PENGUIN SOLUTIONS, INC.

The AI Factory Bet, the Hyperscaler Exit, and Whether Three Structurally Different Businesses Can Converge Into a Premium-Multiple Platform Before the Memory Cycle Turns

1. Corporate Profile & The Three-Business Conundrum

Penguin Solutions is three structurally distinct businesses under one ticker, an AI and HPC systems integrator, a specialty memory module assembler, and an industrial LED components supplier. Whether that structure creates compounding value or depresses every segment’s achievable valuation multiple is the foundational question the investment case demands.

Segment mix and the valuation tension

The structural tension is straightforward.

Investors seeking AI infrastructure exposure receive it in the Advanced Computing segment and, with qualifications, in the Integrated Memory segment’s CXL product development programme. They also receive, without seeking it, exposure to an LED components business operating in a market where Chinese manufacturers have created sustained pricing pressure.

The multiple the market assigns to an AI infrastructure story is substantially higher than the multiple it assigns to a commodity LED business. As long as all three businesses occupy the same financial statements, the aggregate multiple reflects a blend of those competing valuations, a discount relative to what a pure-play Advanced Computing or Memory AI business would command.

A comparison of segment revenue contribution over the past three fiscal years illustrates how the business mix has evolved.

Advanced Computing has declined as a share of total revenue from approximately 52% in FY2023 to approximately 47% in FY2025, driven by the deliberate exit from hyperscale hardware and the wind-down of Penguin Edge.

Integrated Memory grew from approximately 31% to approximately 34% of revenue over the same period, aided by AI-driven DRAM demand and the DDR5 transition cycle.

Optimised LED has been broadly stable as a revenue contributor in absolute terms while declining modestly as a proportion of total, a pattern consistent with a business operating in a slow-growth market where PENG has pricing power at the application-optimised end but limited growth at the commodity end.

2. The Transformation Thesis: Rebrand, SKT Anchor, and the New Leadership Mandate

PENG’s investment case rests on a transformation that is credible in strategic logic and unproven in commercial execution, built around three discrete events: the divestiture of non-core assets, a $200M anchor investment from SK Telecom with an SK Hynix partnership attached, and a new CEO installed in February 2026.

The SGH-to-PENG transition

The rebrand from SGH to PENG in October 2024 reflected a deliberate decision by management to foreground the Penguin Computing heritage as the defining identity of the company and to subordinate the memory and LED businesses to supporting roles within that identity. The practical consequence is that the company now presents itself to investors and customers as an AI infrastructure provider that also manufactures specialty memory modules, rather than as a memory company that acquired some computing assets.

The asset portfolio has been restructured to support this identity. In November 2023, the company divested 81% of its Brazilian commodity memory assembly operations (SMART Brazil) to Lexar Europe. In March 2026, it sold its remaining 19% stake in the renamed Zilia Technologies to the same buyer for $46.08 million, completing the exit. The Brazilian operations produced commodity memory modules with low margins and no strategic connection to the AI infrastructure positioning. Their exit removes a drag on margin optics and signals that management is willing to divest businesses that undermine the transformation narrative, even if those businesses generate revenue.

The Penguin Edge business is being wound down and is expected to cease operations by end of FY2026. Management concluded that serving edge deployments at scale requires a different supply chain, sales motion, and product lifecycle than the enterprise AI HPC business. The wind-down removes a source of revenue that was reported within Advanced Computing and is one of the primary drivers of the 42% year-over-year decline in Advanced Computing revenue reported in Q2 FY2026, creating a misleading headline that obscures the genuine non-hyperscale growth occurring beneath it.

The SK Telecom anchor: Strategic partnership and capital structure implications

The $200 million strategic investment from SK Telecom, which closed in December 2024, is the most structurally significant single event in PENG’s recent corporate history. SK Telecom invested through a special purpose vehicle called Astra AI Infra LLC, acquiring 200,000 convertible preferred shares at $1,000 per share. The preferred shares carry a 6% annual cumulative dividend, payable quarterly in-kind or in cash at PENG’s option, and are convertible into ordinary shares at a conversion price of $32.81 per preferred share. SK Telecom received board representation rights, pro-rata rights for future capital raises, and registration rights for the underlying ordinary shares on conversion.

The capital structure implications are material. At the $32.81 conversion price, the full preferred position converts into approximately 6.1 million ordinary shares, approximately 12% dilution on a fully diluted basis at current share counts. With the stock trading in the $55–62 range as of late May 2026, the preferred shares are deeply in-the-money on a conversion basis, and the 6% annual dividend adds approximately $12 million per year to PENG’s cash obligations if settled in cash, or creates further dilution if settled in-kind. Investors who have purchased PENG above the conversion price are implicitly accepting that the preferred shareholder will eventually receive ordinary equity at a cost basis substantially below the current market price.

The strategic value of the SKT relationship extends beyond the capital itself. SK Telecom is a sister company to SK Hynix within the SK Group conglomerate. At a moment when memory component supply is a binding constraint on AI infrastructure deployment, having a direct relationship with SK Hynix’s parent provides Penguin with potential preferential access to advanced DRAM and CXL memory components. In January 2025, Penguin formalised this by signing a strategic collaboration agreement with both SK Telecom and SK Hynix at CES 2025, covering the development and delivery of comprehensive AI data centre solutions including advanced memory products and AI edge servers.

This tri-party relationship is non-binding and its commercial outputs remain unproven, but the structural alignment it creates is the right partnership architecture for what PENG is attempting to build.

The new CEO: Kash Shaikh’s mandate

Mark Adams, who had served as CEO since 2019, retired effective February 2026. The board appointed Kash Shaikh as President and Chief Executive Officer. Shaikh, aged 56, most recently served as CEO of Securonix, a cybersecurity SaaS company. Prior to that he held executive roles at Dell Technologies, Hewlett Packard Enterprise, Virtana, and Cisco, background that is directly relevant to enterprise technology go-to-market and AI-enabled software products.

The compensation structure signals board intent clearly. His package includes an $890,000 base salary, a target bonus of 125% of salary, a $2,000,000 sign-on bonus subject to repayment conditions, and multi-year RSU and PSU grants tied to relative total shareholder return versus the Russell 2000 Index and to stock price appreciation hurdles. The performance structure aligns Shaikh’s interests with sustained stock price appreciation rather than short-term revenue volume, consistent with the transformation from hardware-volume growth to higher-quality, higher-margin AI platform revenue.

Adams remains with the company in an advisory capacity for nine months. Shaikh’s first public earnings call in April 2026 demonstrated command of the AI factory narrative and the inference infrastructure thesis, though it offered limited technical depth on the specifics of CXL memory architecture or the operational complexity of large-scale HPC deployment. Whether his enterprise software background translates effectively to managing hardware-intensive, project-based infrastructure deployments is the open question the FY2026 and FY2027 results will answer.

3. Business Model Architecture: Revenue Streams, Margin Profiles, and the Lumpy Hardware Problem

PENG generates revenue through three mechanisms with fundamentally different margin profiles, revenue visibility characteristics, and cyclical drivers. The blended gross margin of approximately 28-31% will remain constrained until the services layer within Advanced Computing and the premium CXL products within Memory grow as a share of total revenue.

Advanced Computing revenue structure

Advanced Computing revenue, $648M in FY2025, approximately 47% of total, comprises two economically distinct components: hardware product revenue and services revenue. Hardware product revenue is generated from the design and delivery of custom HPC and AI compute clusters for enterprise, government, research, and defence customers. These are large, bespoke engagements that typically involve multi-rack GPU or CPU deployments, custom networking fabric, storage integration, and site preparation. T

he deal sizes are large, the sales cycles are long, and the revenue recognition is back-end weighted toward project completion milestones. This creates the quarterly variability that characterises the segment, a single large deployment recognised in one quarter can swing segment revenue by 15–25% relative to an adjacent quarter with no comparable recognition event.

Services revenue within Advanced Computing, generated from managed services, post-deployment operations support, and the Penguin Services Organisation, is structurally different: it is recurring, relationship-based, and carries higher gross margins than hardware. Management has not separately disclosed the exact services revenue proportion within Advanced Computing, but commentary across multiple earnings calls describes services as growing as a proportion of the segment mix and as the highest-quality revenue component.

The Stratus Technologies business, which provides fault-tolerant server platforms and associated maintenance contracts for continuous-availability applications, contributes a recurring revenue floor that buffers against project-revenue volatility.

The ICE ClusterWare software platform is the layer through which PENG is attempting to build a software-attached recurring revenue stream on top of hardware deployments. ClusterWare manages AI cluster orchestration, workload scheduling, and operational monitoring. If adopted at scale across the enterprise HPC installed base, it could create a subscription revenue layer that generates cash independently of hardware refresh cycles. At present, management has not disclosed ClusterWare revenue as a separate figure, and its commercial scale remains unproven.

Integrated Memory revenue structure

Integrated Memory, $464M in FY2025, approximately 34% of total, generates revenue from the design and assembly of specialty DRAM modules, Flash storage products, and supply chain services under the SMART Modular brand. The business model is that of a value-added module assembler: PENG sources DRAM and NAND components from IDMs, assembles them into modules with custom form factors, higher reliability testing standards, and extended temperature or ruggedisation specifications, and sells them to enterprise, telecommunications, networking, and industrial customers who require specifications that commodity module suppliers cannot reliably deliver.

