QuantumScape

From R&D to Industrial Scale in Next-Gen Energy Storage

Purpose of the Analysis

This analysis is about more than one company, it’s about understanding whether QuantumScape can transform a decade of scientific ambition into industrial and financial reality.

The purpose of this analysis is to evaluate QuantumScape as both a technology innovator and an investment opportunity, separating promise from execution risk. By examining the company’s strategy, financial profile, regulatory environment, and competitive positioning, the goal is to determine whether its solid-state battery technology can realistically transition from laboratory prototypes to commercial-scale production.

This thesis does not aim to provide short-term trading recommendations, but rather to assess QuantumScape’s long-term potential to become a cornerstone of the global energy transition. For investors, the analysis serves as a framework to weigh the asymmetric risk-reward profile inherent in betting on a generational technology shift.

Ultimately, this work serves as both a due diligence exercise and a forward-looking view on where QuantumScape could fit in the broader EV and energy storage ecosystem. The intent is to help investors and industry observers alike separate narrative from substance, while providing perspective on the asymmetric nature of the opportunity: a company that could either stumble under the weight of execution risk or emerge as a generational winner in the electrification “megatrend”.

Table of Contents

Corporate profile

Founding and Evolution

Company Overview

Management and Leadership

Core Products & Technology Platform

Product Applications & Value Proposition

Operational Readiness & Manufacturing Scale-Up

Commercialization Path & Strategic Partnerships

Market Opportunity & Industry Dynamics

Competitive Landscape

Regulatory & Policy Considerations

Financial Profile & Capital Structure

Key Risks & Execution Challenges

Catalysts

Opinion and Target View

Conclusion

Acknowledgements & Disclaimer

1. Corporate Profile

QuantumScape is a U.S.-based advanced battery developer focused on commercializing solid-state lithium-metal batteries, a technology designed to improve energy density, charging speed, and safety compared to conventional lithium-ion cells. The company operates an R&D-driven model supported by strategic partnerships, most notably with Volkswagen, to transition its proprietary technology from pilot-scale validation to automotive-grade production.

QuantumScape positions itself as a potential enabler of the next generation of electric vehicles, aiming to deliver batteries that extend driving range, shorten charge times, and lower total cost of ownership, thereby capturing a critical role in the accelerating global shift to electrification.

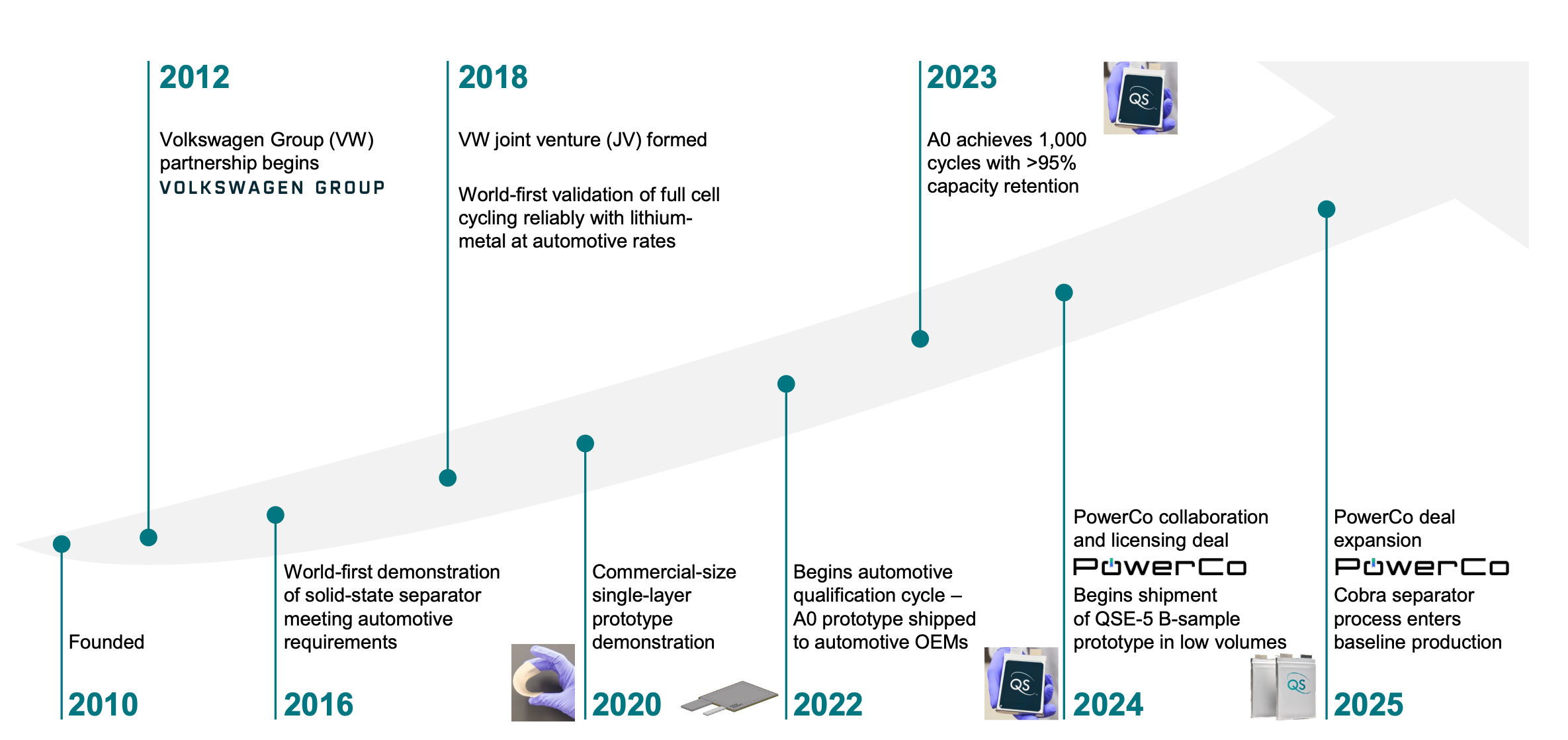

2. Founding and Evolution

Few companies have endured a decade of trial, skepticism, and delay. QuantumScape has, and that endurance may yet redefine the battery industry.

QuantumScape’s history is not one of overnight disruption but of patient persistence in one of the most difficult areas of advanced technology. Since its founding, the company has pursued a singular objective: to make solid-state lithium-metal batteries viable at commercial scale. In a sector where most startups chase incremental gains or pivot under pressure, QuantumScape has doubled down, having technical setbacks, long timelines, and intense scrutiny. This focus has allowed it to build credibility with strategic partners and accumulate the capital needed to sustain a long march toward commercialization. The lesson is that true hard-tech breakthroughs rarely follow smooth trajectories; they are forged through years of resilience and singular focus.

QuantumScape was founded in 2010 by Jagdeep Singh, a Stanford-educated entrepreneur best known for co-founding the optical networking company Infinera, together with Stanford professors Fritz Prinz and Tim Holme. The founders were motivated by a rather simple idea: conventional lithium-ion batteries, while improving incrementally, faced hard limits on energy density, charging speed, and safety due to their liquid electrolyte design.

A breakthrough architecture would be needed if electric vehicles (EVs) were to match the convenience and performance of internal combustion engines. From the beginning, QuantumScape focused exclusively on solid-state lithium-metal batteries, a high-risk, high-reward strategy that differentiated it from peers attempting to optimize existing lithium-ion chemistries.

In its early years, the company operated largely in stealth, funded by venture investors such as Kleiner Perkins and supported by Stanford’s academic ecosystem. This initial phase was marked by a research-driven business model: rather than chasing early revenue, the company prioritized solving fundamental scientific challenges, particularly the development of a stable, dendrite-resistant solid electrolyte.

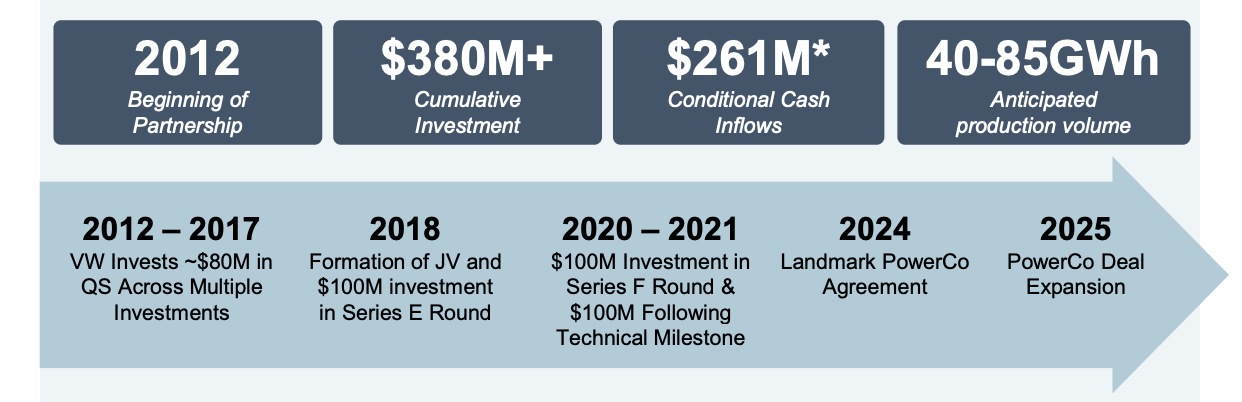

By 2012, QuantumScape had attracted the attention of Volkswagen Group, which made a strategic investment and later established a deep technical collaboration. This partnership was transformative, not only did it provide financial stability, it also positioned QuantumScape within the supply chain of a top-tier automaker, giving the company a clear commercialization pathway at a time when skepticism about solid-state batteries was widespread.

