OMADA HEALTH, INC.

Between-Visit Chronic Care: The Platform Bet, The Concentration Problem, and Whether Omada Can Convert Clinical Evidence into Durable Competitive Advantage Before the Growth Deceleration Narrative Tak

1. Corporate Profile & The Between-Visit Care Thesis

Omada Health is a virtual chronic care provider generating software-grade gross margins on clinically credentialed programmes sold to employers and health plans. Thirteen years of peer-reviewed evidence and CDC recognition validate the core thesis. The March 2026 question is whether that foundation holds against a decelerating growth rate, acute customer concentration, and the structural pressure GLP-1 medications are placing on the entire chronic disease management market.

Omada Health was founded in San Francisco in 2011 by Sean Duffy and Adrian James. The company was built on a specific and empirically grounded insight: the federal Diabetes Prevention Program Outcomes Study had demonstrated that structured lifestyle intervention reduces progression from prediabetes to type 2 diabetes by 58% in at-risk adults, yet the DPP had never achieved commercial scale because in-person delivery through hospitals and community organisations required physical infrastructure that destroyed the unit economics.

Duffy and James concluded that a fully virtual delivery model, combining digital content, remote human coaching, connected devices, and a purpose-built mobile application, could replicate clinical outcomes at a fraction of the cost and at internet scale. That founding bet has been commercially validated: thirteen years later, Omada has served more than two million members since launch, making it one of the largest virtual chronic care providers in the United States by member volume.

The company carries the formal classification of a virtual-first, between-visit healthcare provider, a positioning that shapes how Omada structures its commercial relationships, bills its services, and has its fee revenue treated in institutional customer budgets. Omada positions its programmes as clinical healthcare services delivered between physician visits, clinical in character, clinical in billing, and clinical in the procurement criteria they must satisfy.

This framing enables the company to bill its fees as healthcare provider medical spend rather than software subscription costs, routing the procurement decision to the medical director and health plan committee, subjecting the vendor to clinical evidence requirements as a procurement prerequisite, and making the fees eligible for pre-tax health savings account treatment in self-insured employer structures. The practical consequence of medical spend billing classification is that Omada’s fees are evaluated against a more rigorous standard than wellness technology procurements and are more defensible in employer cost-cutting environments than discretionary software subscriptions.

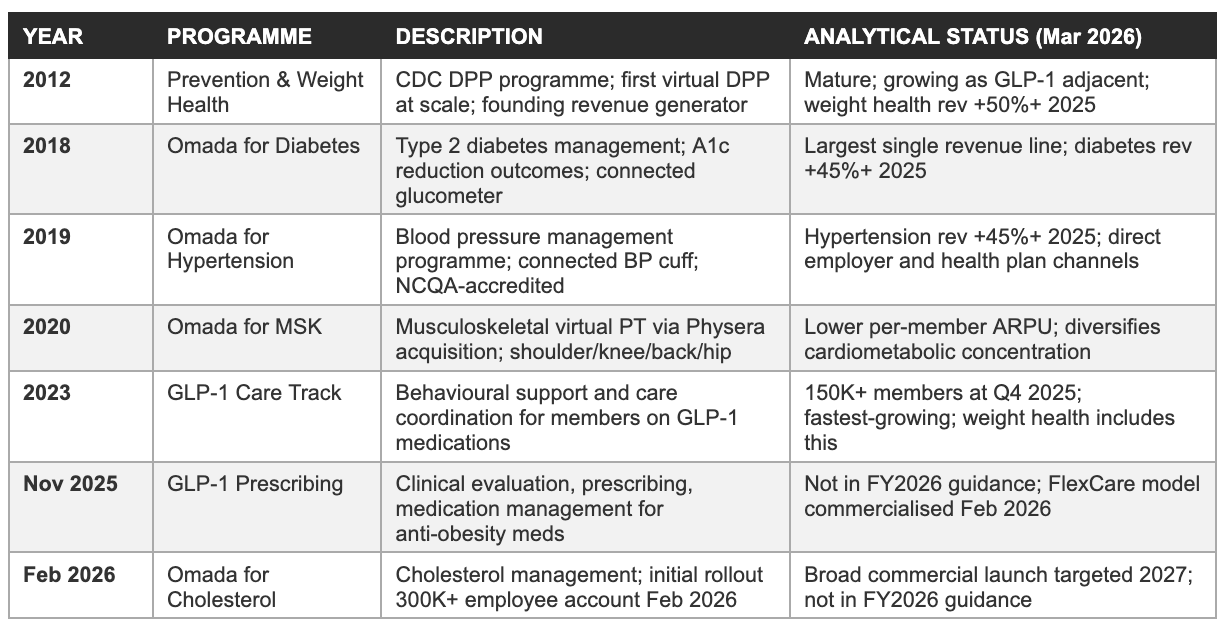

The programme portfolio has expanded substantially from its DPP origins. As of the Q4 2025 earnings call, Omada’s platform spans prediabetes prevention and weight health, type 2 diabetes management, hypertension management, musculoskeletal conditions (virtual physical therapy), GLP-1 companion care for members on GLP-1 medications, GLP-1 prescribing and medication management (launched in late 2025), and cholesterol management (announced February 2026, initial commercial rollout underway).

The company has served more than 2,000 customers across employers, health plans, pharmacy benefit managers (PBMs), and health systems, with an estimated covered lives of more than 25 million as of year-end 2025. The 55% year-over-year member growth to 886,000 enrolled members at December 31, 2025, demonstrates that demand for multi-condition chronic care management remains in active acceleration, even as the company’s revenue growth rate has guided lower for 2026.

Management is led by co-founder and CEO Sean Duffy, who has held the role since the company’s 2011 founding, an unusually long founding-CEO tenure for a pre-profitability healthcare technology company that has had 14 years of operating losses and a public market listing. President Wei-Li Shao joined in a senior operating role to oversee commercial execution. CFO Steven Cook, who joined in April 2024, was the first CFO hired with explicit public-market financial discipline credentials and oversaw the IPO process. The continuity of Duffy’s leadership through the company’s full developmental arc, from DPP-only digital health startup through multi-condition platform and public company, is both a concentration risk (single-founder dependency) and, in our opinion, a strategic asset (institutional knowledge depth and mission conviction that external management would not possess at comparable depth).

The chronic disease addressable market

The market Omada is addressing is vast. The company’s S-1 cites CDC and KFF data indicating that more than 156 million Americans suffered from one or more chronic conditions as of 2022, including obesity, prediabetes, diabetes, hypertension, and musculoskeletal conditions, with approximately 40% of U.S. adults having obesity. Its primary target population is the approximately 154 million individuals covered by commercial health insurance through employer-sponsored plans, the segment at the centre of Omada’s sales motion. Of this 154 million, the company estimated that approximately 18 million individuals had access to one or more Omada programmes as of December 31, 2024, implying that more than 136 million eligible covered lives remain unaddressed.

The S-1 disclosed Omada’s per-condition TAM estimates: prediabetes/weight health approximately $41.4 billion annually, diabetes $17.3 billion, hypertension $31.6 billion, and musculoskeletal conditions a further significant segment, with the combined TAM across all current conditions estimated at approximately $90 billion within the commercial insurance channel alone. These estimates are based on the company’s current programme list prices applied to the clinical prevalence of each condition within the target population, which makes them both a reasonable order-of-magnitude reference and a forward-looking aspiration that requires significant market penetration to realise.

The cholesterol programme announced in February 2026 adds a further addressable population: hypercholesterolaemia affects approximately 94 million U.S. adults, and the condition frequently co-occurs with diabetes, hypertension, and obesity, making it a natural add-on condition within Omada’s existing member base. The clinical and commercial logic of addressing cholesterol within an already-enrolled cardiometabolic member is the same as the logic for the diabetes-hypertension cross-sell: the member is already engaged with the platform, already has a connected care team relationship, and the incremental cost of adding cholesterol monitoring and coaching to an existing member’s programme is a fraction of the cost of acquiring a new member. If the cholesterol programme achieves meaningful attach rates within the existing 886,000-member enrolled base, its contribution to revenue per member per year could be significant without requiring a single new customer logo.

2. Founding Conviction & The 13-Year Road to Positive EBITDA

Omada required thirteen years, roughly $530 million in venture capital, and an accumulated deficit approaching $460 million before delivering its first profitable quarter. That timeline reflects two forces simultaneously: a genuine incubation of clinical evidence and enterprise relationships that the business model requires as foundational infrastructure, and the structural difficulty of generating economic leverage on a revenue model that front-loads acquisition cost against a monthly-accreting revenue stream. Both forces are real, and the interplay between them is what the current valuation is pricing.

The founding insight: DPP at internet scale

The National Diabetes Prevention Program, established by the CDC based on the landmark Diabetes Prevention Program randomised controlled trial, had demonstrated that structured lifestyle intervention, dietary modification, physical activity coaching, and behaviour change support delivered by trained health coaches, reduced progression from prediabetes to type 2 diabetes by 58% relative to standard care, and by 71% in adults over 60. The DPP was clinically validated at the highest level of evidence available: a 3,234-participant, 27-clinical-centre randomised controlled trial funded by the National Institutes of Health. But the programme had an inherent delivery problem.

The original trial protocol required in-person group sessions with trained lifestyle coaches, conducted across 16 weekly sessions followed by monthly maintenance contacts for two years. The infrastructure cost of delivering this protocol through hospitals, YMCAs, and community health organisations meant that programme fees needed to cover facility overhead, trainer salaries, and patient attendance logistics, pricing the programme beyond the reach of most self-insured employers and making it economically unattractive for health plans to cover at scale.

Duffy and James concluded that the DPP intervention’s evidence-based efficacy was separable from its in-person delivery mechanism. The behavioural change content, nutrition education, physical activity programming, habit tracking, emotional support, and accountability, could be delivered through a digital channel combining a mobile application, connected devices, and asynchronous human coaching without material loss of clinical efficacy, because the research evidence suggested that the active ingredient in DPP success was the behavioural science content and the coaching relationship, rather than the physical co-location of coach and participant.

The clinical evidence asset: Why 30 publications matter commercially

Omada had published 30 peer-reviewed clinical studies by the time of its June 2025 IPO, covering outcomes including haemoglobin A1c reduction (a primary measure of diabetes management), systolic blood pressure reduction, weight loss maintenance, healthcare cost savings at the employer and health plan level, GLP-1 companion care weight outcomes, and member engagement durability at 12 and 24 months. These publications are distributed across journals including JAMA Network Open, Diabetes Care, American Journal of Health Promotion, and others, peer-reviewed outlets that carry the credibility required for medical committee review in enterprise health plan and self-insured employer procurement.

The commercial significance of this evidence base is functional and procurement-critical. When a large self-insured employer’s medical committee evaluates a chronic disease management vendor for inclusion in the employee benefits package, the medical director requires peer-reviewed outcome evidence as a prerequisite for the presentation to the medical committee. That filter is absolute: the response time for the evidential request is measured in days or weeks, while building the evidence base required to satisfy it is measured in years. This asymmetry is the mechanism that creates one of Omada’s most durable competitive moats: the evidence base was built over 13 years of operating history and compounds with each additional publication.

A well-funded competitor entering the employer chronic disease management market in 2025 begins its publication timeline at zero, and will reach the minimum evidence base required for health plan formulary considerationl, typically 3-5 years of outcomes data, at the earliest in 2028 or 2029, by which point Omada will carry 17-19 years of published evidence and a substantial incumbent relationship network.

The GLP-1 Care Track outcome data announced on the Q4 2025 earnings call is the most recent and commercially significant addition to this evidence portfolio. Omada disclosed that members in its GLP-1 Care Track who discontinued GLP-1 medications maintained average weight change of only 0.8% after one year, compared to 11-12% weight regain documented in published clinical trials in the absence of behavioural support.

