KOPIN CORPORATION

Two Businesses, One Ticker: A Forty-Year Defense Optics Manufacturer, a New AI-Infrastructure Equity Stake, and the Counterparty That Underwrites It

1. Corporate Profile & The Dual-Identity Thesis

Kopin trades as one ticker but is really two businesses: a forty-year defense optics manufacturer with audited revenue, and a nine-week-old AI equity stake that depends entirely on its counterparty’s credibility. This report treats them as separate questions.

Kopin Corporation supplies microdisplays and optical subassemblies to the United States and allied defense industrial base, a forty-year-old, sub-scale business that produced revenue of $39.3 million in 2025 against a market value that the same year’s results alone do not explain. The gap between the two is filled almost entirely by a single April 2026 announcement: a development collaboration and 19.9% equity stake in Fabric.AI, a company that was an electric-vehicle manufacturer nine months earlier and a stablecoin treasury vehicle five months before that.

This report treats the defense business and the Fabric.AI option as two separate questions, because the evidence supporting each is of a fundamentally different quality, and because the valuation embedded in the current share price depends overwhelmingly on the second question being answered correctly.

The defense business is the company’s core. Microdisplays manufactured by Kopin sit inside thermal weapon sights, pilot helmet-mounted display systems for fixed-wing and rotary-wing aircraft, armored vehicle targeting systems, and training and simulation headsets. Defense applications generated 74% of total revenue in FY 2025, and the company describes itself as a sole-source provider of microdisplays for several programs of record within the Department of War. This is decades-old commercial position. It is also a small one: fiscal 2025 revenue of $39.3 million places Kopin well below the scale of the prime contractors and even the mid-tier optics suppliers it serves, and the business has never, in any year reviewed for this report, generated a full year of profit.

The second business did not exist in its current form before April 2026. In late April 2026, Kopin announced a joint development and license agreement with Fabric.AI, then describing itself as a developer of fabless semiconductor technology for AI data-center infrastructure. Under the agreement, Kopin became the exclusive manufacturer of a jointly developed chip architecture called Neural I/o, intended to use Kopin’s MicroLED technology as an optical transceiver to replace copper wiring between graphics processing units inside AI data centers, and received a 19.9% equity stake in Fabric.AI in the process.

The announcement was followed within two trading sessions by a sustained increase in Kopin’s share price that has persisted, in varying degree, through the writing of this report in June 2026. Section 5 of this report addresses the Fabric.AI relationship in detail, including the history of the counterparty itself, which is relevant to any assessment of how much the 19.9% stake and the associated purchase order are actually worth.

Why this report splits the thesis in two

The defense business and the Fabric.AI option draw on different evidence bases, different time horizons, and different categories of risk, and an investor who is comfortable with one is not automatically comfortable with the other. A reader who wants exposure to a profitable, de-risked defense-optics supplier and a reader who wants exposure to a speculative AI-infrastructure call option are, in practice, evaluating two different securities that happen to share a ticker.

The defense business has four decades of operating history, audited financial statements, and a real, if concentrated, customer base. The Fabric.AI relationship has existed for less than two months as of this writing, generates no revenue recognized to date, and rests on a counterparty whose own corporate history over the preceding year consisted of an electric-vehicle business, then a stablecoin treasury strategy, then an AI semiconductor pivot announced the same week as the Kopin deal. Both facts are true. Reading this report requires holding both in mind at once, because the market price appears to be weighting the second fact far more heavily than its short history would normally justify.

Recent corporate history

Kopin’s recent history is one of repeated strategic resets. In 2023, the company launched what it called the ONE Kopin initiative, consolidating its operating subsidiaries, including Forth Dimension Displays and NVIS, under the unified Kopin brand to reduce redundancy and direct resources toward European and Southeast Asian defense markets.

Beginning in mid-2025, Kopin entered a period of unusually dense corporate activity. In August 2025, it announced a $15 million strategic investment from Theon International, a European maker of night-vision and thermal-imaging systems, comprising an $8 million purchase of a 49% stake in Kopin’s Scottish subsidiary and a $7 million purchase of convertible preferred stock. In September 2025, it closed a $41 million private placement that brought in Theon, Ondas Holdings, and Unusual Machines as strategic investors alongside institutional buyers. Through the back half of 2025 and into 2026, the company layered on additional transactions: a full exit from its Lightning Silicon Technology and Lightning Silicon America joint ventures completed in June 2026, the April 2026 Fabric.AI collaboration, and a May 2026 conversion of Theon’s preferred stock into common shares.

Each transaction is individually explicable. Taken together, they describe a company simplifying its capital structure in some areas while adding meaningful new complexity in others, within a span of less than twelve months.

2. The Core Defense Business: Products, Customers, Concentration & Order Book

Strip away the Fabric.AI announcement and Kopin is a small, concentrated, intermittently profitable optics supplier. The question here is whether the customer base underneath it is diversified enough to stand on its own.

Product lines and end markets

Kopin’s product portfolio breaks into two layers.

The first is the microdisplay itself: a postage-stamp-sized screen built on one of four technology bases, active-matrix liquid crystal, ferroelectric liquid crystal on silicon, organic light-emitting diode, or the newer MicroLED architecture, each suited to different combinations of brightness, power draw, resolution, and operating temperature range.

The second layer is the Application Specific Optical Solution, the lenses, housings, electronics, and image-processing components that turn a microdisplay into a finished subsystem a customer can integrate into a weapon sight, a helmet, or a headset. Kopin sells at both layers: as a component supplier to systems integrators, and increasingly, through programs such as the Theon DarkWAVE collaboration, as a subsystem partner that takes more of the finished product’s value.

Defense applications, principally thermal weapon sights, pilot helmet-mounted display systems for fixed-wing and rotary-wing aircraft, and armored vehicle targeting systems, generated 74% of total revenue in fiscal 2025 (10-K, filed 2026). The remaining revenue is split across training and simulation systems, industrial and medical headsets, three-dimensional optical inspection equipment, and a small, currently immaterial, consumer augmented and virtual reality component business.

Customer concentration: The central near-term risk

Kopin’s 10-K for fiscal year 2025 disclosed that one customer accounted for 63% of total revenue for the year. This is concentration at a level rarely seen even among small defense subcontractors, and it sits alongside the 74% defense-segment concentration described above; the two figures together describe a revenue base that depends, in large part, on the continuation, funding level, and procurement pace of a small number of programs run through a single prime relationship.

The document also disclosed unresolved material weaknesses in internal control over financial reporting as of year-end 2025, with remediation work continuing into 2026, a limitation on the reliability of reported figures that this report flags here and carries into the risk matrix in Section 8 rather than treating as a separate topic.

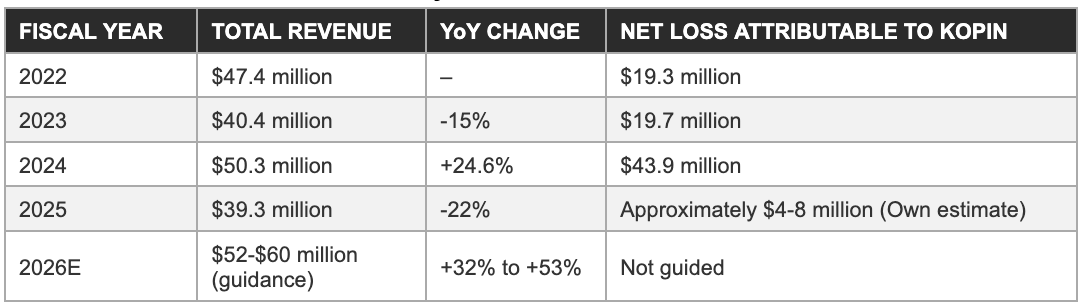

The consequence of this concentration showed up directly in the fiscal 2025 results. Fourth-quarter 2025 revenue fell to $8.4 million from $14.6 million in the prior-year quarter, a decline management attributed to a government shutdown and the associated procurement delays that affected the timing of program orders, product shipments, and contract activity across the defense industrial base generally, not specific to Kopin (fourth-quarter 2025 earnings release, March 2026). Full-year 2025 revenue of $39.3 million was accordingly 22% below the $50.3 million reported in 2024, reversing two consecutive years of growth.