The gross margin in Integrated Memory is structurally constrained by the fact that the primary input cost, DRAM and NAND component pricing, is determined by IDM production economics that PENG does not control. When DRAM pricing rises, as it did through 2024 and 2025 driven by AI infrastructure demand and the DDR5 transition, the margin on memory modules compresses unless PENG can pass through cost increases to customers. This cyclicality means that Integrated Memory’s contribution to the company’s reported gross margin will oscillate in ways that are partly independent of PENG’s operational performance, a dynamic that makes the segment a less reliable anchor for the gross margin expansion narrative than the Advanced Computing services layer.

Optimised LED revenue structure

Optimised LED, $256M in FY2025, approximately 19% of total, generates revenue from the design and sale of application-optimised LED components under the Cree LED brand, serving horticultural, industrial, automotive, and general illumination markets. The segment does not share technology, customers, channels, or supply chain with either Advanced Computing or Integrated Memory. Q2 FY2026 LED revenue was $56M, down 7% year-over-year, attributed to weak demand from China and large U.S. OEM customers. Management has guided the segment to -5% to +5% for FY2026, implying approximately flat revenue.

The LED segment’s primary role in the investment case is as a source of multiple compression. Investors willing to pay 3–5x revenue for an AI infrastructure story will not pay that multiple for the LED revenue, creating a blended discount at the aggregate level. The market effectively prices the LED business at a lower multiple than the rest of the company, and that discount compounds every quarter the segment remains in the portfolio. Without a strategic resolution, divestiture, spin-off, or growth-driven dilution, the LED segment will continue to suppress the composite valuation that the transformation narrative could otherwise support.

4. Advanced Computing: The AI/HPC Systems Business and the Hyperscaler Exit

Advanced Computing is PENG’s largest segment by historical revenue and its most strategically central business, currently executing a deliberate transition toward enterprise, neocloud, and sovereign AI customers. The headline revenue numbers obscure the fact that the underlying non-hyperscale business grew 50% year-over-year in H1 FY2026.

The hyperscaler dependency and its deliberate removal

During FY2024 and FY2025, a portion of Advanced Computing revenue was generated from large hardware deployments to hyperscale cloud customers, orders for GPU cluster infrastructure that were transactional in nature, non-recurring, and subject to the capital expenditure timing decisions of a small number of very large companies. Management made the strategic decision to exit this hyperscale hardware dependency, concluding that the revenue quality was insufficient to justify the concentration risk. For FY2026, management has explicitly guided to zero hyperscale hardware revenue within Advanced Computing.

The practical consequence is a reported Advanced Computing revenue decline that reflects a deliberate customer exit rather than a demand failure. Q2 FY2026 Advanced Computing revenue was $116M, down 42% year-over-year. That decline is attributable to two factors: the absence of the hyperscale hardware revenue recognised in Q2 FY2025, and the ongoing wind-down of Penguin Edge. Both factors are disclosed, both are time-bounded, and both should have a declining impact on year-over-year comparisons as the prior-year periods begin to reflect the post-exit baseline.

The managed services and software support component of the segment has remained resilient through the hyperscaler exit. Stratus Technologies, which provides fault-tolerant server platforms and associated maintenance contracts for always-on enterprise applications, contributed a recurring revenue floor during the transition period. Management noted that Stratus renewal rates and support contract upsells remained stable through H1 FY2026, providing a baseload of revenue that buffers against the project-revenue volatility in the rest of the segment. Stratus’s financial services, industrial control, and healthcare customers represent a structurally different buyer profile from the hyperscale and Edge customers that PENG is exiting, and their renewal behaviour is correspondingly more predictable.

The enterprise, neocloud, and sovereign AI replacement pipeline

The enterprise and neocloud customer segments that PENG is targeting require a different sales motion: longer cycles, deeper technical engagement, managed services attachment, and ongoing relationship management rather than transactional procurement. PENG’s competitive positioning rests on its ability to deliver fully integrated AI compute clusters at a level of customisation and service intensity that large OEMs delivering standard server configurations at volume do not typically offer.

New enterprise customer wins in H1 FY2026 include a Tier One financial institution deploying a CXL-based MemoryAI KV Cache server for AI inference, an enterprise voice AI deployment in collaboration with Deepgram and Dell, an AI makerspace at Georgia Tech, and bookings in federal, energy, and biotech segments.

These are genuine new relationships, but they are early-stage: the revenue contribution from these accounts in H1 FY2026 is modest relative to the hyperscale hardware revenue they are replacing. Seven new enterprise AI HPC logos were added in H1 FY2026 versus three in the prior year period, an acceleration in new logo addition that is the leading indicator of future revenue growth, even if the immediate financial contribution lags the commercial momentum by 12–18 months.

Sovereign AI represents an emerging demand category that PENG is actively pursuing. National AI programmes in Europe, the Middle East, and the Asia-Pacific region require on-premise AI compute clusters that operate within data sovereignty constraints, cannot be hosted on U.S. hyperscaler infrastructure for regulatory reasons, and must be built and maintained by a trusted vendor with a proven HPC integration track record.

Penguin’s heritage in air-gapped government HPC deployments and its NVIDIA Elite Partner status make it a credible candidate for sovereign AI infrastructure awards. These deployments are characteristically large-value, relationship-anchored, and multi-year in their services tail, precisely the revenue quality profile PENG is attempting to build.

The NVIDIA Elite Partner designation provides PENG with priority GPU allocation, a meaningful procurement advantage in a supply-constrained market where GPU lead times have extended to six to twelve months for some customer classes. The Dell distribution partnership provides channel reach into enterprise accounts that PENG would not otherwise access through its direct sales organisation alone, effectively extending the sales coverage of the segment without proportional headcount investment.

These two channel advantages are operationally significant and difficult for smaller pure-play HPC integrators to replicate without equivalent partner relationships.

ICE ClusterWare and the software differentiation argument

ICE ClusterWare is PENG’s cluster orchestration software platform, managing workload scheduling, resource allocation, and operational monitoring for HPC and AI compute clusters. A customer who deploys a Penguin-built AI compute cluster and runs ClusterWare for ongoing management creates a recurring software revenue relationship that generates cash independently of hardware refresh cycles. Management expanded the OriginAI portfolio at NVIDIA GTC in March 2026, introducing blueprints specifically designed for inference-heavy workloads.

If ClusterWare achieves broad adoption among Penguin’s installed base of enterprise HPC customers, it could become a structurally significant source of recurring revenue that transforms the segment’s revenue quality over time. The evidence that this is occurring is, as yet, absent from the disclosed financials: management has not broken out software revenue within Advanced Computing, and no ClusterWare ARR or customer count metric has been publicly disclosed. Until a quantified software revenue figure is reported, the software differentiation argument remains a thesis rather than a demonstrated business line, and should be weighted accordingly in any financial model of the segment’s margin trajectory.

5. Integrated Memory: The Cyclical Engine and the CXL Bet

Integrated Memory delivered 63% year-over-year revenue growth in Q2 FY2026, the strongest segment performance, driven by AI infrastructure demand and the DDR5 transition cycle. The CXL product programme is the bet on structural differentiation before the inevitable commodity pricing correction.

The DDR5 transition and AI memory demand

The transition from DDR4 to DDR5 DRAM has been accelerating through 2024 and 2025 as AI server platforms and high-performance workstations adopt DDR5-capable processors at scale. DDR5 provides approximately 1.6x the bandwidth of DDR4 at comparable latency.

For SMART Modular, DDR5 adoption has created a strong replacement cycle in its enterprise, telecom, and networking customer base, requiring the higher-density, higher-reliability DDR5 modules that SMART Modular specialises in. In Q1 FY2026, Integrated Memory grew 41% year-over-year to $137M on DDR5 transition demand. Q2 FY2026 accelerated further to 63% growth, reflecting both the DDR5 cycle and AI server build-out demand.

The AI infrastructure demand driver is additive to the DDR5 transition. Large-scale AI model training and inference deployments require substantially more memory per GPU than traditional compute workloads, creating demand for higher-density DRAM configurations in AI server platforms. This memory demand growth is durable in the sense that each successive generation of large language models requires more memory to store weights, key-value caches, and intermediate activations. SMART Modular’s ability to deliver high-density, high-reliability DDR5 modules at enterprise scale positions it directly in this demand stream.

The risk embedded in this growth story is DRAM pricing cyclicality. The memory industry is characterised by alternating oversupply and undersupply cycles driven by IDM capital expenditure decisions with 18–24 month lead times. When IDMs add significant DRAM capacity in response to current tight supply, the resulting supply increase typically creates an oversupply condition and a sharp price decline.

A 20% decline in DRAM spot prices flowing through to module pricing could reduce Integrated Memory revenue materially even without any change in unit volume, and could compress margins simultaneously if input cost declines lag module pricing adjustments, a timing dynamic that is structurally unfavourable for module assemblers.

CXL MemoryAI and the system-level memory play

The Compute Express Link (CXL) MemoryAI product line is the most commercially significant new development within Integrated Memory. CXL is an open interconnect standard that enables CPU-to-memory communication at near-DRAM bandwidth over the PCIe bus, allowing memory resources to be pooled and expanded beyond the physical DIMM slot constraints of individual server CPUs. For AI inference workloads that require large key-value caches for long-context LLM inference, the ability to access 8–11TB of memory per server rather than the 1–2TB available through conventional DIMM slots addresses a genuine architectural bottleneck.