The mid-2010s were a period of intensive R&D. QuantumScape demonstrated proof-of-concept cells that validated the core chemistry and began scaling to larger multilayer formats. Importantly, Volkswagen increased its stake multiple times, committing more than $300 million over several rounds and eventually securing joint development rights. This level of OEM buy-in was rare in the sector and signaled that QuantumScape’s approach was considered technically credible and strategically important. This period framed QuantumScape less as a speculative lab project and more as a potential cornerstone of the EV supply chain, with long development timelines.

The company’s pivotal strategic leap occurred in late 2020, when it went public via a merger with Kensington Capital Acquisition Corp., a SPAC led by automotive industry veteran Justin Mirro. The deal raised over $1 billion in gross proceeds, at the time one of the largest financings in the battery sector, providing a multi-year funding runway to support the transition from laboratory validation to pilot-scale manufacturing.

The IPO coincided with a surge of investor enthusiasm for EV-related companies, propelling QuantumScape’s market capitalization to levels that briefly exceeded established battery makers despite the absence of revenue. While the capital infusion was unquestionably positive, the public listing introduced a new dynamic: execution milestones would now be scrutinized quarterly, and any slippage in timelines could directly impact investor confidence and valuation.

Post-IPO, QuantumScape’s narrative has been defined by progress toward manufacturability. The company established its QS-0 pilot facility in San Jose to produce multilayer cells at pre-commercial scale and began preparing for customer sampling. The partnership with Volkswagen was further institutionalized through a joint venture aimed at building a large-scale manufacturing facility in Europe, although timelines remain contingent on successful scale-up at QS-0.

Key inflection points in recent years have included demonstrating 10-layer and then 24-layer cells, achieving promising cycle-life data, and reporting progress toward fast-charge performance. Each milestone has been accompanied by heightened scrutiny: investors weigh reported technical progress against the risk that scaling challenges could delay or dilute the technology’s eventual commercialization.

Today, QuantumScape stands at a critical juncture in its evolution. Having secured capital, partnerships, and proof-of-concept results, the company is transitioning from a science-driven startup into an execution-driven enterprise. For long-term investors, the company’s history illustrates both its durability, over a decade of persistence in one of the toughest areas of materials science, and the binary nature of its opportunity.

If successful, QuantumScape could supply the enabling technology behind next-generation EVs and capture significant share in a trillion-dollar market; if unsuccessful, it risks being overtaken by faster-moving incumbents or alternative chemistries. The company’s evolution to date underscores why its future rests on proving not just scientific validity, but, most importantly, industrial scalability.

3. Company Overview

QuantumScape is not chasing incremental gains in batteries, it is betting everything on a breakthrough platform that could reset the EV industry’s performance curve.

The company overview of QuantumScape is best understood as a contrast to conventional battery makers. While most of the sector operates within the boundaries of lithium-ion chemistry, focused on cost reductions and incremental gains, QuantumScape has set itself apart by pursuing a fundamentally different architecture. Its mission is not to compete at today’s margins but to unlock tomorrow’s possibilities, aiming to commercialize solid-state lithium-metal cells that directly tackle the three core barriers to EV adoption: energy density, charging time, and safety.

By anchoring itself to a high-risk, high-reward scientific problem and aligning early with Volkswagen, QuantumScape structured itself more like a deep-tech platform than a commodity producer. This unusual positioning is the foundation of its investment case: if successful, it will not simply participate in the battery market, it could redefine it.

Business focus and mission

QuantumScape Corporation is a U.S.-based advanced battery developer focused on one of the most ambitious goals in clean technology: commercializing solid-state lithium-metal batteries at scale.

Its strategic focus has always been on solving the hard science problem that constrains EV adoption, how to build a fundamentally better battery, not just an incrementally improved one. At the center of QuantumScape’s mission is the belief that step-change advances in energy storage are essential to make electric vehicles competitive with, and ultimately superior to, internal combustion engines on convenience, cost, and performance.

Unlike conventional battery companies that generate revenue early by supplying commodity cells, QuantumScape is structured more like a deep-tech platform company. It has spent over a decade operating in an R&D-driven model, funded by a combination of venture capital, strategic investors, and later public equity markets.

The company’s business model reflects this focus on capital efficiency and long-term positioning. Rather than building massive factories prematurely, QuantumScape plans to progress through stages: laboratory validation, pilot-scale production (the QS-0 line in San Jose), customer sampling, and eventual scale-up in joint facilities with OEMs.

The model envisions multiple revenue streams in the future: direct cell sales through joint ventures, licensing of its proprietary solid-state electrolyte platform, and potentially partnerships beyond automotive, such as in stationary storage or aerospace. Importantly, QuantumScape’s structure allows it to leverage partners’ manufacturing and distribution capabilities while retaining control over its intellectual property, which already includes more than 200 issued or pending patents.

The mission and business design highlight both the opportunity and the risk. The opportunity is clear: if QuantumScape succeeds in achieving its stated performance metrics at commercial scale, it will not simply be another battery supplier, it could redefine the EV value chain and capture disproportionate economics. The risk is equally apparent: as a pre-revenue company dependent on technology scale-up, its future rests on execution over the next five to ten years. Yet this asymmetric profile, the chance to enable the next generation of EVs against the risk of technical or manufacturing failure, is precisely what attracts long-term investors seeking exposure to transformative clean technology.

Market need and problem definition

The transition to electric vehicles (EVs) represents one of the largest industrial shifts of the 21st century, yet it remains constrained by the limitations of today’s lithium-ion batteries. While these batteries have enabled the first wave of EV adoption, they are reaching the practical limits of their performance envelope. The average EV sold today offers a range of 250-300 miles under standard conditions, which, while acceptable for early adopters, still lags consumer expectations shaped by internal combustion vehicles capable of 400–500 miles per tank.

Extending EV range generally requires larger, heavier, and more expensive battery packs, a trade-off that erodes efficiency and profitability. Charging remains another barrier: even at high-powered fast chargers, most EVs still require 30-40 minutes to achieve an 80% charge, a timeframe that falls short of the convenience consumers expect. Safety also remains a persistent concern, as the flammable liquid electrolytes used in lithium-ion batteries can lead to catastrophic failures under thermal runaway conditions.

For automakers, these technological ceilings represent more than an engineering inconvenience, they are a strategic and regulatory risk. Governments in the U.S., Europe, and China have introduced aggressive targets to phase out internal combustion engine sales within the next 10-15 years. To comply, OEMs must not only scale EV production but also convince mass-market consumers to adopt them. That requires batteries with longer ranges, faster charging, and uncompromised safety, delivered at cost structures that allow for profitability.