The explanation is plausible and consistent with what other small defense suppliers reported over the same period, but it also demonstrates exactly the vulnerability that concentrated, program-dependent revenue creates: a delay affecting one or two customers’ procurement calendars is enough to move Kopin’s full-year results by more than twenty percentage points.

A single customer representing 63% of revenue, combined with a defense segment representing 74% of revenue, means that Kopin’s near-term financial outcomes are determined less by the breadth of its addressable market and more by the procurement calendar, budget cycle, and continued goodwill of a small number of counterparties. The order momentum described later in this section is real, but it does not yet change this underlying structure.

Theon International: A diversification vector

The relationship with Theon International, a night-vision and thermal-imaging systems manufacturer listed on Euronext Amsterdam, is the clearest evidence that Kopin’s customer base is beginning to diversify outward from its historical reliance on the United States defense market. The original August 2025 agreement gave Theon a 49% stake in Kopin’s Scottish subsidiary for $8 million and $7 million of convertible preferred stock paying a 4% annual dividend, convertible into common stock at $3.00 per share.

The companies have since moved from a financial relationship into a commercial one: a $1 million initial DarkWAVE development order announced in the first quarter of 2026 is intended to bring a 960p OLED module to production readiness for Theon’s DARK-I night-vision platform, which management has described as addressing an installed base of approximately two million standard night-vision goggles (first-quarter 2026 earnings release, May 2026). In May 2026, Theon converted the entirety of its preferred stock into 2,380,973 common shares at the fixed $3.00 conversion price, retiring the preferred class and converting what had been a yield-bearing instrument into straightforward common equity exposure.

Theon is, by the standard this report applies throughout, a genuine counterparty: it is an operating manufacturer with its own decades of commercial history in night vision and thermal imaging, and its investment and order flow into Kopin are commercial transactions between two established businesses rather than a speculative cross-holding between two recently repositioned companies. Section 6 of this report returns to Theon specifically as a point of contrast against the Fabric.AI relationship discussed in Section 5.

Order book and recent program momentum

Order flow through the first quarter of 2026 and the weeks following it has been the strongest in recent memory by management’s own characterization, and the underlying contracts are disclosed with enough specificity to be evaluated individually rather than taken purely on management’s word.

A $21.5 million follow-on production contract for thermal-imaging eyepiece assemblies, awarded by a major United States defense prime after quarter-end, is the largest single award and continues an existing production relationship rather than opening a new one.

A $3.2 million initial order for the Sentinel FPV product, a first-person-view drone display system featuring what the company calls Dual Situational Awareness, formally opens a new market segment, first-person-view drones, with a stated potential for as many as 40,000 units by the end of 2028 if the program scales; that scaling is explicitly described as potential rather than contracted. European helmet-mounted display orders added more than $5 million across a Tier-1 production order and an advanced avionic order for a rotary-wing platform.

A Phase I Small Business Innovation Research award from the United States Army, the second MicroLED-focused federal award in six months and building on a $15.4 million Industrial Base Analysis and Sustainment contract from September 2025, funds further development of full-color, smaller-format MicroLED displays for soldier-borne applications.

Combined, these awards total approximately $31 million of disclosed new and follow-on business across the first quarter of 2026 and the weeks immediately following it. That figure is meaningful relative to a company with $39.3 million of total 2025 revenue, and it lends support to management’s reiterated 2026 guidance range of $52 to $60 million. It is also, by construction, a collection of relatively small individual awards rather than a single program win that would materially change the concentration profile described above; the $21.5 million thermal-imaging contract, the largest of the group, extends an existing relationship rather than diversifying away from it.

Several of the company’s defense contracts are structured as indefinite-delivery, indefinite-quantity vehicles, which management has characterized as offering uncapped revenue potential tied to demand through 2030; this structure provides genuine multi-year visibility into the existence of a program, but it does not commit a specific dollar volume of orders, so it should be read as a favorable contracting structure rather than a guaranteed revenue stream.

Manufacturing footprint and the made-in-USA argument

Kopin manufactures in the United States and in Scotland, and management has placed increasing emphasis on domestic manufacturing as a competitive and regulatory advantage, particularly as it pursues AI-infrastructure applications that the company says are subject to government and Department of War procurement rules requiring domestic manufacture. In the first quarter of 2026, the company announced a commitment to bring full-scale OLED microdisplay manufacturing in-house at its Westborough, Massachusetts headquarters, funded in part by an Industrial Base Analysis and Sustainment award, with capital expenditure guided at approximately $5 million in each of 2026 and 2027.

This in-house buildout follows directly from the June 2026 termination of Kopin’s prior OLED licensing and services relationship with Lightning Silicon Technology, discussed further in Section 4; Kopin retained a perpetual, royalty-free license to certain Lightning Silicon OLED microdisplay technology as part of that exit, alongside a limited royalty obligation of $7.50 per display on certain orders secured between April and October 2026. The domestic-manufacturing argument is real and is likely to matter more, not less, as defense and government AI-infrastructure procurement rules tighten, but it is also a capital commitment layered on top of a business that used $15.5 million of cash in operations in 2025, a point this report carries into Section 4.

3. Financial History, Capital Structure & Dilution

Kopin has not produced a profitable full fiscal year in any period covered by this report, and it has financed the resulting cash consumption almost entirely through the sale of new shares. The share count has roughly doubled since 2022. This section sets out the revenue and loss history, the financing history that sits behind it, and what the resulting capital structure means for an investor evaluating the stock today.

Five-year revenue and loss history

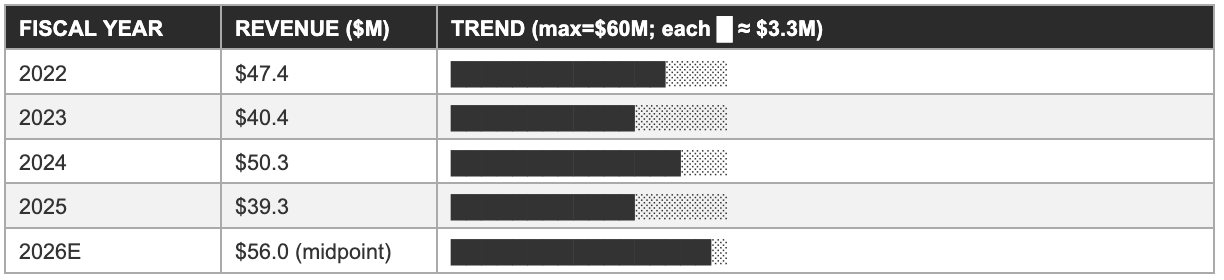

Revenue has moved in a narrow band with no clear multi-year trend: $47.4 million in 2022, $40.4 million in 2023, $50.3 million in 2024, and $39.3 million in 2025, before a guided recovery to $52 to $60 million in 2026. Net losses have been considerably more volatile than revenue, driven by non-recurring items including the $24.8 million litigation reserve recognized in the first quarter of 2024 and a $4.1 million quarter of net income recorded in the third quarter of 2025, itself driven substantially by non-operating gains on investments rather than core operating profitability.

The 2024 net loss is the figure most likely to mislead a reader who does not adjust for the litigation reserve. Excluding the $24.8 million reserve recognized in the first quarter of 2024, the year’s underlying loss would have been roughly comparable to 2023’s $19.7 million, consistent with a business narrowing its losses gradually rather than one that deteriorated meaningfully in 2024. The reserve itself related to a multi-year legal dispute that has since been resolved and is not, on the evidence available, expected to recur, but it is a useful reminder that single-year net loss figures at a company this size can be moved by tens of millions of dollars by one item unrelated to ongoing operations.

Quarterly Pattern Through Early 2026

The quarterly cadence through 2025 and into the first quarter of 2026 illustrates both the litigation-related distortion described above and the underlying volatility in product margins. The first quarter of 2025 produced a $3.1 million net loss, the second quarter a $5.2 million net loss, the third quarter a $4.1 million net income driven by non-operating investment gains, and the fourth quarter a return to a net loss alongside revenue of only $8.4 million as government-shutdown-related procurement delays compressed shipments.

The first quarter of 2026 produced revenue of $10.6 million, essentially flat against the first quarter of 2025’s $10.5 million, and a net loss of $3.8 million, with product revenue of $5.4 million more than offset on the cost side: cost of product revenue equaled approximately 103% of product sales in the quarter, meaning the product business alone operated at a negative margin before accounting for grant income, collaboration revenue, and non-operating gains that brought the consolidated result to a smaller net loss (first-quarter 2026 10-Q, May 2026).

