Ouster, Inc.

The Platform Bet: Digital Lidar, the StereoLabs Acquisition, and Whether Ouster Can Win the Physical AI Infrastructure Race Before Capital Patience Runs Out

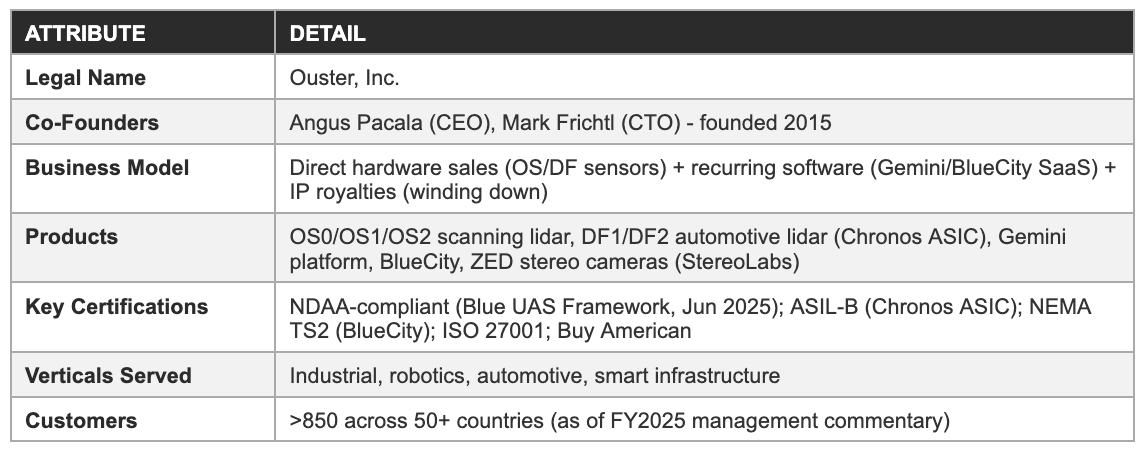

1. Corporate Profile

Ouster, Inc. is not simply a lidar hardware company. It is a decade-long architectural wager, that CMOS semiconductor physics applied to light detection and ranging would follow the same cost and performance trajectory as the digital camera revolution, now entering the phase where that bet either pays off at commercial scale or faces the same reckoning that has consumed most of its Western competitors. The analytical challenge is separating genuine structural improvement from one-time financial tailwinds, and understanding whether the StereoLabs acquisition accelerates the thesis or complicates an already demanding execution agenda.

Ouster is a provider of high-performance digital lidar sensors, perception software, and AI stereo vision cameras. The company serves four commercial verticals: industrial automation, robotics, automotive ADAS, and smart infrastructure. It is the surviving entity of the March 2023 all-stock merger with Velodyne Lidar, Inc. and the 2021 acquisition of Sense Photonics, Inc. Its co-founders, CEO Angus Pacala and CTO Mark Frichtl, have led the company continuously since its 2015 founding, an unusual tenure for a pre-profitability deep-technology hardware company operating in a sector that has claimed Luminar Technologies (Chapter 11, late 2025), AEye, and numerous other Western lidar companies.

Ouster’s core product family is the REV7-generation OS-series scanning digital lidar (OS0, OS1, OS2) and the DF-series ASIL-B automotive lidar built on the custom Chronos ASIC. Its software stack includes Gemini, a real-time perception platform for smart infrastructure deployments, and BlueCity, a Gemini-powered intelligent traffic solution deployed at over 1,200 active sites globally as of Q4 2025 (source: Q4 2025 earnings call, March, 2026). The NEMA TS2 traffic certification held by BlueCity is the only such certification in the lidar industry for safety-critical signal actuation, a meaningful competitive moat in U.S. DOT procurement.

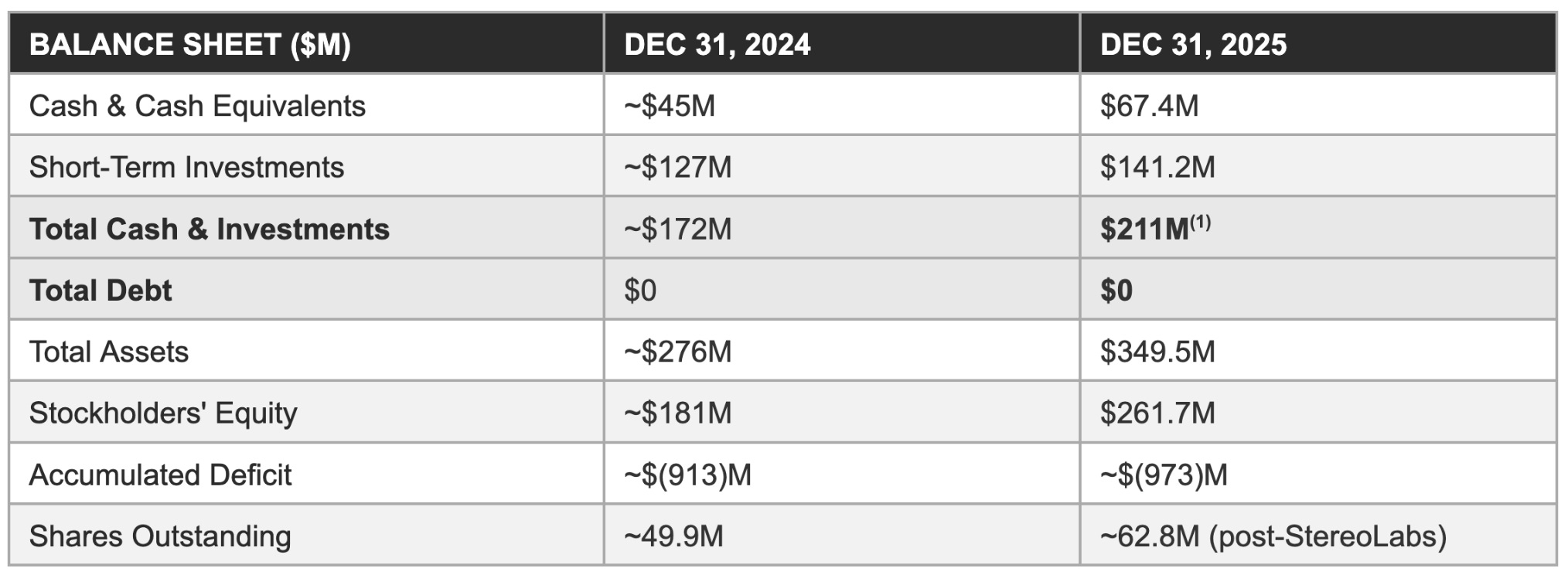

As of December 2025, Ouster held $211 million in cash and short-term investments with zero debt (source: Q4 2025 earnings release, March 2026), the strongest balance sheet in Western lidar and a structural competitive advantage in multi-year customer programme pursuit. 2025 revenue was $169.4 million, of which $146.4 million was product revenue (up 32% year-over-year) and approximately $23 million was primarily one-time IP royalties from long-term licence contracts. The royalty contribution lifted reported the gross margin to 49%, approximately 8 percentage points above the 41% normalised baseline that is the correct reference point for forward modelling. The company delivered positive Q4 2025 adjusted EBITDA of $11 million, its first, but remains net-loss negative on a full-year basis with $973 million in accumulated deficit as of December 31, 2025.

Company at a glance

The following table presents some facts about the company, for the purpose of the analysis:

2. Founding Conviction & The CMOS Architecture Bet

In 2015, Angus Pacala and Mark Frichtl made a bet that most of the lidar industry regarded as impractical: that complementary metal-oxide-semiconductor (CMOS) fabrication processes, the same physics underlying every digital camera sensor and smartphone imaging system, could be applied to light detection and ranging, and that the resulting cost and performance trajectory would ultimately make every competing architecture obsolete. A decade later, the bet has been validated across seven silicon generations, commercially confirmed through $23 million in competitor royalty payments, and not yet fully monetised at the scale management has guided. Whether the payoff arrives before capital patience expires is the central analytical question.

The architecture in plain language

Conventional lidar architectures, including the mechanical spinning systems pioneered by Velodyne and the analog VCSEL/avalanche photodiode approaches used by most first-generation commercial lidar, relied on components and processes originally developed for non-lidar applications, adapted rather than purpose-designed. Ouster’s founders argued from first principles that the correct long-term architecture was to co-design both the emitter (a vertical-cavity surface-emitting laser, or VCSEL, array) and the detector (a single-photon avalanche diode, or SPAD, array) on standard CMOS processes.

The consequence of this choice, if it proved manufacturable, was significant: standard CMOS foundries serving the mobile phone, automotive, and industrial imaging markets operate at volumes orders of magnitude larger than lidar-specific applications, and their capital investment in process advancement is funded by those non-lidar volumes. A CMOS lidar manufacturer is therefore a beneficiary of billions of dollars of foundry R&D investment paid for by Apple’s iPhone camera and Sony’s image sensor business, a cost-reduction dynamic unavailable to any architecture that requires a non-standard semiconductor process.

The VCSEL emitter enables massively parallel beam emission, hundreds of laser channels operating simultaneously, without the moving mechanical parts that limit mechanical lidar in high-vibration industrial environments and impose the per-unit cost floor of precision machined assemblies. The SPAD detector, specifically Ouster’s backside-illuminated (BSI) implementation first introduced in the L3 chip generation, achieves what management has described as a 10× photon sensitivity improvement over front-side illuminated SPAD designs, a performance leap that translates directly into longer detection range and better performance in adverse lighting conditions at equivalent laser power. The digital output of the SPAD array enables on-chip signal processing that eliminates the analogue signal conditioning chain required by APD-based receivers, reducing both component count and susceptibility to electrical interference.

The CMOS architecture wager has been commercially validated by the fact that Velodyne, once the dominant global lidar company and Ouster’s largest competitor, paid Ouster approximately $23 million in IP royalty revenue in 2025 under long-term licence contracts for CMOS lidar patents acquired in the Velodyne merger. A competitor paying royalties to a smaller acquirer on its own core technology is not an ordinary commercial event. It is documentary evidence that the patent portfolio and the architecture it protects are substantively differentiated.