This is a clinically important and commercially exploitable finding: it directly addresses the central objection that PBMs and health plans have to GLP-1 coverage, which is that the $15,000-$18,000 annual drug cost produces outcomes that disappear when the medication is discontinued. An Omada-supported GLP-1 discontinuation outcome of 0.8% weight change versus 11-12% in controls is the quantification of the companion care value proposition, and it is the data point that enables the spend guarantee structure that at least one large PBM partner has offered to employer clients through its Omada partnership.

The accreditation stack: Regulatory moats in commercial form

Omada holds three categories of accreditation that function as procurement prerequisites in the enterprise healthcare channel. The CDC National DPP recognition is the most foundational: it designates Omada’s prediabetes prevention programme as a CDC-recognised DPP, which is required for coverage as a preventive service under the Affordable Care Act’s preventive services mandate.

This mandate requires qualified health plans to cover certain preventive services without cost-sharing, and CDC DPP recognition is the specific credential that unlocks zero-cost-to-member enrolment, the feature that makes DPP programme enrolment rates commercially viable. Omada was the first virtual DPP provider to obtain this recognition, and the combination of that tenure with breadth of condition coverage and clinical evidence depth gives Omada an institutional standing in the enterprise channel that more recently accredited competitors have yet to build.

The NCQA (National Committee for Quality Assurance) Diabetes Care Recognition and the URAC (Utilization Review Accreditation Commission) Health Website and Health Coaching accreditations are required by several large national health plans as conditions of vendor panel inclusion. These accreditations certify compliance with quality standards for clinical programme design, data management, and member safety protocols that health plans use as a proxy for quality and risk management.

Obtaining and maintaining these accreditations requires operational infrastructure, clinical oversight processes, quality assurance systems, complaint resolution procedures, and periodic re-certification audits, that represents a non-trivial ongoing investment and creates a meaningful entry barrier for commodity wellness applications lacking the clinical infrastructure to qualify.

The commercial consequence of this accreditation stack is substantive: Omada’s fees qualify for medical spend treatment in self-insured employer benefit plans. In the corporate benefits purchasing environment, medical spend is evaluated by the medical committee rather than the benefits purchasing department, carries a distinct budget treatment and tax status, and is typically renewed under longer contract horizons with higher switching costs. This categorisation, and the 90%+ three-year customer retention rate it enables, is structurally achievable precisely because Omada’s fees are subject to medical committee governance rather than the discretionary vendor review cycles that drive churn in the wellness technology sector.

Why thirteen years of losses

The $530 million in venture capital financing raised pre-IPO and the approximately $457 million accumulated deficit as of December 31, 2025, are the financial signature of a business that chose to invest heavily in pre-revenue infrastructure before attempting to generate profitable returns. Three compounding factors explain the duration.

First, the enterprise healthcare sales cycle is inherently slow: a typical large self-insured employer benefits decision requires a request-for-proposal process, medical committee clinical review, legal negotiation of service agreements and business associate agreements under HIPAA, open enrollment integration, communication campaign design, and a 12-month contract period before the first revenue dollar is recognised. New enterprise relationships commonly require 12 to 24 months from first contact to revenue, meaning that sales investment today produces revenue 12-24 months in the future.

Second, the per-member-per-month revenue model creates a cash flow structure that penalises rapid growth: customer acquisition costs are incurred immediately, technology and care team infrastructure must be built in advance of demand, and revenue accretes monthly over multi-year contract periods, creating a structural working capital deficit in high-growth periods that requires external capital to bridge.

Third, Omada made a deliberate strategic choice to invest in the clinical evidence base, commissioning and conducting the 30 peer-reviewed studies that are now its primary competitive moat, before attempting to monetise at scale. Competitors who entered the market with a wellness technology positioning and lower clinical evidence standards could bypass this cost, but Omada’s founders believed the healthcare procurement environment would ultimately reward clinical credibility over technology sophistication, and the 90%+ customer retention rate and 128% net dollar retention suggest that judgement was correct.

3. Business Model Architecture: PEPM Economics, Channel Structure & Concentration Risk

Omada generates 66-71% gross margins on a per-enrolled-member-per-month revenue stream paid by employers and health plans, fees structured as clinical medical spend rather than software subscriptions, which determines who procures it, how it is budgeted, and how sticky it becomes at renewal. The architecture is capital-efficient by design. Its central vulnerability is that the same channel partnerships driving that efficiency concentrate approximately 60% of revenue through two unnamed intermediaries.

The PEPM revenue model: Structure and economics

Omada generates revenue primarily through a per-enrolled-member-per-month (PEPM) pricing model under which its employer and health plan customers pay a monthly fee for each member actively enrolled in an Omada programme. The pricing is condition-specific: the prediabetes prevention and weight health programme carries a different PEPM than the diabetes management programme, which carries a different PEPM than hypertension or MSK, reflecting the different care team intensity and clinical infrastructure required for each condition.

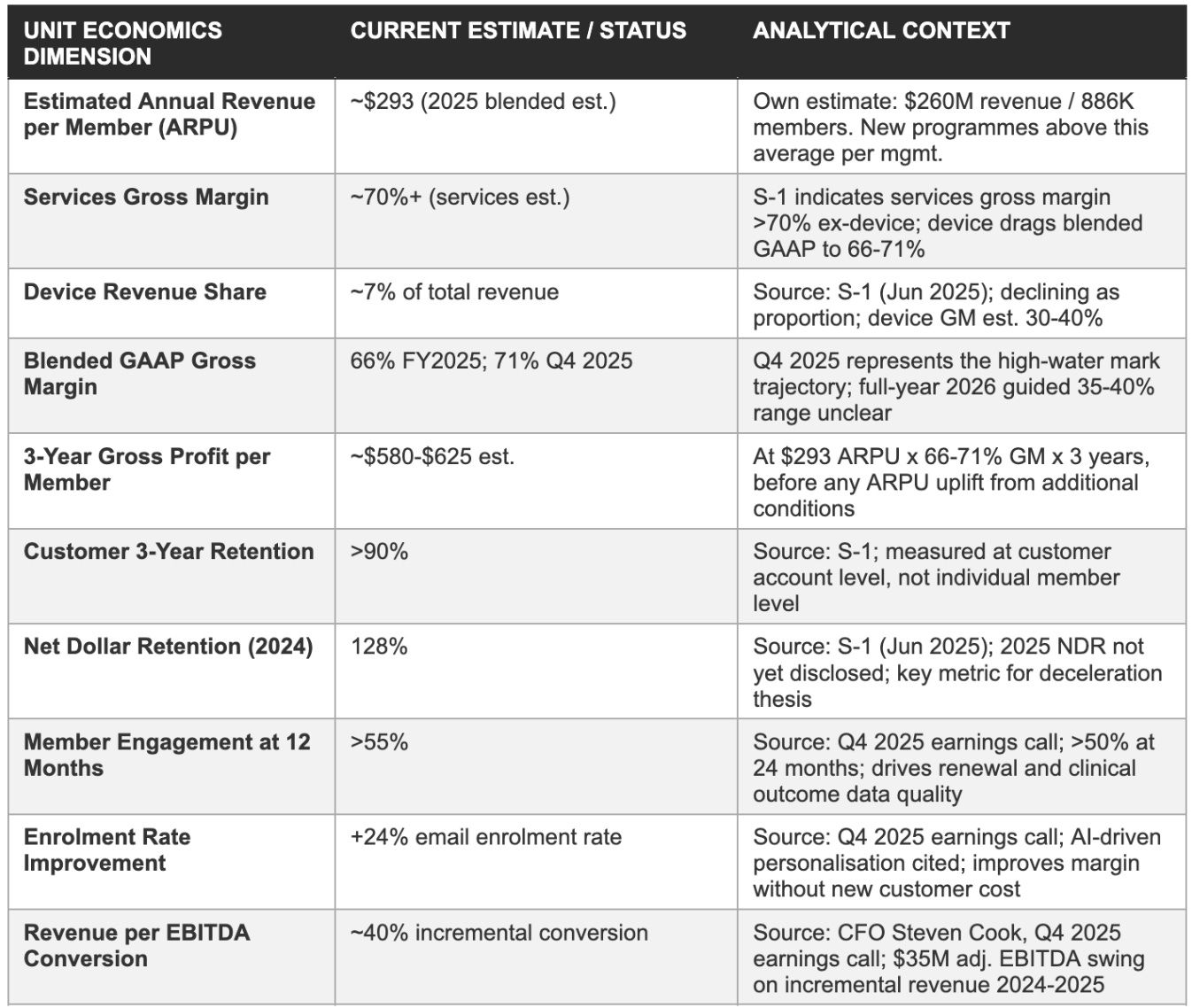

The blended average revenue per enrolled member per year across the full 2025 member base was approximately $293 (Own estimate: $260M total revenue / 886K members), though management confirmed on the Q4 2025 earnings call that new programmes including GLP-1 prescribing and cholesterol management are priced above this blended average, implying that programme mix evolution toward higher-acuity or higher-complexity conditions is a natural upward pressure on revenue per member over time.

The PEPM model generates revenue that is recurring within each contract period, contractually committed by the employer or health plan customer for the duration of the agreement (typically 12 months with annual renewal options and multi-year preferred agreements), and which continues without requiring a per-transaction action by either the payer or the enrolled member to trigger payment. This structure is the origin of the gross margin profile: the primary cost of serving enrolled members is the care team staffing (health coaches, clinical oversight, content delivery), which scales with the member population but not with the number of monthly billing cycles.

Once a care team cohort is staffed and an enrolled member population is active, incremental revenue from additional enrolments within an existing customer account adds gross profit at rates that approach the programme’s service gross margin, which the company’s services gross margin (stripping out device costs) is estimated at more than 70%. The convergence of gross margins toward 71% in Q4 2025 reflects the ongoing shift in revenue mix away from device revenue and toward pure services revenue as the installed member base matures.

The device revenue component represents approximately 7% of total revenue and carries materially lower gross margins than the services component, estimated at 30-40% versus 70%+ for services. Device revenue exists not as a profit centre but as an enrolment and engagement enabler: connected devices create a data feedback loop between the member and the care team that increases programme engagement, improves outcome data quality for clinical monitoring, and reduces the dropout risk that would impair customer renewal rates. Management has consistently characterised device economics as subordinate to the strategic value of the engagement mechanism they enable, and the trajectory of gross margin expansion, from approximately 54% in 2022 to 66% in FY2025 to 71% in Q4 2025, confirms that the business model’s profitability improves as device revenue share declines as a proportion of total revenue.

The company also recognises a secondary revenue stream from certain outcome-contingent contract structures in which a portion of programme fees is deferred and recognised only upon achievement of defined clinical outcomes, such as a minimum percentage of enrolled members achieving a target level of programme engagement or a target weight reduction. These outcome-based contracts represent a minority of total revenue but are analytically significant as an indicator of management’s confidence in clinical programme efficacy: a company that is willing to accept outcome-contingent payment terms is expressing a belief that the contracted outcomes will be delivered.

The PBM spend guarantee structure referenced on the Q4 2025 earnings call, where a large PBM partner has offered employer clients a guarantee that combined GLP-1 drug plus Omada programme costs will not exceed a defined per-member threshold, is an extension of the outcome-based contracting logic into the GLP-1 channel.

Channel architecture: Three distribution pathways

Omada operates a business-to-business-to-consumer distribution structure across three primary channels. The direct employer channel involves contracts with self-insured employers who procure Omada’s programmes directly as an employee benefit, administered through the employer’s benefits portal with Omada as a contracted healthcare provider.