A negative product gross margin in the most recently reported quarter is a meaningful data point on its own, independent of any one-time items elsewhere in the income statement. It indicates that, at current shipment volumes, the core defense optics business is not covering its direct production costs without the benefit of grant income, license fees, and investment gains. Whether the order momentum described in Section 2 restores positive product margins through volume and fixed-cost absorption, as management expects, is a near-term and observable test of the recovery thesis.

Cash position and operating cash use

Kopin ended fiscal 2025 with $61.6 million of cash, cash equivalents, restricted cash, and marketable securities, up from $36.6 million a year earlier, an increase driven almost entirely by financing activity rather than operations (10-K, filed 2026). Net cash used in operating activities was $15.5 million in 2025 and $14.2 million in 2024, meaning the business has consumed broadly similar amounts of cash in operations across both years regardless of whether revenue grew or declined. A

s of the end of the first quarter of 2026, cash and cash equivalents stood at $34.1 million, with an additional $25.3 million of restricted cash, of which $23.0 million secures obligations related to the company’s strategic partnership and financing transactions, for a combined cash, restricted cash, and marketable securities position of approximately $59.5 million (first-quarter 2026 10-Q, May 2026). At the 2025 rate of operating cash consumption, this position provides on the order of three to four years of runway if cash use does not increase, though the company has stated its intention to invest further in OLED manufacturing capacity and in the Fabric.AI collaboration, either of which could shorten that runway.

The dilution history

Kopin has financed its operating cash needs primarily through the sale of new equity, and the share count reflects this clearly. Weighted-average shares outstanding were approximately 91 million in 2022, rose to approximately 110 million by mid-2023, reached approximately 133 million across full-year 2024, and stood at 166 million in the first quarter of 2025 before reaching 187 million in the first quarter of 2026. The most recently disclosed share count outside this quarterly series was approximately 185.3 million as of June 2026.

Two financings completed in 2025 illustrate both the recurring need for capital and the volatility of the price at which that capital has been raised: a public offering of 43.0 million shares of common stock and pre-funded warrants that generated gross proceeds of $33.9 million at $0.65 per share, and a private placement that generated approximately $38.1 million of net proceeds from 19,545,950 shares at $2.10 per share. A shareholder who held stock through both transactions absorbed dilution at a price roughly one-third of the level the second raise commanded only months later, a sequencing that reflects how quickly sentiment toward the stock changed across 2025 rather than any change in the underlying business between the two raises.

4. Fabric.AI and the Neural I/o Opportunity: Counterparty Quality and Technology Realism

Nearly all of Kopin’s re-rating since the announcement traces to one counterparty. Before crediting the technology, this section asks who Fabric.AI actually is and what it has actually committed to pay.

The counterparty’s history

The company now known as Fabric.AI was, as recently as the third quarter of 2025, an electric-vehicle manufacturer trading under a different name and a different ticker, with a market capitalization in the low single-digit millions of dollars. In August 2025, the company rebranded around a stablecoin and digital-asset treasury strategy, adopting the StableX name and ticker and shifting its stated business purpose toward holding and deploying stablecoin-linked assets.

That positioning lasted roughly eight months. In late April 2026, the same week Kopin announced the joint development and license agreement, the company rebranded a second time, to Fabric.AI, adopting an AI semiconductor and data-center infrastructure narrative built substantially around the Neural I/o collaboration with Kopin itself. In other words, the counterparty’s current identity, the one underwriting roughly $5 million of confirmed near-term payments and up to $15 million of contingent development funding to Kopin, was created in the same announcement that created the obligation.

A company that was an electric-vehicle maker nine months before this report, a stablecoin treasury vehicle five months before this report, and an AI semiconductor developer as of the announcement itself is not, by any conventional standard, an established counterparty with an independent track record of execution in the field it now claims to operate in. This is not a judgment about whether the underlying chip architecture can work; it is a statement about how much weight the counterparty’s name, balance sheet, and announced intentions should carry on their own, separate from Kopin’s own engineering credibility.

What was agreed

Press coverage of the announcement widely described a “$15 million order” from Fabric.AI to Kopin. The underlying disclosure in Kopin’s SEC filings is more precise and, in one respect, more modest: an initial purchase order of $5 million, payable within ten business days of the joint development agreement’s execution, and a separate pool of up to $15 million in milestone-contingent Development Funds, payable through Fabric.AI as Kopin achieves at least one Successful Demo under the agreement, a defined term whose specific technical criteria were not disclosed in the filings reviewed for this report.

The distinction here is important: $5 million is a confirmed, near-term cash commitment; the additional $15 million is a ceiling on contingent funding tied to milestones that have not yet been defined publicly in enough detail to assess how achievable or how distant they are. Kopin separately received a 19.9% equity stake in Fabric.AI as part of the arrangement, a stake whose value is a direct function of Fabric.AI’s own market value, which itself is a function almost entirely of the same Neural I/o narrative.

This creates a circularity worth naming plainly. Kopin’s equity stake in Fabric.AI is valuable to the extent the market believes the Neural I/o collaboration will succeed, and the market’s belief in the collaboration’s prospects is itself heavily informed by Kopin’s own public statements about the collaboration. The two companies’ valuations have, since the announcement, moved together on the same set of disclosures, an arrangement that can be entirely legitimate as a structuring choice and can also amplify shared upside and shared downside in a way a simple cash sale would not.

The technology: What Neural I/o proposes

Neural I/o is described as an optical interconnect architecture that uses Kopin’s MicroLED arrays as light-emitting transceivers to move data between graphics processing units inside an AI data center, in place of the copper wiring and, in more advanced rack designs, the silicon-photonics transceivers that are the current state of the art. The underlying physics is not exotic: MicroLEDs can be modulated quickly enough to carry data, and using light rather than copper to move data over short distances inside a data center is a well-established general direction across the optical interconnect industry, discussed further in Section 7.

What is novel, if it works as described, is using a microdisplay manufacturer’s existing MicroLED fabrication base, built for soldier-worn displays and helmet optics, as the foundation for a data-center interconnect product, an application several steps removed from anything Kopin has previously commercialized at scale.

No independent third-party validation of Neural I/o’s performance, power efficiency, or manufacturing yield at data-center-relevant volumes was identified in the sources reviewed for this report. The company’s own disclosures describe a development program working toward a demonstration, not a shipped or independently benchmarked product. This is normal for a program at this stage, and it is also the central reason the technology should be assessed as an early-stage development effort rather than a proven commercial capability, regardless of how the share price has already responded to the announcement.

Why the counterparty question cannot be separated from the Technology Question

An investor evaluating Neural I/o purely as an engineering question, can this MicroLED architecture move data fast enough and cheaply enough to compete with copper and silicon photonics, is asking a different question than an investor evaluating Fabric.AI as a commercial partner, does this counterparty have the balance sheet, customer relationships, and execution history to turn a development agreement into recurring, scaled revenue for Kopin.

The first question may eventually be answered favorably through Kopin’s own engineering work and the demonstration milestones referenced in the agreement. The second question, on the evidence available as of this report, points toward a counterparty with no independent operating history in AI semiconductors, no disclosed customer relationships of its own with data-center operators or hyperscalers, and a balance sheet built around the very announcement under discussion rather than around prior commercial success.

A favorable answer to the first question does not automatically produce a favorable answer to the second, because Fabric.AI would still need to secure its own customers, financing, and execution capacity to convert a successful Kopin-built demonstration into the kind of volume that would make the up-to-$15 million Development Funds, let alone any larger follow-on order, a reality rather than a ceiling that is never reached.

None of this means the collaboration is worthless or that it should be dismissed; Kopin’s own MicroLED fabrication capability and decades of optical-systems manufacturing experience are real, transferable assets, and the $5 million initial purchase order is a confirmed, near-term cash receipt regardless of what happens afterward. The point of this section is narrower and, in this report’s view, more useful: the substantial increase in Kopin’s enterprise value since April 2026 has been driven by a counterparty whose own history, examined directly, should lower rather than raise the confidence an investor places in the larger, contingent, and longer-dated parts of the announced relationship.