In March 2026, PENG announced the MemoryAI KV Cache Server, a CXL-based appliance providing up to 11TB of disaggregated memory for inference deployments. A Tier One financial institution was disclosed as an early adopter in Q2 FY2026. The CXL SMART Modular NV-CMM E3.S 2T module achieved CXL Consortium compliance, adding it to the official Integrators List, a prerequisite for OEM and enterprise procurement consideration. The Optical Memory Appliance programme is in earlier development, with first revenues anticipated in the late calendar 2026 to early calendar 2027 timeframe.

The commercial case for CXL as a margin-improving product is plausible: CXL memory appliances are system-level solutions requiring hardware design expertise, firmware development, and system integration that commodity module suppliers cannot replicate. If CXL adoption in enterprise AI inference accelerates, the MemoryAI product line could command gross margins substantially above the blended segment average. Enterprise adoption of CXL has, however, consistently been slower than initial industry projections.

The PCIe Gen 5 ecosystem required for full CXL bandwidth is only now reaching broad deployment in new server generations, and enterprise buyers have been cautious about adopting memory disaggregation architectures that require changes to application memory management. One reference customer in financial services is meaningful as a proof point but does not confirm mass-market adoption timing.

6. Optimised LED: The Stranded Asset

The Optimised LED segment generates approximately $250-260M of annual revenue from industrial, horticultural, and automotive applications under the Cree LED brand. It bears no structural relationship to the AI infrastructure platform PENG is building, and its continued presence depresses the composite multiple the market will award to the rest of the company.

The Cree LED business: Strengths and structural limits

The Cree LED brand carries genuine market recognition. The Cree XLamp and J Series packaged LED components have long-standing customer relationships in precision lighting, horticultural systems, and automotive illumination, where performance consistency and reliability specifications differentiate Cree products from lower-cost alternatives. The brand provides pricing power in its core markets that pure commodity LED suppliers cannot match, and the application engineering expertise embedded in the Cree LED product development organisation represents real intellectual property with commercial value.

The competitive environment has nonetheless deteriorated structurally over the past five years. Chinese LED manufacturers, operating within vertically integrated supply chains that combine epitaxial wafer growth, chip fabrication, packaging, and module assembly, have reduced manufacturing costs to levels that Western suppliers cannot match on commodity applications.

Cree LED has responded by focusing on application-optimised, higher-specification products where Chinese competitors have less advantage. This positioning is commercially sound but constrains the growth ceiling: the high-specification segment is smaller and grows more slowly than the commodity segment, and the pricing premium on application-optimised products narrows as Chinese manufacturers move up the quality curve.

Revenue in Q2 FY2026 was $56M, down 7% year-over-year, with weakness attributed to demand softness in China and from large U.S. OEM customers. Management has guided the segment to -5% to +5% for FY2026, implying approximately flat revenue. Its gross margin, estimated at 28-33%, is broadly in line with the Integrated Memory segment but without the growth optionality. The segment contributes roughly 15–20% of total PENG revenue while contributing essentially zero to the AI infrastructure narrative.

The strategic case for divestiture

A sale or spin-off of Cree LED to a strategic buyer, a lighting-focused industrial company or a private equity firm specialised in industrial technology, would simultaneously deliver cash proceeds to fund CXL product development, remove the segment that depresses the composite valuation multiple, and allow PENG to present a sharper AI infrastructure story to investors without the constant need to explain the LED business. Management has provided no public signal of such a review, and absent one, investors must price the LED segment as a permanent feature of the financial profile.

The valuation arithmetic of a potential LED divestiture is illustrative. At 1.0–1.4x revenue, a typical range for profitable, branded industrial components businesses sold in M&A, the Cree LED segment could attract proceeds of $250–360M. Applied to debt reduction, these proceeds would meaningfully improve the net cash position. Applied to share repurchases at current prices, they would reduce diluted share count. In neither scenario do the proceeds destroy value for PENG shareholders, and in either scenario the residual business, Advanced Computing and Integrated Memory, would be positioned to attract a materially higher forward revenue multiple than the current blended rate.

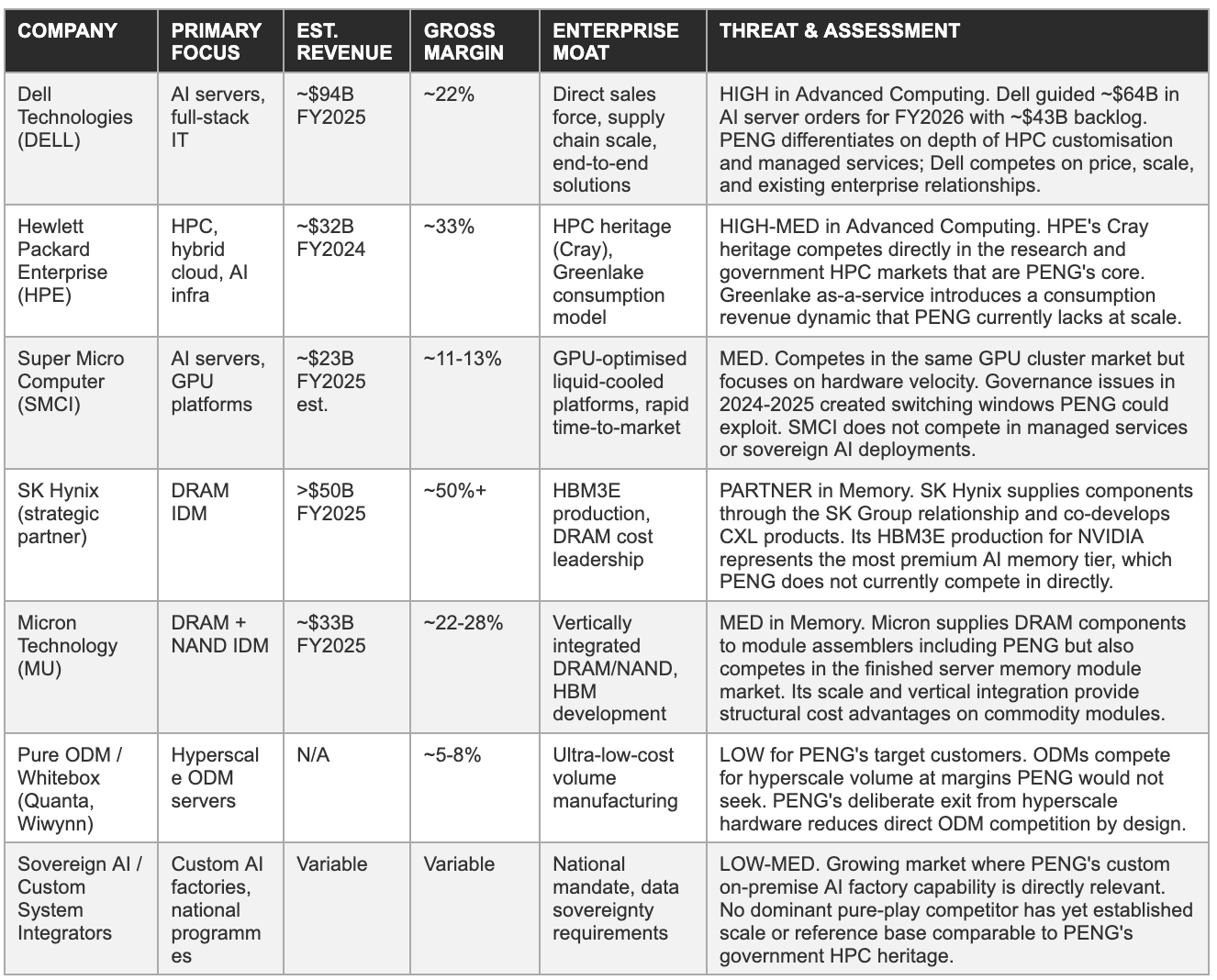

7. Competitive Landscape

PENG competes in three separate arenas simultaneously: against large-scale AI server OEMs in Advanced Computing, against module assemblers and IDMs in Integrated Memory, and against Chinese manufacturers in Optimised LED. Its defensible positions are narrow but real, centred on services depth in HPC and specialty specifications expertise in memory.

PENG’s competitive position in Advanced Computing is strongest when customers want a technically sophisticated, services-enriched, custom-architecture AI compute deployment rather than a standard GPU server from a volume OEM. That customer profile, federal agencies, research institutions, financial institutions with proprietary workloads, sovereign AI programmes with data localisation requirements, is real, growing, and underserved by the volume product lines of large OEMs.

It is also a segment where PENG competes on technical capability and relationship depth rather than on price, which is structurally supportive of the higher-margin services attachment the company needs to drive margin expansion.

In Integrated Memory, the competitive dynamic is more constrained. SMART Modular competes against other specialty module assemblers, including Avant Technology, Kingston Technology, and the specialty module divisions of the IDMs themselves, on specifications, reliability certifications, and supply chain service levels.

The CXL product development programme is the avenue through which PENG attempts to move from module assembly competition into a system-level product category where the competitive field is less crowded and the margin opportunity is materially better. Until CXL achieves commercial scale, the Memory segment competes primarily on the quality and breadth of its specialty module certifications, a position that is defensible but not expanding.