Seven chip generations: The cadence that proves the thesis

The operational evidence for the CMOS thesis is not the founding narrative but the silicon cadence. From the Whitney first-generation chip through the L3 BSI SPAD, the production REV7 platform, and the concurrent L4 and Chronos ASIC programmes currently in development, Ouster has executed a new significant chip generation approximately every 12-18 months without publicly disclosed schedule failures. Each generation has delivered meaningful performance or cost improvement: the L3 BSI SPAD’s photon sensitivity gain, the REV7’s manufacturing leverage enabling gross margin expansion from 10% in 2022 to approximately 41% normalised in 2025, and the Chronos ASIC’s ASIL-B functional safety certification unlocking automotive procurement eligibility.

The L4 chip, which management on the Q4 2025 earnings call described as ‘the most significant product overhaul in company history’ and which is expected to enable a 2× TAM expansion through lower price points, has not yet received a commercial launch date. The phrase ‘most significant product overhaul in company history’ is analytically significant: it implies greater scope than any prior generation, and greater scope historically correlates with greater schedule risk. The L4’s absence of a commercial launch date in March 2026, while the six prior publicly discussed generations all delivered on stated timelines, is the primary technical uncertainty in the investment thesis and is addressed in detail in the Risk Matrix (Section 12).

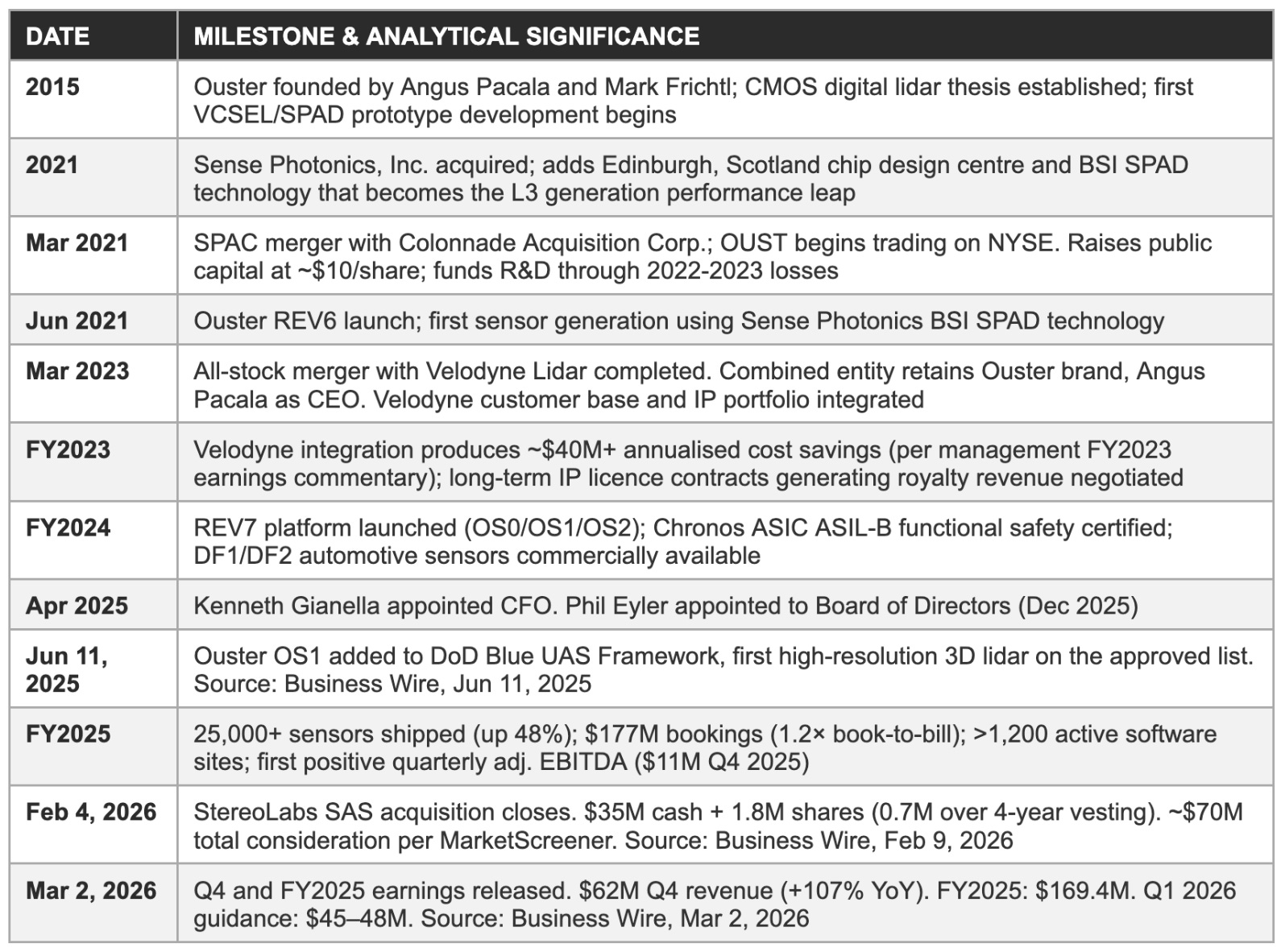

3. Corporate Timeline & Consolidation History

Ouster has executed three acquisitions and a SPAC listing in the four years since going public, each materially reshaping its cost structure, competitive position, and capital requirements. The Velodyne merger, widely expected to destroy value through integration friction, instead delivered IP royalties, customer consolidation, and cost savings that substantially exceeded pre-merger analyst expectations. The StereoLabs acquisition, completed February 4, 2026, is the most consequential transaction yet: it represents a strategic pivot from lidar-only hardware to a multimodal sensing and perception platform that management calls Physical AI.

What the Velodyne merger actually achieved

The March 2023 Velodyne merger was the most consequential transaction in Ouster’s history prior to StereoLabs. Pre-announcement, the merger was received sceptically: Velodyne was a direct lidar competitor with an overlapping customer base, a historically adversarial IP relationship with Ouster, and a cost structure that had produced its own substantial losses. The integration case rested on headcount consolidation, manufacturing leverage, and the potential to use the combined entity’s IP portfolio more productively.

Three years later, the result is unambiguous: the Velodyne merger was transformative. The $23 million in primarily one-time royalty revenue recognised in 2025, flowing from the long-term IP licence contracts negotiated in the merger aftermath, represents a direct cash return on the integration that required no ongoing operational effort to collect. The headcount and facility consolidation produced the cost savings management guided.

The Velodyne customer accounts were retained and grew; the book-to-bill of 1.2× in 2025 reflects demand from a consolidated base that includes former Velodyne customers. The merger, in retrospect, was a capital-efficient way to acquire IP royalty rights, eliminate a direct competitor, absorb its customer base, and achieve manufacturing scale simultaneously. It is the single most important piece of evidence that Ouster’s management team can execute complex M&A, a relevant data point as investors assess the StereoLabs integration risk.

4. The CMOS Digital Lidar Platform: Hardware, Silicon Roadmap & What ‘Most Significant Product Overhaul in Company History’ Actually Means

The sensor hardware platform is the engine of Ouster’s gross margin improvement, the asset that generates the IP royalties from Velodyne, and the foundation on which the software stack’s switching costs are built. Understanding the REV7 generation’s current commercial position and the L4/Chronos roadmap’s forward implications is essential to forming a view on whether the 30-50% growth framework is achievable through FY2026-2028.

REV7: The current commercial platform

The REV7 platform, comprising the OS0 (wide field-of-view, 360° scanning), OS1 (mid-range scanning), and OS2 (long-range scanning) sensors, represents Ouster’s fourth major commercial chip generation and the first to be deployed at meaningful production scale. REV7 is manufactured on standard CMOS processes through Benchmark Electronics (final sensor assembly, domestic U.S. manufacturing, Buy American certified) and Fabrinet (precision optical assembly). The domestic Benchmark relationship is not a preference but a legal prerequisite for federal procurement: Buy American certification under the Infrastructure Investment and Jobs Act and NDAA-compliant procurement require U.S. assembly, a requirement that Chinese lidar manufacturers cannot satisfy regardless of price.

REV7’s gross margin contribution is the clearest financial evidence that the CMOS cost curve thesis is operational. 2022 gross margin was 10%; 2024 was 36%; normalised 2025 (excluding ~$23M royalties) is approximately 41%. This 31-percentage-point improvement in three years is driven by three compounding mechanisms: CMOS foundry process maturation reducing per-chip cost; volume manufacturing leverage at Benchmark and Fabrinet; and the growing proportion of sensors shipped with Gemini or BlueCity software subscriptions attached, software revenue carrying materially higher gross margins than hardware.

The automotive stack: DF series and chronos ASIC

The DF1 and DF2 automotive lidar sensors, built on the Chronos application-specific integrated circuit (ASIC), represent Ouster’s entry into the automotive ADAS tier-1 supply chain. The Chronos ASIC carries ASIL-B functional safety certification, the automotive industry’s standard for hardware systems where failure may result in serious injury, and the DF series products are priced and specified for automotive OEM qualification programmes.

As of March 2026, Ouster has not disclosed any production-volume automotive OEM design win, though DF-series qualification programmes with automotive customers are active. The automotive vertical is a smaller component of current revenue than industrial and robotics but represents the highest unit-volume potential if OEM qualification programmes convert to production orders.

L4 and chronos-next: Forward silicon roadmap

Management’s description of the next-generation chip as ‘the most significant product overhaul in company history’ on the Q4 2025 earnings call (March, 2026) is the most analytically consequential statement in the earnings release and deserves careful decomposition. ‘Most significant’ implies a scope change that exceeds prior generations, likely a combination of substantially improved photon sensitivity over the already-improved L3 BSI SPAD, a new VCSEL architecture enabling the lower manufacturing costs that would support sub-$800 price points management has referenced for TAM expansion, and possibly a new integration level that further reduces the component count and assembly complexity. Management also stated that 2026 will see ‘more product commercialisations than any year in the company’s history’ (Q4 2025 earnings call), implying the L4 is targeted for commercial launch in 2026.

The L4 delay risk is not hypothetical: it is the single risk most capable of cascading into profitability timeline slippage, extended cash consumption, and potential equity dilution. Management’s track record across six prior generations without a disclosed schedule failure provides the strongest available mitigant, but ‘most significant overhaul in company history’ is not a phrase that reduces schedule risk. Investors should monitor H1 2026 for tape-out confirmation or preview announcements as the primary L4 milestone.