5. Theon International: A contrast case in counterparty quality

Kopin’s relationship with Theon International is useful to this report mainly for its small scale and its contrast value: it sits inside the same set of 2025 and 2026 strategic transactions as the Fabric.AI relationship while looking almost nothing like it on the dimension that matters most, the independent, verifiable history of the counterparty itself.

Theon International is a manufacturer of night-vision and thermal-imaging systems for military and security customers, listed on Euronext Amsterdam, with its own multi-decade operating history, audited financial statements, and an existing customer base of European and allied militaries independent of any relationship with Kopin. When Theon committed capital to Kopin, $8 million for a 49% stake in Kopin’s Scottish subsidiary and $7 million for convertible preferred stock in August 2025, it did so as an established operating company deploying capital from its own balance sheet into a complementary supplier, the kind of strategic-investor transaction that is common and generally constructive across the defense industrial base.

The subsequent commercial order flow, beginning with the DarkWAVE development order for Theon’s DARK-I night-vision platform, follows the same pattern: a real product, a real installed base of approximately two million standard night-vision goggles that the new module is intended to address, and a counterparty whose ability to pay and to place follow-on orders does not depend on the success of the announcement that created the relationship in the first place.

The test this report applies throughout is simple: would this counterparty exist, in roughly its current form, with roughly its current balance sheet, if the relationship with Kopin had never been announced. For Theon, the answer is clearly yes; Theon was a substantial, listed night-vision manufacturer before any Kopin transaction and remains one regardless of how the Kopin relationship develops.

For Fabric.AI, examined in Section 4, the answer is no; the entity in its current form, under its current name, with its current narrative, came into existence in the same announcement that created the financial relationship with Kopin. The contrast does not make the Fabric.AI relationship illegitimate, but it does mean the two relationships should not be assigned the same confidence level simply because both appear as line items in the same set of 2025 and 2026 disclosures.

6. Competitive Landscape: Microdisplays

In its core business, Kopin is a credible but sub-scale player in a market run by far larger consumer-electronics companies. Its edge is accreditation and program history, not unique technology.

The microdisplay market spans consumer virtual and augmented reality headsets, industrial and medical imaging, and defense and security optics, and the competitive set differs meaningfully across those end markets.

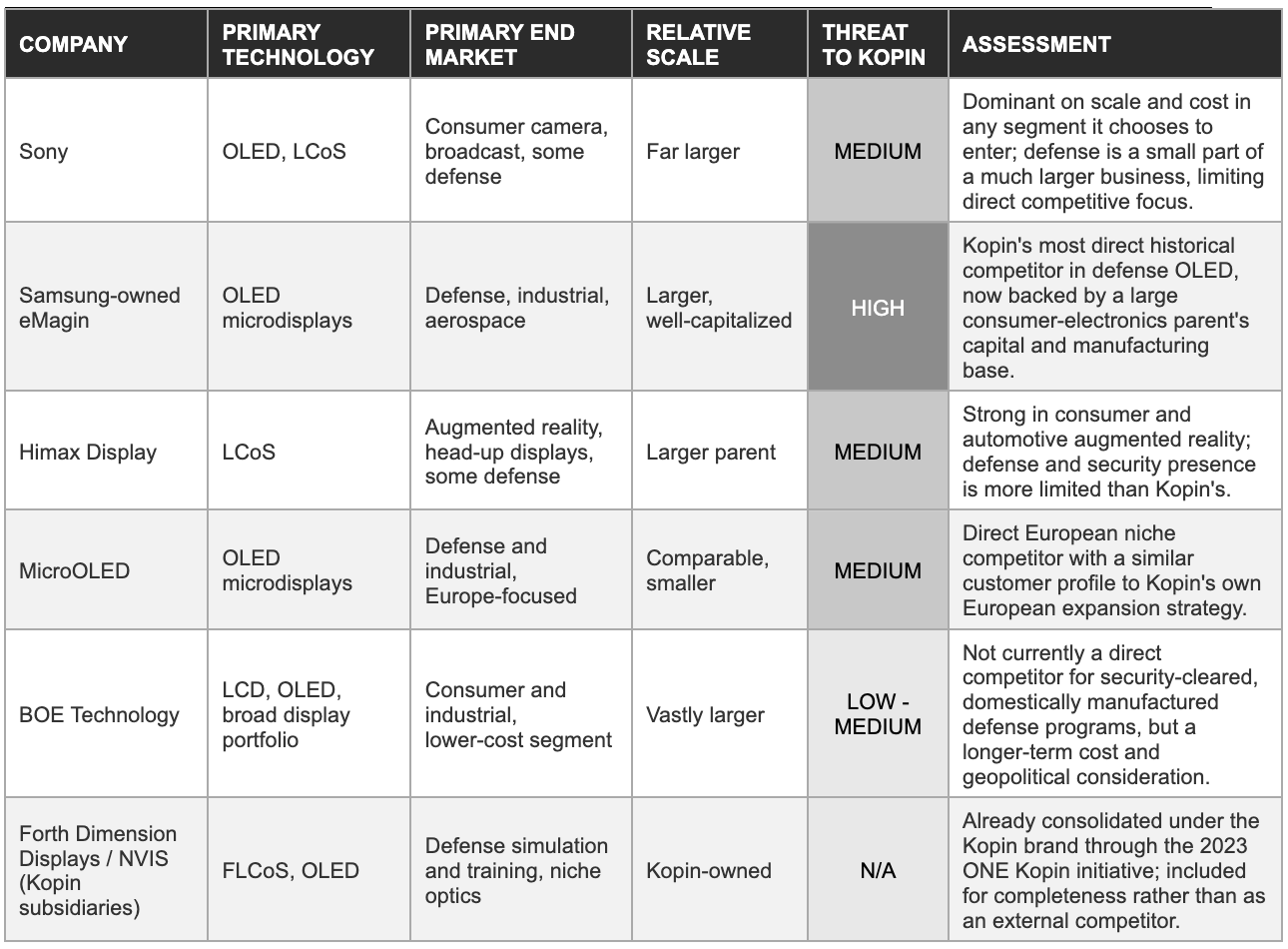

Sony remains the dominant force in OLED and liquid-crystal-on-silicon microdisplays broadly, with a microdisplay business built on a base of consumer camera viewfinder and broadcast-camera demand that dwarfs the entire defense microdisplay market in volume terms, giving it manufacturing scale economics that a company of Kopin’s size cannot match directly. eMagin, once Kopin’s closest direct competitor in OLED microdisplays for defense and industrial applications, was acquired and is now controlled by a large consumer-electronics parent, giving it access to capital and manufacturing scale that an independent eMagin previously lacked.

Himax Display and MicroOLED both compete in the liquid-crystal-on-silicon and OLED segments respectively, with Himax drawing on its much larger parent’s semiconductor manufacturing base and MicroOLED, a French manufacturer, building a defense and industrial niche position in Europe that overlaps directly with Kopin’s own European ambitions. BOE Technology, the Chinese display giant, participates at the lower end of the cost spectrum and represents a longer-term competitive and geopolitical consideration for Western defense supply chains generally, though it is not currently a head-to-head competitor for the security-cleared, domestically-manufactured programs that form Kopin’s core defense revenue.

What protects Kopin’s position

Kopin’s durable advantage in its core market is not a patented technology that competitors cannot replicate, all four microdisplay technologies Kopin produces are well-understood and used by multiple manufacturers globally, but the accumulated weight of program qualification: decades of integration into specific helmet-mounted display systems, weapon sights, and training platforms that have already passed the qualification, testing, and security-clearance processes defense primes require before approving a new microdisplay supplier.

A competitor with comparable or superior underlying display technology would still need to pass through a multi-year qualification cycle on each specific program before it could displace Kopin as an incumbent supplier, and the Made-in-USA and security-clearance requirements attached to many defense programs further narrow the realistic competitive set to a handful of Western manufacturers. This is a real, if modest, moat. It is also one that protects existing program relationships more than it guarantees Kopin will win new ones against equally qualified Western competitors such as eMagin or MicroOLED, and it does nothing to protect the company in the AI-infrastructure market discussed in the following section, where none of Kopin’s defense qualification history carries any weight.

7. Competitive Landscape: AI Optical Interconnects

The competitive set Kopin faces through the Fabric.AI collaboration has almost no overlap with the competitive set described in Section 6. Optical interconnects for AI data centers are being pursued by several companies that have each raised more capital, in some cases by an order of magnitude or more, than Kopin’s entire market capitalization, and that have done so specifically to solve this problem, not as a side project layered onto an existing defense optics manufacturer.