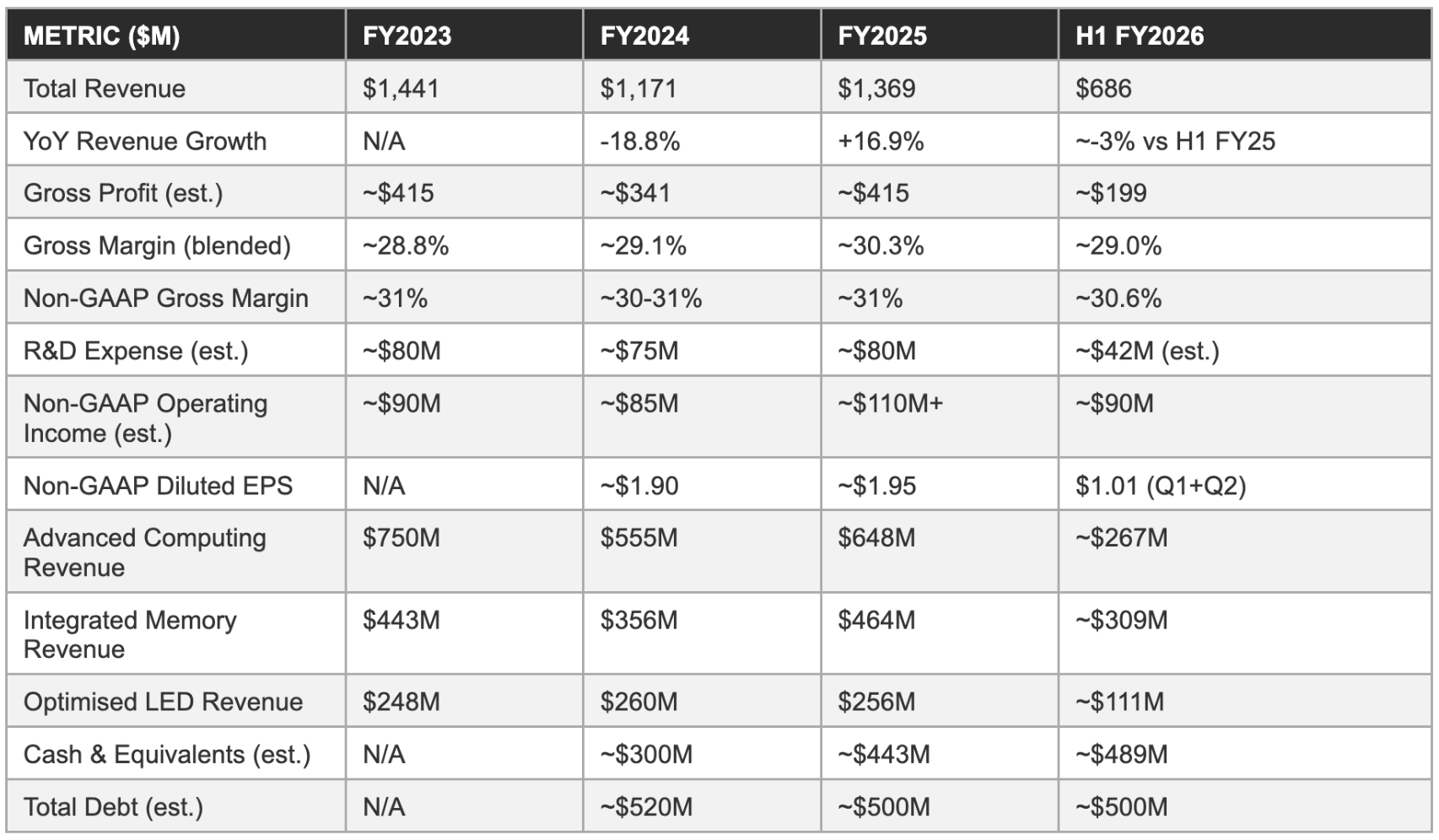

8. Financial History and the Gross Margin Ceiling

PENG’s financial history through FY2025 shows a company generating $1.2–1.4B in annual revenue at blended gross margins compressed between 27% and 31%. Margin improvement in H1 FY2026 is encouraging but remains early-stage, and the 40% long-term target requires simultaneous execution across multiple difficult levers.

Income statement progression: FY2023 through H1 FY2026

Revenue trend

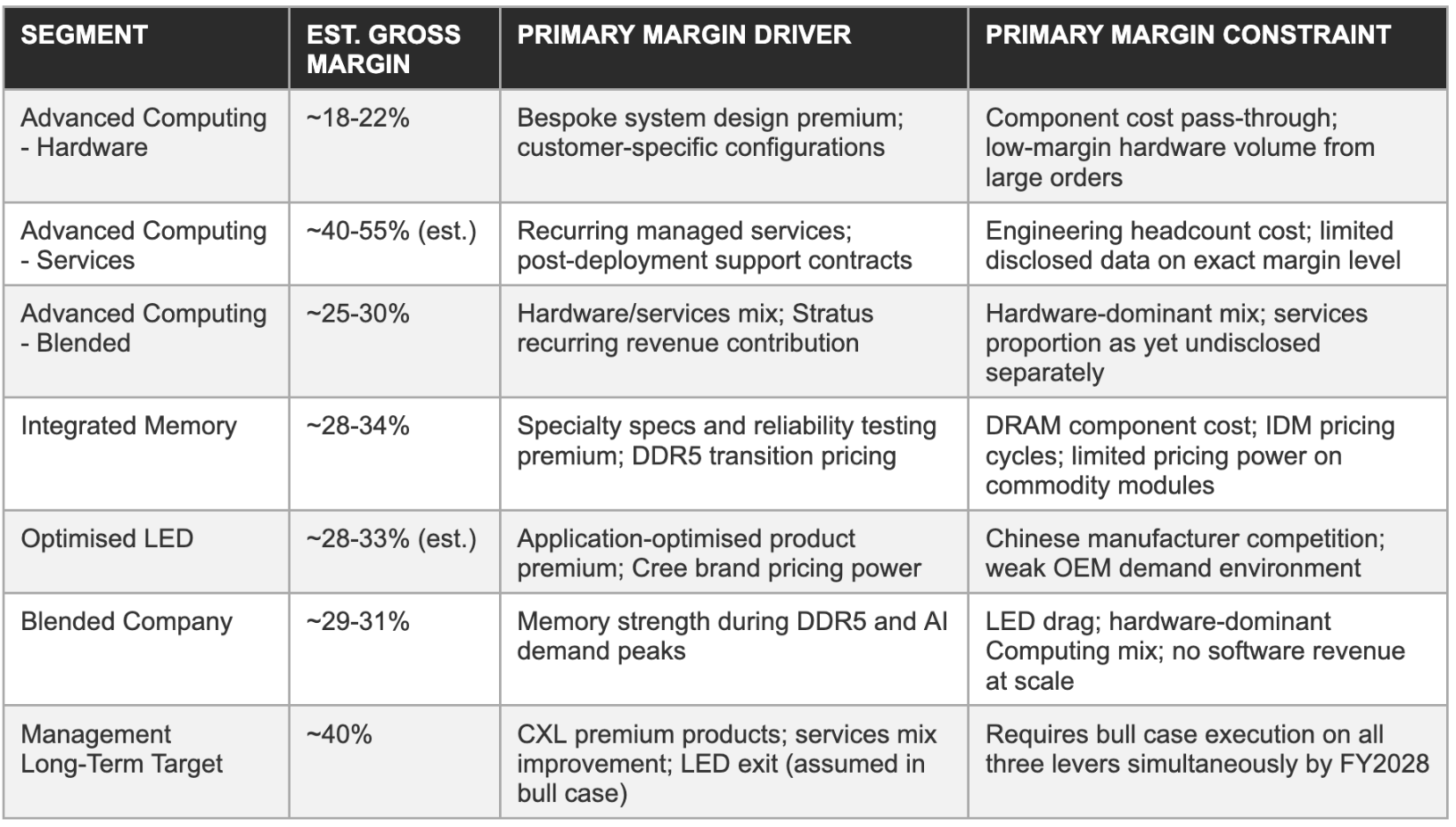

Segment gross margin comparison

The three segments carry materially different gross margin profiles. The table below presents estimated gross margins for each segment alongside the blended company average, illustrating why the composite margin is structurally constrained and where improvement must originate.

The 40% gross margin target: What it requires

Management has stated a long-term gross margin target of 40%, compared to the current blended non-GAAP level of approximately 31%. Reaching 40% requires a fundamental shift in revenue mix that cannot occur through volume growth alone. The primary levers are: growth of the services component within Advanced Computing, which carries margins substantially above the segment average; growth of CXL and premium memory products within Integrated Memory at margins above commodity module assembly; and a reduction in the weight of Optimised LED in the total revenue mix, whether through organic dilution or through divestiture.

Under the bull case FY2028 scenario, CXL products contributing approximately 15–20% of Integrated Memory revenue at 45%+ gross margins, Advanced Computing services growing to represent 35-40% of that segment at 50%+ margins, and Optimised LED exiting the portfolio, the blended margin could approach 37–39%.