Direct employer relationships are higher-touch and longer-cycle to acquire, requiring benefits manager engagement, medical committee review, legal negotiation, and open-enrolment integration, but they provide direct access to the employer’s HR and benefits decision-making hierarchy, eliminate channel partner margin sharing, and create a bilateral relationship that is less intermediated and therefore less susceptible to unilateral renegotiation by a distribution intermediary. The direct employer channel is where Omada’s clinical evidence and accreditation moats are most directly visible to the procurement decision-maker.

The health plan and PBM channel involves embedding Omada’s programmes within the benefit designs that health plans offer to their commercial employer clients, or within the GLP-1 medication management solutions that PBMs sell to employer pharmacy benefit clients. A single health plan contract can unlock access to millions of covered lives because the health plan’s employer clients collectively represent a large aggregated population, and the PBM’s GLP-1 management framework creates a natural channel for enrolling members who are already on GLP-1 medications into Omada’s GLP-1 Care Track.

The efficiency of this channel is its core commercial advantage: Omada can reach a much larger covered lives pool through health plan and PBM relationships than it could through direct employer sales force investment alone. But the efficiency creates the concentration risk: if the channel intermediary changes its preferred vendor list, builds an in-house programme, or renegotiates pricing terms, the impact flows through to a disproportionately large share of Omada’s revenue.

The health system channel involves contracts with hospital systems and integrated delivery networks that offer Omada’s programmes to patient populations through a care coordination model that connects Omada’s virtual programme with the health system’s primary care infrastructure. This channel is currently a smaller contributor to total revenue than the employer and health plan channels, but it represents a strategic expansion pathway into populations that are enrolled through clinical referral rather than employer benefit administration, a fundamentally different and potentially more clinically integrated enrolment pathway that could improve programme engagement and outcomes relative to the predominantly marketing-driven enrolment of the employer channel.

Customer concentration: The central near-term investment risk

As of Q1, 2025, one health plan or PBM accounted for 31% of Omada’s revenue, and a second health plan or PBM accounted for 29% of its revenue, a combined 60% of total revenue flowing through two unnamed intermediary channel partners. This is the single most important risk disclosure in the company’s public filing history, and it remains unresolved in the information available as of March 2026.

The concentration figures cited above are for the three months ended March 31, 2025, the most recent quarterly period disclosed in the S-1 filed in May 2025 for the June IPO. The FY2025 10-K, expected in April 2026, will be the first opportunity for investors to observe whether either or both partners have crossed above or below the 10% threshold that triggers mandatory disclosure of revenue concentration. Industry analysis by Rocket Digital Health and Fierce Healthcare has identified these partners as Cigna-affiliated entities, specifically, Cigna’s health plan subsidiary and Cigna’s PBM affiliate (Evernorth/Express Scripts), though neither Omada nor either alleged partner has confirmed this identification publicly.

The structural implication matters more than the name confirmation: if both concentration counterparties are affiliated with a single ultimate parent (Cigna/Evernorth), the effective concentration risk is more severe than the 31% / 29% split suggests, because a strategic decision at the Cigna group level to build or acquire a competing chronic care solution could simultaneously affect both channel relationships.

The mitigants against the concentration risk are real but incomplete. The 128% net dollar retention in 2024 demonstrates that the customer base as a whole was expanding its spend, not contracting it, a 128% NDR means that the 2024 cohort collectively spent 28% more with Omada than the same cohort had spent in 2023, which includes both organic member growth within existing accounts and new programme additions.

The Q4 2025 earnings call commentary that both weight health and diabetes and hypertension grew at least 45% each in 2025 suggests that the expansion dynamic within the concentration accounts is continuing. However, 128% NDR is a lagging indicator measured at the aggregate customer cohort level; it does not guarantee that the specific relationships generating 60% of revenue will remain intact at the same pricing and scope. The 2025 NDR, which management has not yet separately disclosed and which will be reported in the 2025 annual report, is the most important single financial metric that investors cannot currently observe.

The customer concentration risk is further compounded by the fact that Omada has limited public disclosure about the economics of its channel partner relationships. Health plan and PBM channel contracts typically involve a revenue-sharing or channel margin arrangement in which the channel partner receives a portion of the PEPM fee in exchange for distribution access, meaning that Omada’s gross margin on the channel-partner-distributed revenue may be materially lower than on direct employer revenue.

If the channel partners are subject to cost-reduction pressure, as PBMs broadly are in the current healthcare cost containment environment, the first area of renegotiation in any renewal cycle may be the channel margin, which would create gross margin pressure at the same time as the revenue deceleration optic is challenging investor sentiment.

Unit economics: Per-member revenue and margin architecture

The following table presents the illustrative per-member economics of a software-and-services-attached Omada member across a three-year contract horizon, using management disclosures and our own estimates. These figures are illustrative and based on blended averages; actual per-member economics vary by programme, channel, and customer type.

4. Platform Evolution & Growth Vectors: Multi-Condition Expansion, GLP-1, and the Prescribing Pivot

Omada has expanded from a single diabetes prevention programme to a six-condition cardiometabolic platform, with each new condition added to an existing employer account requiring a fraction of the acquisition cost of a new logo. GLP-1 medications are simultaneously the fastest-growing demand driver and the most structurally ambiguous risk: member enrolment tripled in twelve months, while the question of whether PBM channel partners will internalise the companion care value chain remains open. The prescribing capability launched in early 2026 is the step that could materially change the revenue model's ceiling.

The expand-within-account economic logic

Omada’s multi-condition expansion strategy is structurally elegant from a unit economics perspective. An employer that has already contracted with Omada for a diabetes prevention programme has already completed the longest and most expensive phase of the customer acquisition process: the request-for-proposal, the medical committee clinical review, the legal negotiation of the healthcare service agreement and business associate agreement, the benefits portal integration, and the open-enrolment communication campaign.

Every additional condition added to that employer’s Omada deployment, hypertension management, GLP-1 Care Track, MSK virtual therapy, cholesterol, requires only an incremental contract amendment and a marginal additional enrolment communication effort, not a full re-prosecution of the procurement cycle. The incremental gross profit of a second condition sold to an existing employer is therefore substantially higher than the gross profit of the first condition sold to a new employer, because the channel acquisition cost is near zero and the marginal cost of adding a second condition to a care team that is already operational for the first condition is limited to the incremental care team capacity and programme-specific clinical infrastructure required.

This expand-within-account economic mechanism is the structural explanation for the 128% net dollar retention rate in 2024. When the 2023 cohort of customer accounts collectively spent 28% more with Omada in 2024 than in 2023, that incremental spend came primarily from three sources: organic member growth within existing accounts as the eligible employee population accessed available programmes; new condition additions within existing accounts as employers expanded their Omada deployment to cover additional conditions; and price escalation on renewing contracts reflecting the expanded clinical evidence base and improved outcomes data.

The company’s disclosure that weight health revenue, diabetes revenue, and hypertension revenue each grew at least 45% in 2025 demonstrates that the expand-within-account motion is simultaneously driving parallel growth across multiple conditions, not concentrating in a single high-growth category that would be susceptible to a single-programme demand cycle.

The February 2026 launch of Omada for Cholesterol represents the sixth programme condition in the portfolio. Management disclosed that the broader commercial launch of the cholesterol programme is targeted for 2027, and that no revenue contribution from cholesterol is embedded in the FY2026 guidance of $312-322 million. The strategic significance of the cholesterol launch is not its near-term revenue contribution but its demonstration that the expand-within-account motion can be extended beyond the cardiometabolic core into adjacent conditions that share the same patient population: hypercholesterolaemia affects approximately 38% of U.S. adults, and the condition has a high rate of co-morbidity with diabetes, hypertension, and obesity, conditions that Omada is already managing in its enrolled member base.

A member enrolled in Omada for Diabetes who also has elevated cholesterol is a near-zero-cost acquisition target for Omada for Cholesterol, requiring only a clinical eligibility screen and a programme extension offer from the existing care team.

GLP-1: The dominant near-term growth vector and its structural ambiguity

Omada disclosed at the Q4 2025 earnings call that it has supported more than 150,000 members on GLP-1 medications as of year-end 2025, compared with more than 50,000 at year-end 2024, a tripling in twelve months that represents the fastest-growing member category in the company’s operating history. Weight health revenue (which includes GLP-1 care track members) grew more than 50% in 2025, according to management commentary on the Q4 2025 earnings call. The GLP-1 Care Track positions Omada as the behavioural support, care coordination, and medication management oversight layer that makes GLP-1 medications more effective and more durable, addressing the two central problems that self-insured employers face when making coverage decisions about GLP-1 drugs.

The first employer GLP-1 problem is cost: branded semaglutide (Ozempic, Wegovy) and tirzepatide (Mounjaro, Zepbound) carry annual list prices of approximately $15,000 to $18,000 per patient, and with the obesity prevalence in the commercial insurance population estimated at 40% of adults, the actuarial impact of broadly covering GLP-1 medications is potentially catastrophic to self-insured employer benefit budgets. Employers that cover GLP-1s need a mechanism to ensure that the drug spend translates into durable health improvements that reduce downstream healthcare costs, not just weight loss that reverses when the medication is discontinued.

The second problem is discontinuation: published clinical research, including data from the STEP and SURMOUNT trials, demonstrates that patients who discontinue semaglutide or tirzepatide without structured behavioural support regain an average of approximately 11-12% of body weight within one year of discontinuation, essentially reversing the clinical gains achieved during therapy.

Omada’s GLP-1 Care Track directly addresses both problems. The behavioural support programme reduces the dosing levels required to achieve clinical thresholds for some members, reducing the drug cost per outcome achieved. The companion care framework reduces dropout risk before clinical targets are reached, improving the effective utilisation of the drug spend.

And most significantly, the programme sustains outcomes after discontinuation: the Q4 2025 disclosure that Omada GLP-1 Care Track members who discontinued GLP-1 medications showed average weight change of only 0.8% after one year, compared to 11-12% regain in controls, is the data point that enables the spend guarantee model that at least one large PBM partner has offered to employer clients through the Omada channel. A spend guarantee structure that contractually caps the combined drug-plus-Omada-programme cost per member at a defined threshold, backed by Omada’s outcome data, converts the GLP-1 coverage decision from an open-ended actuarial liability into a bounded cost management commitment.

The GLP-1 Care Track clinical evidence is strong, the 0.8% discontinuation weight change versus 11-12% in controls is a compelling signal. The structural concern runs deeper: the same PBM and health plan partners who are currently distributing Omada’s GLP-1 Care Track carry powerful financial incentives to build or acquire proprietary companion programmes and internalise the economic value currently flowing to Omada. A PBM that controls the GLP-1 formulary, dispenses the medication, and collects the companion care fee is capturing the full value chain. At current GLP-1 volume and growth trajectory, that economic incentive is substantial enough to attract competitive capital.

The prescribing pivot: A model-changing step under conservative guidance

In November 2025, Omada announced plans to launch a prescribing capability that would combine its behavioural change programme with clinical evaluation and medication management for anti-obesity medications including GLP-1 drugs. The announcement noted that Omada would not directly dispense medications but would provide clinical oversight, prescription management, and care coordination services that connect members with appropriate medication access.

On February 2026, Omada commercialised GLP-1 FlexCare, described as an option that gives employers a structured pathway to connect eligible employees with clinical evaluation, prescribing, and ongoing medical oversight for GLP-1 medications alongside Omada’s lifestyle and behavioural support, explicitly structured so that the employer does not assume the financial coverage obligation for the GLP-1 drug costs themselves.

The FlexCare model is commercially innovative because it separates the prescribing and oversight service (which Omada can bill for directly) from the drug cost (which remains the member’s responsibility or a separate insurer function). This structure allows Omada to enter the prescribing business without taking on the actuarial risk of drug cost coverage, positioning it as a clinical orchestrator rather than an at-risk payer. The revenue model for prescribing is expected to be priced above the current blended ARPU of approximately $293 per member per year, reflecting the higher clinical intensity and regulatory infrastructure required for prescribing oversight.