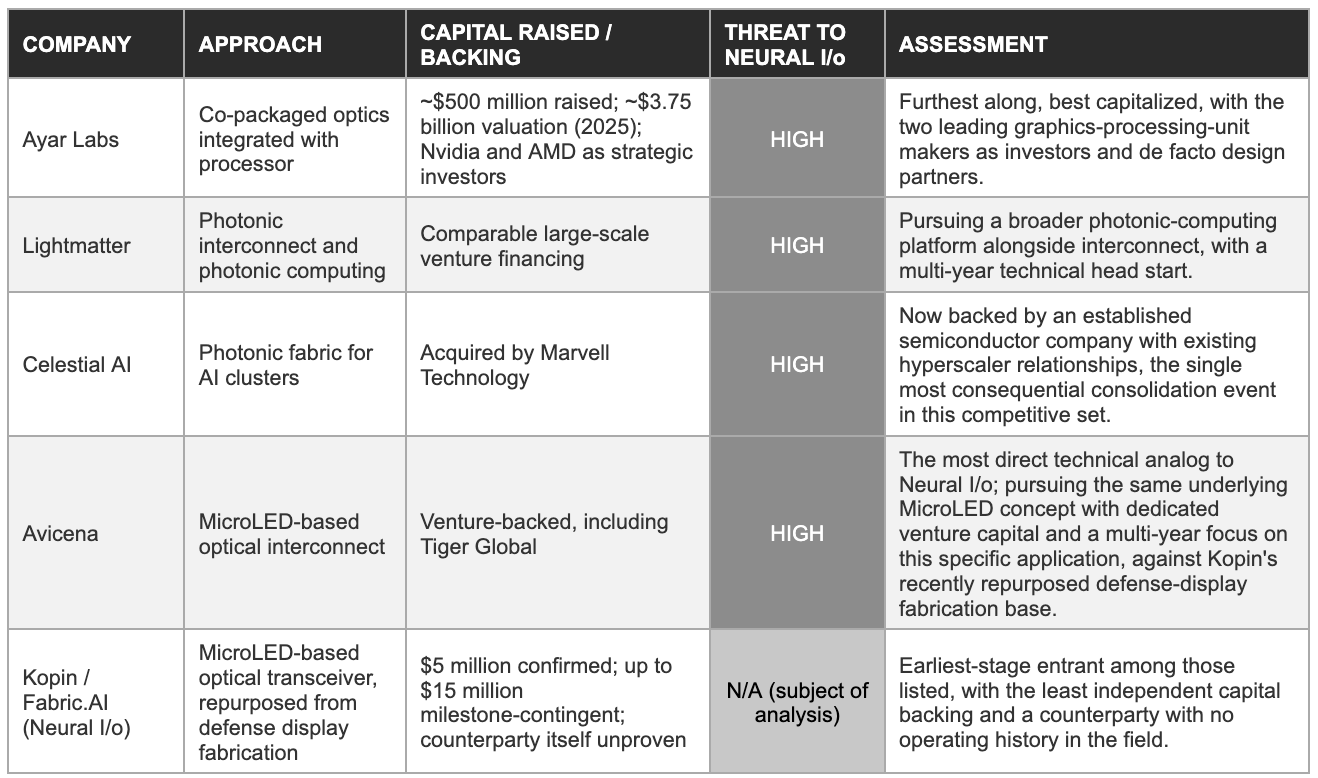

The underlying industry problem that Neural I/o, and every company described in this section, is attempting to solve is real and well-documented: as AI training and inference clusters scale to tens of thousands of graphics processing units, the copper interconnects that have historically linked those chips together run into physical limits on bandwidth, power consumption, and reach, creating demand for optical alternatives that can move data faster, over longer distances within a data center, and at lower power per bit. This is the same broad opportunity that Ayar Labs, Lightmatter, Celestial AI, and Avicena, among others, have been pursuing for several years, each with a different technical approach to getting light in and out of a silicon chip.

Ayar Labs has raised approximately $500 million in financing and was valued at approximately $3.75 billion in 2025, with Nvidia and AMD both participating as strategic investors, alongside chip-industry veterans on its founding and leadership team; its approach uses co-packaged optics integrated directly alongside the processor. Lightmatter has raised comparable amounts of capital pursuing photonic interconnect and photonic computing simultaneously.

Celestial AI, pursuing a photonic fabric approach, was acquired by Marvell Technology, a large, established semiconductor company, giving its technology a direct path into Marvell’s existing data-center customer relationships. Avicena is the closest direct technical analog to Kopin’s approach: it is specifically pursuing MicroLED-based optical interconnects for AI infrastructure, the same underlying display technology Kopin is proposing to repurpose through Neural I/o, and has raised meaningful venture capital from investors including Tiger Global specifically to pursue this architecture.

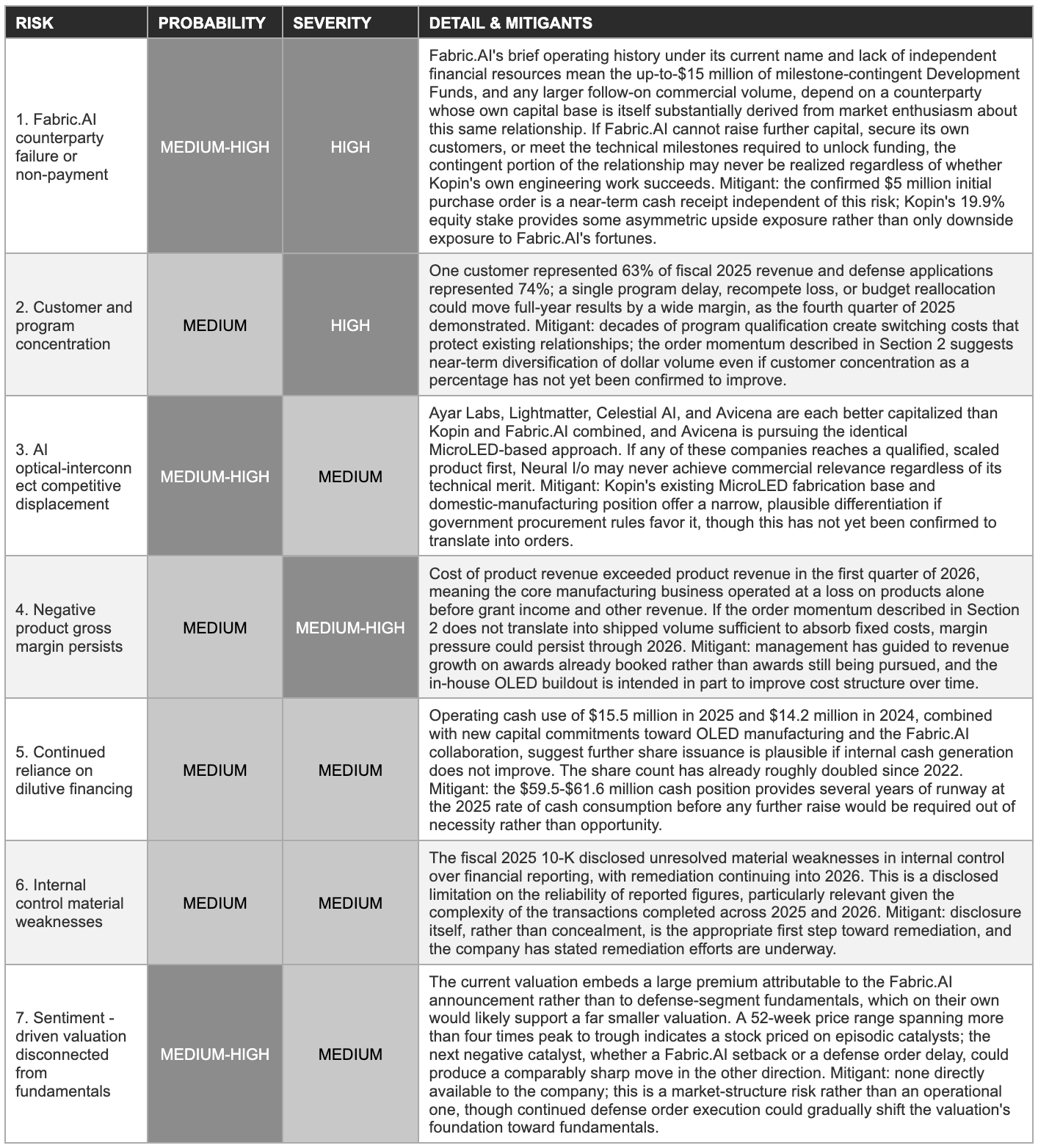

8. Risk Matrix

Each risk below is a named variable that determines which scenario in Section 9 plays out. Ranked by probability and severity combined.