Reaching 40% outright likely requires all three levers to perform simultaneously, with LED removed from the portfolio. Under the base case, where LED remains, services grow modestly, and CXL remains early-stage, the FY2028 blended margin is more likely to reach 33–35%. The 40% target is achievable but reserved for the bull case execution trajectory, and investors who build a base case financial model around it will be consistently disappointed.

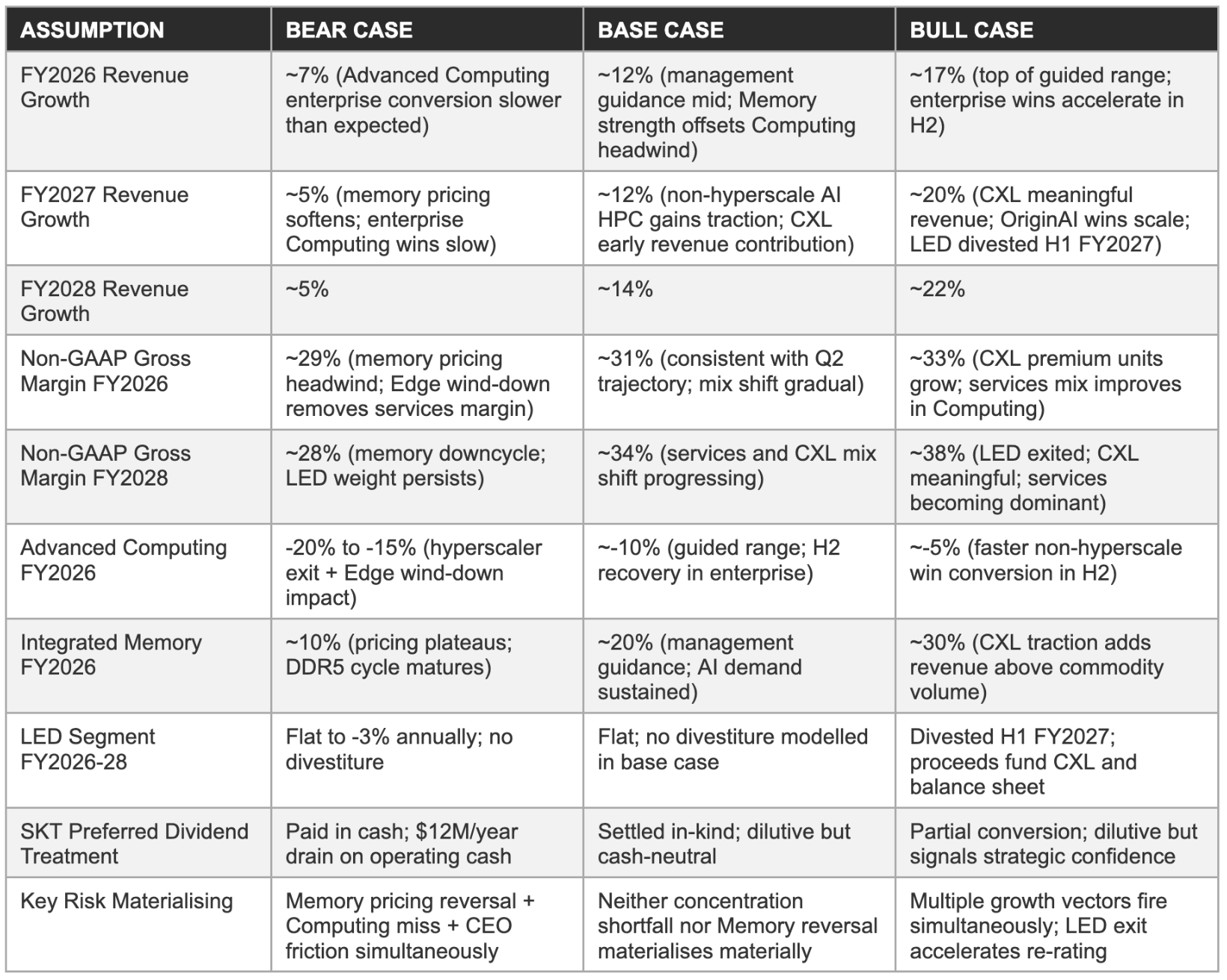

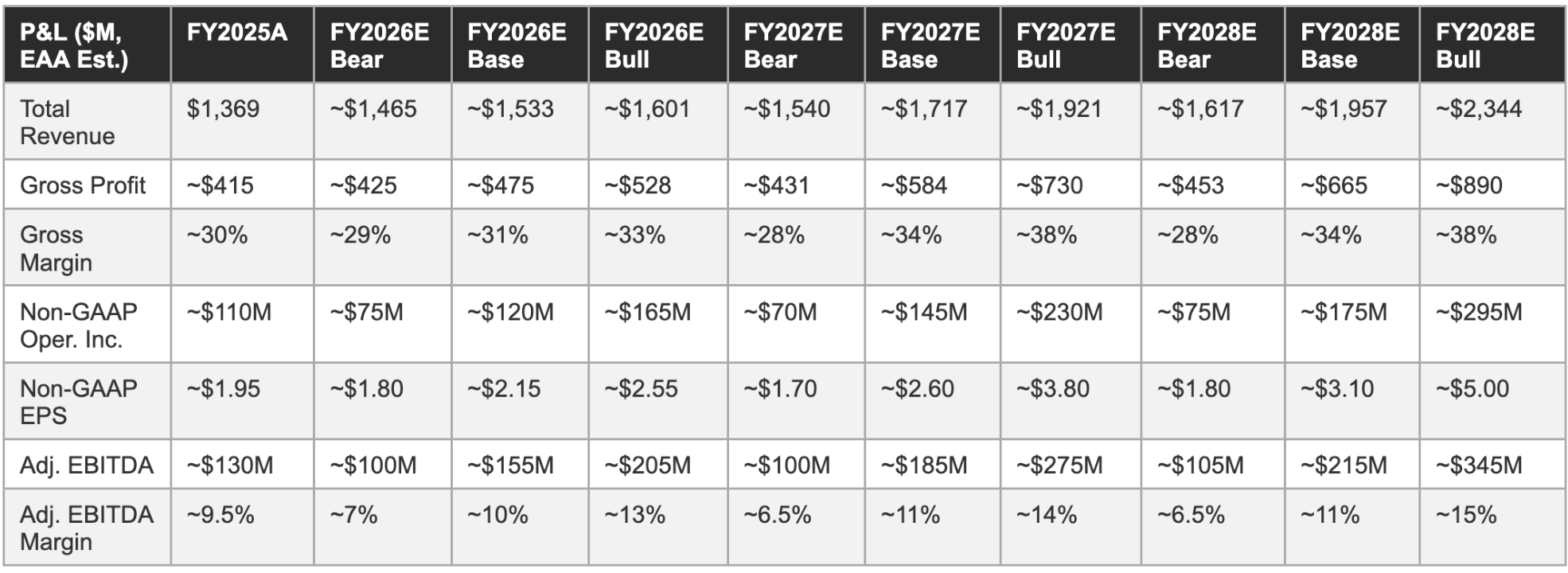

9. Forward Financial Model: Bear / Base / Bull Through FY2028

The three scenarios below are anchored to management’s FY2026 guidance of approximately 12% revenue growth and non-GAAP EPS of $2.15.