5. The Software Layer: Gemini, BlueCity & the Recurring Revenue Transition

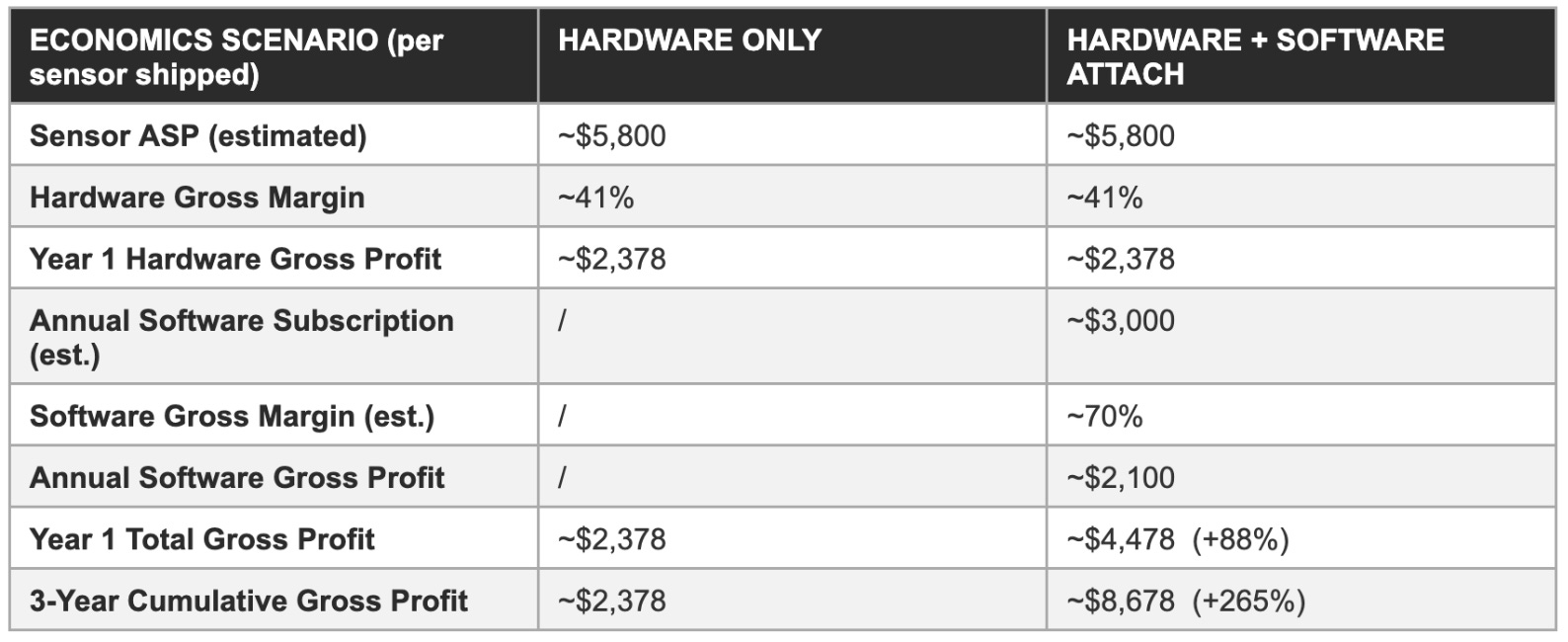

The transition from hardware-only to software-attached is the primary mechanism by which Ouster’s unit economics improve over time, and it is the aspect of the business most systematically undervalued in headline revenue and margin figures that treat all sensors as equivalent. A sensor shipped with a Gemini or BlueCity annual subscription generates three to five years of recurring gross profit that does not appear in the year-one hardware sale, and each active site represents a switching-cost asset that compounds with each renewal.

Gemini: Enterprise perception platform

Gemini is Ouster’s cloud-connected real-time perception platform for smart infrastructure applications. It combines OS-series lidar hardware with AI detection models trained on Ouster’s own sensor data, delivering occupancy analytics, object classification, and event triggering for use cases including perimeter security, facility monitoring, logistics yard management, and transportation infrastructure. The platform is deployed at over 1,200 active sites globally as of Q4 2025, covering over 65 million square feet of monitored space per management commentary. 2025 saw bookings more than double year-over-year, and software-attached sensors exceeded 15% of total units shipped, up from effectively zero two years prior.

The seven-figure annual enterprise Gemini licence signed in 2025 with a leading global technology company through the Constellis/LEXSO channel represents the highest-value single software transaction in the company’s history. It demonstrates that the Gemini platform can compete for large-scale enterprise security deployments at an annual contract value that, when multiplied across a pipeline of similar-scale customers, could contribute meaningfully to the path to profitability even independent of hardware volume growth.

BlueCity: Smart traffic and the NEMA TS2 certification moat

BlueCity is Ouster’s Gemini-powered intelligent transportation system (ITS) solution, targeting traffic operations, intersection safety management, and multi-modal transportation analytics for public sector customers, primarily state and municipal Departments of Transportation. BlueCity is deployed at U.S. DOT programmes in Utah (100+ intersections disclosed), Tennessee, and New Jersey as of Q4 2025 management commentary. The NEMA TS2 certification, required for safety-critical signal actuation applications in U.S. traffic management systems, has been achieved by BlueCity and, to our knowledge, by no other lidar-based ITS solution as of March 2026. This certification took multiple years to obtain and represents a genuine entry barrier for competitors seeking to address the safety-critical ITS segment.

Management guided an active BlueCity international expansion programme for 2026, including pilots in Europe and the Middle East. European deployment carries an additional structural advantage: the General Data Protection Regulation (GDPR) creates compliance obligations for camera-based traffic monitoring systems that do not apply to lidar-only systems, which generate no personally identifiable data. A lidar-only traffic monitoring system is inherently GDPR-compliant in a way that camera-based alternatives are not, providing BlueCity with a competitive positioning advantage in EU procurement that has no equivalent in the U.S. market and that requires no additional product investment to exploit.

Attach rate economics: The compounding engine

The attach rate progression, effectively 0% in 2022, approximately 5% in 2023, and exceeding 15% in FY2025, is the financial metric most directly linked to long-term gross margin re-rating. Each 1-percentage-point gain in attach rate on a 25,000-unit annual shipment base adds approximately 250 software-attached sensors. At an estimated $3,000 annual software subscription with 70% gross margin, that generates approximately $525,000 in additional recurring annual gross profit, compounding with each renewal year. Reaching a 30% attach rate on a hypothetical 40,000-unit FY2027 shipment base would add over $15 million in annual recurring gross profit relative to 2025 levels, without a single additional hardware sale.

6. The StereoLabs Acquisition: Rationale, Terms & What EBITDA-Positive at $16M Revenue Actually Implies

The February 4, 2026 acquisition of StereoLabs SAS for approximately $35 million in cash and 1.8 million OUST shares, totalling approximately $70 million per MarketScreener, is the most significant strategic decision Ouster has made since the Velodyne merger and the most important open question in the near-term investment thesis. The rationale is coherent. The execution risk is real. And the financial characteristics of the target are materially more favourable than the market’s initial reaction suggested.

Deal terms - What is actually known

Ouster completed the acquisition on February 4, 2026, paying approximately $35 million in cash and issuing 1.8 million shares of OUST common stock, of which 0.7 million shares are subject to a four-year release schedule, a retention mechanism aligned with keeping StereoLabs co-founders Cecile Schmollgruber (CEO), Edwin Azzam, and Olivier Braun in their operating roles. This vesting structure is analytically significant: it provides four years of management continuity incentive while limiting the immediate share count impact to 1.1 million shares.

The total consideration at the February 9, 2026 announcement close price of approximately $19.71 per share (Benzinga data, Feb 9, 2026) implies a share component of approximately $35 million, for a total consideration of approximately $70 million. This figure is per MarketScreener’s deal database and should be treated as an estimate pending Ouster’s formal purchase price allocation in the Q1 2026 10-Q.

StereoLabs generated approximately $16 million in unaudited revenue in 2025 and was EBITDA-positive at close. This combination implies a revenue multiple of approximately 4.4× at $70 million total consideration, which is modest for a high-growth AI perception software company with 90,000+ deployed cameras and a large active developer community. The acquisition was accounted for as a business combination, and StereoLabs’ financial results are consolidated into Ouster’s beginning Q1 2026. Royalty revenue from StereoLabs, if any, is not separately disclosed.

StereoLabs’ EBITDA-positive status at acquisition is the most important financial characteristic and is explicitly highlighted by management as evidence that the acquisition is ‘accretive to the path to profitability’. This is not merely promotional language: an acquired business that adds gross profit without adding net losses accelerates the combined entity’s profitability timeline. Investors who model the acquisition as dilutive before FY2026 combined results are published should note that management’s explicit guidance, Q1 2026 revenue of $45-48M, Opex growth 5-8% from 2025 levels, was set after the acquisition close and incorporates the StereoLabs contribution.

The strategic rationale: Why cameras, why now

The strategic logic articulated by Pacala in the February 2026 TechCrunch interview is specific: lidar provides accurate range and depth data, but it lacks the dense spatial context and object detail that cameras deliver. For the Physical AI applications, warehouse robotics, autonomous vehicles, smart infrastructure, that Ouster’s customers are building, sensor fusion between lidar and cameras is not optional architecture; it is the minimum viable sensing stack. A company that provides only lidar forces its customers to source, integrate, calibrate, and maintain a second sensing system from a separate vendor, adding integration cost and complexity that slows deployment and creates ongoing maintenance overhead. A company that provides both, pre-integrated and pre-fused, removes that overhead.

StereoLabs’ specific value proposition within that thesis is not just cameras: it is the ZED Software Development Kit (SDK), the developer community that has built production applications on the ZED SDK across robotics, industrial automation, and mapping, and the AI depth estimation model that StereoLabs has built, a foundational model that derives precise depth from stereo camera imagery without requiring lidar.

That model, combined with Ouster’s lidar depth data, creates a fusion pipeline that is potentially more robust than either modality alone, and that can degrade gracefully in conditions where one modality is impaired. The developer community, which management describes as many thousands of active engineers, represents an organic customer acquisition channel for Ouster lidar products at near-zero incremental sales cost, a channel that direct sales force expansion cannot replicate at the same efficiency.