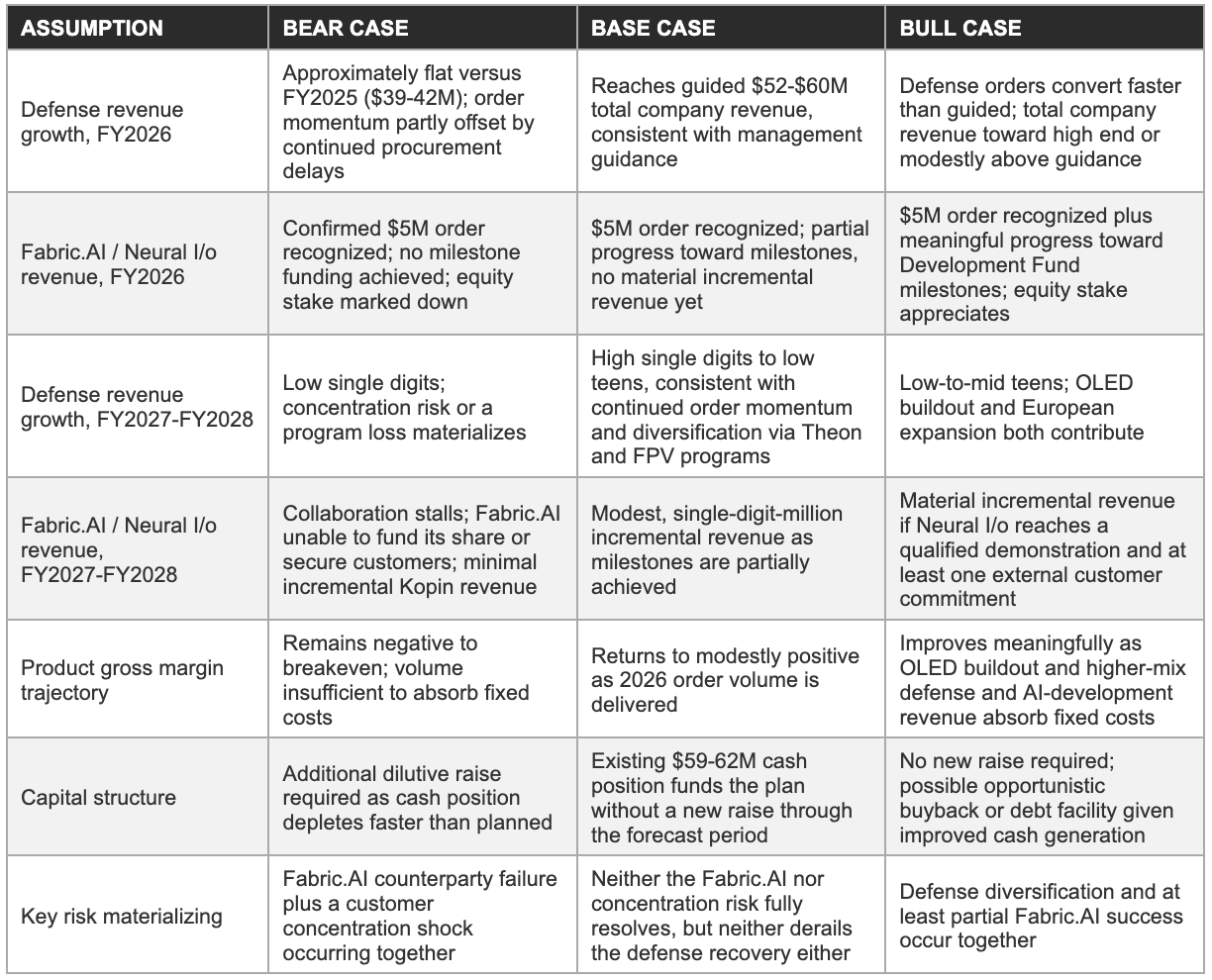

9. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios below separate defense revenue from Fabric.AI revenue explicitly, because the two rest on entirely different evidence and shouldn’t borrow credibility from each other.

Model assumptions by scenario

Three-year revenue and loss projection

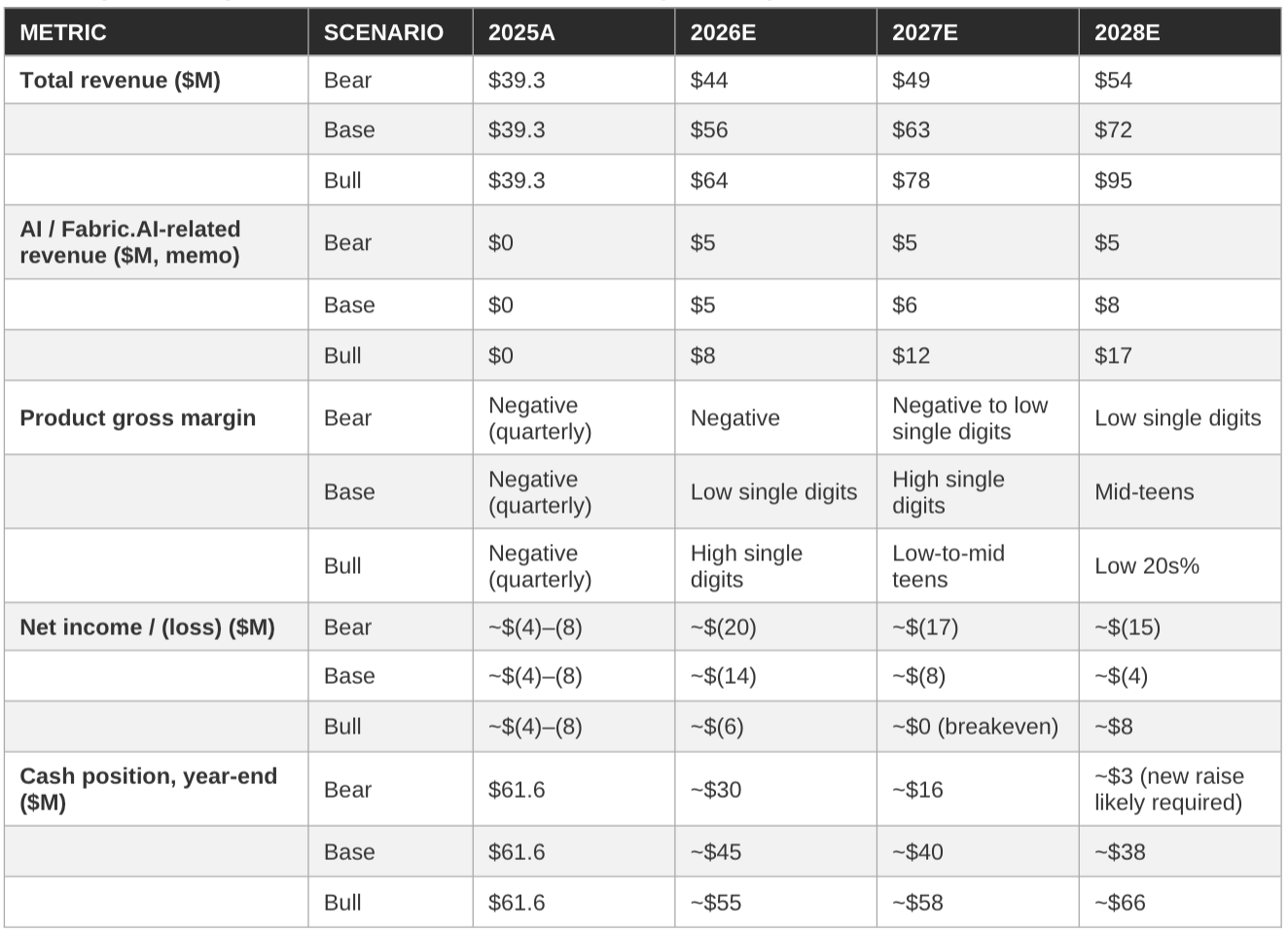

10. The Implied Valuation Question

At current levels, Kopin trades at a multiple its defense business alone doesn’t explain. This section asks what the price actually requires Kopin and Fabric.AI to deliver.