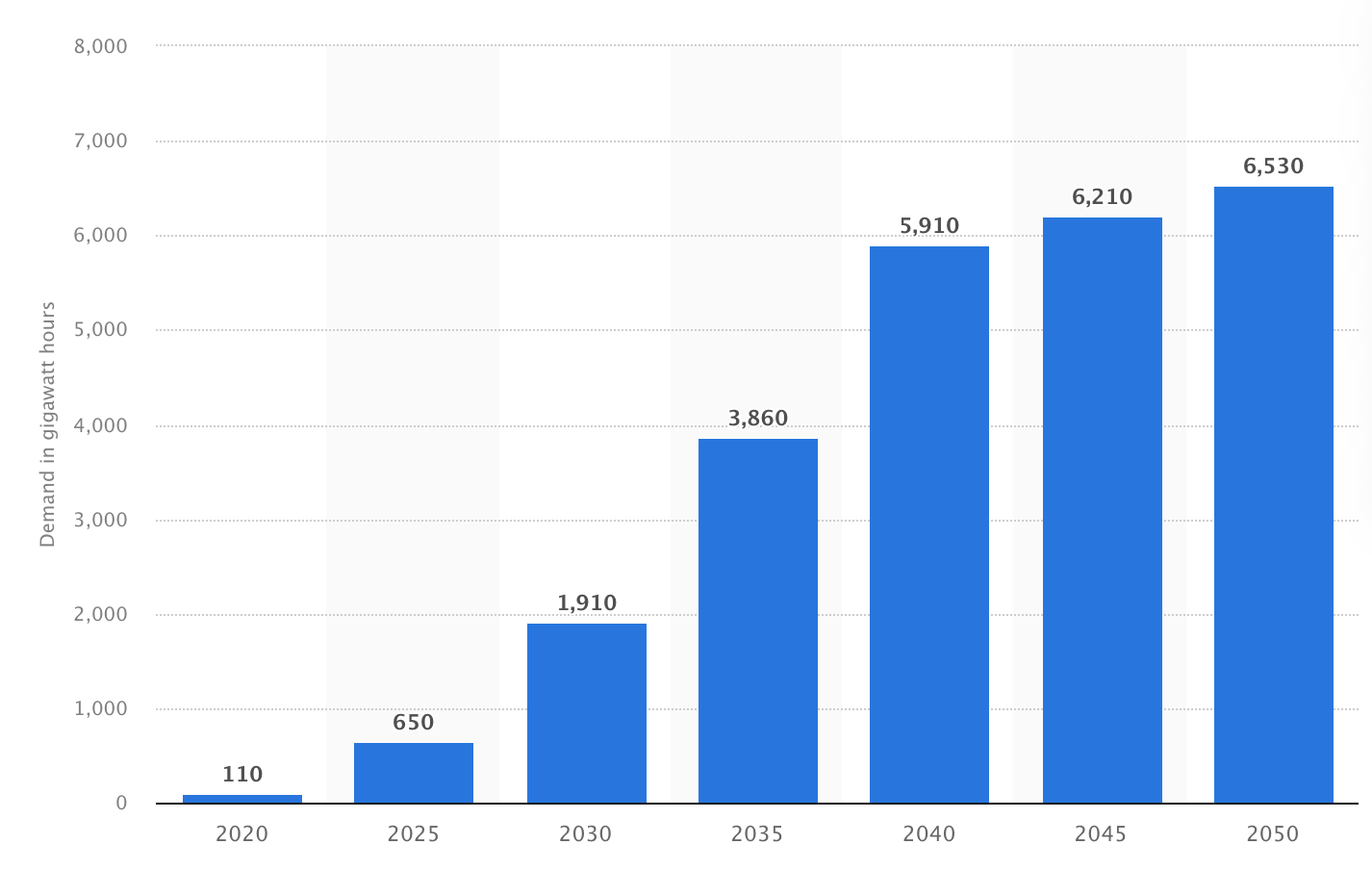

The scale of the challenge is immense: by 2030, global EV sales are projected to require several terawatt-hours of annual battery capacity, creating a trillion-dollar market opportunity in energy storage. Yet most of the world’s battery supply chain remains committed to incremental lithium-ion improvements, leaving a gap for technologies that can provide a step-change in performance.

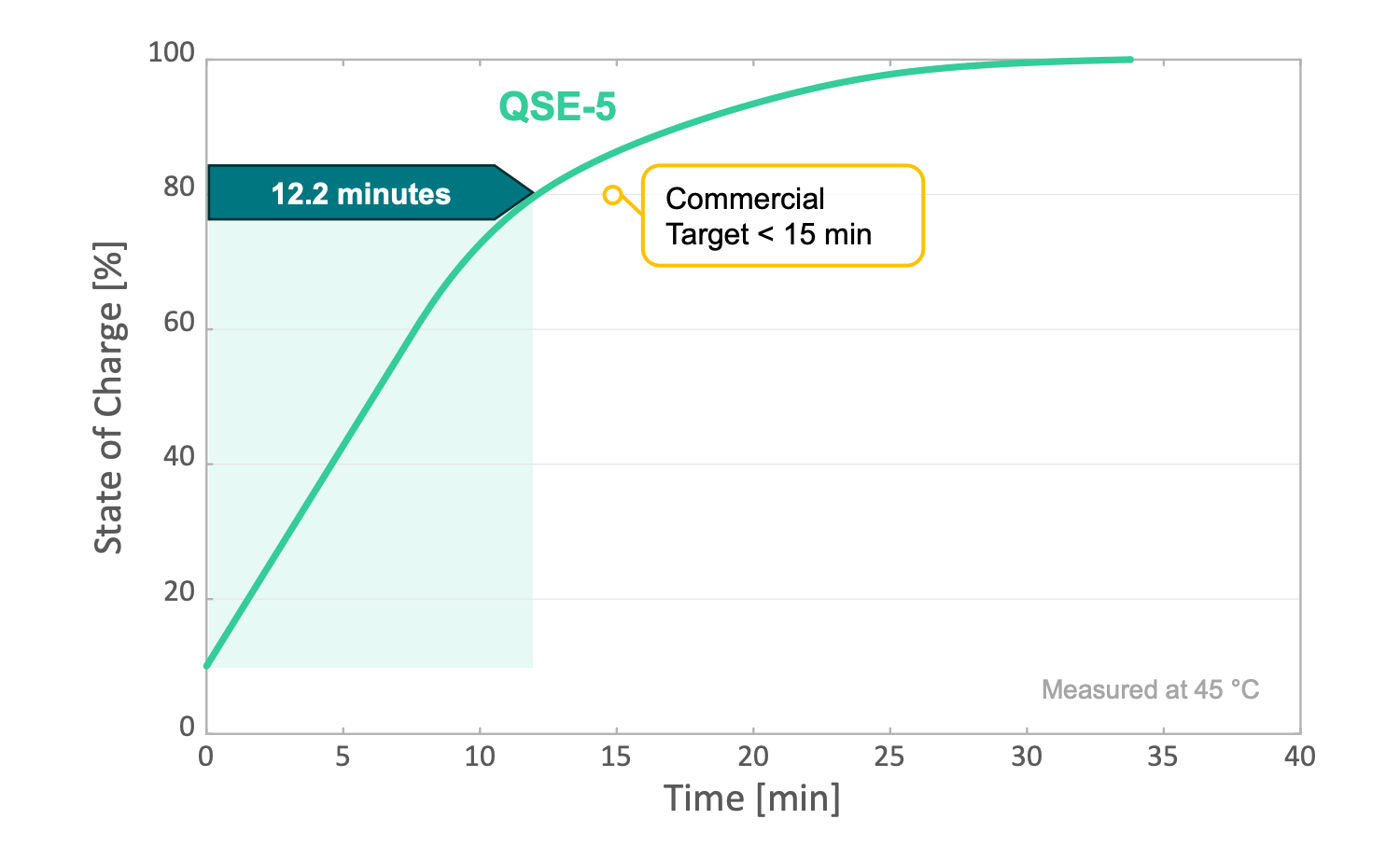

This gap defines QuantumScape’s addressable problem. The company’s solid-state lithium-metal design is positioned to directly target the three key consumer and OEM pain points: energy density, charging speed, and safety. By eliminating the liquid electrolyte and enabling lithium-metal anodes, QuantumScape aims to double energy density, allow an 80% recharge in under 15 minutes, and substantially reduce fire risk.

This is not merely an engineering milestone, it is a commercial imperative. As EV penetration accelerates, the OEMs that secure access to superior batteries will capture market share, while those locked into standard lithium-ion chemistries risk commoditization. The timing is critical: the next five years will determine which technologies are validated and scaled in time to meet the 2030 regulatory mandates. QuantumScape’s proposition is to be at the forefront of that transition, offering investors exposure to one of the few technologies with the potential to reset the performance curve of the EV industry.

How QuantumScape’s platform addresses the problem

QuantumScape’s platform is designed to solve the core limitations of lithium-ion batteries by replacing the liquid electrolyte with a proprietary solid ceramic electrolyte and enabling the use of pure lithium-metal as the anode. This architectural shift is fundamental. In conventional lithium-ion cells, the graphite anode occupies substantial volume and weight, limiting how much energy can be stored.

By contrast, lithium-metal anodes offer far higher theoretical energy density. The obstacle historically has been dendrite formation, needle-like growths that short-circuit the cell when lithium is plated onto the anode during charging. QuantumScape claims its solid electrolyte not only blocks dendrites but also allows stable cycling across hundreds of charge-discharge events. If validated at scale, this would unlock a practical pathway to doubling energy density relative to leading lithium-ion cells.

The company has also prioritized fast-charging performance, another consumer pain point. Laboratory data released by QuantumScape suggests its cells can achieve an 80% charge in under 15 minutes without significant degradation. Achieving this at scale would close one of the biggest psychological gaps for consumers comparing EVs with gasoline vehicles. Safety is a third pillar of the value proposition: the solid electrolyte is nonflammable, eliminating the liquid components most prone to combustion in thermal runaway scenarios. This addresses not only consumer confidence but also regulatory and insurance risk, factors that can materially impact EV adoption curves.