Model assumptions

Three-year P&L projection

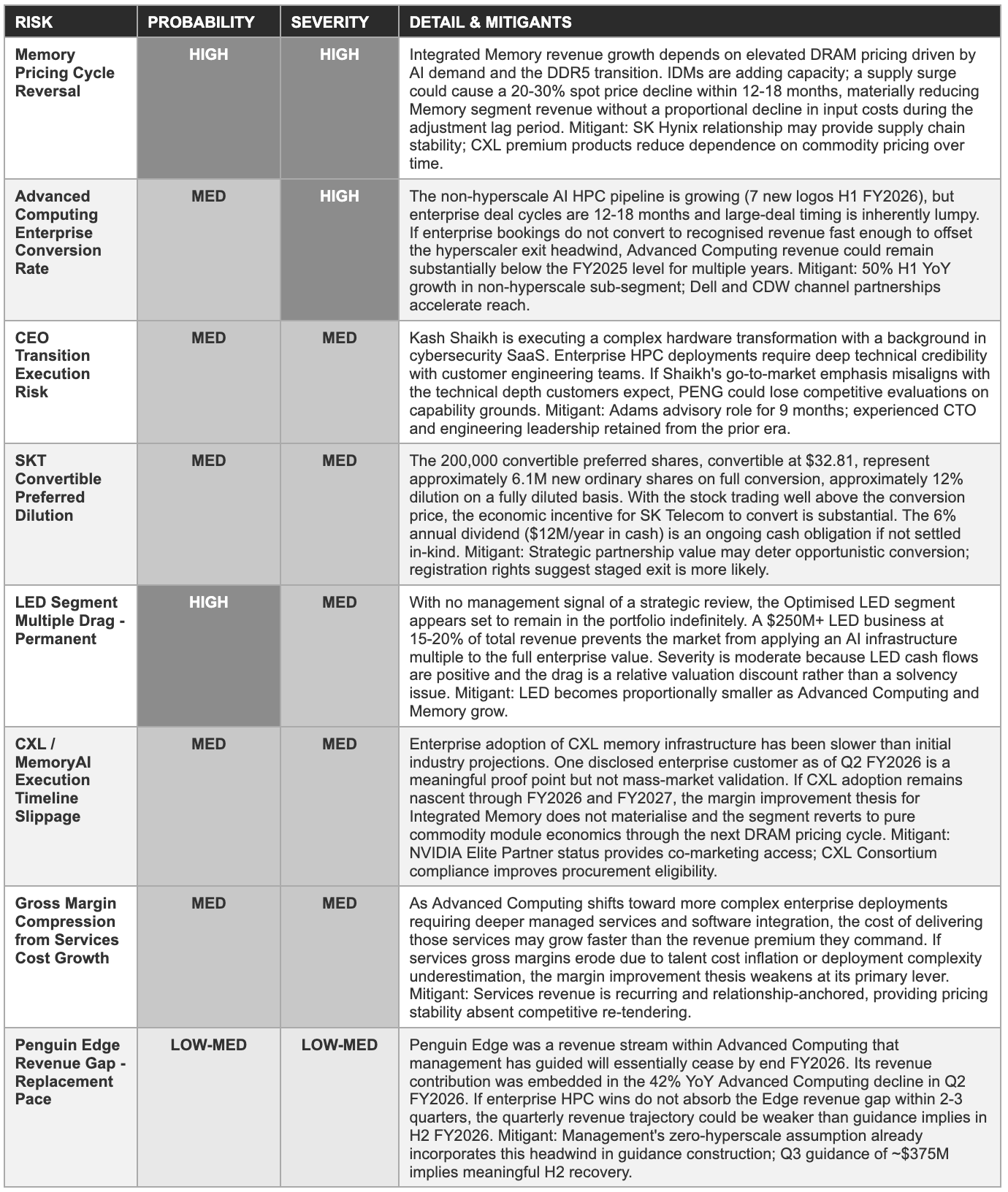

10. Risk Matrix

Each risk below is a specific variable whose outcome determines which forward scenario materialises. Probability reflects likelihood of a materially negative outcome within 24 months; severity reflects the degree of long-term impairment if materialised. Risks are ordered by the combined weight of both dimensions.

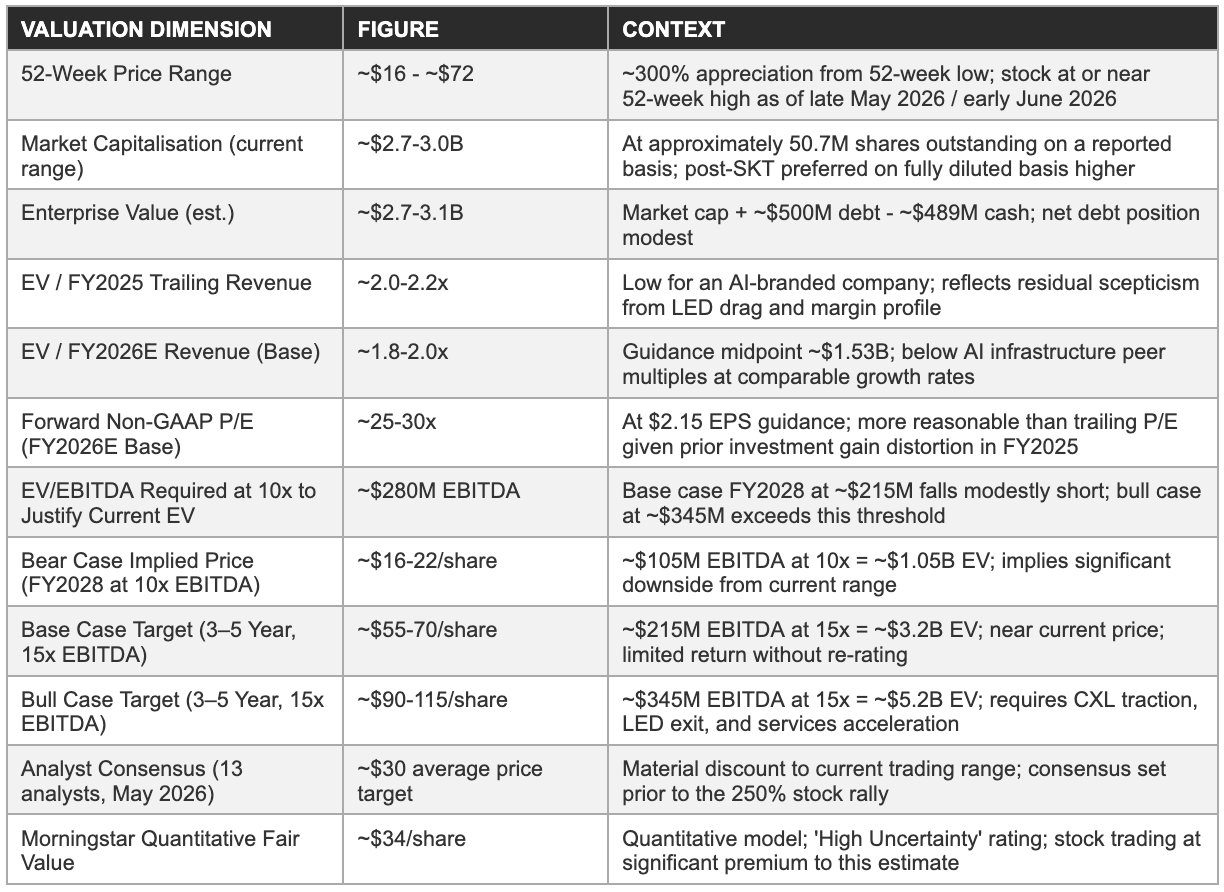

11. The Valuation Question: What the Current Price Requires

PENG’s stock has risen approximately 300% from its 52-week low, compressing forward multiples and raising the performance bar the business must clear. At current levels, the market is pricing in successful execution of the AI factory platform strategy, not merely the possibility of it.

Revenue multiple context

At the current market capitalisation range and TTM revenue of approximately $1.4B, PENG trades at approximately 1.9–2.1x trailing revenue. At the FY2026 guidance midpoint revenue of approximately $1.53B, the forward multiple is approximately 1.8–2.0x. These multiples would be reasonable for a stable, low-growth hardware business.

The market is not pricing PENG as a stable hardware business; the recent move suggests it is beginning to price it as an AI infrastructure growth company. Whether that re-rating is justified depends on whether Advanced Computing enterprise wins accelerate and whether CXL products achieve meaningful commercial traction before the commodity memory cycle turns.

For context, Dell Technologies trades at approximately 1.0–1.2x forward revenue despite its AI server leadership position. HPE trades at approximately 0.7–0.9x forward revenue. Super Micro Computer has traded between 1.0x and 3x forward revenue depending on sentiment around its AI server order book and governance conditions. Pure-play AI infrastructure software companies trade at 8–15x forward revenue. PENG’s current 2x multiple suggests the market is awarding it something between a hardware company and a software-enriched infrastructure platform, a positioning that requires delivery on the services and software differentiation narrative to sustain.

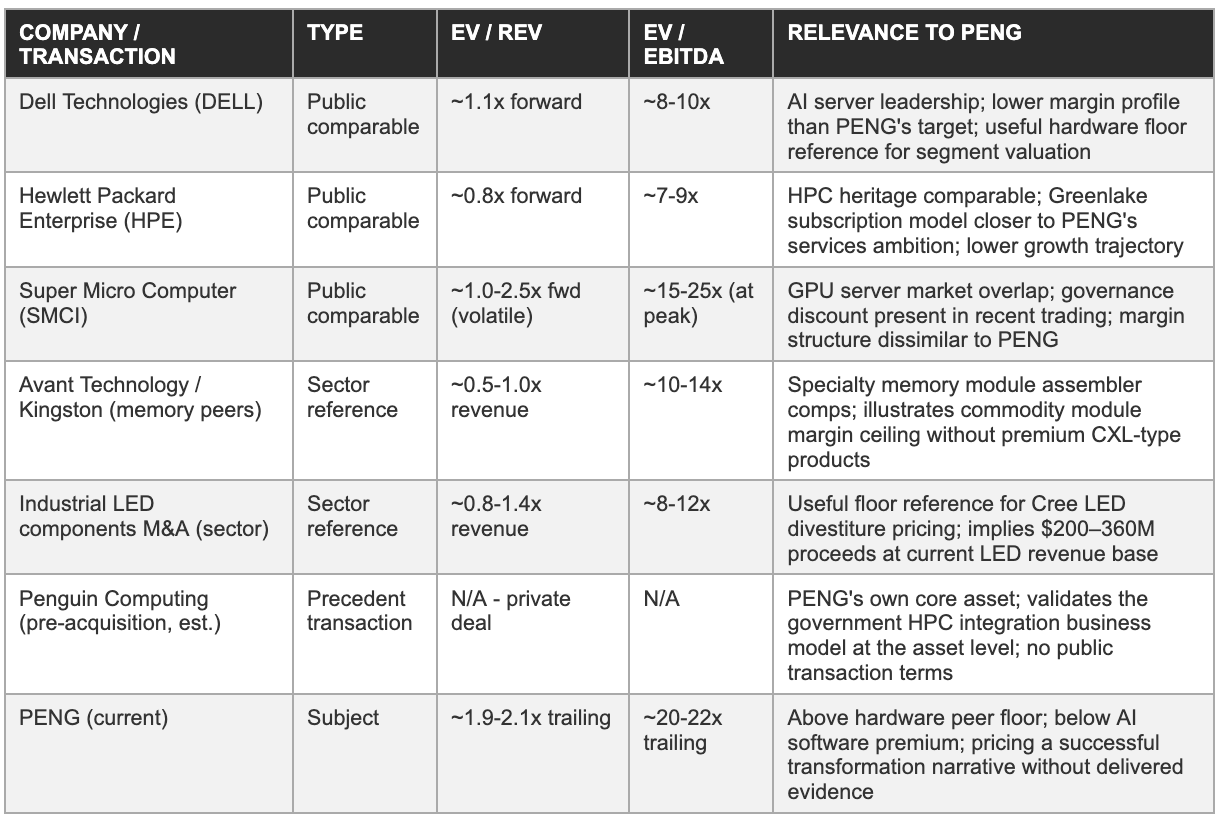

Comparable company and transaction reference

The following table assembles the most relevant comparable companies and reference transactions to contextualise PENG’s current valuation. No single comparable is perfectly analogous: PENG’s three-segment structure, the LED drag, and the transformation phase all differentiate it from pure-play peers. The table is presented as a range of reference points rather than a direct pricing benchmark.

