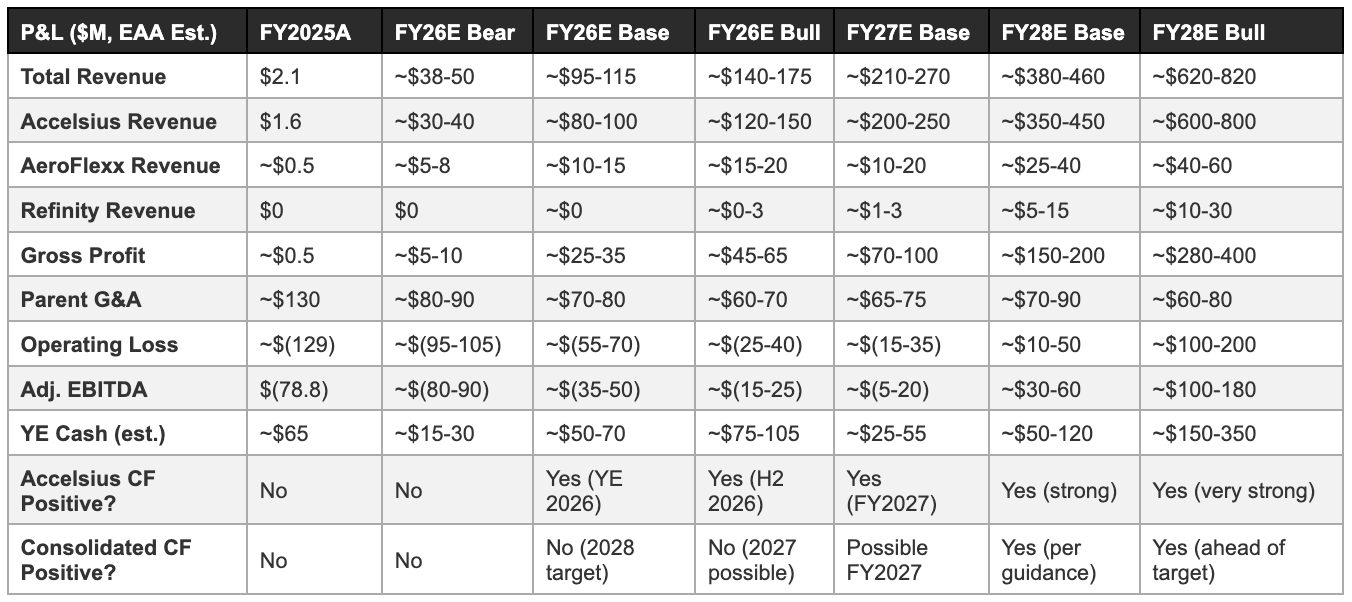

Three-year P&L projection

Valuation framework

Innventure’s equity cannot be valued through conventional earnings multiples at the current stage, the business has 2.1 million dollars in trailing revenue and a 78.8 million dollar adjusted EBITDA loss. Two frameworks apply: sum-of-the-parts, which applies the implied valuations of operating companies to Innventure’s ownership percentages and nets out parent-level obligations; and scenario-based forward enterprise value, which applies market multiples to projected FY2028 outcomes under each scenario.

The sum-of-the-parts framework uses the Accelsius Series B post-money valuation of 665 million dollars as the Accelsius mark, with Innventure’s ownership estimated at approximately 45 to 52% after the Series B dilution (the pre-Series B ownership of 52.7% disclosed in Mar 2025, reduced by the JCI and Legrand investment). Innventure’s attributable Accelsius value is therefore approximately 300 to 345 million dollars at the Series B mark.

AeroFlexx and Refinity have no recent third-party valuation events; assuming a modest combined holding value of 50 to 150 million dollars for the two businesses, and netting parent-level obligations including the accumulated deficit, the going-concern risk discount, and the dilution overhang, a sum-of-parts range of approximately 300 to 450 million dollars for the entire Innventure equity emerges. At the current trading range of approximately 500 to 600 million dollars in market capitalisation, the market is either implying a premium to the sum-of-parts, pricing in the option value of future operating company exits and the Accelsius growth trajectory, or the Series B valuation of 665 million dollars is itself being discounted by the market.