What should not be treated as a commercial commitment: the StereoLabs acquisition announcement does not include any binding agreement by StereoLabs customers to purchase Ouster lidar, any contractual commitment by existing Ouster customers to adopt ZED cameras, or any obligation by either party’s developer communities to adopt the combined platform. The cross-sell thesis is an analytical possibility, not a disclosed commercial contract. Investors are cautioned to evaluate the thesis on its commercial logic and the management track record rather than on any specific revenue commitment, which does not exist.

7. Four Verticals, One Balance Sheet: Revenue Architecture & Concentration Risk

Ouster’s multi-vertical commercial architecture is the structural characteristic that most directly separates it from every Western lidar company that has failed or been severely distressed in the 2023-2025 period. The vertical diversification is not merely a marketing positioning choice, it is the mechanism that sustained product revenue growth through the automotive programme timing disappointments that have been endemic to the autonomous vehicle industry, and that provided the commercial resilience the Luminar failure mode explicitly lacked.

Revenue by vertical - What is and is not disclosed

Ouster does not report disaggregated revenue by vertical in its quarterly earnings releases. The Q4 2025 earnings call identified warehouse automation, robotaxi, and mapping as primary Q4 drivers. Prior earnings commentary has consistently indicated that industrial automation and robotics collectively represent the majority of product revenue, with smart infrastructure (Gemini/BlueCity) growing fastest in percentage terms and automotive (DF series) smallest in absolute terms but with the largest potential volume at scale. Two customers individually exceeded 10% of 2025 product revenue, per the 2025 10-K disclosure. Neither customer has been publicly named.

The two-customer concentration risk

The disclosure that two unnamed customers each accounted for more than 10% of FY2025 product revenue creates a specific analytical risk that investors must assess without the ability to verify independently: if either or both of these customers reduces, delays, or terminates their Ouster purchasing programmes, the impact on FY2026 product revenue could be material and rapid. The 1.2× product book-to-bill implies a diversified bookings pipeline not concentrated in two accounts, which is the primary mitigant.

The StereoLabs acquisition adds over 10,000 new customer accounts to the combined entity’s revenue base, reducing concentration risk over time even if the underlying customer mix is unchanged. However, it would be analytically irresponsible to dismiss the concentration risk simply because the overall demand picture is positive, a single customer relationship disruption in H1 2026, superimposed on the royalty normalisation creating apparent revenue deceleration, would be poorly timed relative to investor expectations.

Smart infrastructure: The software revenue quality leader

The BlueCity and Gemini deployments represent the highest-quality revenue component in Ouster’s current business: contractually recurring, government-sponsored where DOT-funded, with genuine switching costs (NEMA TS2 recertification requirements, staff retraining, months of accumulated algorithmic tuning), and growing independent of hardware sales volume.

Each state DOT programme that Ouster wins creates a reference account that accelerates subsequent state agency procurement through peer-to-peer due diligence sharing, a network effect in the institutional government market that requires years to build and cannot be purchased. The Utah DOT (100+ intersections disclosed), Tennessee, and New Jersey programmes collectively form a reference network that is now a competitive asset in new state agency procurement.

8. Regulatory Moats & the NDAA Advantage: Why the Competitive Map Is Not Symmetric

The competitive analysis in Section 9 must be read with an understanding established here: the lidar market is not a single market with symmetric competitive dynamics. It is several overlapping markets, some of which are legally accessible to all vendors and some of which are structurally protected from the vendors that represent the most aggressive price competition. Ouster’s regulatory certification portfolio collectively defines a protected market perimeter within which Chinese lidar vendors are either legally excluded or functionally disqualified regardless of sensor specifications or price.

NDAA Section 889 and the Blue UAS framework

National Defense Authorization Act (NDAA) Section 889, as expanded by the 2024 American Security Drone Act (ASDA), restricts U.S. federal agencies and recipients of federal funds from procuring unmanned aerial systems, components, or software from covered foreign entities, a category that encompasses PRC-headquartered manufacturers including Hesai Technology and RoboSense. Beginning December, 2025, federal agencies may no longer operate covered UAS, and contractors and grantees using federal funds may not procure them. This is not a prospective restriction that may be enacted, it is effective law.

On June 11, 2025, Ouster’s OS1 was approved by the Defense Innovation Unit (DIU) and added to the Blue UAS Framework. This made the OS1 the first high-resolution 3D lidar sensor on the approved list, and the approval follows a rigorous DoD cybersecurity testing and supply chain vetting process. The practical consequence is that any U.S. government agency, military contractor, state or local government using federal grant money for UAS applications must use Ouster (or a similarly approved alternative) for 3D lidar. Hesai and RoboSense are excluded from this procurement category by statute, and the waiver process requires Congressional certification of national interest, a process that is both slow and politically unfeasible for Chinese lidar procurement in the current geopolitical environment.

Buy American and the infrastructure investment and jobs act

Ouster’s sensors are assembled domestically by Benchmark Electronics, providing Buy American certification. The Infrastructure Investment and Jobs Act (IIJA) allocates $550 billion in new infrastructure spending, with domestic content requirements that effectively exclude non-domestically manufactured sensor components from federally funded smart infrastructure programmes. BlueCity’s deployment in Utah, Tennessee, and New Jersey DOT programmes is commercially viable partly because the BlueCity hardware meets these requirements, a qualification that a Chinese-manufactured or offshore-assembled sensor cannot obtain regardless of the NDAA status of the underlying semiconductor components.

NEMA TS2 Traffic certification

The NEMA TS2 standard governs traffic control equipment deployed in safety-critical U.S. signal actuation applications. BlueCity has obtained NEMA TS2 certification. To our knowledge, no other lidar-based ITS solution holds this certification as of March 2026. The certification required a multi-year process and is specific to the BlueCity system’s hardware-software combination, a competitor cannot simply obtain the certification for a generic lidar sensor but must certify the complete traffic management system. This creates a years-long head start in the segment of the ITS market where signal actuation safety is the primary procurement requirement, which is also the highest-value segment because it involves recurring software maintenance contracts tied to safety-critical infrastructure.

ASIL-B Automotive certification

The Chronos ASIC’s ASIL-B (Automotive Safety Integrity Level B) functional safety certification under ISO 26262 is the prerequisite for automotive OEM qualification programmes. An uncertified lidar sensor cannot be qualified for safety-relevant automotive applications regardless of its detection performance. Chinese lidar vendors including Hesai and RoboSense have pursued ASIL-B certifications for their own automotive products; the certification is not uniquely Ouster’s. However, for the specific DF-series platform built on the Chronos ASIC, the certification is confirmed and commercially active, enabling Ouster to compete for automotive OEM programmes that represent the highest-volume potential use case for lidar if autonomous driving adoption accelerates.

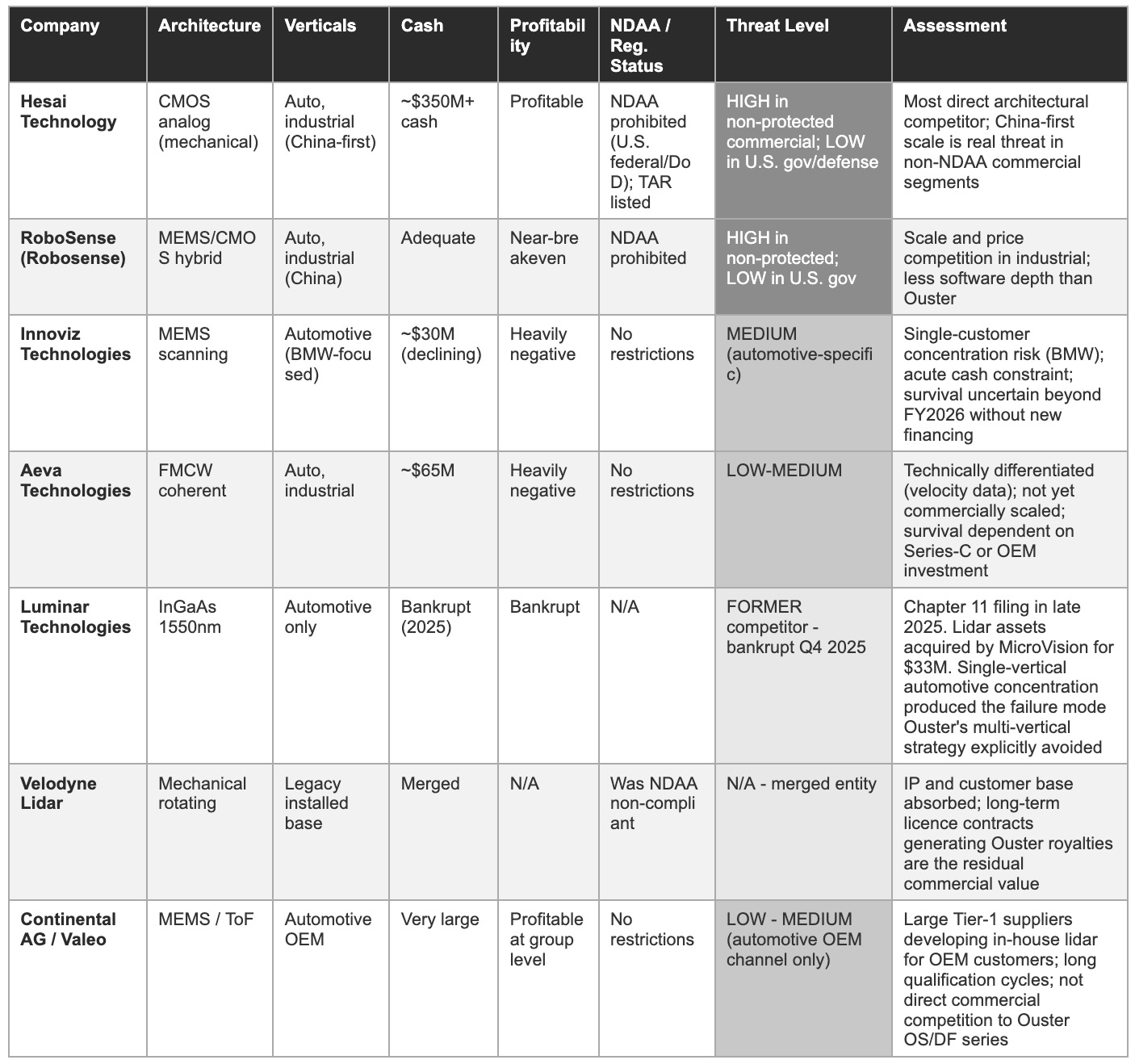

9. Competitive Landscape: The Chinese Scale Problem & Why Luminar’s Bankruptcy Matters

The lidar competitive landscape in March 2026 is profoundly different from the one that existed at the time of Ouster’s SPAC listing in 2021. The Western lidar industry has undergone a period of consolidation that has eliminated or severely impaired most of the dozen or more publicly listed lidar companies that existed at peak market enthusiasm. The survivors are, with few exceptions, better positioned now than they were in 2021, fewer better-capitalised competitors, more rational pricing, and more clearly defined market segments. The threat, as always, comes from Chinese manufacturers whose scale advantages in the unprotected segments of the global market are real and growing.