A market capitalization range of $850 million to $1.15 billion against fiscal 2025 revenue of $39.3 million implies a revenue multiple of roughly 22 to 29 times trailing revenue, and against the FY2026 guidance midpoint of approximately $56 million, a forward multiple of roughly 15 to 21 times.

Defense-optics and microdisplay peers of comparable scale and growth profile, where directly comparable public data exists, have historically traded at low single-digit to low double-digit multiples of revenue, not multiples in the high teens or twenties. The gap between Kopin’s current multiple and what its defense business alone would likely command if it traded as a standalone entity is the most direct quantitative expression of how much value the market has assigned to the Fabric.AI relationship specifically.

Valuation framework

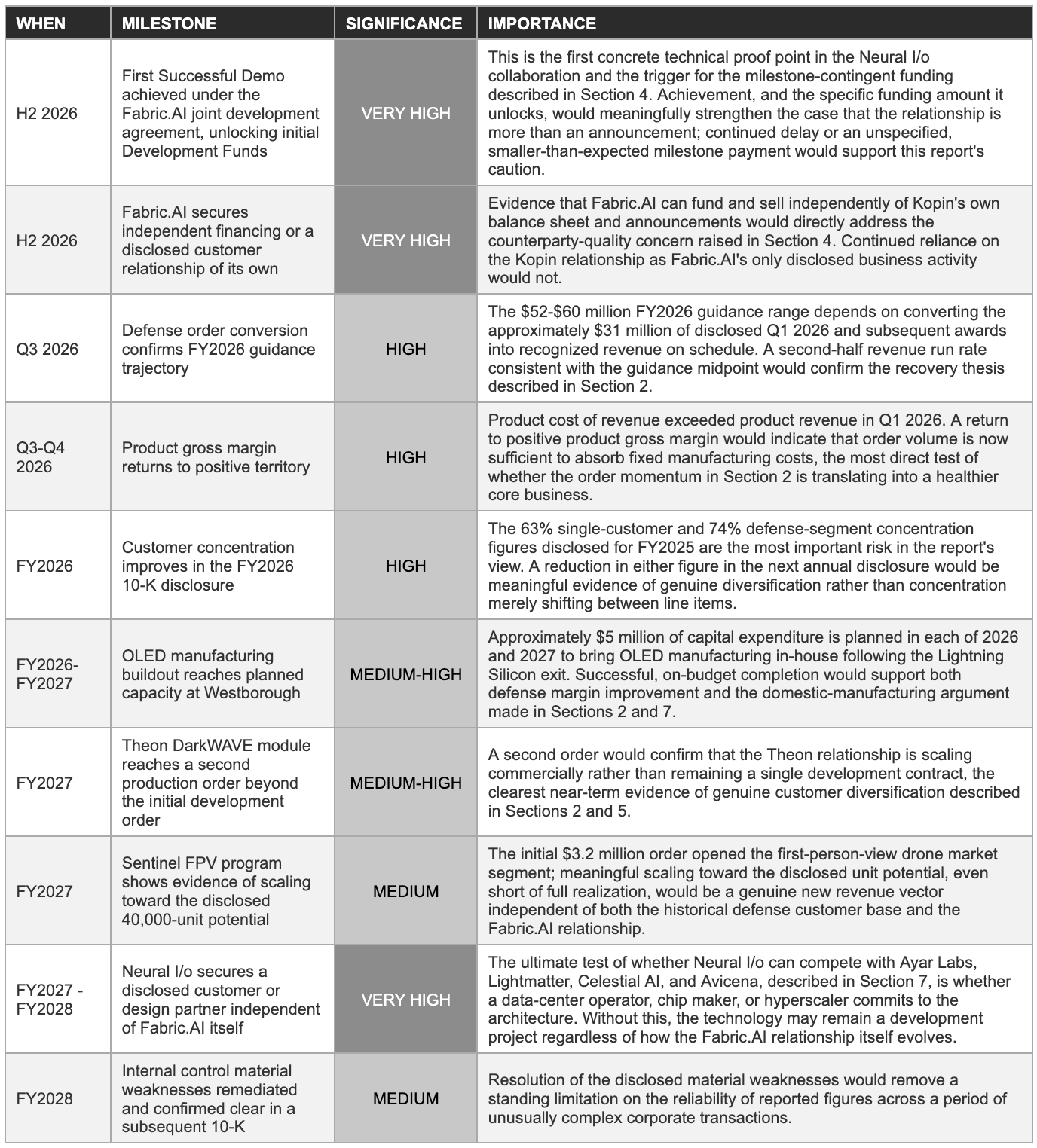

11. Milestone Tracker: What to Watch Through 2028

The milestones below translate the risks and scenarios discussed earlier into specific, observable proof points. The first Successful Demo milestone under the Fabric.AI agreement and the next two quarters of defense order conversion are the two highest-stakes near-term observations; most of what is unresolved in this report’s analysis will become clearer, in one direction or the other, within the next twelve months.

12. Opinion & Investment Perspective: Bull, Base & Bear Cases

What follows is this report’s view as of June 2026, not investment advice or a recommendation to buy, hold, or sell any security. The bear case is given the same depth of treatment as the bull case throughout, consistent with this report’s approach across every section.

The bull case: Three pillars

The first pillar is that the defense business, considered entirely on its own and without crediting any value to Fabric.AI, has shown genuine signs of recovery. The approximately $31 million of disclosed new and follow-on awards across the first quarter of 2026 and the weeks following it, spanning thermal-imaging follow-on production, the new Sentinel FPV product line, European helmet-mounted display orders, and continued government research funding for MicroLED development, support management’s reiterated guidance of $52 to $60 million in FY2026 revenue. If delivered, this would represent the strongest revenue year in the company’s recent history and would do so without requiring any contribution from Fabric.AI.

The second pillar is that Kopin’s underlying manufacturing capability, the only company management credibly describes as producing all four microdisplay technologies, including a meaningful MicroLED fabrication base, is a genuine and transferable asset regardless of which specific commercial application ultimately monetizes it best. If Neural I/o does not succeed, that same MicroLED capability remains available for defense, industrial, or other future applications; the asset is not solely dependent on Fabric.AI’s success to have value.

The third pillar is optionality. Even assigning a low probability of success to the Fabric.AI relationship, the AI optical-interconnect market described in Section 7 is large enough, and the capital markets’ appetite for AI-infrastructure stories strong enough, that a modest probability of meaningful success, multiplied by a very large potential market, can still represent a legitimate, asymmetric call option for a shareholder who understands and accepts the odds. The $222 million scale of capital that Ayar Labs alone has attracted to pursue a similar problem is itself a signal that the market that Neural I/o is attempting to enter is real and well-funded by serious investors, even if Kopin and Fabric.AI are not currently the best-positioned entrants into it.

The bear case: Three concerns

The first concern is the one this report has emphasized throughout: the counterparty standing behind the larger, more valuable parts of the Fabric.AI relationship has no independent operating history, no disclosed customers of its own, and a balance sheet built substantially around the same announcement under examination. If Fabric.AI cannot fund its share of ongoing development or fails to secure outside customers, the up-to-$15 million Development Funds and any larger future commercial relationship may simply never materialize, leaving Kopin with the confirmed $5 million order, a 19.9% stake in a company whose value depends on the same unrealized outcome, and little else from the relationship that has driven most of the recent share-price increase.

The second concern is that even a technically successful Neural I/o demonstration would still need to win commercial adoption against Ayar Labs, Lightmatter, Celestial AI, and Avicena, each of which has a multi-year head start, design relationships with chip makers, and, in Celestial AI’s case, the backing of an established semiconductor company with existing hyperscaler relationships. Avicena’s pursuit of the identical MicroLED architecture is a particularly direct competitive threat that the market’s reaction to the Kopin-Fabric.AI announcement does not appear to have priced with much weight.