The key analytical point about the prescribing capability is that management has explicitly excluded any revenue contribution from GLP-1 prescribing, FlexCare, and the cholesterol programme from the FY2026 revenue guidance of $312-322 million. The guidance is built entirely on existing programme lines with known enrolled member populations and historical renewal rates, it is, in management’s characterisation, a conservative baseline anchored on proven performance.

If the prescribing capability, FlexCare, and cholesterol programmes collectively generate $15-30 million of incremental revenue in the second half of FY2026, a modest assumption given the initial cholesterol rollout at a 300,000-employee account and the established GLP-1 Care Track installed base, the actual FY2026 revenue outcome could be in the range of $327-352 million, implying 26-36% growth and potentially closing a significant portion of the gap between the guided deceleration and the prior-year trajectory.

5. Distribution Moats & Competitive Landscape

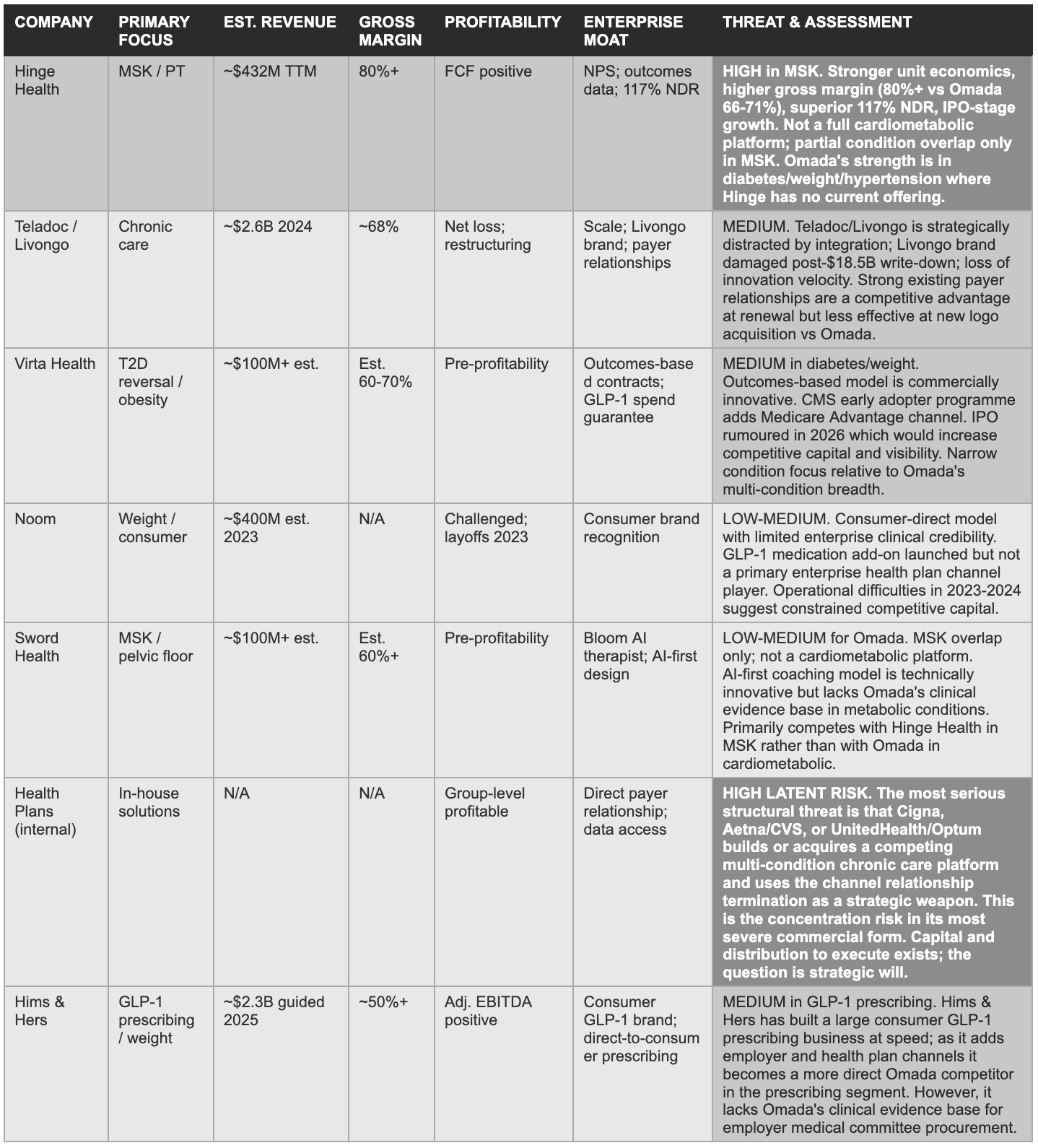

Omada's durable advantages are evidence-institutional and regulatory: CDC DPP recognition, NCQA and URAC accreditations, and 30 peer-reviewed publications form a procurement prerequisite stack that competitors cannot shortcut regardless of capital. Hinge Health represents the most credible near-term competitive threat, with superior MSK unit economics and a 117% NDR. The deeper structural risk comes from health plan channel partners who possess the data, the employer relationships, and the financial incentive to build competing programmes in-house.

Moat architecture: What is and is not defensible

The CDC National Diabetes Prevention Program recognition is the most durable single competitive asset in Omada’s portfolio. It designates Omada’s prevention programme as a CDC-approved DPP delivery organisation, which is the prerequisite for reimbursement under the ACA’s preventive services mandate, the mechanism that allows the programme to be offered to enrolled members at zero cost. A virtual DPP provider without CDC recognition must either charge members directly (severely impairing enrolment rates) or navigate a different and more complex reimbursement pathway that does not deliver the zero-cost enrolment economics that make the programme commercially viable at employer scale.

The recognition process requires a multi-year track record of delivering outcomes consistent with the DPP protocol standards, meaning that a competitor entering the virtual DPP market in 2025 will begin the recognition process at zero and achieve it, at the earliest, in 2028 or 2029. By that point, Omada will have had CDC recognition for approximately a decade, with the commercial evidence base and enrolled member relationships that accompany that tenure.

The NCQA and URAC accreditations function as procurement-channel filters: several large national health plans require these accreditations as conditions of vendor panel inclusion. The practical effect is that a digital health company that lacks these accreditations cannot be offered by those health plans to their employer clients as a covered benefit, regardless of the quality of its technology or outcomes data.

Obtaining these accreditations requires building the clinical quality infrastructure that the accrediting bodies require, and maintaining them requires ongoing operational investment and periodic re-certification audits. A well-capitalised competitor can clear these barriers, but the minimum lead time runs to 12-24 months and ongoing compliance cost that raises the effective minimum scale required to make entry into the health plan channel economically rational.

The clinical evidence base of 30 peer-reviewed publications is the most commercially active moat in the day-to-day enterprise procurement process. When a self-insured employer’s benefits committee evaluates a chronic disease management vendor, the medical director will typically request outcome studies published in peer-reviewed journals as a prerequisite for committee consideration.

The response time for that request is measured in days or weeks; building the evidence base required to satisfy it is measured in years. A competitor without peer-reviewed publications of comparable breadth and depth cannot pass the medical director’s preliminary filter, regardless of the quality of its member experience or the sophistication of its AI capabilities. This filter is the practical expression of Omada’s clinical credibility moat in the procurement cycle.

The medical spend billing classification is a commercial moat rather than a technical one: it reflects the combination of the CDC recognition, the NCQA and URAC accreditations, and the peer-reviewed clinical evidence that collectively enable Omada to argue, and to substantiate before employer benefits and medical committees, that its fees constitute clinical healthcare services qualifying for medical spend treatment under self-insured employer plan design.

This classification is not granted automatically; it requires the clinical credentialing that Omada has built over 13 years. A technology company entering the chronic disease management market with a software product positioning and limited clinical evidence cannot claim medical spend treatment for its fees without the same credentialing infrastructure, and without medical spend treatment, the willingness-to-pay gap between Omada and a technology-positioned competitor creates a significant pricing premium that Omada can sustain as long as its clinical differentiation is credible.

Competitive landscape: Assessment by category

The digital chronic care competitive landscape in 2026 has bifurcated in a way that is analytically instructive for Omada’s investment case. The single-condition point solutions have faced severe commercial pressure as employers have rationalised their vendor relationships in favour of consolidated multi-condition platforms.

Teladoc’s 2020 acquisition of Livongo for $18.5 billion and the subsequent $13.4 billion impairment charge in 2022 is the most visible cautionary tale: Livongo was the dominant single-condition diabetes management brand, with compelling outcomes data, strong NPS scores, and enterprise contract momentum, but Teladoc’s integration thesis failed to create the multi-condition clinical platform that employers were increasingly demanding, and the combined entity has been operationally and financially distressed since the write-down.

In contrast, companies that have built genuine multi-condition or multi-modality platforms, like Hinge Health in MSK, Virta Health in diabetes reversal, and Omada in cardiometabolic management, have maintained or improved their commercial positioning through the sector rationalisation.

The Teladoc/Livongo failure mode: Lessons for Omada

Teladoc’s acquisition of Livongo in 2020 for $18.5 billion is the analytical reference case that every digital chronic care investor must engage with. Livongo was, in 2020, the strongest enterprise digital health company in the United States: dominant brand recognition in diabetes management, NPS scores that routinely exceeded traditional healthcare benchmarks, peer-reviewed clinical outcome evidence, a 150% net dollar retention rate that implied extraordinary account expansion dynamics, and enterprise contract momentum with major self-insured employers and health plans.

The Teladoc acquisition thesis was that combining Livongo’s chronic care management with Teladoc’s acute and primary care virtual platform would create a comprehensive virtual care system capable of capturing the full spectrum of a member’s healthcare needs, preventing the chronic disease deterioration that drives emergency and acute care utilisation, while simultaneously serving the acute and primary care needs that chronic disease patients generate at higher rates than the general population.

The thesis was strategically coherent but operationally unfounded. The integration was plagued by product roadmap conflicts between teams that had built fundamentally different technology architectures, cultural friction between organisations with different operating philosophies, and management departure at the Livongo leadership level that removed the institutional knowledge required to execute the combined platform vision.

The result was a $13.4 billion impairment charge in 2022, a write-down that effectively acknowledged that the combined entity was worth approximately $5.1 billion less than the acquisition price, representing one of the largest value destructions in digital health M&A history. Teladoc’s stock declined approximately 96% from its February 2021 all-time high to its 2023 lows, and the company has been engaged in a multi-year restructuring and segment reorganisation ever since.

The lesson for Omada’s investment thesis are two.

First, the failure of Livongo as an independent entity was integration-driven rather than a clinical model failure. The Livongo diabetes management programme was clinically effective and commercially differentiated; Teladoc’s integration thesis created the damage, driven by product roadmap conflicts and the strategic decision to merge with an organisation whose priorities were incompatible with the clinical programme’s operational requirements. Omada, as an independent public company with a CEO who has led it for 13 years and a management team whose incentives are aligned with sustained independent growth, is not structurally subject to the same integration failure risk.

Second, the Teladoc/Livongo collapse removed the most well-capitalised and most credentially impressive competitor from the enterprise chronic care market. The companies and relationships that were Livongo’s before the Teladoc acquisition are now available to Omada, and the disruption to Livongo’s customer relationships in the 2021-2024 period created switching windows that Omada and others were positioned to exploit. The 12 consecutive quarters of product revenue growth that Ouster delivered through adversity, while Luminar collapsed, has an analogue in Omada’s ability to grow through the period that destroyed most of its digital health peers.