The Luminar failure mode: Analytical autopsy

Luminar Technologies’ Chapter 11 bankruptcy filing in late 2025 is analytically instructive because the failure mode is precisely the opposite of Ouster’s strategic architecture. Luminar concentrated entirely on the automotive OEM market with a technically differentiated but manufacturing-expensive InGaAs 1550nm platform, in a market where production programme timing is notoriously unpredictable and where the revenue gap between pilot programme and production scale can span three to five years.

When Luminar’s primary OEM customer programme timing shifted, there was no industrial, robotics, or smart infrastructure revenue base to sustain operations during the wait. The cash was consumed; the equity was diluted; and ultimately the organisation could not survive the interval between technical validation and production ramp.

The contrast with Ouster’s 2025 is instructive: Ouster’s industrial and robotics verticals collectively grew while Luminar was in distress. Ouster’s 12 consecutive quarters of product revenue growth across 2023–2025 occurred through exactly the period when automotive programme timing was most unpredictable. The multi-vertical diversification that analysts sometimes characterise as ‘dilution of focus’ is, in the lidar sector’s historical record, the characteristic that separates the survivors from those that did not.

10. Financial History & The Royalty Normalisation: What the Headline Numbers Actually Mean

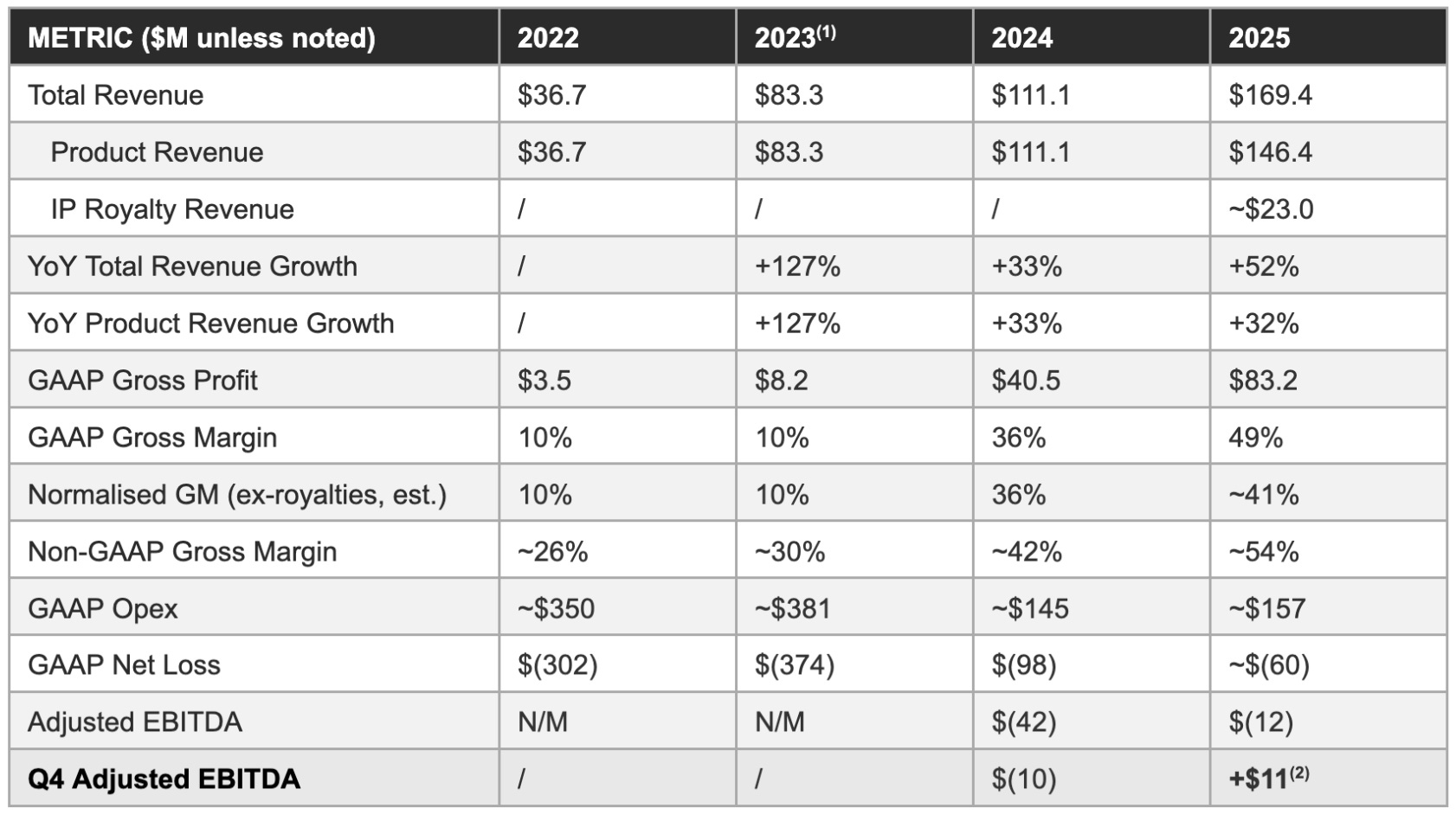

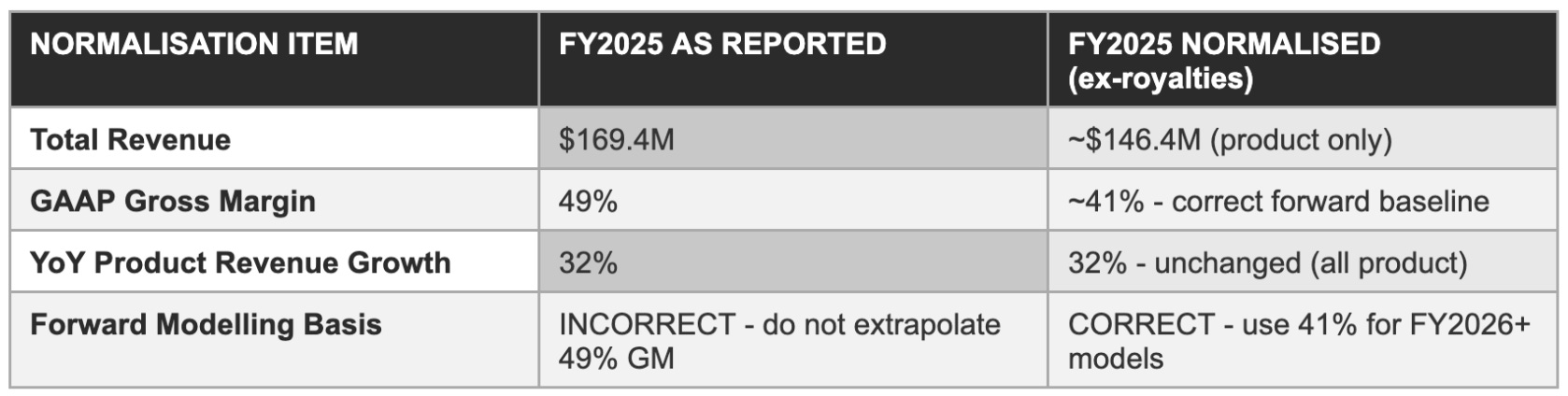

2025’s $169.4 million in revenue and 49% gross margin are materially influenced by approximately $23 million in primarily one-time IP royalties, a contribution that lifted both the revenue growth rate and the margin profile above the underlying operational trajectory. Any investor modelling FY2026 off reported 2025 metrics without adjusting for the royalty normalisation will misread the financial trajectory. The analytical imperative is to separate the structural improvement, which is substantial and genuine, from the one-time contribution.

Income statement progression 2022-2025

The royalty normalisation: The most important analytical adjustment

Management guided royalty revenue of less than $5 million for full-year FY2026, compared to approximately $23 million in 2025, an approximately $18 million year-over-year headwind. This normalisation will produce the following visible effects in FY2026 reported metrics: total revenue growth will appear to slow despite strong underlying product revenue growth; GAAP gross margin will appear to compress from 49% to the guided 35-40% range; and comparisons to 2025 headline metrics will universally look worse than comparisons against the normalised 2025 baseline. The risk is not business deterioration, it is analytical confusion that could trigger investor sentiment deterioration based on misread headline metrics.