Strategically, QuantumScape has focused on maintaining an IP-led platform rather than pursuing early commoditization. Its solid electrolyte design, along with manufacturing processes and cell architecture, are covered by a growing patent portfolio of more than 200 issued or pending patents. This intellectual property is key to the business model: rather than competing directly in the crowded lithium-ion market, QuantumScape intends to supply differentiated cells via joint ventures with automotive OEMs. Volkswagen is the anchor partner, but the platform could theoretically extend to other automakers, consumer electronics, and even grid-scale storage over time.

The near-term execution focus is on manufacturability. Building the QS-0 pilot line in San Jose represents the first step toward proving that its solid-state cells can be produced reliably in multilayer formats, moving from single-layer test cells to 10-, 24-, and eventually 48-layer commercial prototypes. This transition from scientific feasibility to industrial scalability is the most critical inflection point for the company. QuantumScape’s platform offers an asymmetric profile: if the solid electrolyte delivers at scale, the company could leapfrog lithium-ion incumbents and establish itself as a foundational supplier to the EV industry. If it fails, however, years of R&D investment may not translate into commercial relevance. The binary nature of this outcome underscores why QuantumScape is viewed as both a high-risk and potentially transformative investment.

What makes QuantumScape’s profile compelling is not just the technology it pursues but the structure of its strategy. By resisting premature scale-up, focusing on IP protection, and leveraging partners for manufacturing and distribution, the company has designed a model that maximizes upside while mitigating some capital intensity. Its roadmap, from lab validation to pilot-scale to joint ventures, reflects both discipline and ambition.

The overview underscores why QuantumScape is a binary play: years of scientific progress have positioned it as one of the few credible contenders to challenge lithium-ion’s dominance, but execution on manufacturability will determine whether it becomes a cornerstone of the EV supply chain or another casualty of hard-tech risk. The opportunity is generational, the risk, structural, but that is precisely the asymmetry that attracts long-term capital.

Ultimately, the success of this technological and commercial vision depends not only on the strength of the platform, but also on the caliber of the team tasked with executing it, making leadership a critical next focus

4. Management and Leadership

QuantumScape’s leadership is a blend of visionary founders and seasoned operators, united by the task of transforming breakthrough science into industrial reality.

At the heart of QuantumScape’s investment case lies its leadership team. The company’s journey has moved beyond scientific discovery into the far more difficult phase of manufacturing readiness, requiring not only technical brilliance but also operational discipline, financial stewardship, and legal resilience.

From co-founder and CTO Tim Holme, who has provided continuity of vision since inception, to CEO Siva Sivaram, an industry veteran renowned for scaling complex technologies, the team reflects a carefully constructed balance of science and execution. Their combined expertise ensures that QuantumScape is not just advancing chemistry but also building the organizational and operational framework required to industrialize it. For investors, leadership is not an accessory here, it is the decisive factor that determines whether potential becomes reality.

Dr. Siva Sivaram - President & CEO

Professional background and career milestones

Dr. Siva Sivaram is a seasoned technologist and executive whose career spans over three decades, distinguished by leadership roles across semiconductor, data storage, and cleantech industries. He holds a Ph.D. and M.S. in Materials Science from Rensselaer Polytechnic Institute and a B.S. in Mechanical Engineering from the National Institute of Technology, Tiruchirappalli. His early career includes key operational and leadership roles at Intel and Matrix Semiconductor, where he gained significant experience in pioneering 3D semiconductor technologies.

Later, as Executive Vice President of Memory Technology at SanDisk, he oversaw the development of breakthrough NAND flash memory innovations, including early 3D NAND architecture.

In 2008, Dr. Sivaram founded Twin Creeks Technologies, marking his transition into entrepreneurship by steering advanced solar cell and equipment manufacturing. This venture reinforced his capacity to translate research-intensive technologies into scalable product lines. After Twin Creeks, he held senior roles at Western Digital, becoming Executive Vice President of Technology and Strategy and ultimately President of Technology and Strategy. In these capacities, he shaped corporate strategy and operational scaling for one of the world’s largest data storage firms.

He joined QuantumScape in September 2023 as President, tasked with heading technology and manufacturing teams precisely as the company began its transition from lab-based validation to commercial prototyping. In February 2024, he was appointed CEO and a Board member, marking the culmination of a carefully planned leadership transition. His track record of translating complex technologies into high-volume products positions him uniquely to lead QuantumScape through its most critical growth phase. Cultura- and scale-oriented, Dr. Sivaram is the kind of operator who brings scientific capabilities into industrial reality.

Founding vision & role in shaping strategy

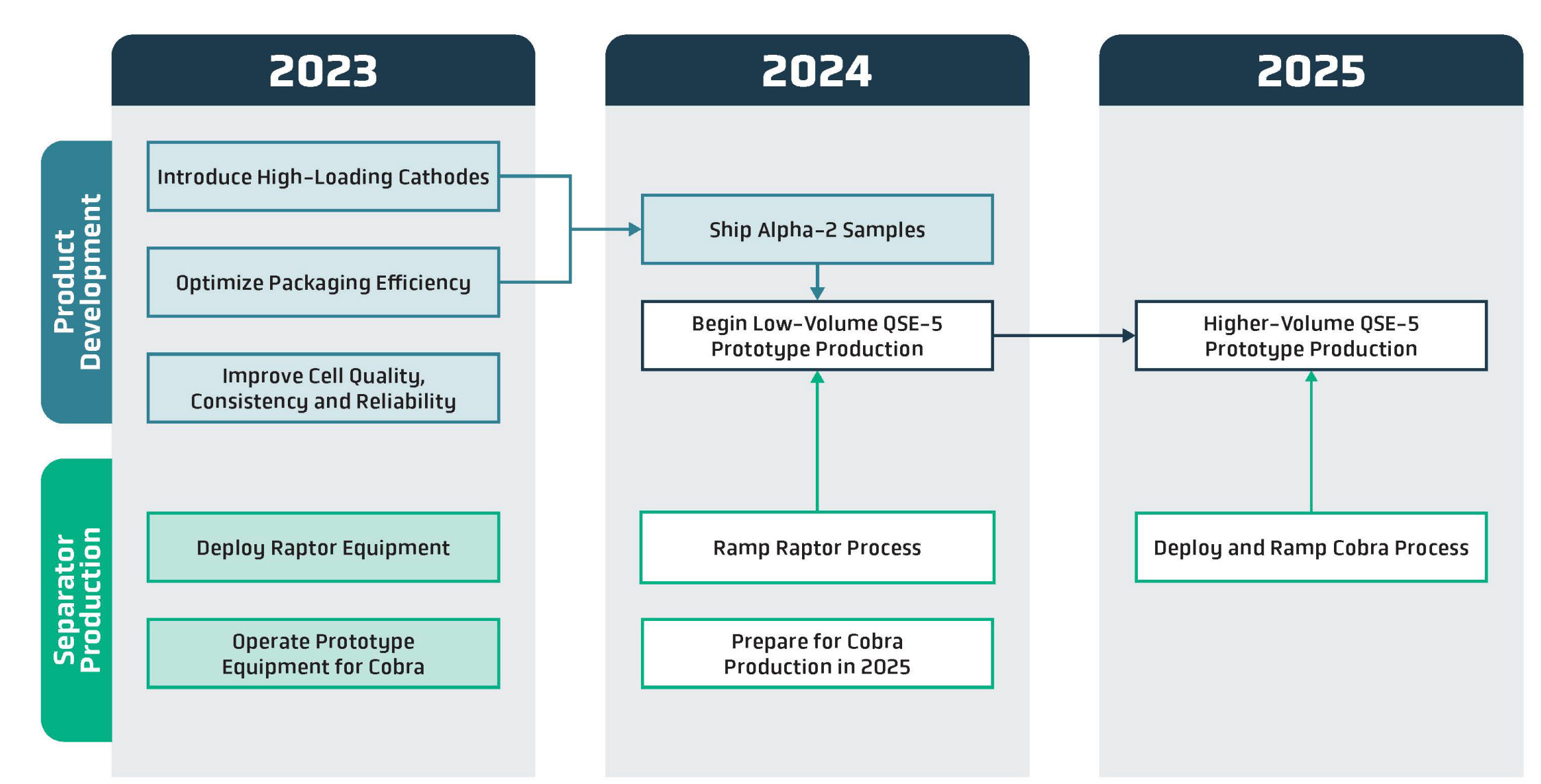

Although not a founder, Dr. Sivaram has become the operational steward of QuantumScape’s decade-old vision: to revolutionize energy storage with solid-state lithium-metal batteries. Upon his arrival as President, the company had already established a compelling technology base but lacked a manufacturing mindset. Dr. Sivaram immediately began aligning R&D with pragmatic milestones, such as shipping “Alpha-2” prototypes to automotive customers and defining the QSE-5 cell as its first planned commercial product.