Forward scenario multiples: In the base case, FY2028 revenue of approximately 380 to 460 million dollars at a 3x to 5x revenue multiple (conservative for a company at early scale with ongoing cash burn reduction) implies an enterprise value range of roughly 1.1 to 2.3 billion dollars. After adjusting for projected cash position and ongoing dilution from capital raises, the per-share value in the base case scenario is materially above the current trading range.

In the bull case, FY2028 revenue of 620 to 820 million dollars with an approaching 20% EBITDA margin at a 5x to 8x revenue multiple implies an enterprise value of 3.1 to 6.6 billion dollars, a range that, net of capital structure adjustments, implies the $38 to $50 per share range cited by activist investors as their bull case target. In the bear case, a prolonged ramp delay and continued dilution could produce a per-share value at or below current levels by 2028, as the value created in operating companies is partially captured by successive equity issuances rather than compounding in the existing share count.

A third valuation reference is the implied milestone that current prices require Innventure to deliver. At a market capitalisation in the range of 500 to 600 million dollars, an investor purchasing today is implicitly asserting one of two things: either that Accelsius alone is worth approximately 300 to 350 million dollars at Innventure’s current ownership stake and that AeroFlexx, Refinity, and the platform are worth the balance; or that the sum of the three operating companies’ values, net of parent-level obligations, will compound to a level that justifies the current entry price over a three-to-five-year investment horizon.

The first assertion is supported by the Series B valuation mark. The second requires the base case or bull case execution trajectory to materialise. Investors who are buying the second assertion without modelling the bear case, in which dilution erodes the per-share value of even successful operating company outcomes, are underpricing a risk that is specific to the capital structure rather than to the operating companies’ commercial quality.