Balance sheet & liquidity as of December 31, 2025

Revenue and gross profit trend: Visual comparison

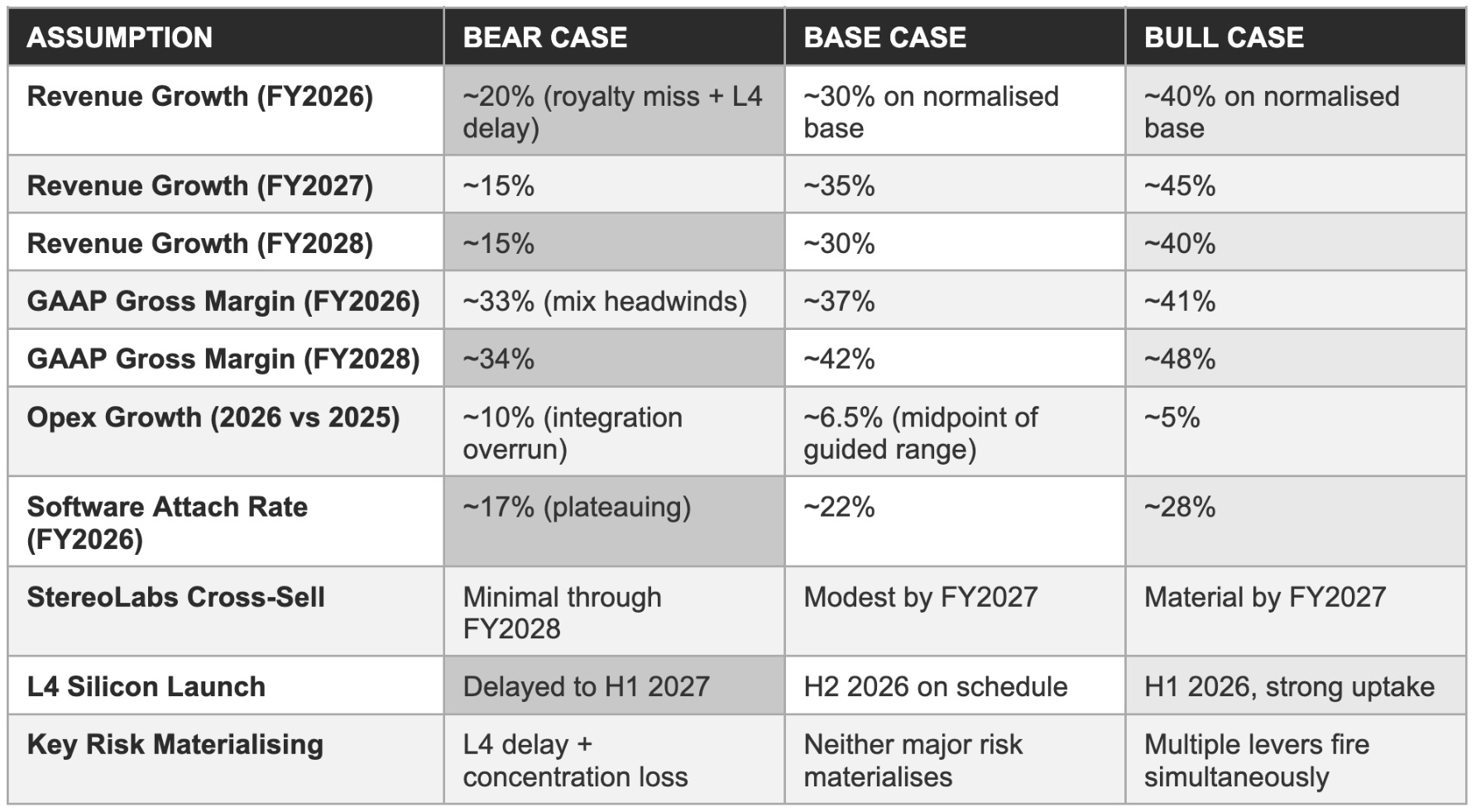

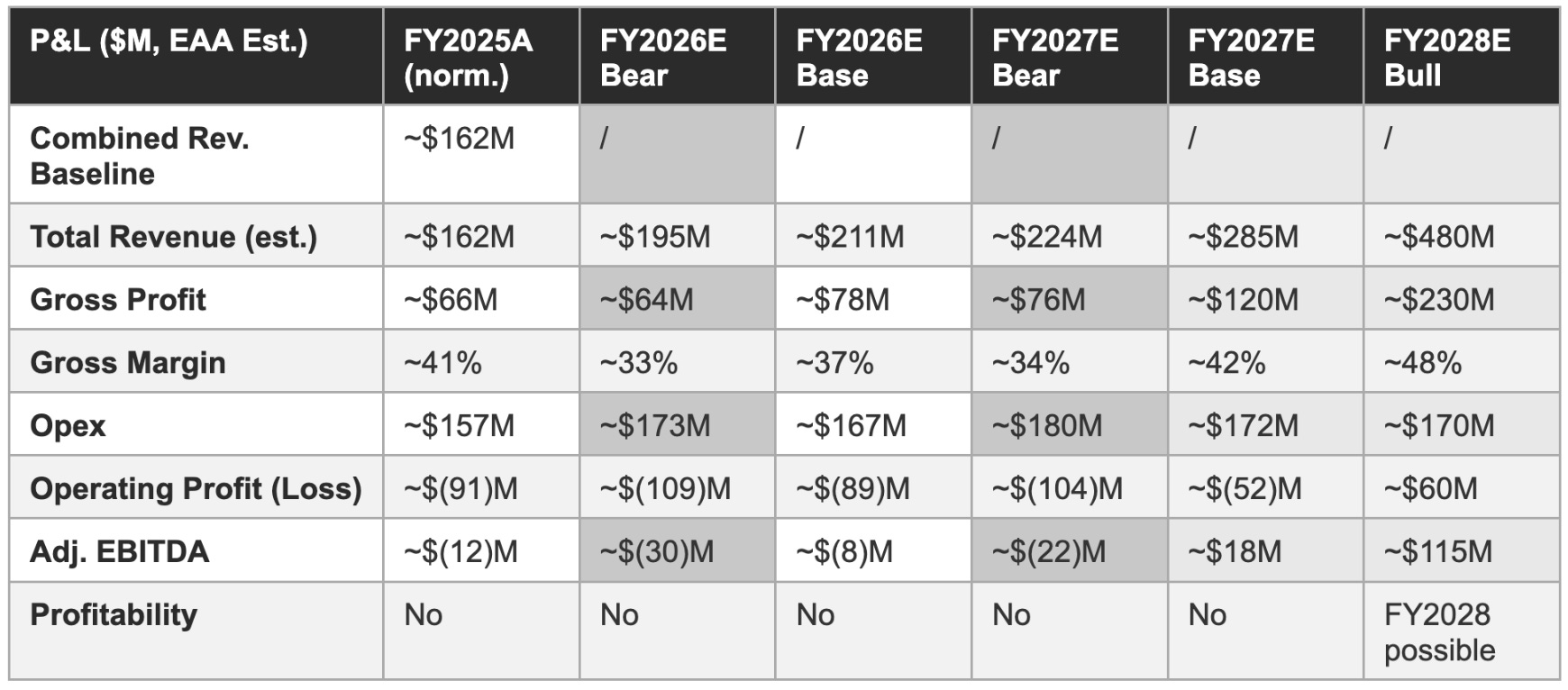

11. Forward Financial Model: Bear / Base / Bull Through FY2028

The three-scenario model below is built on management’s disclosed long-term financial framework, 30-50% annual revenue growth, 35-40% gross margins (excluding royalties), Opex growth 5–8% from 2025 levels, applied to the normalised 2025 product revenue baseline of approximately $146.4 million, plus a pro-forma StereoLabs contribution of approximately $16 million unaudited 2025 revenue (combined baseline of approximately $162 million). All estimates are our own projections and are not endorsed by, attributed to, or reviewed by Ouster management.

Model assumptions

Three-year P&L projection

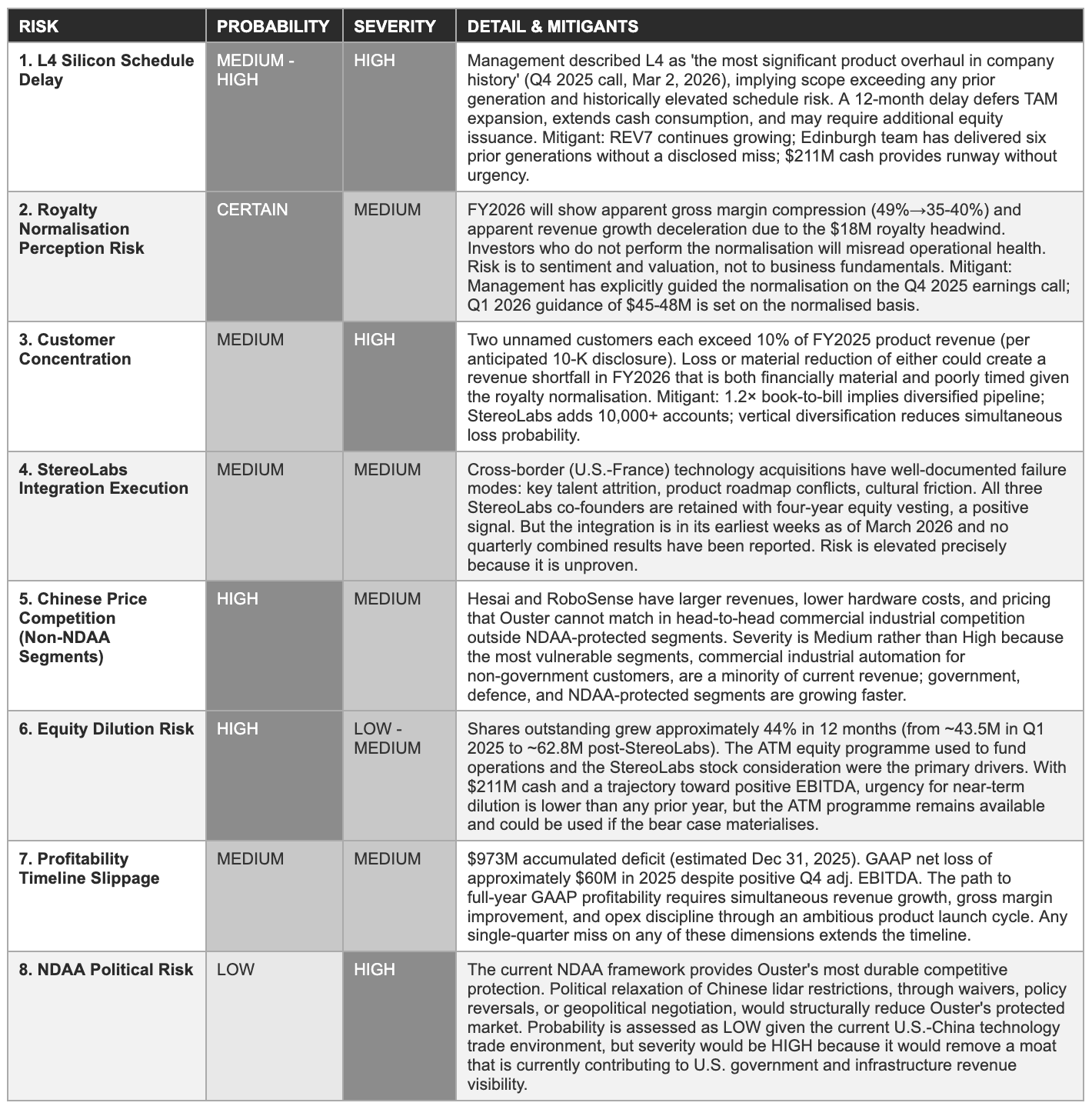

12. Risk Matrix

The risks below are not presented as reasons to dismiss the investment thesis. They are the specific variables whose outcomes determine whether the bull case, base case, or bear case of Section 11 is realised. Each is assessed on probability, likelihood of materialising as a significant negative outcome over the next 24 months (and severity), the degree to which it would impair the long-term investment case if it materialised. Greyscale shading: dark grey = HIGH; mid-grey = MEDIUM; light grey = LOW.