His strategic influence extends to developing a three-part blueprint emphasizing real-world demonstration, ecosystem-building, and continual platform innovation. He has framed the QSE-5 as the launching point for showcasing the company’s technology in production-relevant formats, while also working to forge partnerships across materials suppliers, equipment vendors, and OEMs. Under his direction, QuantumScape pursued a capital-light model, partnering with PowerCo (Volkswagen’s battery unit) to industrialize manufacturing rather than build proprietary gigafactories outright. This model reflects a strategic shift, from building everything in-house to orchestrating a networked platform approach.

Equally important is his role in reframing how the company communicates with investors. Where the founder’s narrative leaned heavily on scientific breakthroughs, Dr. Sivaram now emphasizes industrial feasibility, roadmap clarity, and cross-functional execution. He has introduced greater transparency into milestone reporting, which over time can reduce volatility in investor sentiment. By grounding QuantumScape’s long-term plan in manufacturing realism, while maintaining aggressive innovation, he is positioning the company to deliver on the founder’s vision with timelines and execution discipline that long-term investors can track credibly.

Leadership style & execution track record

Dr. Sivaram leads with a highly pragmatic, execution-focused style defined by transparency, humility, and operational discipline. He has emphasized that “manufacturing teaches you humility,” reflecting recognition that scaling technologies emphasizes consistency over laboratory breakthroughs. His public statements consistently communicate realistic, iterative progress: for example, discussing prototype performance data and milestones without overpromising or speculative rhetoric.

He also prioritizes close collaboration with partners and customers. Dr. Sivaram has underscored the importance of early feedback loops, evident in how he described Alpha-2 customer shipments as a critical input in accelerating product readiness. This iterative feedback-oriented mindset reflects a quality-centric leadership philosophy. He is known for being detail-oriented, ensuring that engineering, operations, and partner engagement are tightly aligned. Importantly, he appears comfortable making trade-offs, recognizing that premature scaling could undermine credibility more than delayed progress.

What distinguishes his leadership is not just technical expertise but his credibility with both engineers and investors. In past roles at Western Digital and SanDisk, he earned a reputation for bringing advanced semiconductor and storage technologies into mass production without compromising quality. That track record reassures stakeholders that QuantumScape’s bold claims will be matched with disciplined execution. For a company where investor trust hinges on meeting milestones, Dr. Sivaram’s blend of pragmatism and accountability provides a stabilizing force. His style helps cultivate confidence that the company’s scientific promise is backed by industrial merit, making him an indispensable figure in QuantumScape’s next chapter.

Alignment with investors & role in investment thesis

Dr. Sivaram’s compensation reflects the significance of his role: in addition to base salary and bonus opportunities, he received substantial equity awards tied to time and performance milestones, aligning his incentives with QuantumScape’s success. Such alignment underscores his personal stake in delivering results. For long-term investors, equity-heavy pay packages are critical, as they link executive outcomes with shareholder value creation.

In the context of your investment thesis, he is the linchpin. QuantumScape’s potential, redefining EV energy storage, rests on one key execution vector: scaling prototype cells into manufacturing-grade products in partnership with OEMs. Dr. Sivaram’s track record suggests he is uniquely capable of delivering on that vector. His background gives institutional credibility, reduces execution risk, and enhances the likelihood that technical breakthroughs translate into commercial relevance.

Moreover, his presence as CEO signals to both partners and markets that QuantumScape is serious about moving beyond the laboratory. Investors often discount pre-revenue technology firms due to lack of experienced industrial leadership; Dr. Sivaram directly addresses that concern. His background in scaling complex, capital-intensive technologies makes him not only a steward of the company but also a bridge of confidence between the lab, the factory floor, and Wall Street. Without him, the story remains a speculative science project; with him, it evolves into a credible industrial execution play. That asymmetry of outcomes, contingent on his leadership, is central to why long-term investors must evaluate his role as inseparable from the QuantumScape thesis.

Dr. Tim Holme - Co-founder & Chief Technology Officer

Dr. Tim Holme is one of QuantumScape’s original co-founders and a key architect of its scientific foundation. He holds a Ph.D. in mechanical engineering from Stanford University, where his research specialized in electrochemical energy systems. Prior to founding QuantumScape, his academic and professional work centered on solving materials and engineering challenges at the intersection of energy and sustainability. This background gave him the technical grounding to lead the development of QuantumScape’s solid-state battery architecture and to oversee its transition from theoretical concept to a validated prototype platform.

In his current role as Chief Technology Officer, Dr. Holme is responsible for guiding the company’s technical vision and overseeing all aspects of research and development. He leads teams focused on electrolyte chemistry, lithium-metal anode integration, and multilayer cell design, ensuring that the firm maintains its edge in a field crowded with competitors chasing incremental advances. Strategically, Holme’s work is not confined to the lab; he plays a pivotal role in aligning long-term R&D with productization goals, ensuring that scientific progress translates into manufacturable outcomes. His leadership has been instrumental in key milestones such as the validation of multi-layer solid-state prototypes and the progression of pilot-line cells for customer sampling.

Dr. Holme’s role is especially critical given the nature of QuantumScape’s thesis. Unlike more established lithium-ion players, the company’s differentiation lies entirely in its ability to execute on a new technology paradigm. As CTO and co-founder, Holme provides both continuity and credibility, ensuring that the scientific rigor underpinning the platform is not diluted as the firm moves toward commercialization. His influence is central to maintaining the company’s technological edge while navigating the inevitable trade-offs between speed, scalability, and performance. Without his stewardship, the risk of strategic drift or technical misalignment would be significantly higher. In short, Holme embodies the link between QuantumScape’s founding vision and its future industrial execution, making his role indispensable to both the company’s success and its long-term investment case.

Dr. Mohit Singh - Chief Development Officer

Dr. Mohit Singh brings a strong background in materials science and battery research, with a Ph.D. in Materials Science and Engineering from Stanford University. Before joining QuantumScape, his career included extensive academic and industry work in electrochemistry, energy storage, and material innovation. His combination of scientific expertise and practical engineering knowledge positioned him to contribute directly to the firm’s core mission of solving the most difficult challenges in solid-state battery development.

As Chief Development Officer, Dr. Singh plays a pivotal role in bridging the gap between research breakthroughs and scalable productization. He is responsible for the design, testing, and iteration of multilayer solid-state cells, leading cross-functional teams that span materials engineering, process development, and systems integration. His work ensures that QuantumScape’s laboratory results are translated into cells that can withstand real-world automotive conditions, meeting the stringent performance, durability, and safety requirements of OEM partners. Strategically, Singh’s oversight of development activities aligns the firm’s technical roadmap with customer milestones, including the delivery of Alpha and B-sample prototypes. By focusing on manufacturability, reliability, and performance validation, he ensures that QuantumScape’s technology matures in step with commercial expectations.

Laboratory successes are meaningful, but the investment thesis requires consistent demonstration of progress toward automotive-grade batteries. Singh’s leadership mitigates a major risk in deep-tech ventures: the failure to bridge the “valley of death” between science and commercialization. His position ensures not only that R&D stays aligned with long-term strategy but also that each milestone reduces uncertainty in the company’s path to market. By driving development discipline, he enhances the probability that QuantumScape’s groundbreaking electrolyte and anode technology can be industrialized at scale, making him a central figure in turning the company’s vision into investable reality.

Dr. Luca Fasoli - Chief Operating Officer

Dr. Luca Fasoli holds a Ph.D. in Physics from the Swiss Federal Institute of Technology (ETH Zurich) and has built a career that blends deep technical expertise with operational leadership. Before joining QuantumScape, he served in senior roles at Applied Materials and other high-tech firms, where he gained experience in scaling advanced manufacturing processes for complex technologies. His background provides him with both the scientific literacy to engage with QuantumScape’s research-heavy environment and the operational acumen to translate innovation into disciplined execution.

As Chief Operating Officer, Dr. Fasoli is responsible for overseeing QuantumScape’s day-to-day operations, with a particular focus on scaling the company’s pilot production capabilities. He manages the integration of engineering, manufacturing, supply chain, and quality systems to ensure that QuantumScape’s prototypes evolve into production-ready cells. His role involves building the operational infrastructure that allows scientific breakthroughs to be repeated at industrial volumes, a challenge that requires both process rigor and cross-functional coordination. Strategically, Fasoli is central to the company’s pilot line (QS-0) and the eventual build-out of joint manufacturing ventures with OEM partners. His leadership ensures that operational execution keeps pace with customer demands and investor expectations, turning technological progress into measurable output.