The implied milestone calculation

For a market capitalisation of approximately $2.8B to be rational on a 3–5 year investment horizon, PENG must deliver a revenue and profitability profile that, at a reasonable terminal multiple, implies a fair value at or above the current price. At a 10x EV/EBITDA multiple, consistent with a diversified industrial technology business with modest growth, PENG needs approximately $280M in annual EBITDA to justify a $2.8B enterprise value.

The base case FY2028 EBITDA projection of approximately $215M falls modestly short of this threshold at that multiple. Achieving it requires either the bull case EBITDA trajectory (approximately $345M by FY2028 at a 10x multiple) or a higher multiple assigned by the market to the AI infrastructure narrative.

At a 15x EV/EBITDA multiple, justified if CXL products achieve meaningful revenue and services attach rates improve gross margins toward 35-38%, the base case FY2028 EBITDA of approximately $215M implies an enterprise value of approximately $3.2B, marginally above current levels and implying modest returns over a 3-year hold. The bull case FY2028 EBITDA of approximately $345M at 15x implies approximately $5.2B enterprise value, a materially higher stock price versus current levels. The bear case FY2028 EBITDA of approximately $105M at 10x implies approximately $1.05B enterprise value, a significant decline from current levels.

Valuation framework table

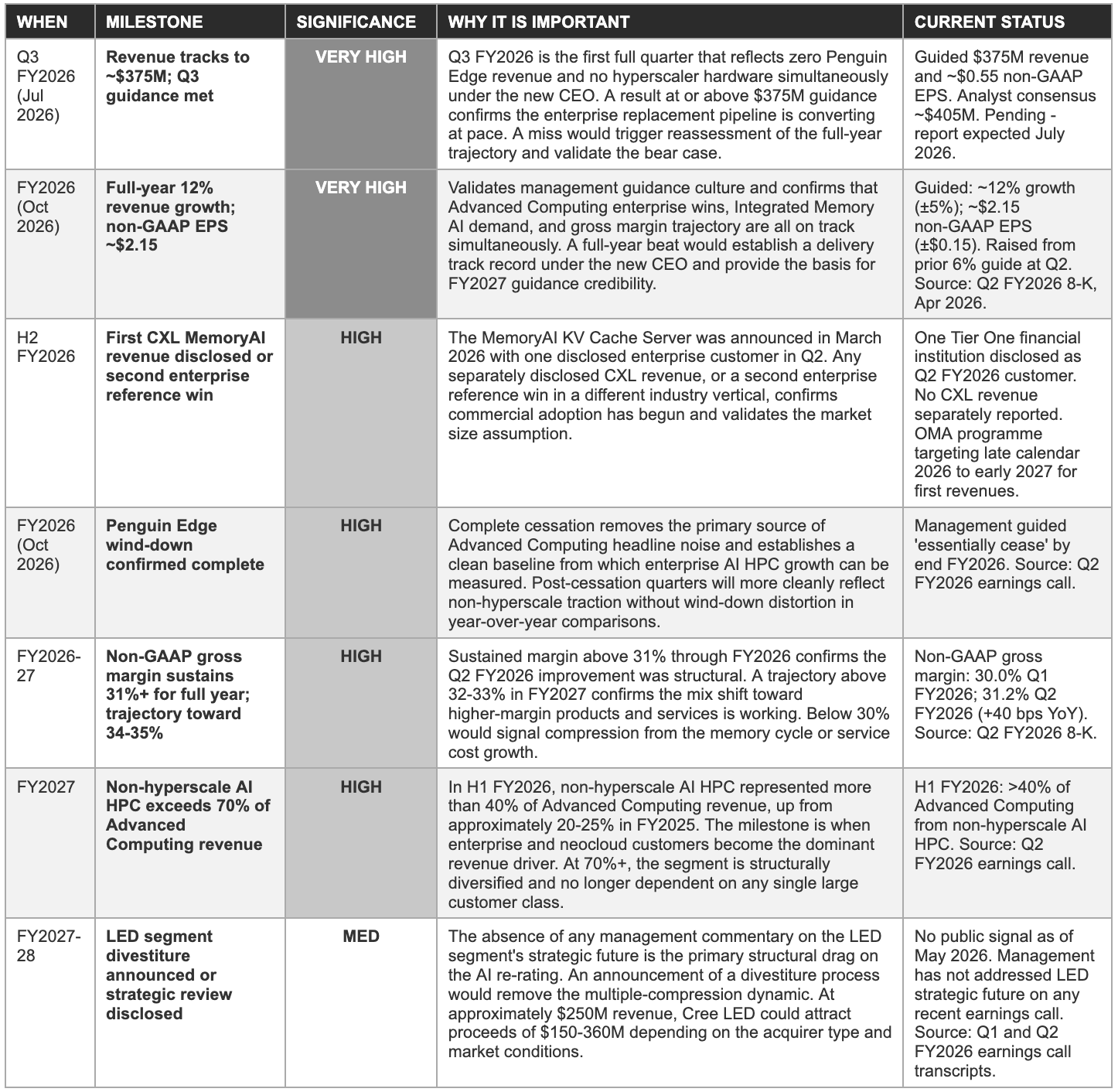

12. Milestone Tracker: What to Watch 2026-2028

The Q3 FY2026 result and FY2026 full-year delivery are the two highest-stakes near-term observations. Everything else is secondary until the trajectory of the hyperscaler exit recovery is confirmed by sequential data.