13. The Implied Valuation Question: What Does ~$1.25B Market Cap Require Ouster to Deliver?

At approximately $20.00 - $22.00 per share (H1 March, 2026) and 62.80 million shares outstanding, Ouster’s market capitalisation is approximately $1.25 billion. This valuation is not justified by current earnings, as the company reported a full-year net loss of approximately $60 million in 2025. It is a forward-looking claim on the business Ouster can build across the next three to five years. The analytical discipline required is to calculate explicitly what that claim implies about commercial outcomes, then assess the probability of those outcomes against the evidence available.

Revenue multiple analysis

At $1.25B market cap against a normalised 2025 revenue baseline of approximately $162 million, Ouster trades at approximately 7.7× forward normalised revenue, in the context of Q1 2026 guidance of $45-48M implying a run-rate of approximately $180-192M annually. Pre-profitability hardware-software platform companies with 30%+ growth and improving margins have historically commanded 4-15× forward revenue multiples depending on margin trajectory, market size credibility, and execution consistency. Ouster’s 7.7× normalised forward revenue multiple is therefore within the range of comparable pre-profitability platform businesses, neither dramatically cheap nor dramatically expensive, assuming the 30-50% growth framework is achievable.

The implied milestone calculation

For $1.25 billion in market capitalisation to be rational at a 5-year horizon, Ouster must achieve a revenue and profitability milestone combination that a reasonable investor would value at $1.25 billion or more today. At a 15× EV/EBITDA multiple, appropriate for a growing technology infrastructure business with recurring software revenue achieving its first years of sustained profitability, Ouster needs to generate approximately $80-85 million in annual EBITDA to justify the current market cap on a terminal-value basis.

Against our FY2028 bull-case EBITDA estimate of approximately $115 million, this target is achievable. Against the base case of approximately $18 million in FY2027 EBITDA, it is not achievable on a 2-year horizon but may be achievable on a 5-year horizon if the growth trajectory continues. Against the bear case, it is not achievable on any reasonable horizon.

The practical consequence of this calculation: the current $1.25B market cap is pricing in the base-to-bull scenario continuity through approximately FY2028–2029. It is not pricing in a bear-case scenario. Investors purchasing at $20.00-$22.00 per share are implicitly accepting the execution risk embedded in the L4 silicon roadmap, the StereoLabs integration, and the royalty normalisation, and receiving, as compensation, the operating leverage embedded in the 30-50% growth framework if it delivers. Whether that is an attractive trade depends on investors’ individual conviction about Ouster’s execution capability and the competitive moat durability assessed in Sections 8 and 9.

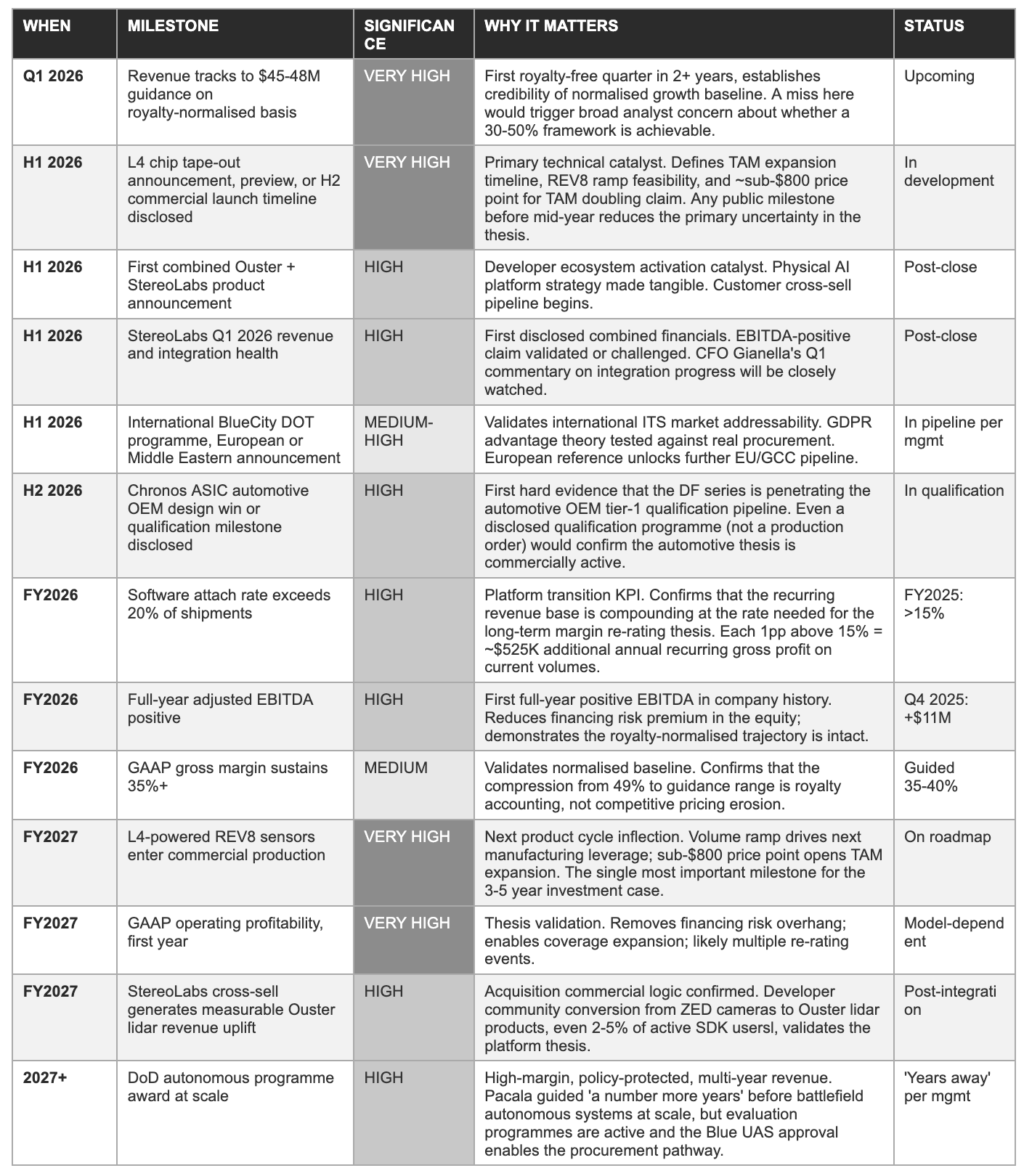

14. Milestones, Catalysts & What to Watch in 2026-2028

Management committed on the Q4 2025 earnings call to three priorities for 2026: commercialise the most significant product overhaul in company history; extend Physical AI platform leadership; and execute toward profitability. These priorities translate into a set of observable proof points that investors can track quarterly, each of which either confirms or challenges the investment thesis. The milestones below are ordered by analytical significance to the long-term investment case.

15. Opinion & Investment Perspective: Bull, Base & Bear Cases

This section reflects our analytical perspective as of March 2026. It is not a buy or sell recommendation. It is an attempt to present the investment case with intellectual honesty about what the evidence supports, what remains genuinely uncertain, and where the bear case deserves analytical weight equal to the bull case, which in this instance is considerable. The bear case must be read with the same rigour as the bull case, not as a perfunctory risk disclosure.

The bull case - Four pillars

The first pillar is architectural validation. Seven silicon generations without a disclosed schedule failure. $23 million in competitor royalty payments. Gross margin improvement of 31 percentage points in three years. A DoD Blue UAS approval that took competitors multiple years to match and that none have yet achieved for 3D lidar. The competitive moat is not theoretical; it has been tested by competition, litigation, market stress, and a global semiconductor shortage, and has strengthened in each encounter.

The second pillar is financial trajectory credibility. Twelve consecutive quarters of product revenue growth, spanning the post-SPAC correction, the Velodyne merger integration, and the automotive programme delays that killed Luminar, is a statement about multi-vertical commercial resilience that is empirically rare in the hardware technology sector. Adjusted EBITDA improving from $(42) million in 2024 to $(12) million in 2025, with Q4 2025 positive at $11 million, is a trajectory that, on a normalised basis, points directly toward full-year profitability within 12–24 months if the growth framework is maintained.

The third pillar is M&A execution track record. The Velodyne merger was widely expected to destroy value; instead it generated IP royalties, absorbed a competitor, and consolidated an installed base. StereoLabs was acquired at 4.4× revenue for an EBITDA-positive target with 90,000 deployed cameras and an active developer community, a capital-efficient way to add the camera modality, developer ecosystem, and AI perception software stack that the Physical AI platform thesis requires. Neither transaction required emergency equity issuance at distressed prices. Both were funded from a position of balance sheet strength.

The fourth pillar is structural market protection. The NDAA and Blue UAS Framework create a protected domestic market for Ouster that Chinese competitors are legally excluded from, regardless of price or performance. The IIJA domestic content requirements protect the smart infrastructure revenue stream. The NEMA TS2 certification protects the safety-critical ITS segment. These are not transient competitive advantages, they are statutory protections embedded in U.S. law, ASDA compliance requirements that became effective December 2025, and multi-year certification processes that competitors cannot shortcut.

The bear case - Four concerns

The first concern is the L4 schedule risk. Management’s statement that the L4 is ‘the most significant product overhaul in company history’ directly implies the largest development scope in the company’s history, and larger scope means more potential failure modes. The six prior generation track record is the best available mitigant, but it is not a guarantee. A 12-month L4 delay compresses the FY2026-2027 revenue trajectory, extends the cash consumption period, and creates the conditions under which additional ATM equity issuance becomes likely. The cascading consequences, deferred TAM expansion, extended losses, dilution, constitute the primary bear case scenario.