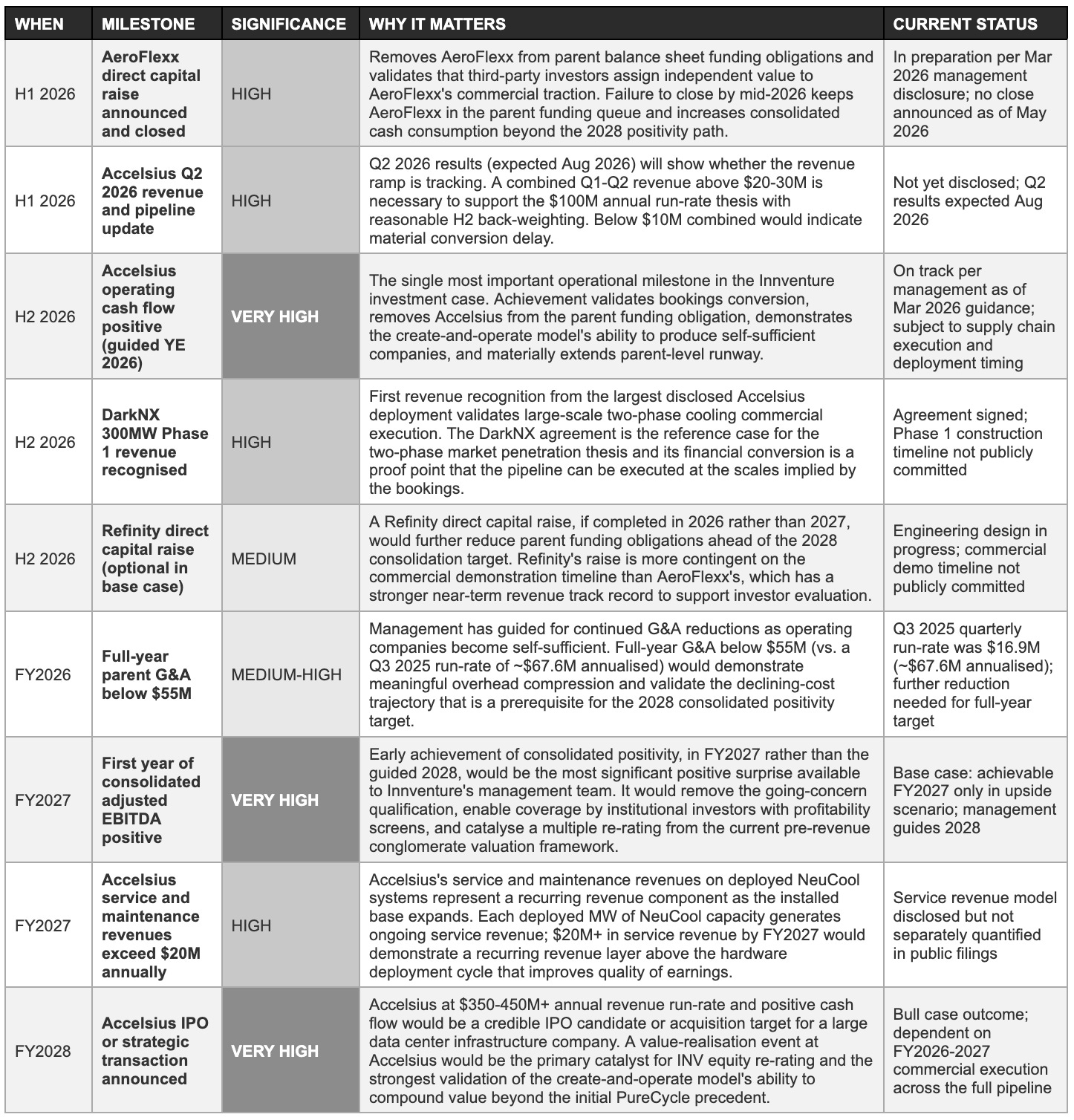

12. Milestone Tracker: What to Watch 2026-2028

Management’s three stated priorities for 2026, Accelsius cash flow positivity by year-end, AeroFlexx and Refinity direct capital formation, and parent G&A reduction, translate into a specific set of observable proof points.