QuantumScape’s investment thesis hinges not only on the promise of solid-state technology but also on the company’s ability to manufacture consistently at scale. This is where operational leadership becomes a decisive factor. Without a COO capable of aligning R&D, engineering, and production processes, even the best scientific platform would risk stalling in the transition to commercialization. Fasoli’s experience in scaling complex technologies directly reduces this execution risk. For long-term investors, his presence provides confidence that QuantumScape is building not just a breakthrough battery, but the operational backbone required to support industrial-scale production. In this sense, Fasoli is more than an operator; he is the architect of the company’s ability to deliver on its promises at commercial scale, making his role fundamental to the long-term value creation thesis.

Kevin Hettrich - Chief Financial Officer

Kevin Hettrich brings more than two decades of financial leadership across high-growth and technology-driven industries. He holds a degree in finance and has served in senior financial roles at large public companies, including SanDisk and Western Digital. His career has been defined by managing complex capital structures, leading financial planning and analysis teams, and supporting technology organizations through both rapid expansion and restructuring phases. This background gives him a blend of operational finance expertise and capital markets experience, skills well-matched to a pre-revenue, R&D-heavy company like QuantumScape.

As Chief Financial Officer, Hettrich’s role goes far beyond traditional balance sheet oversight. He is responsible for stewarding QuantumScape’s capital, ensuring that the company maintains sufficient liquidity to fund its technology development and pilot production programs through the mid-2020s. This involves structuring budgets for R&D, manufacturing scale-up, and joint venture commitments while maintaining the discipline needed to operate as a pre-revenue firm in public markets. He also manages investor relations, articulating the company’s progress and capital requirements to a market that scrutinizes execution risk closely. Strategically, Hettrich is tasked with aligning the company’s long-term financing needs with its staged commercialization milestones, reducing dilution where possible while maintaining flexibility to raise capital when required.

Unlike established manufacturers with steady operating cash flows, QS’s valuation and survival depend heavily on prudent capital management. Missteps in financing strategy, investor communication, or cost discipline could compromise the firm’s ability to reach commercialization. Hettrich’s leadership mitigates these risks by ensuring a transparent, staged financing roadmap tied to technical milestones. His ability to sustain market confidence, while balancing burn rate with the enormous capital needs of scaling, will likely determine whether the company can navigate the next five years without excessive shareholder dilution. For long-term investors, his role is not just administrative but existential: he manages the lifeline that will determine whether QuantumScape has the runway to turn breakthrough science into a viable industrial business.

Michael McCarthy - Chief Legal Officer & Head of Corporate Development

Michael McCarthy brings over two decades of legal and corporate development expertise, with a career spanning leadership roles in both private and public companies. He holds a J.D. and has served as General Counsel and corporate secretary in several technology-driven organizations, including SanDisk and Western Digital. His background includes leading complex corporate transactions, managing intellectual property strategy, and overseeing governance in highly regulated, innovation-heavy industries. This mix of transactional and operational experience makes him well-suited to support QuantumScape as it navigates the dual challenges of rapid growth and public company scrutiny.

In his current role as Chief Legal Officer and Head of Corporate Development, McCarthy oversees all legal, compliance, and corporate governance functions, while also shaping QuantumScape’s external partnerships and growth initiatives. He manages regulatory disclosures, intellectual property protection, and contractual negotiations with suppliers, customers, and joint venture partners. Strategically, his mandate extends into corporate development, where he plays a central role in structuring deals with automotive OEMs, scaling partners, and potential future collaborators. Given QuantumScape’s reliance on both proprietary IP and strategic alliances for commercialization, McCarthy’s leadership ensures that the firm’s legal and contractual frameworks enable long-term value capture rather than leaving the company vulnerable to competitors or suppliers.

QuantumScape is a pre-revenue, IP-rich company operating in a highly competitive and geopolitically sensitive industry. Its valuation and long-term defensibility depend heavily on the strength of its intellectual property, the durability of its joint venture agreements, and its ability to protect shareholder interests in negotiations with much larger industrial partners. As head of corporate development, McCarthy also influences how QuantumScape pursues strategic options, whether through joint ventures, licensing, or partnerships, which directly impacts the company’s capital efficiency and eventual market positioning. In essence, his role provides the legal and strategic scaffolding that allows the company’s scientific and operational progress to translate into sustainable shareholder value. For investors, this is not peripheral: it is a crucial element of how QuantumScape turns technical potential into defensible, long-term business economics.

Taken together, QuantumScape’s leadership forms a multi-dimensional team designed for one singular mission: bridging the gap between the lab and the factory floor. The founders provide continuity and technological depth, while later-stage executives bring the discipline of scaling, capital management, and legal structure.

This deliberate mix reflects a recognition that success in batteries is not just about discovery but also about execution under immense industrial and financial pressure. Evaluating the company, confidence in management is inseparable from confidence in the thesis. QuantumScape’s future will ultimately be defined not just by its electrolyte or its anode, but by the ability of its leaders to guide those innovations into mass production and defend the value they create.

With the leadership foundation established, attention turns to the company’s core products and technology, the tangible innovations around which the entire thesis is built.

5. Core Products & Technology Platform

QuantumScape isn’t just building a better battery, it’s engineering an entirely new platform for energy storage that could reset the performance curve of electric mobility.

The core of the QuantumScape thesis rests on its technology platform. Unlike conventional lithium-ion companies competing on cost and scale, QuantumScape’s value lies in ‘re-architecting’ the cell itself, introducing a solid ceramic electrolyte and lithium-metal anode that promise step-change improvements in energy density, charge speed, and safety.

This is not an incremental chemistry tweak; it is a reimagining of the battery’s foundation. For investors, understanding the platform is essential, because it defines both the extraordinary upside, transforming EV economics and adoption, and the binary risks tied to manufacturability and scalability.