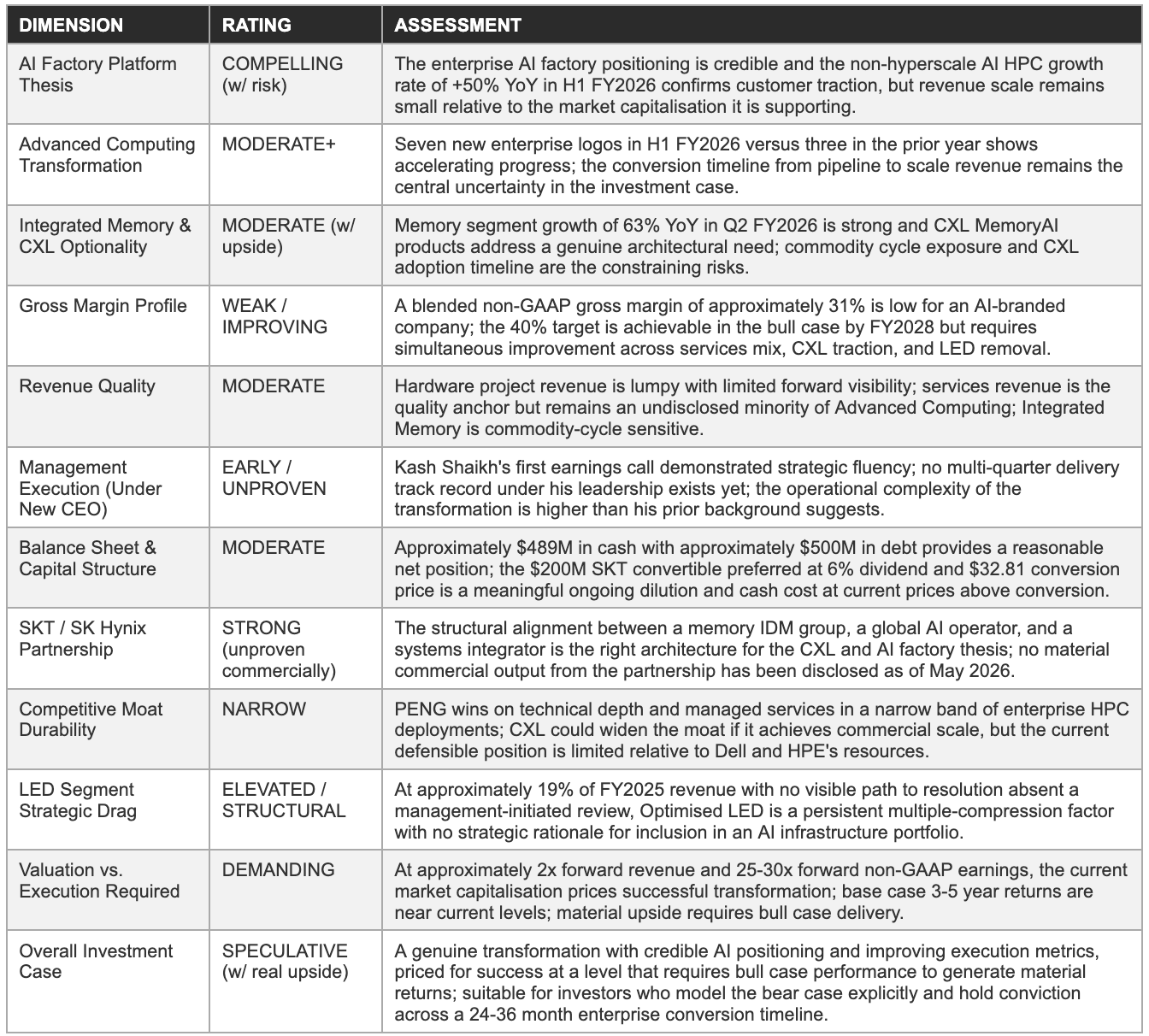

13. Investment Scorecard, Opinion & Conclusion

PENG has genuine strategic positioning and a credible transformation thesis, trading at a price that already reflects successful execution of that thesis. The bull case and the bear case are assessed below with equal weight.

Investment scorecard

The bull case: Four pillars

The first pillar is the inference infrastructure demand curve. AI workloads are shifting from model training, dominated by a small number of hyperscale operators with largely standardised hardware procurement, toward production inference, which requires diverse, on-premise, low-latency deployment architectures across enterprise verticals including financial services, healthcare, government, and education.

This demand curve favours integrators who can deliver custom, managed, on-premise AI compute clusters at enterprise scale with ongoing operational support. PENG’s Penguin Computing heritage and the OriginAI and ICE ClusterWare platform position it as exactly this type of provider in a market that does not yet have a clear dominant incumbent at the custom integration layer.

The second pillar is the memory architecture transition. The key-value cache memory wall, the limitation on AI inference workload performance imposed by the physical DRAM capacity constraints of conventional server architectures, is a genuine and growing problem as context windows expand and multi-agent AI systems place higher memory demands on inference infrastructure. CXL memory disaggregation addresses this wall.

If CXL achieves the adoption trajectory that networking fabric technology achieved from 2012 to 2018, moving from niche HPC deployments to mainstream enterprise data centres over five to six years, PENG’s early commercial position in CXL memory appliances could compound into a structurally differentiated and high-margin product line that justifies a premium to the current multiple.

The third pillar is the SK Group relationship. SK Hynix is investing aggressively in next-generation memory architecture including HBM4 and CXL-capable memory products. A systems integrator with a formal collaboration agreement with SK Hynix and SK Telecom, and $200M of SK capital on its balance sheet, has a preferential development partnership with the memory IDM most aggressively pursuing the AI memory opportunity. This is a product roadmap and supply access advantage that competitors without equivalent IDM relationships cannot replicate on a short timeline.

The fourth pillar is the balance sheet position. Approximately $489M in cash against approximately $500M in debt provides management with the runway to execute the CXL product development cycle, the enterprise sales motion investment, and the managed services capability build without being forced to raise dilutive capital at a depressed valuation. The $46M received from the Zilia Technologies exit in March 2026 improved the position incrementally. The bear case does not create a near-term solvency risk, it creates an execution risk, and the balance sheet provides the time required to address execution shortfalls without financial distress.

The bear case: Four concerns

The first and most acute concern is the valuation level relative to delivered financial evidence. PENG’s stock has risen approximately 250% from its 52-week low in a period during which the company reported a 6% revenue decline in Q2 FY2026 and has not yet delivered a single quarter of data confirming that the enterprise AI HPC replacement pipeline is converting at the pace required to sustain the current market capitalisation. The market is pricing a narrative while the earnings are delivering a transition. If Q3 FY2026 misses the $375M guidance, the multiple compression from these levels could be rapid and severe.

The second concern is the memory cycle timing. The Integrated Memory segment is operating at elevated revenue levels supported by AI-driven DRAM demand and DDR5 transition dynamics, both tailwinds that are likely to moderate as the DDR5 transition matures and as IDM capacity additions respond to the current tight supply environment. If a pricing correction begins in H2 FY2026 or H1 FY2027, Integrated Memory revenue could decline materially from its current elevated level precisely as Advanced Computing is still building its enterprise replacement revenue, creating a simultaneous multi-segment revenue headwind with no near-term offset.

The third concern is the gross margin reality. At approximately 28–31% blended non-GAAP gross margin, PENG’s current margin profile is structurally inconsistent with the premium multiple it is beginning to attract. Software and AI platform businesses trade at high multiples partly because high gross margins generate substantial operating leverage at scale. PENG’s gross margins are closer to those of an OEM hardware assembler than an AI platform provider. If the CXL products take longer than management hopes to achieve meaningful revenue, and if services attach rates improve only gradually, the margin profile the current multiple implies will not be visible in the financial statements for two to three years.

The fourth concern is the LED structural drag combined with management inaction. Every quarter that the Optimised LED segment remains in the portfolio at approximately $250–260M annual revenue, the blended multiple PENG can attract is constrained by the market’s refusal to award AI infrastructure valuations to LED component sales. Management has made no public statement about a strategic review, a divestiture timeline, or even a recognition that the LED segment creates a valuation tension. If LED remains a permanent feature of the portfolio through FY2027 and beyond, the re-rating that the bull case requires is structurally limited by an asset that generates modest but uninspiring cash flows with no connection to the transformation narrative being sold to investors.

The bottom line

Penguin Solutions is a company whose strategic direction is right, whose product development bets are plausible, and whose recent stock performance has moved substantially ahead of its delivered financial evidence. The AI factory positioning is coherent, the SK Telecom anchor is genuinely valuable, the non-hyperscale AI HPC growth rate of 50% in H1 FY2026 is encouraging, and the CXL memory product is addressing a real architectural problem. These are not trivial positives, and they are the foundation of a credible long-term thesis.

The investment case at current price levels is demanding. The market capitalisation of approximately $2.8B on TTM revenue of approximately $1.4B implies that the transformation succeeds, that enterprise AI HPC wins accumulate at pace, that CXL achieves commercial scale, that gross margins expand toward 35-38%, and that the LED segment either exits or becomes immaterial. The base case model suggests that this trajectory is achievable by FY2028, but generates only modest returns from current levels. The bull case generates compelling returns. The bear case generates significant losses.

Investors who purchase PENG at current levels should do so with an explicit and quantified view of the bear case, a position size appropriate for a speculative single-name investment, and a monitoring framework anchored to the Q3 FY2026 result, the FY2026 full-year delivery, and the first evidence of CXL revenue at scale. Those three data points, arriving over the next 8–12 months, will determine whether the current market capitalisation is the beginning of a sustained re-rating or the peak of a narrative-driven move. The two-sentence version of this report’s conclusion: the thesis is real; the price is not yet supported by the evidence.

Sources

This report has been prepared using exclusively publicly available information as of May 2026. Primary sources: Canadian Solar Q1 2026 earnings release and earnings call transcript (May 2026, Globe Newswire); Q4 2025 and full-year 2025 earnings release and earnings call transcript (March 2026, Globe Newswire); Q3 2025 earnings release (November 2025, Globe Newswire); Q2 2025 earnings release (August 2025, Globe Newswire); Canadian Solar 20-F annual report for fiscal year 2024 (filed April 2025, SEC EDGAR, File 0001375877); CS PowerTech joint venture formation disclosure (November 2025, SEC Form 6-K); GLP-1 FlexCare and cholesterol programme press releases where applicable; Omada for Cholesterol press release (February 2026, Globe Newswire); U.S. Patent Trial and Appeal Board final written decisions on Trina Solar TOPCon patent challenges against Canadian Solar subsidiaries (April 2026, USPTO PTAB); Morningstar shares outstanding and market data (May 2026); Stockanalysis.com revenue history and segment data; Bloomberg NEF module price index references (Q1 2026); Wood Mackenzie U.S. utility-scale solar and storage market data (2025 annual report); Lawrence Berkeley National Laboratory Utility-Scale Solar report (2025 edition); U.S. Department of Energy Advanced Manufacturing Production Credit (45X) statutory text and IRS guidance; IRA FEOC framework as codified in 26 U.S.C. § 30D and related Treasury guidance (2024-2025); IEEPA solar tariff proclamations and Federal Register notices (2025-2026); First Solar, JinkoSolar, and Hinge Health public filings referenced for competitive landscape comparisons.

Disclaimer

This report has been prepared by EAA Partners for informational and educational purposes only. It does not constitute financial advice, investment advice, an offer to buy or sell any security, or a solicitation of any investment decision. Nothing in this report should be construed as a recommendation to buy, hold, or sell shares of Penguin Solutions, Inc. (NASDAQ: PENG) or any other security. All information is sourced from publicly available materials believed to be reliable as of June, 2026 but is not guaranteed to be complete, accurate, or current. AI tools were used to assist in refining language and improving clarity, as English is not our first language, but all research, analysis, and conclusions are our own.