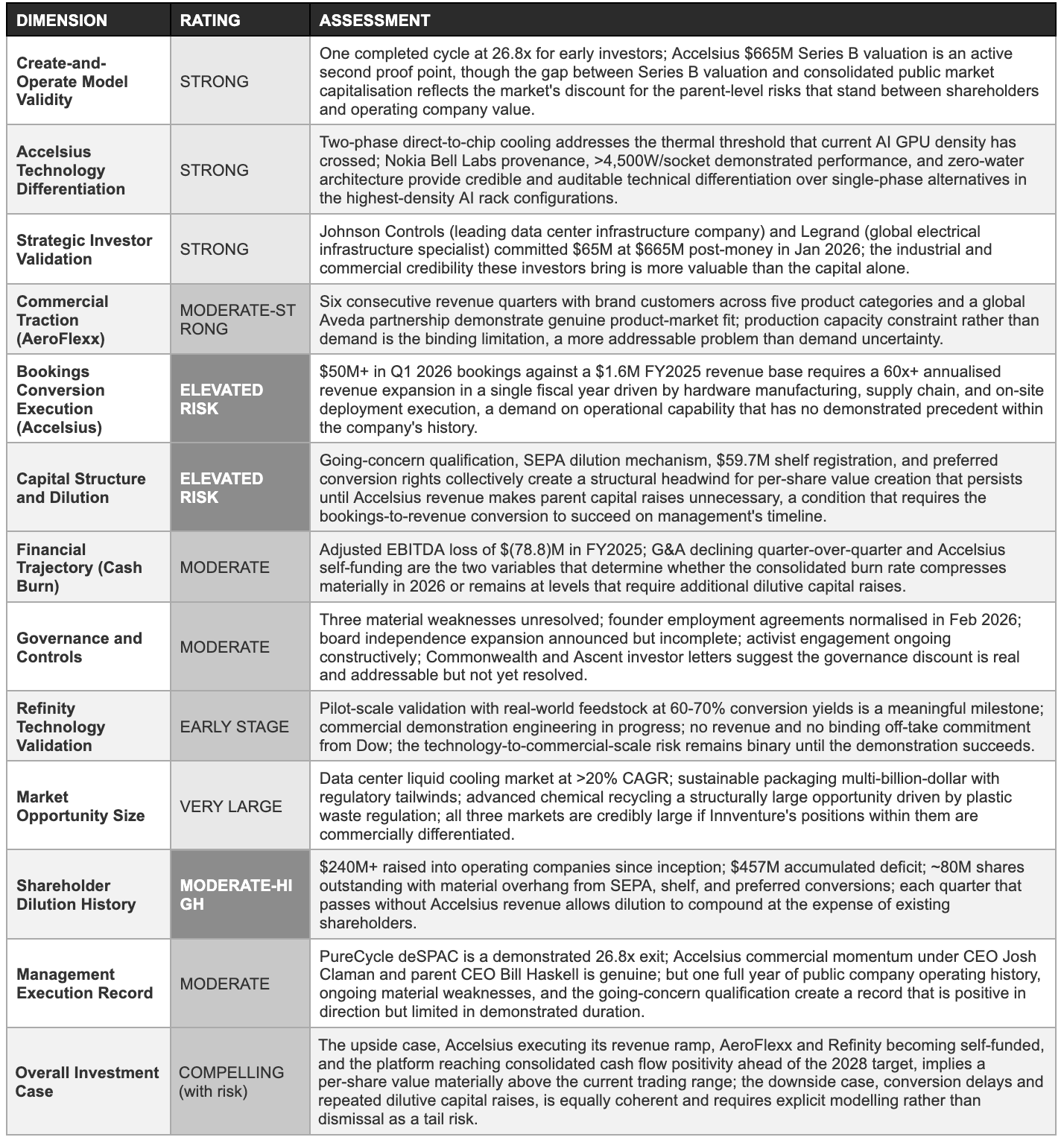

13. Investment Scorecard & Opinion: Bull, Base, and Bear Cases

What follows is our view as of May 2026, an attempt to present the bull, base, and bear cases with equal rigour and equal depth. The bear scenario has attracted serious market weight through the going-concern qualification, the deSPAC discount, and the pre-revenue financial profile, and it deserves the same depth as the bull case. The scorecard table summarises the multidimensional assessment; the following text explains why each case is internally coherent rather than presenting one as the obvious conclusion.

Investment scorecard

The bull case: What has to be true

The bull case requires a specific sequence of events to resolve favourably within 18 to 24 months. Accelsius must convert its $50 million-plus Q1 2026 bookings and the broader one-billion-dollar-plus pipeline into recognised revenue at a pace that supports the $100 million annual run-rate by year-end 2026 and operating cash flow positivity at the Accelsius subsidiary level by the same date. This is the primary requirement, without it, every other part of the bull case is contingent on a financial position that has not been validated.

The commercial conditions for this execution are present: the DarkNX 300 megawatt agreement is signed, the NeuCool MR250 and IR150 products are commercially available, Johnson Controls and Legrand have committed capital and commercial relationships that support deployment, and the thermal forcing function from AI infrastructure continues to drive demand independent of Innventure’s own commercial efforts.

The execution risk is therefore primarily internal, supply chain management, production capacity expansion, and deployment coordination, rather than demand-side. A hardware company with $50 million in committed bookings that fails to convert them typically does so because of operational capability gaps rather than because customers changed their minds.

AeroFlexx must complete its direct capital raise at a valuation that validates independent investor assessment of the business’s commercial value, and it must use that capital to fund the production line expansion required to honour the Aveda global commitment. Refinity must progress to commercial demonstration without requiring additional parent capital, a condition that is achievable if the engineering design for the commercial demonstration is completed and a partner facility is identified within 2026 as planned.