Core battery architecture

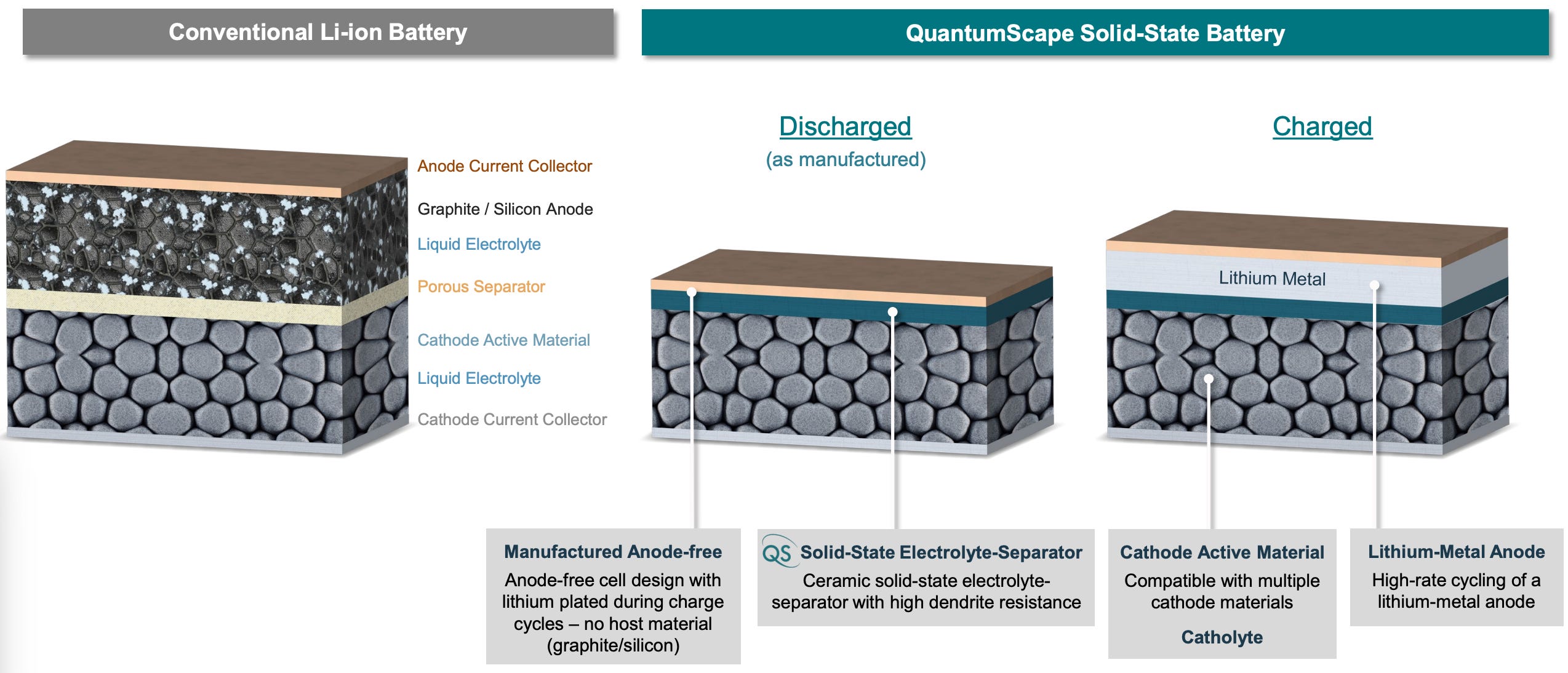

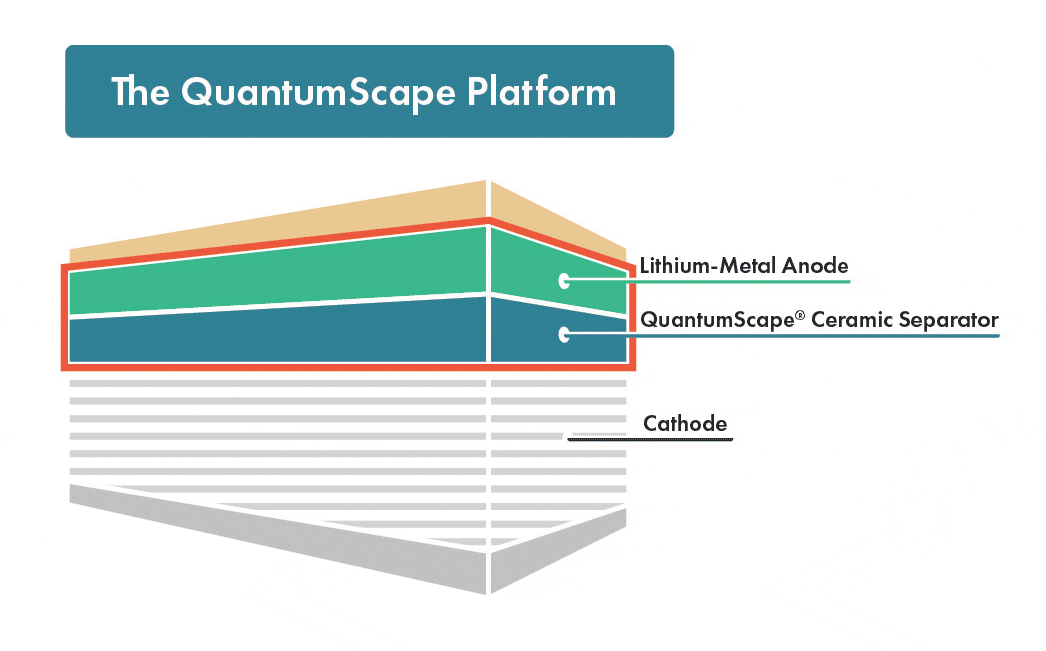

QuantumScape’s core innovation lies in its rethinking of the fundamental architecture of lithium-based batteries. Unlike conventional lithium-ion cells, which rely on a liquid electrolyte and a composite anode made of graphite or silicon, QuantumScape’s design eliminates the need for a host anode material. Instead, the company uses a pure lithium-metal anode that forms in situ during the first charge cycle. This is enabled by a proprietary solid ceramic separator, which performs the dual function of conducting lithium ions while simultaneously acting as a physical barrier against dendrite formation, the long-standing technical hurdle that has prevented lithium-metal batteries from reaching commercialization.

The architecture is built around pouch cells in which multiple layers of cathode, separator, and current collectors are stacked to create a scalable module. The cathode side of the architecture remains compatible with industry-standard materials, including nickel manganese cobalt (NMC) and lithium iron phosphate (LFP), making it adaptable to both premium and cost-sensitive market segments. By enabling the use of a lithium-metal anode, the architecture dramatically increases theoretical energy density, targeting improvements of 50-100% over current lithium-ion designs. This gain comes not from incremental chemistry tweaks but from a reconfiguration of the underlying structure.

From an operational perspective, the absence of a traditional anode simplifies the bill of materials and reduces manufacturing complexity at the cell assembly stage. However, this comes with new challenges in separator manufacturing and layer stacking, areas where QuantumScape has invested heavily in process engineering. The ceramic separator is central to the platform’s differentiation: it must simultaneously exhibit high ionic conductivity, mechanical strength, and manufacturability at scale. Achieving this balance has required years of proprietary materials research, which the company views as its key competitive moat.

Understanding the architecture is critical because it dictates both the upside and the risks embedded in QuantumScape’s thesis. If successful, the solid-state design could enable vehicles with longer ranges, faster charging, and greater safety capabilities that would command premium adoption among OEMs. But the same architectural departure also introduces execution risks: scaling ceramic separators, ensuring defect-free layer stacking, and integrating the cells into automotive packs are all unproven at industrial levels. The architecture, in essence, is both the company’s greatest strength and the focal point of its execution risk profile, making it central to any long-term investment assessment.