6. AI & Technology: OmadaSpark, Meal Map & Whether ‘Compassionate Intelligence’ Is a Durable Moat

Omada's AI position rests on a proprietary longitudinal dataset spanning tens of millions of care team messages and billions of data points across thirteen years and two million members, the training foundation that produced a 24% email enrolment rate improvement in 2025. The honest analytical tension is that large language model capabilities are commoditising at a pace that narrows the marginal quality gap between proprietary fine-tuning and commodity foundation models. AI is a genuine product improvement driver today; whether it becomes an irreplicable competitive moat depends on how quickly Omada can extend its data advantage before commodity models close the gap.

The proprietary data advantage

Omada’s most credible AI-specific competitive asset is its proprietary longitudinal dataset, which management disclosed on the Q4 2025 earnings call encompasses tens of millions of care team messages and billions of data points accumulated across more than a decade of member engagement and two million total members served since launch. This dataset covers the full spectrum of chronic disease management interactions: weight tracking, blood glucose readings, blood pressure measurements, food logs, medication adherence records, care team message content, engagement pattern data, and outcome trajectories across prediabetes, diabetes, hypertension, weight health, and MSK programmes.

Building a comparable dataset requires years of operating history with enrolled member populations who have consented to data use for programme improvement, and the specific interaction patterns and outcome trajectories that characterise effective chronic disease management in a virtual coaching context remain absent from any publicly available dataset.

The commercial application of this data advantage is most visible in the enrolment rate improvement: management cited a 24% improvement in email enrolment rates attributable to AI-driven personalisation in the Q4 2025 earnings call. In the Omada model, enrolment rate is the single most important operational lever for margin improvement, because eligible covered lives already exist within contracted customer accounts and the incremental cost of converting an additional eligible life to an enrolled member is near zero relative to the cost of adding a new customer account.

A 24% improvement in enrolment rate, if sustained and extended across the full covered lives base of 25 million, would generate a material increase in enrolled members and therefore in recurring PEPM revenue without requiring any additional sales force investment or new customer contract.

The engagement durability metrics disclosed by management provide further evidence of the data advantage in action: more than 55% of members in their twelfth month and more than 50% in their twenty-fourth month engaged with the platform at least once monthly in 2025. In the chronic disease management context, 12-month and 24-month engagement rates are the leading indicators of the clinical outcome durability that drives health plan formulary placement and employer contract renewal decisions.

A competitor without the longitudinal data required to optimise the personalisation features that drive engagement sustainability at 12 and 24 months will face a structurally lower engagement rate, which will translate into worse outcome data, weaker renewal rates, and a less compelling clinical evidence base for future enterprise procurement.

OmadaSpark and Meal Map: Current product capabilities

OmadaSpark is an AI-powered digital coaching assistant that delivers wellness education, habit formation coaching, and motivational content to members between scheduled care team interactions. It functions as an always-available supplement to the human coach relationship, providing on-demand responses to health questions, habit tracking prompts, and educational content tailored to the member’s specific programme and condition history.

Meal Map is an AI-enabled dietary tracking and guidance tool that uses image recognition and nutritional database integration to allow members to track food intake through photographs rather than manual nutritional logging, a significant reduction in the friction of dietary compliance monitoring that historically limited the utility of food tracking as a clinical tool.

Both products were launched in 2025, and management reported that members who have used OmadaSpark and Meal Map demonstrate materially higher levels of ongoing engagement and return to the application more frequently than those who have not yet used the tools. This engagement improvement is the leading indicator of the retention improvement that flows into renewal rates and net dollar retention, the financial metric most directly linked to the long-term gross margin improvement story.

The care team augmentation dimension of Omada’s AI investment is less visible to outside investors but may be more consequentially economically. Management disclosed that AI tools for care team members, assistants that help coaches identify members at risk of disengagement, prioritise outreach, suggest personalised intervention content, and document clinical interactions more efficiently, are deployed across the Omada care team platform.

The economic significance of care team AI augmentation is straightforward: the primary operating cost in the PEPM business model is care team staffing, and any productivity improvement in care team efficiency directly improves the cost of goods sold per member and therefore gross margin. If AI augmentation enables each health coach to manage a 20-30% larger member population with equivalent or better engagement quality, the gross margin improvement from care team efficiency gains could be material over a 12-24 month horizon, independent of any revenue growth.

The commoditisation risk: An honest assessment

The bear case for Omada’s AI competitive position is direct and cannot be dismissed: large language models capable of generating personalised health coaching content, dietary guidance, motivational support, and clinical question responses are now available at near-zero marginal cost via API from OpenAI, Anthropic, Google, and others.

A well-funded competitor, or a large PBM building an in-house GLP-1 companion programme, can integrate state-of-the-art foundation model capabilities into a digital coaching application in months rather than years, without the multi-year investment in proprietary dataset construction that Omada has made. The barrier to building an AI coaching assistant that is subjectively indistinguishable from OmadaSpark for a general health-literate audience has dropped dramatically in the past two years.

The counterargument (that Omada’s proprietary longitudinal dataset provides a training advantage that commodity models cannot replicate) is credible but requires qualification. The relevant question is not whether Omada’s AI models, fine-tuned on its proprietary data, are better at general health coaching than a foundation model accessed via API. The relevant question is whether the marginal quality improvement from Omada’s proprietary data is large enough to be a meaningful driver of member enrolment, engagement, and outcome decisions relative to a competitor using commodity foundation model capabilities.

In tasks such as nutrition guidance, habit formation coaching, and motivational support for behaviour change, the performance of commercial foundation models is already competitive with human coaching at a general level, and the gap between foundation model performance and Omada’s fine-tuned performance may be smaller in practical terms than the data asset framing suggests. AI is a meaningful product improvement lever for Omada in 2026 but is not yet a decisive irreplicable moat, and its contribution to competitive differentiation is most credible in the specific clinical context of multi-year outcome management. AI cannot yet optimise without the longitudinal training data that Omada possesses.

7. Financial History & The Revenue Deceleration Question

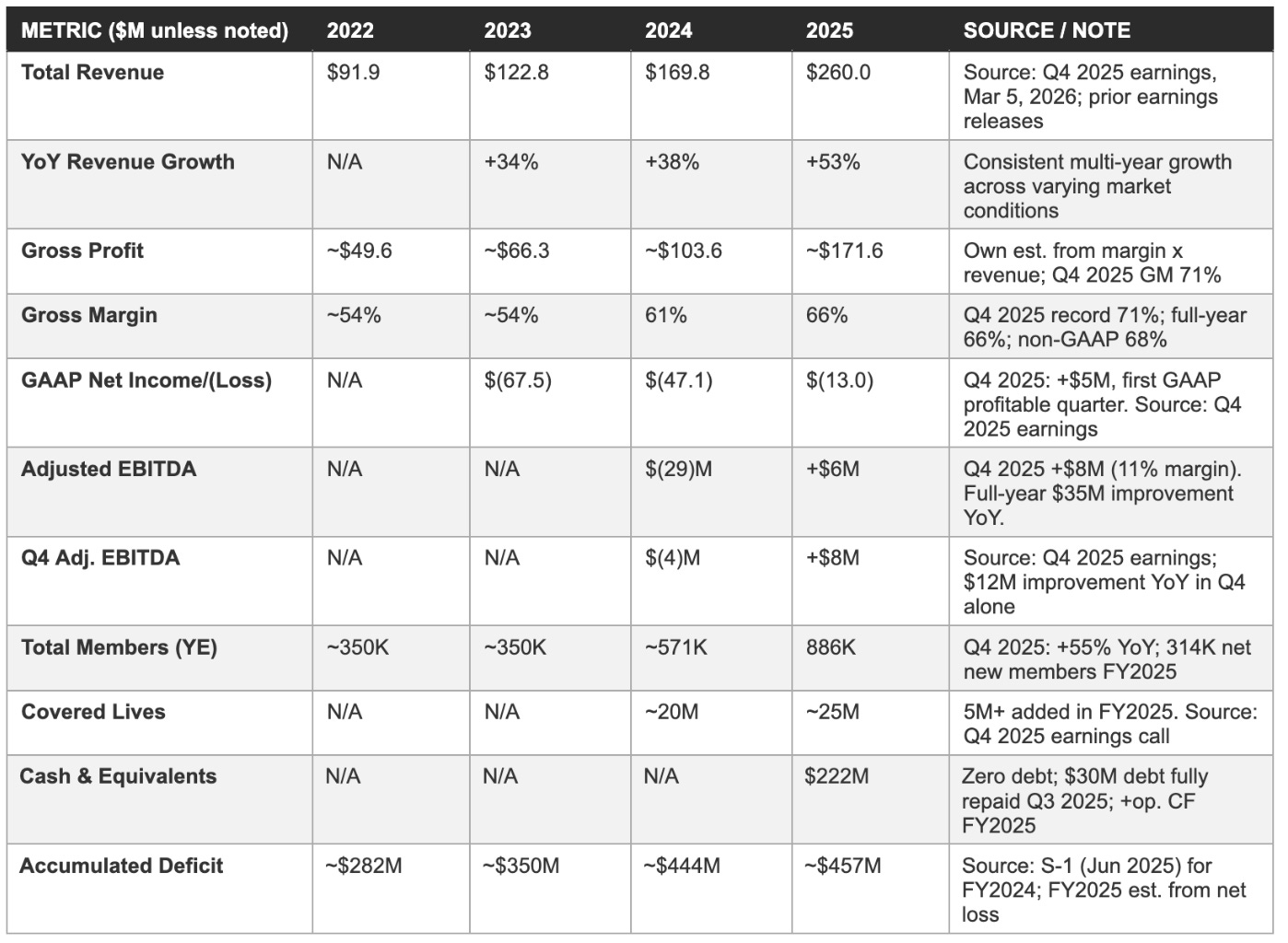

Revenue compounded at 34%, 38%, and 53% across 2022-2025, gross margin expanded from 54% to 71% in Q4, and adjusted EBITDA swung from -$29 million to +$6 million in a single year, a $35 million improvement that confirms the model generates operating leverage at scale. The FY2026 guidance of 22% growth triggered a 15% post-earnings stock decline and the narrative the current price is pricing. Five distinct analytical frames are required to assess whether that guidance represents conservative anchoring or genuine deceleration, and they point in different directions.