The parent G&A must compress from the current ~$67 million annualised run-rate to the $50-55 million range as operating companies self-fund, reducing the parent cash burn and extending the runway without requiring additional dilutive issuances. If all of these conditions are met, Innventure by FY2028 is a company with $380 to $460 million in consolidated revenue, approaching positive adjusted EBITDA, no going-concern qualification, and an Accelsius subsidiary that is approaching IPO or strategic transaction viability, a profile that would justify a material re-rating from the current valuation.

The bear case: What fails and why

The bear case is structurally coherent and should be given equal weight in any honest assessment. The core scenario is that Accelsius’s bookings conversion is slower than management has guided, not because the demand is absent, but because the manufacturing and supply chain execution challenge of moving from $1.6 million to $100 million-plus in a single fiscal year is as demanding as any comparable hardware company ramp in the data center infrastructure industry.

The most common failure mode for hardware companies at comparable growth velocities is not demand shortfall; it is the simultaneous complexity of scaling component procurement, production quality control, logistics, and field deployment engineering at an unprecedented pace.

In the bear case, Q1 2026 revenue is below $5 million, Q2 is below $15 million, and management updates its revenue outlook for FY2026 to a range well below the $100 million run-rate target. This disclosure, combined with the existing going-concern qualification, would create a sentiment spiral: the market would reduce its confidence in the bookings quality and the pipeline durability, share price would decline, the cost of equity capital through the SEPA and any additional offering would increase, and management’s ability to retain talent and execute commercial conversations would be impaired by the public disclosure of a significant miss against a highly visible target.

The parent would in the bear case be required to draw on the SEPA and potentially conduct an additional registered direct offering in the second half of 2026 to fund Accelsius’s continued scale-up investment and the parent-level overhead, generating further share dilution at a depressed price. AeroFlexx’s direct capital raise, attempted during a period of parent going-concern uncertainty and a high-profile Accelsius miss, would face investor scepticism that could delay or impair the process.

Refinity’s commercial demonstration timeline would slip as shared services resources are reprioritised. By FY2028, the consolidated result in the bear case is revenue of $120 to $150 million, real and growing commercial revenue, but a per-share value that has been diluted by several rounds of capital raises to the point where existing shareholders have experienced negative returns despite genuine operational progress at the operating company level.

The bottom line

Innventure at the current trading range represents an asymmetric bet on a specific execution sequence: Accelsius converting bookings to revenue, two operating companies becoming self-funded, and the parent overhead compressing as planned. Until bookings conversion is demonstrated in recognised revenue, not merely in pipeline disclosures, the investment case requires conviction in the execution thesis rather than confidence from demonstrated performance.

Sources

This report has been prepared using exclusively publicly available information as of May 2026. Primary sources: Innventure, Inc. Q4 and full-year 2025 earnings release (Mar 2026, Globe Newswire); Q4 2025 earnings slides (Mar 2026, Investing.com); FY2025 Form 10-K (Mar 2026, SEC EDGAR); Form 8-K going-concern and auditor change disclosure (Aug 2025, SEC EDGAR); Form S-1/A registration statement (Apr 2025, SEC EDGAR); Form DEF 14A proxy statement (May 2025, SEC EDGAR); Form S-3 shelf registration (Mar 2026, SEC EDGAR); Accelsius Series B closing press release (Jan 2026, BusinessWire/ir.innventure.com); Innventure Mar 2026 milestone and capital formation press release (Globe Newswire); Innventure statement on Commonwealth Asset Management 13D (Feb 2026, Globe Newswire/ir.innventure.com); Ascent Capital Schedule 13D/A investor letter (Apr 2026, SEC EDGAR); Innventure capital allocation strategy press release (Apr 2026, Globe Newswire); Q1 2026 results announcement date notice (May 2026, Globe Newswire); Accelsius NeuCool IR150 launch coverage (Apr 2026); Data Center Dynamics Accelsius Series B coverage (Feb 2026); Daily Political Roth conference coverage (Mar 2026); Innventure.com management profiles and company pages.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Innventure, Inc. (NASDAQ: INV) or any other security. All information is sourced from publicly available materials believed to be reliable as of May, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.