The third concern is that the defense business, on the most recent evidence, is not yet healthy enough to be treated as a stable floor under the stock. A 22% revenue decline in 2025, a negative product gross margin in the most recently reported quarter, 63% single-customer revenue concentration, and unresolved material weaknesses in internal control over financial reporting together describe a business that requires several more quarters of clean execution before an investor should treat its recovery as confirmed rather than guided. A reader who believes the Fabric.AI option is worthless still needs to separately underwrite whether the defense business alone is worth the residual value implied at current prices, and the evidence reviewed in this report does not make that an easy case to make with confidence.

The combination that would most damage the investment case, a Fabric.AI counterparty failure occurring at the same time as a renewed defense procurement delay or a loss of share with the concentrated customer described in Section 2, sits outside this report’s base case but is not remote, and an investor purchasing at current levels is, in practice, accepting that combined risk in exchange for the optionality described in the bull case above.

The base-case evidence, real order momentum, a genuine if early-stage technology collaboration, and a cash position sufficient to fund the next several quarters without forced dilution, supports a more balanced outcome than either the bull or bear case alone, but balanced does not mean low-risk, and this report does not believe the current valuation range reflects how early-stage and counterparty-dependent the larger part of the bull case actually is.

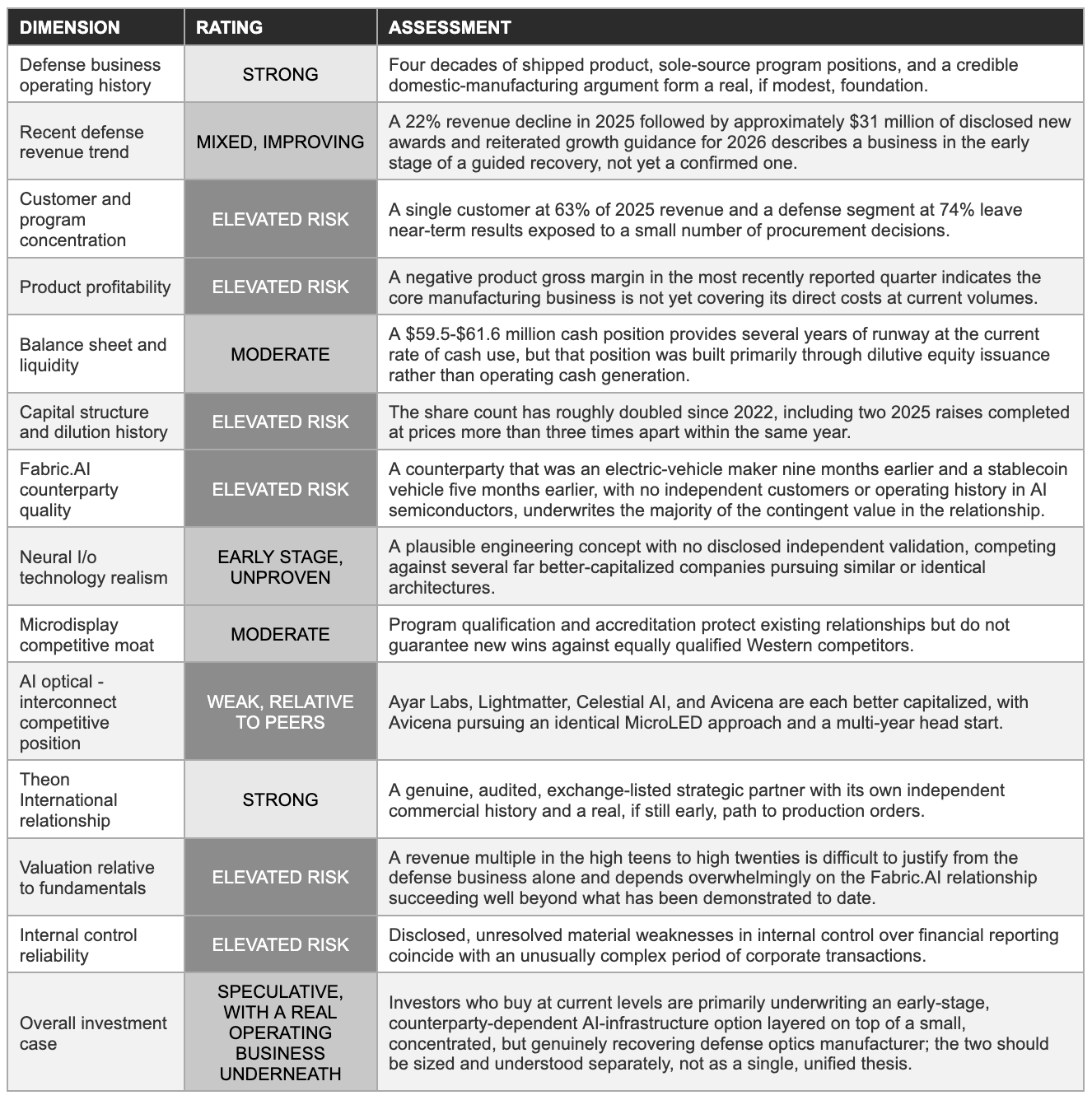

13. Investment Scorecard & Conclusion

The scorecard below distills the preceding twelve sections into a single reference frame. The picture is genuinely mixed rather than uniformly positive or negative: the defense business shows real, if early, signs of recovery, while the larger driver of the current valuation rests on evidence this report views as thin relative to the value the market has assigned to it.

The bottom line

Kopin’s defense business, considered on its own, is a small, concentrated, but genuinely improving optics manufacturer with decades of program history and a credible, if modest, recovery underway in 2026. That business does not, on the evidence reviewed in this report, support the current valuation range on its own. The remainder of the valuation rests on a collaboration with Fabric.AI that is barely two months old as of this writing, governed by a confirmed $5 million order and a milestone-contingent funding ceiling rather than a confirmed larger commitment, and backed by a counterparty whose own corporate history over the prior year consisted of an electric-vehicle business, then a stablecoin treasury strategy, then the very AI semiconductor pivot now driving Kopin’s share price.

None of this means the bet cannot pay off. The optical-interconnect problem Neural I/o is attempting to solve is real, well-funded by serious investors when pursued by other companies, and large enough that even a modest probability of meaningful success could justify a real premium over where the defense business alone would trade.

What this report concludes is narrower: an investor at current levels should understand precisely how much of the price is attributable to a nine-week-old relationship with an unproven counterparty, should not mistake the depth of sell-side coverage initiated entirely after that relationship was announced for independent confirmation of its prospects, and should watch the milestones in Section 11, particularly the first Successful Demo and any evidence of Fabric.AI’s ability to operate and fund itself independently, as the most direct near-term tests of whether the bull case in Section 12 or the bear case is closer to correct.

The single most useful discipline this report can offer a reader is to keep the two businesses separate when forming a view: ask first whether the defense optics manufacturer, on its own, is attractive at the implied standalone valuation in Section 10, and ask second, independently, whether a recently formed relationship with a recently repositioned counterparty deserves the remainder. Conflating the two questions is, in this report’s assessment, the most likely source of an overpriced decision in either direction.

Sources

This analysis is based on publicly available information as of June 2026. Primary sources include: Kopin Corporation fourth-quarter and full-year 2025 earnings release and call (March 2026); Kopin Corporation first-quarter 2026 earnings release, 10-Q, and call (May 2026); Kopin Corporation 10-K for fiscal year 2025; Kopin Corporation 8-K filings related to the Fabric.AI joint development and license agreement (April 2026), the Theon International strategic investment and subsequent preferred stock conversion (August 2025 and May 2026), and the Lightning Silicon Technology and Lightning Silicon America exit (June 2026); company and partner press releases regarding the Sentinel FPV, DarkWAVE, European helmet-mounted display, and Small Business Innovation Research and Industrial Base Analysis and Sustainment awards; third-party financial data aggregators for share price, share count, and analyst coverage data; and public reporting and company disclosures regarding Fabric.AI, formerly StableX Technologies, formerly an electric-vehicle manufacturer, and regarding competing optical-interconnect companies including Ayar Labs, Lightmatter, Celestial AI, and Avicena. All specific figures are sourced to these materials unless explicitly identified as own estimates.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Kopin Corporation (NASDAQ: KOPN) or any other security. All information is sourced from publicly available materials believed to be reliable as of June, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.