Quarterly revenue progression: The 2025 acceleration

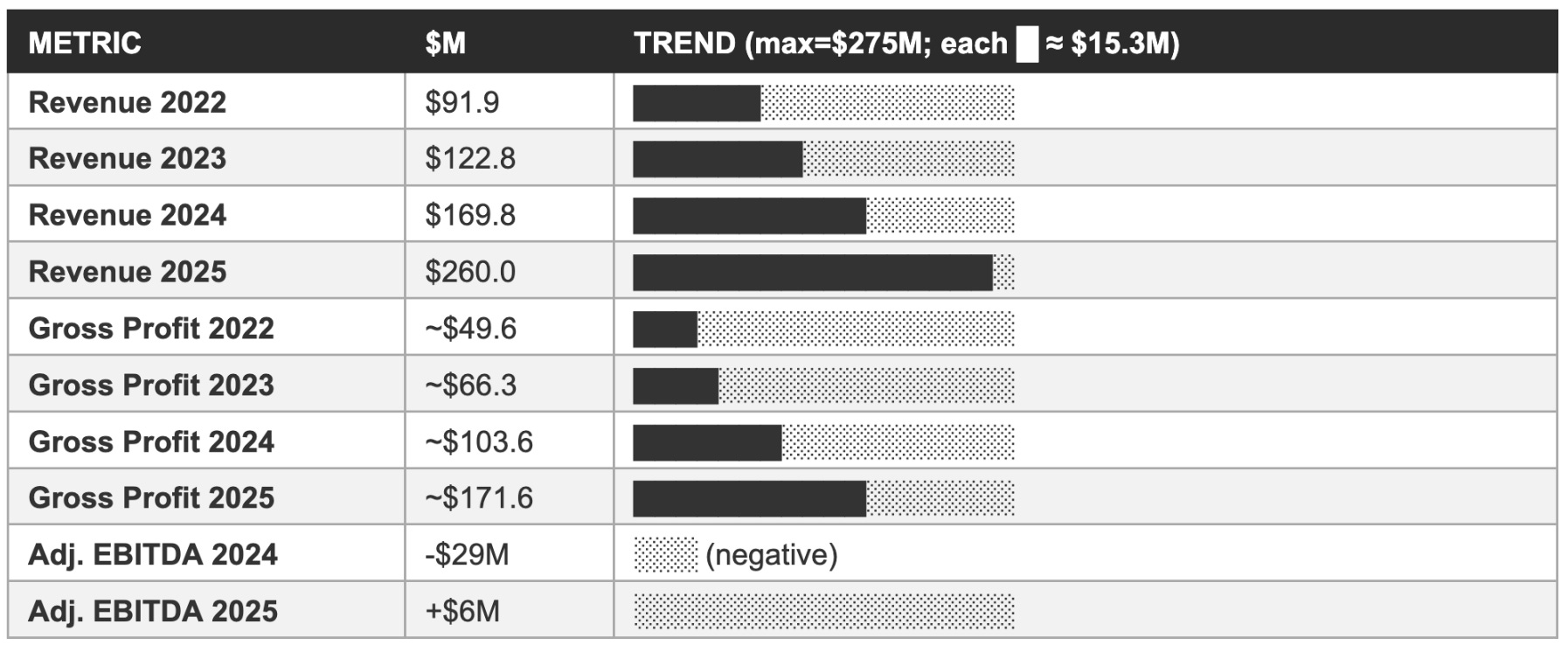

The quarterly revenue progression through 2025 is important because it contextualises both the full-year achievement and the FY2026 guidance. Q1 2025 revenue was $55.0 million (up 49% year-over-year), Q2 2025 was $61.4 million (up 49%), Q3 2025 was $68.0 million (up 49%), and Q4 2025 was $76.0 million (up 58%). The full-year total of $260.0 million represented 53% growth. The sequential acceleration from Q3 to Q4, 49% to 58% year-over-year, is the most recent data point in the trajectory and is inconsistent with a narrative of structural demand deceleration.

The Q4 2025 beat relative to the January 2026 preliminary revenue announcement ($72-74 million) of approximately $2-4 million further suggests that demand conditions entering Q4 were stronger than even management’s contemporaneous assessment. The FY2026 guidance of $312-322 million implies a Q4 2026 quarterly run-rate of approximately $85-90 million (assuming back-half weighting consistent with the membership enrolment cycle), which is a sequential increase from the $76 million Q4 2025 result and not a sequential revenue decline at any point in the guided trajectory.

The Q3 2025 earnings call was the first quarter in which Omada delivered positive adjusted EBITDA as a public company: $2.38 million at the adjusted EBITDA level versus a loss in the prior year period. Management raised full-year FY2025 guidance on the Q3 call from $235-241 million to $251.5-254.5 million, and adjusted EBITDA guidance from a loss of $9-5 million to a range of -$2 million to breakeven, guidance that management ultimately beat decisively, with the full-year result of +$6 million adjusted EBITDA versus the guided -$2M to breakeven range.

This pattern of raising guidance and then beating the raised guidance is the empirical foundation for the conservative guidance culture characterisation: a management team that raised guidance twice in 2025 and then beat the second raise by approximately $6 million on adjusted EBITDA has demonstrated a systematic tendency to guide below its actual delivery.

Income statement progression: 2022 through 2025

Revenue and gross profit trend: Visual comparison

The deceleration question: Five analytical frames

The 22% FY2026 revenue growth guidance that management provided on the March, 2026 earnings call requires five distinct analytical frameworks to evaluate properly, and investors who apply only one or two of them will reach systematically biased conclusions about the investment case.

The first analytical frame is absolute dollar growth. The 22% growth guidance on a $260 million base implies approximately $57 million of incremental revenue in FY2026. In absolute dollar terms, this is larger than the incremental revenue added in any prior year: 2025 added approximately $90 million of incremental revenue (vs. $58 million in 2024, $47 million in 2023), so FY2026’s $57 million incremental is a decline from 2025’s exceptional absolute growth but is in line with 2024. The percentage deceleration is mathematically inevitable at larger absolute revenue scales; the question is whether the dollar growth trajectory, not the percentage growth trajectory, is consistent with the multi-year valuation case.

The second analytical frame is guidance construction methodology. Management has established a clear conservative guidance culture in its first full year as a public company: it raised 2025 guidance twice (from $222 million to $235-241 million to $251.5-254.5 million to the final $260 million actuals). The FY2026 guidance of $312-322 million was explicitly stated to exclude any revenue contribution from three new programme categories: GLP-1 prescribing, GLP-1 FlexCare, and the cholesterol management programme. If these three categories collectively generate even $15-30 million of revenue in the second half of FY2026, a modest assumption given the initial cholesterol rollout at a 300,000-employee account and the established GLP-1 Care Track member base, the actual FY2026 result could be $327-352 million, implying 26-36% growth rather than the guided 22%.

The third analytical frame is the seasonal enrolment cycle. Omada’s member base adds the majority of net new members in Q1 of each year, when new employer contract cohorts open for enrolment at the beginning of the plan year. Members enrolled in Q1 contribute a full year of PEPM revenue in the subsequent 12 months, while members enrolled in Q3 or Q4 contribute only one to two quarters of PEPM revenue in the year of enrolment. The FY2026 guidance implicitly reflects this seasonality: Q1 2026 guidance of $72-75 million is lower than Q4 2025’s $76 million in absolute terms, reflecting the period before new Q1 enrolments accumulate, but the full-year guidance midpoint of $317 million implies significant back-half acceleration as the Q1 2026 enrolment cohort’s PEPM revenue accretes through the year.

The fourth analytical frame is the covered lives versus penetration rate dynamic. Omada ended 2025 with 25 million covered lives and 886,000 enrolled members, an effective penetration rate of approximately 3.5% of covered lives. If the Q1 2026 enrolment season adds another 5 million covered lives through new contract wins (consistent with the 5 million added in 2025), but the enrolment rate on those new covered lives is only 2-3% in the first year, the incremental revenue contribution from the new covered lives in FY2026 is modest relative to the total revenue base. The path to sustained high-percentage growth on a $260 million base requires either meaningful penetration rate improvement in existing covered lives (which the 24% email enrolment rate improvement suggests is occurring) or significant net new covered life additions that start generating revenue in the same fiscal year they are contracted.

The fifth analytical frame is the concentration risk normalisation. The two PBM/health plan partners that represented approximately 60% of Q1 2025 revenue are the most important variables in the FY2026 revenue outcome, and they are the variables investors cannot directly observe. If the commercial relationships with these partners are stable or growing then 22% growth guidance represents conservative guidance that has material upside probability. If either relationship has been renegotiated at lower pricing or lower scope, the FY2026 guidance may already incorporate that headwind, and the underlying organic growth from the diversified base of 2,000+ customers may be stronger than the aggregate guidance implies. The 2025 10-K concentration disclosure, expected in April 2026, is the first data point that will allow investors to assess whether the concentration level is improving, stable, or worsening.

8. Forward Financial Model: Bear / Base / Bull Through FY2028

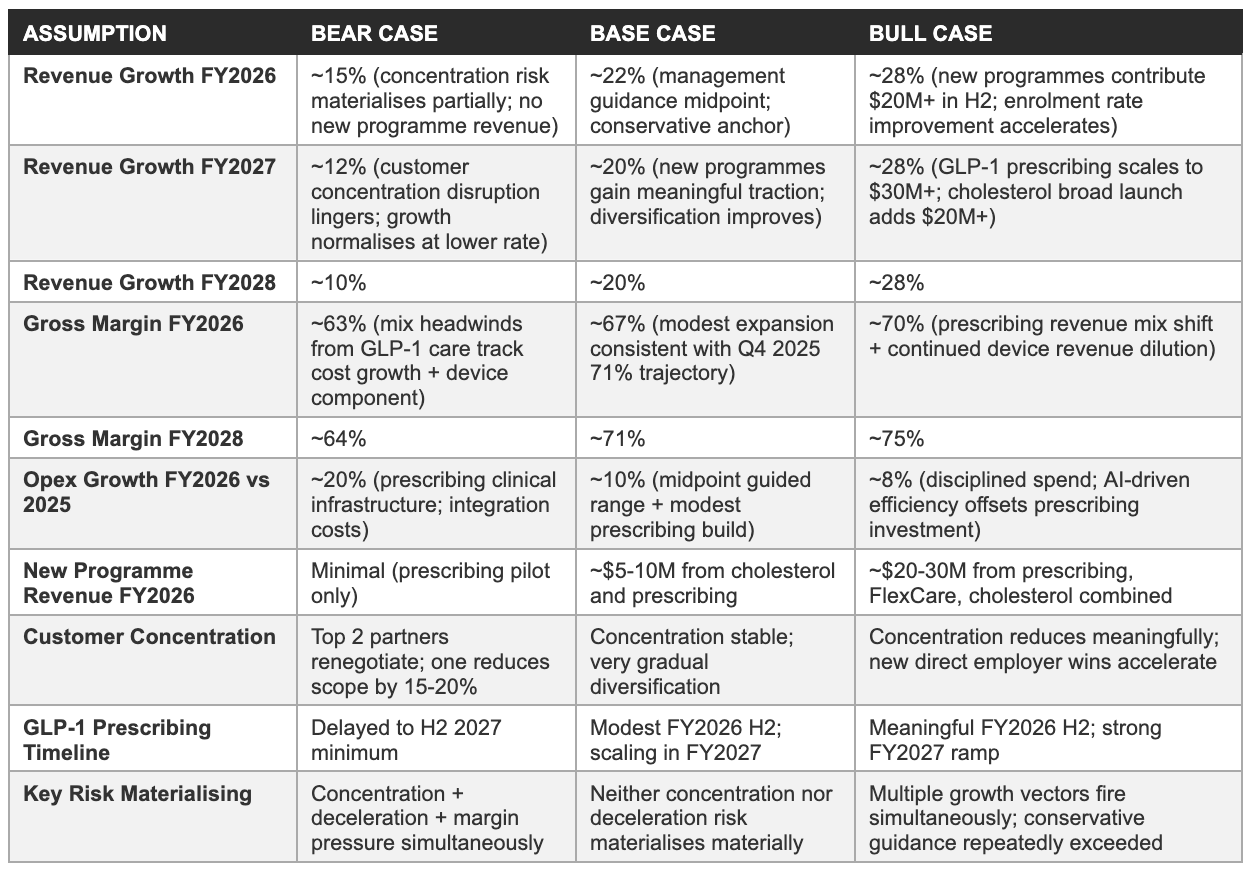

The three scenarios below are anchored to management's FY2026 guidance of $312-322 million revenue and $7-15 million adjusted EBITDA, with FY2027 and FY2028 projections layered on top. New programme revenue from GLP-1 prescribing, FlexCare, and cholesterol is excluded from the base case in FY2026, consistent with management's own guidance construction. All forward estimates are our own projections; the bear case receives the same analytical rigour as the bull case.