The second concern is the royalty normalisation confusion risk. The first two or three quarters of FY2026 will present Year-over-Year comparisons in which reported gross margin has declined from 49% to 35-40% and reported revenue growth has decelerated. Analysts who do not perform the normalisation will misread the business as deteriorating. In a market that has already demonstrated skepticism about hardware technology companies with pre-profitability track records, a misleading headline metric sequence at exactly the moment when investor patience is most constrained could produce sentiment-driven selling that is disconnected from business fundamentals but real in its price impact.

The third concern is the StereoLabs integration risk. Cross-border (U.S.–France) technology acquisitions have a statistical failure rate that is well documented in academic M&A research. The operational integration of two engineering organisations with different cultures, different product roadmaps, and different customer bases across a transatlantic distance involves coordination challenges that cannot be fully observed by external analysts. The four-year equity vesting for co-founders Schmollgruber, Azzam, and Braun is the right structural incentive, but incentives do not eliminate cultural friction, product roadmap disagreements, or customer disruption during integration uncertainty.

The fourth concern is the capital efficiency track record. $973 million in accumulated deficit represents nearly a billion dollars of invested capital that has not yet generated an accounting return. For investors focused on capital allocation quality over a decade-long horizon, the question is whether the next phase of Ouster’s development, characterised by the stated intent to reach profitability, will produce a different capital efficiency profile than the development-stage decade that preceded it. The answer is not knowable in March 2026 but will be partially revealed by the FY2026 EBITDA trajectory and the degree to which StereoLabs integration costs are contained within the guided 5-8% Opex growth.

16. Conclusion, Investment Scorecard & Disclaimer

Ouster has done most of the hard things right. What isn’t proven yet is whether the execution quality that got it here extends to the most ambitious chip programme in its history, in a year when the headline numbers will look worse than last year to anyone not paying attention. That’s the frame. Everything that follows tries to be honest about both sides of it.

What the evidence supports

Ouster is not a speculative bet on a technology that might work someday. The CMOS architecture has been validated across seven chip generations, each delivered on schedule. Velodyne, once Ouster’s largest competitor, paid approximately $23 million in IP royalties in FY2025 under long-term licence contracts negotiated after the merger. GAAP gross margin improved from 10% to roughly 41% normalised over three years. Product revenue grew for 12 consecutive quarters through the period that put Luminar into bankruptcy and left Innoviz fighting for survival.

The multi-vertical commercial model is the structural reason Ouster is still here. Industrial, robotics, smart infrastructure, and automotive together provide a demand base that does not go to zero when a single customer segment slips its programme timing. That is exactly what happened to Luminar: one vertical, one customer concentration, one programme delay, and there was no floor. Ouster’s Q4 2025 revenue grew 107% year-over-year in a quarter when Luminar was in Chapter 11. The comparison is not subtle.

The balance sheet, roughly $176 million in cash and investments post-StereoLabs, zero debt, is a competitive weapon in an industry where counterparty solvency is now a procurement criterion. Procurement officers at state DOTs, DoD contractors, and automotive OEMs are not indifferent to whether their lidar supplier will still exist in three years. Ouster is the only Western lidar company where that question has a clear answer.

Where uncertainty remains

The investment case has one load-bearing assumption: the L4 chip launches in 2026 on the timeline management described on the Q4 2025 earnings call. Everything downstream, the TAM expansion to sub-$800 price points, the next gross margin step from 41% toward 50%, the primary technical catalyst for FY2026 investor sentiment, depends on that one deliverable. Management called it “the most significant product overhaul in company history.” That is not reassuring language from a schedule risk perspective. Larger scope has historically meant more potential failure points, and while the Edinburgh team has delivered six prior generations without a disclosed miss, a track record is not a guarantee.

The royalty normalisation will make FY2026 look worse than FY2025 in every headline metric. Reported gross margin drops from 49% to 35-40%. Total revenue growth decelerates on a year-over-year basis. Any investor reading the Q1 or Q2 2026 numbers without adjusting for the $18 million royalty headwind will misread deterioration into a business that is actually growing. The risk here is not to the business, management pre-guided this explicitly on the March 2026 earnings call. The risk is to sentiment if that pre-guidance is not widely absorbed.

StereoLabs is the right acquisition at the right price, but it is roughly six weeks old as of this writing. Cross-border integrations between U.S. and French engineering teams have a well-documented failure rate in M&A research, and the three co-founders’ four-year equity vesting is the correct retention mechanism but not a guarantee of smooth execution. The first two combined quarterly results will tell investors far more than the deal announcement did.

Finally, the two unnamed customers each exceeding 10% of FY2025 product revenue are an unresolved concentration risk sitting inside otherwise healthy-looking aggregate metrics. Losing either in the same quarter the royalty normalisation is creating headline pressure would be badly timed in a way that is hard to communicate out of.

The bottom line

At roughly $22 per share, the market is pricing in base-to-bull case execution through FY2027-2028. That is not irrational given the track record, but it means there is limited margin for error in the near term. Investors buying today are not paying for a cheap, overlooked company. They are paying for a well-positioned one and betting that the L4 delivers, StereoLabs integrates cleanly, and the royalty normalisation is understood rather than misread.

The bear case, L4 delay plus integration friction plus royalty perception confusion in the same six-month window, is not probable, but it is possible, and it is the scenario in which the current valuation has the most downside. The bull case, L4 on schedule, first combined products in H2 2026, software attach rate above 20%, BlueCity EU programme announced, produces a narrative shift that the $38-50 analyst consensus range is pricing correctly.

The non-biased summary is this: Ouster has earned the right to be taken seriously, and the next 12 months will determine whether it earns the right to be re-rated. The L4 milestone is the single data point that matters most. Everything else is noise until that one is resolved.

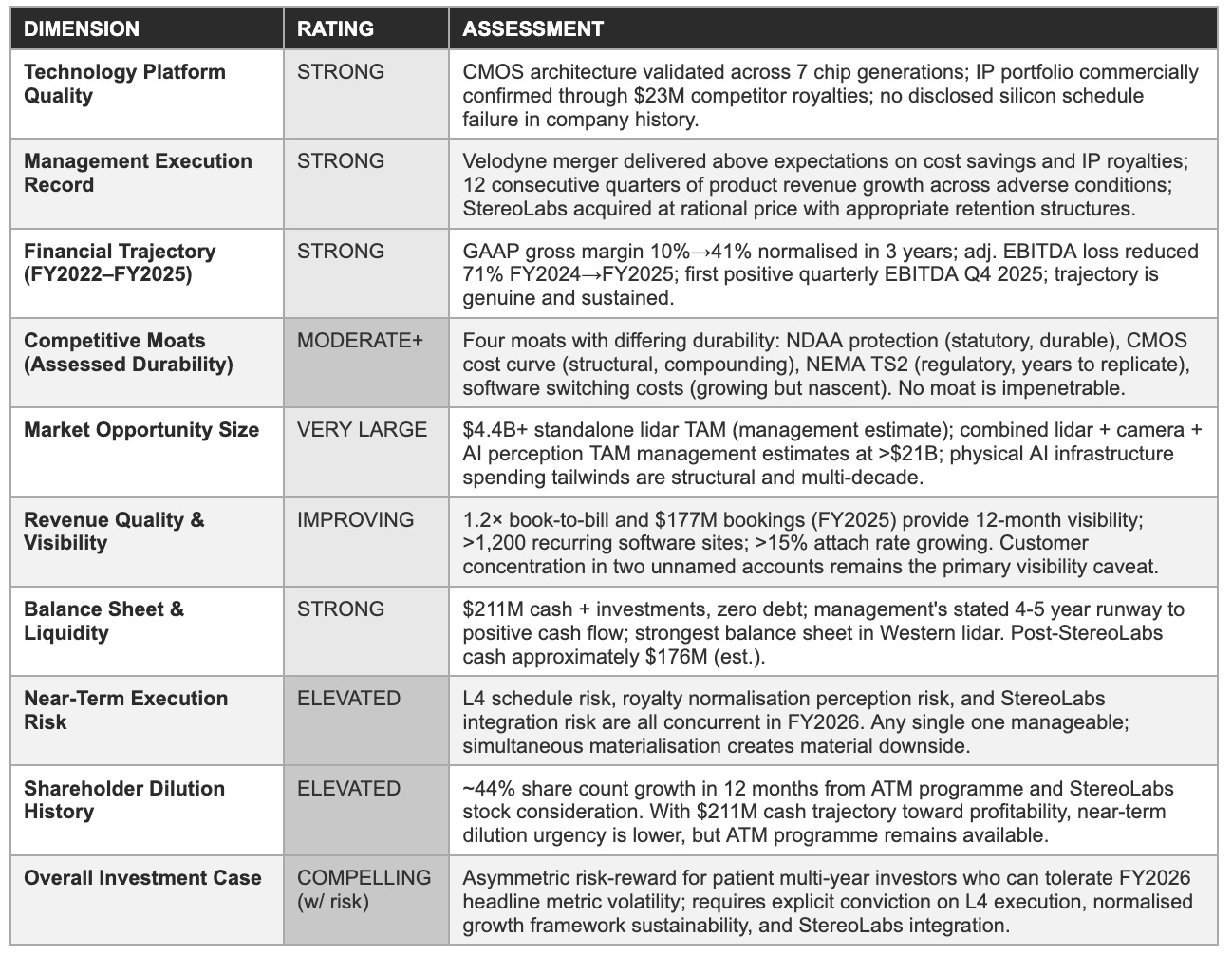

Investment scorecard

Sources

This analysis is based exclusively on publicly available information. Primary sources: Ouster, Inc. Q4 and full-year 2025 earnings release and press release (March 2, 2026, Business Wire); Q4 2025 earnings call transcript (March 2, 2026, accessed via Yahoo Finance, Motley Fool, and Moby); StereoLabs acquisition announcement and 8-K filing (February 9, 2026, Business Wire); Blue UAS Framework approval press release (June 11, 2025, Business Wire); TechCrunch interview with CEO Angus Pacala (February 9, 2026); Morningstar stock data (March 4, 2026); Investing.com analyst consensus (March 3, 2026); MarketScreener acquisition database (February 2026); Benzinga, Yahoo Finance, and StockTitan financial data; Advexure NDAA/Blue UAS compliance analysis; and publicly available SEC filings and prior-period earnings releases. All data cited is sourced from these public materials unless explicitly identified as our own estimate.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Ouster, Inc. (Nasdaq: OUST) or any other security. All information is sourced from publicly available materials believed to be reliable as of March, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.