Model assumptions

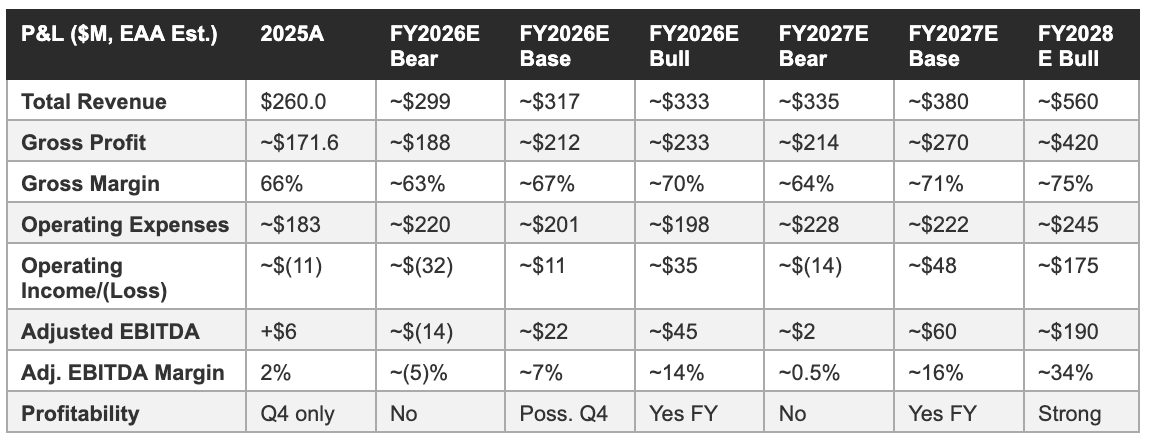

Three-year P&L projection

Cash runway analysis

Omada ended 2025 with $222 million in cash and cash equivalents and zero debt, having fully repaid its $30 million debt facility during Q3 2025. The company generated positive operating cash flow in 2025, confirming that the adjusted EBITDA positive trajectory has translated into actual cash generation rather than merely accounting improvement. Management’s stated objective is to reach sustained positive cash flow from operations, a threshold that the base case model suggests is achievable in FY2027 given the $60 million adjusted EBITDA projection under that scenario, which would translate to positive operating cash flow after working capital adjustments and capital expenditure.

In the bear case, where adjusted EBITDA is approximately $2 million in FY2027 and operating cash flow may still be modestly negative after working capital and capex, the $222 million cash position provides a substantial buffer: even consuming $30-40 million per year in net cash (which would represent a significantly worse outcome than the 2025 operating cash flow generation), Omada would have sufficient runway to reach FY2030 without requiring additional capital. The bear case does not create an immediate solvency risk; it creates a dilution risk if the company is forced to access capital markets at a depressed valuation to fund a prolonged period of below-guidance performance. The $222 million cash cushion is the primary reason that dilution risk is rated LOW-MEDIUM in the risk matrix rather than HIGH despite the operating losses history.

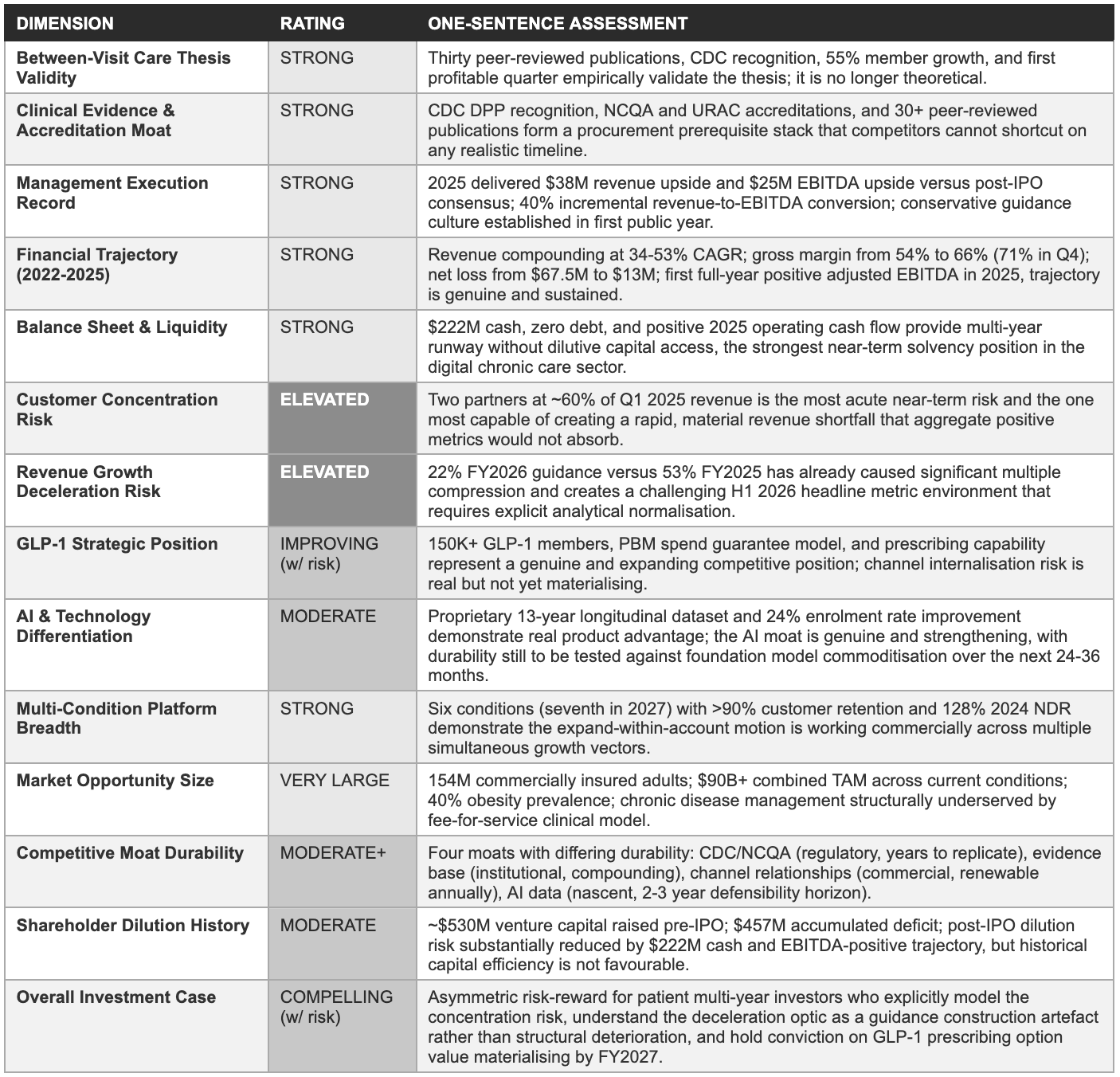

9. Risk Matrix

Each risk below is a specific variable whose outcome determines which of the three Section 8 scenarios is realised. Probability reflects likelihood of a significant negative outcome within 24 months; severity reflects the degree of long-term impairment if it materialises. Risks are ordered by the combined weight of both dimensions.

10. The Implied Valuation Question: What Does ~$850M Market Cap at ~$14.50 Require Omada to Deliver?

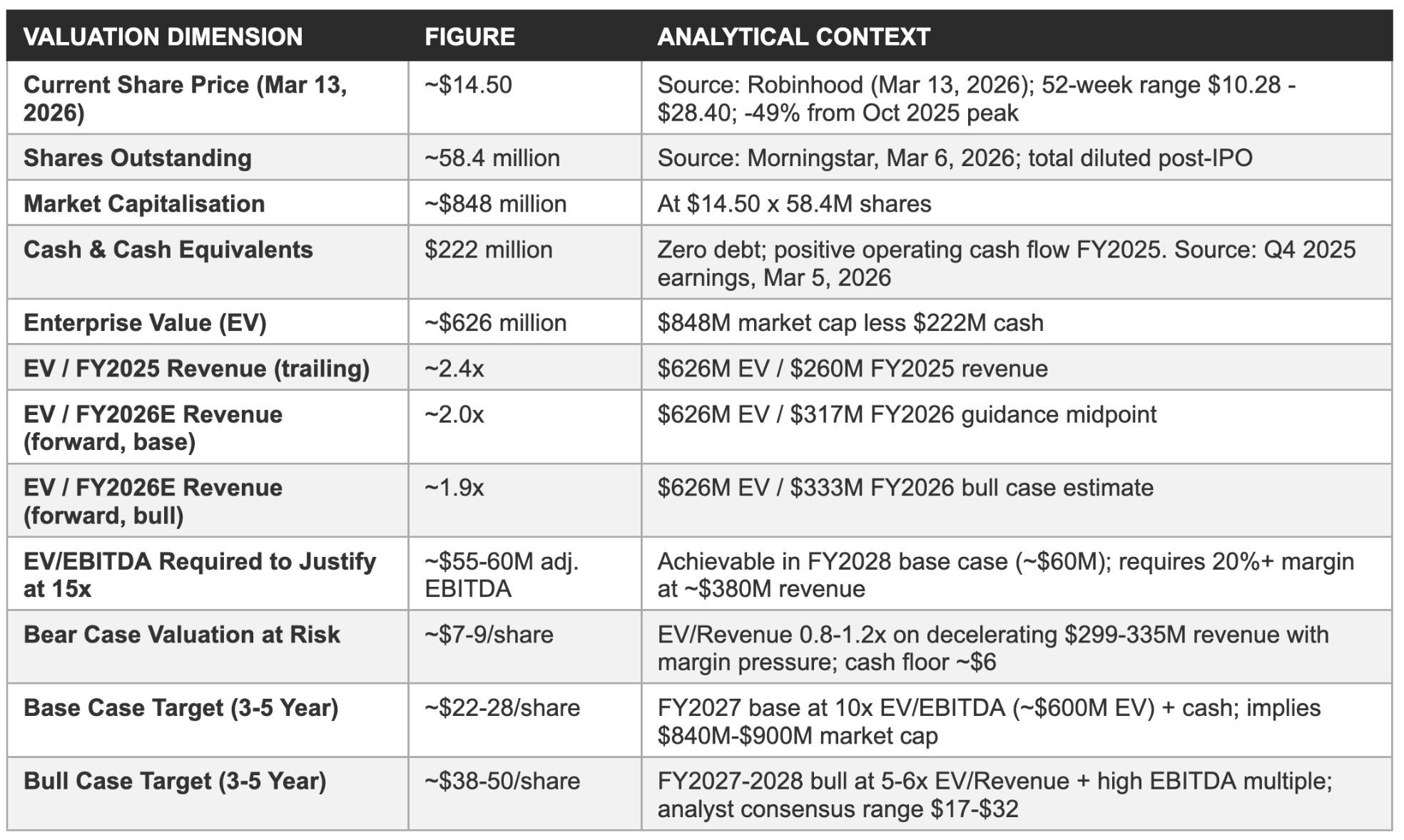

At approximately $14.50 per share, Omada trades at roughly 2.0x forward enterprise value to revenue, a multiple that implies the market has priced in meaningful probability of the bear case, sustained sector-wide multiple compression from the 2021-2023 digital health de-rating, or both. The company reported a $13 million net loss in 2025; the current $626 million enterprise value is a forward claim on what the business will deliver across the next three to five years. The analytical discipline is to calculate explicitly what that claim requires.

Revenue multiple context

The EV/revenue multiple provides an imperfect but useful reference frame for assessing how much of the bull, base, or bear case is embedded in the current share price. At $14.50 per share and $222 million in cash, the enterprise value of approximately $626 million represents 2.4x 2025 trailing revenue of $260 million and approximately 2.0x the FY2026 guidance midpoint of $317 million. These are historically low multiples for a digital health platform company delivering 22-53% annual revenue growth with 66-71% gross margins and a trajectory toward 20%+ adjusted EBITDA margins.

The primary comparable transactions and trading multiples in the digital health space, Hinge Health at approximately 4-6x forward revenue in its pre-IPO rounds, Teladoc/Livongo at the time of acquisition at approximately 15x forward revenue, and Virta Health at approximately 6-8x revenue in its most recent private financing, all suggest that the 2.0x current multiple is below the range that similar businesses have commanded at similar stages of commercial development.

The obvious counterargument is that the digital health sector has undergone a structural de-rating since the 2021 peak valuations: Teladoc’s implosion, Noom’s operational struggles, the Series D and late-stage venture correction, and the disappointing performance of most 2021 digital health IPOs have collectively made investors deeply sceptical of elevated digital health multiples. Omada is being repriced in the context of that scepticism, not against the 2021 market conditions.

At 2.0x EV/forward revenue, the current multiple implies that the market requires substantial additional evidence of execution before it is willing to rerate the stock, and that the Q4 2025 earnings beat alone was insufficient to trigger that rerating. The guidance deceleration on the same earnings call may have reinforced rather than resolved the scepticism.

The implied milestone: What revenue and EBITDA are required?

For the current (approx) $850 million market capitalisation to be rational at a 3-5 year investment horizon, Omada must achieve a revenue and profitability milestone combination that a reasonable investor would value at $850 million or more in present value terms. At a 15x EV/EBITDA multiple, Omada needs to generate approximately $55-60 million in adjusted EBITDA annually to justify the current enterprise value. Against the base case FY2028 adjusted EBITDA estimate of approximately $60 million, that target is achievable within the modelling horizon. Against the bear case scenario, the five-year horizon offers a materially more constrained path to that threshold.

An alternative framing uses EV/revenue: at a 5x EV/forward revenue multiple Omada would need to achieve approximately $125 million in EV to justify the current multiple (note: current EV is already $626M, so this framing implies the market requires the stock to grow to justify the current price only at a higher multiple).

The more useful calculation is the forward price: if Omada achieves $380 million in FY2027 revenue (base case) with a 20%+ adjusted EBITDA margin (approximately $76 million EBITDA), and the market assigns a 10x EV/EBITDA multiple at that point, the implied enterprise value is approximately $760 million, plus the $222 million cash balance (reduced by cumulative cash consumption), implying a market capitalisation of approximately $900-950 million versus today’s $850 million, a modest return that explains why the bull case, which requires higher revenue growth and margin achievement, is required to justify a materially higher share price.

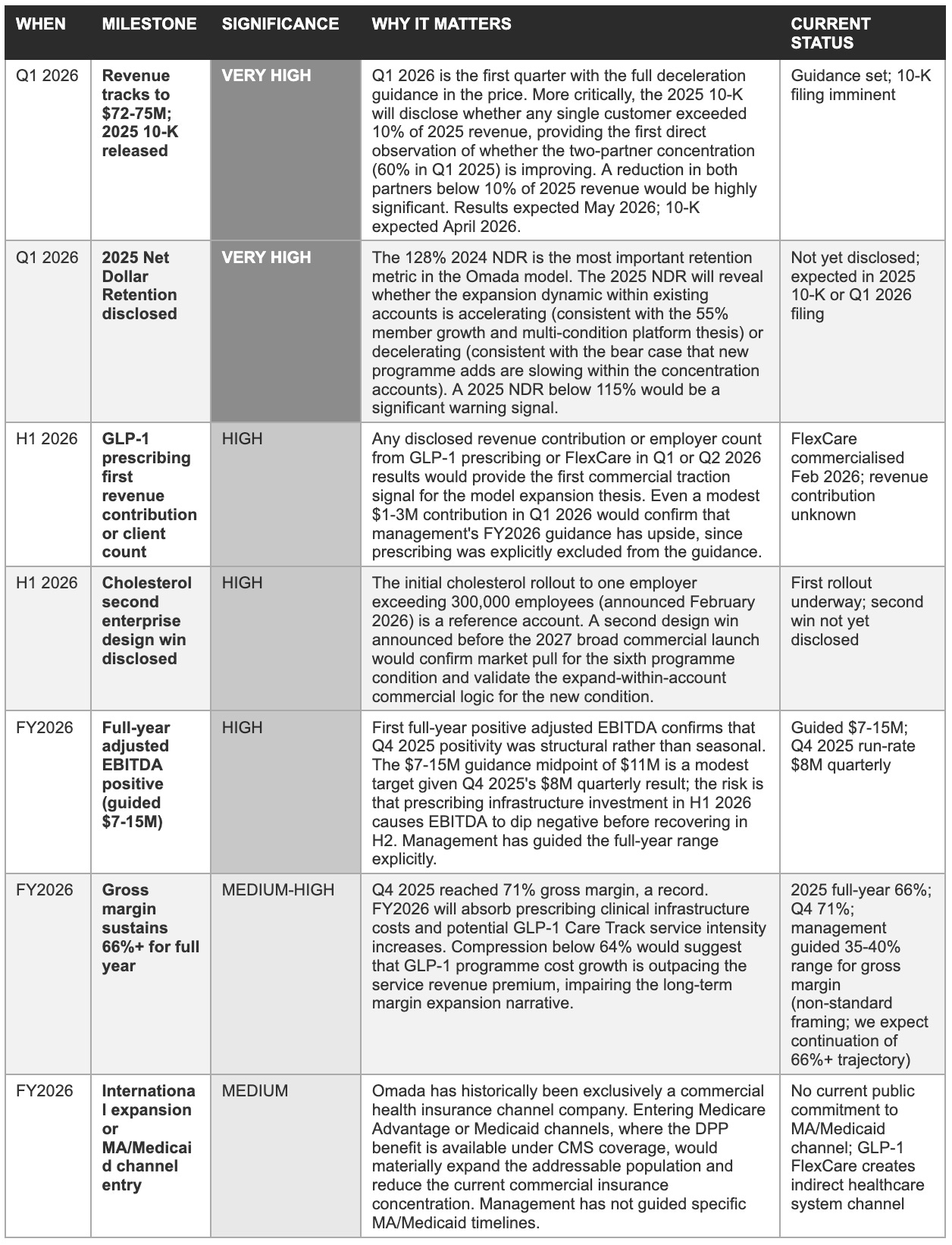

11. Milestone Tracker: What to Watch in 2026-2028

Management's three stated priorities for 2026, platform expansion through prescribing and cholesterol, AI-driven enrolment improvement, and progress toward 20%+ adjusted EBITDA margins, translate into a specific set of observable proof points. The 2025 10-K concentration disclosure and the Q1 2026 revenue result are the two highest-stakes near-term observations; everything else is secondary until those are resolved.

12. Opinion & Investment Perspective: Bull, Base & Bear Cases

What follows is our analytical view as of March 2026, not an investment recommendation, but an attempt to present the bull, base, and bear cases with equal rigour. At a price roughly 50% below its October 2025 peak, the bear scenario has attracted serious market weighting and deserves the same analytical depth as the bull case.

The bull case: Four pillars

The first pillar is the financial trajectory credibility. Omada delivered 53% revenue growth in 2025 to reach $260 million, while simultaneously achieving its first full-year positive adjusted EBITDA of $6 million and its first profitable quarter (Q4, +$5 million net income). The company beat post-IPO analyst consensus by $38 million on revenue and $25 million on adjusted EBITDA in its first full year as a public company, the single most important datapoint in evaluating management’s guidance credibility.

The adjusted EBITDA improvement from -$29 million in 2024 to +$6 million in FY2025, a $35 million year-over-year swing, demonstrates operating leverage that the bear case cannot analytically dismiss. CFO Steven Cook’s disclosure that the business converted approximately 40% of incremental revenue to the adjusted EBITDA line in 2025 confirms that the operating leverage is structural: as revenue grows faster than operating expenses, the EBITDA margin expands arithmetically, and the trajectory from 2% adjusted EBITDA margin in 2025 toward the long-term 20%+ target is credible given the scale of the revenue base against which that leverage compounds.

The second pillar is the clinical evidence and accreditation moat stack. Thirty peer-reviewed publications, CDC National DPP recognition, NCQA and URAC accreditations, and 13 years of enterprise customer relationships form a procurement prerequisite architecture that competitors cannot shortcut with capital investment on any realistic timeline. The clinical evidence base functions as the filter through which enterprise health plan and employer procurement decisions are made. A competitor entering the enterprise cardiometabolic management market in 2026 begins its peer-reviewed publication timeline at zero and its CDC DPP recognition process at zero, and will not have a comparable evidence base before 2030 at the earliest.

The combination of this evidence depth with the medical spend billing classification that it enables, routing procurement to clinical committees rather than technology buyers, achieving medical budget treatment rather than software budget treatment, and creating renewal incentive structures aligned with clinical outcomes rather than feature satisfaction, is the structural origin of the 90%+ three-year customer retention rate the business has demonstrated across its commercial history.

The third pillar is the GLP-1 structural positioning. Omada is one of the few digital health companies that is positioned to benefit from GLP-1 medication adoption rather than being disrupted by it. The 150,000 members supported on GLP-1s at year-end 2025 (up from 50,000 at year-end 2024) represents a tripling in twelve months, driven by the same employer and health plan channel relationships that are Omada’s primary distribution infrastructure.

The GLP-1 Care Track’s published outcome data, 0.8% average weight change in discontinuing members versus 11-12% in controls, provides the clinical foundation for the spend guarantee contracting model that at least one large PBM partner has offered to employer clients. The prescribing capability and FlexCare product launched in early 2026 deepen Omada’s position from companion vendor to clinical care provider, which is a qualitatively different and more defensible commercial relationship than a pure behavioural support supplement to a PBM’s drug distribution business.

The fourth pillar is the balance sheet strength and cash position. The $222 million cash balance with zero debt and positive operating cash flow provides management with multi-year runway to execute the prescribing capability rollout, the cholesterol programme commercial launch, and the AI investment cycle without being forced to raise dilutive capital at a depressed valuation.

In a sector where counterparty solvency has become a procurement criterion, enterprise employers and health plans conducting vendor due diligence now routinely ask whether their chronic disease management vendor will still be operational in three years, Omada’s balance sheet is a competitive asset in enterprise sales conversations. The ability to commit to multi-year programme continuity without the qualification that this commitment is subject to continued venture funding or successful capital market access is a differentiation that cash-constrained competitors cannot match.

The bear case: Four concerns

The first and most acute bear case concern is the customer concentration structure. Two unnamed PBM/health plan partners representing approximately 60% of Q1 2025 revenue create a vulnerability that the aggregate positive metrics, high net dollar retention, rapid member growth, strong gross margins, tend to obscure, because those metrics are primarily driven by the same concentration accounts. A strategic decision by either large partner to reduce the scope of its Omada relationship, renegotiate pricing below the current level, or accelerate development of a competing in-house solution would create a revenue impact that could not be offset in the near term by growth in the other 2,000+ customer accounts.

The commercial logic for a PBM to make exactly this strategic decision is straightforward: the GLP-1 companion care market that Omada is helping to pioneer is large enough to attract the PBM’s own product development investment, and the combination of the PBM’s drug dispensing data, employer relationships, and clinical data infrastructure represents a compelling basis for building a proprietary companion programme. This risk sits squarely within the natural competitive dynamic that follows from building a valuable market with channel partners who have both the capability and the incentive to internalise it.

The second concern is the FY2026 deceleration narrative momentum. The post-earnings stock decline of approximately 15% in the days following the March, 2026 results demonstrates that the market interpreted 22% guidance as evidence that the hyper-growth phase is ending, regardless of the underlying analytical case for conservative guidance construction. The sequential quarterly comparisons through H1 2026 will present year-over-year revenue growth percentages that are materially lower than 2025’s 49-58% quarterly range, because the 2025 comparator period was the high-growth acceleration phase, and analysts and investors who do not explicitly model the absolute dollar growth trajectory will read decelerating percentage growth as deteriorating commercial quality.

In a market that has already demonstrated deep scepticism about digital health business models following the Teladoc/Livongo debacle and the Noom operational struggles, the sentiment dynamics of headline metric deceleration can create price pressure that is disconnected from business fundamentals but real in its share price impact. Management has pre-guided this dynamic explicitly; the business fundamentals are intact. The risk concentrates in the multiple, which is the most important variable determining whether investors who purchase at the current $14.50 price generate satisfactory returns over a 3-5 year horizon.