Performance characteristics & differentiation

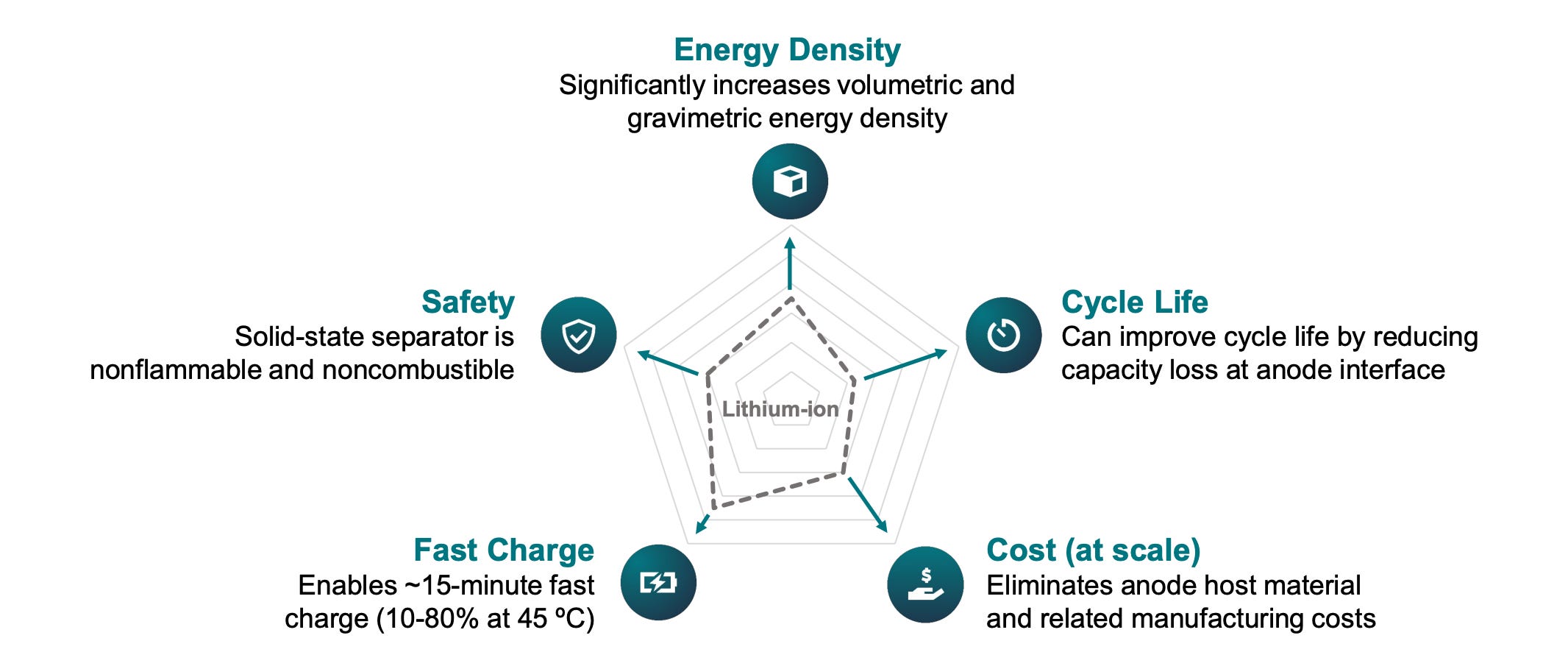

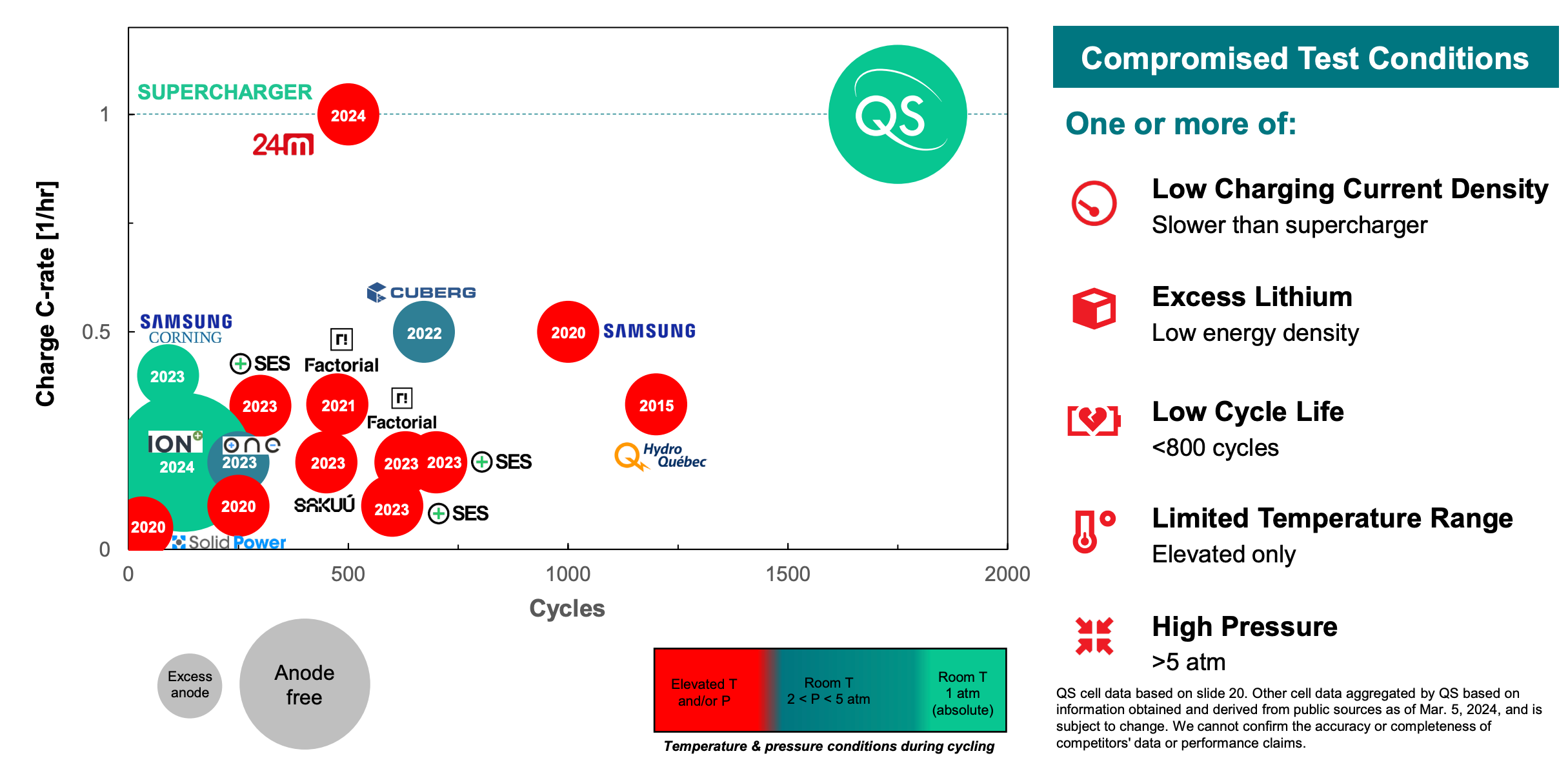

QuantumScape’s investment case is inseparable from the performance profile of its solid-state battery platform. The company positions its technology as a step-function improvement over incumbent lithium-ion cells, particularly across four dimensions that matter most to automotive OEMs: energy density, charge rate, safety, and cycle life. On each of these, the company has demonstrated compelling laboratory results that, if replicated at scale, would represent a decisive competitive advantage.

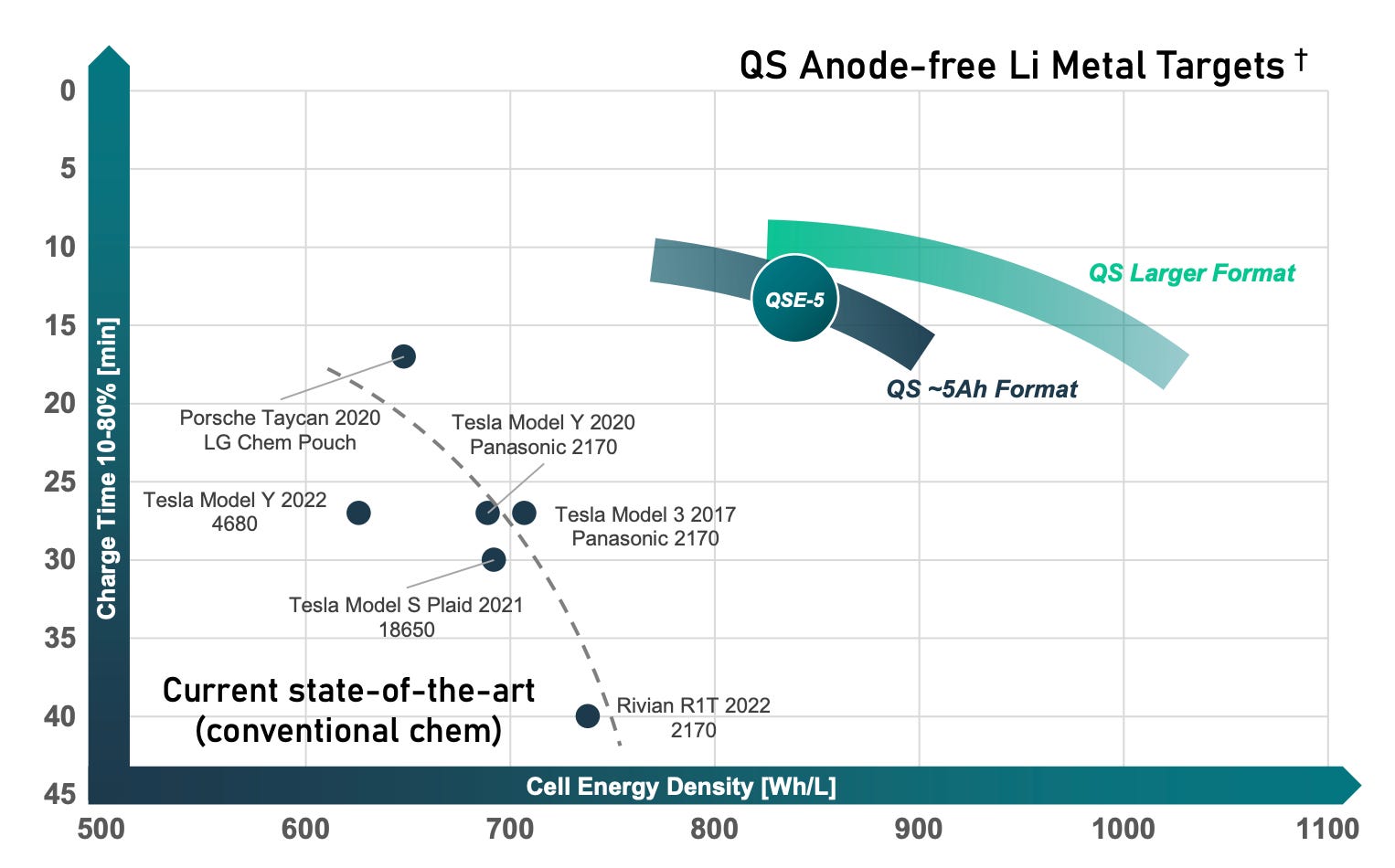

Energy density is the most visible differentiator. By replacing a graphite or silicon anode with lithium-metal, QuantumScape targets energy densities in the 900-1,000 Wh/L range, roughly 50-80% higher than today’s commercial lithium-ion cells. For automakers, this translates into longer driving range without increasing pack size or weight, or alternatively, maintaining current range with smaller, lighter, and cheaper battery packs. In an industry constrained by cost-per-kilowatt-hour and vehicle weight, this kind of efficiency gain is strategically valuable.

Charge rate is a second critical factor. QuantumScape has reported that its cells can charge from 10% to 80% in approximately 15 minutes under laboratory conditions. This compares favorably to conventional fast-charging lithium-ion systems, which typically require 30-45 minutes for the same interval. Faster charge times reduce range anxiety for consumers and accelerate EV adoption, particularly in mass-market segments where charging infrastructure remains uneven. If replicated in the field, this advantage could become a meaningful selling point for OEMs adopting the technology.

Safety is another area of potential differentiation. Conventional lithium-ion batteries carry the inherent risk of thermal runaway due to flammable liquid electrolytes. QuantumScape’s solid ceramic separator is non-flammable and designed to block dendrite penetration, substantially lowering the probability of catastrophic failure. While safety alone does not guarantee adoption, it is an increasingly critical factor for regulators, insurers, and OEM risk managers, particularly as vehicle electrification scales globally.

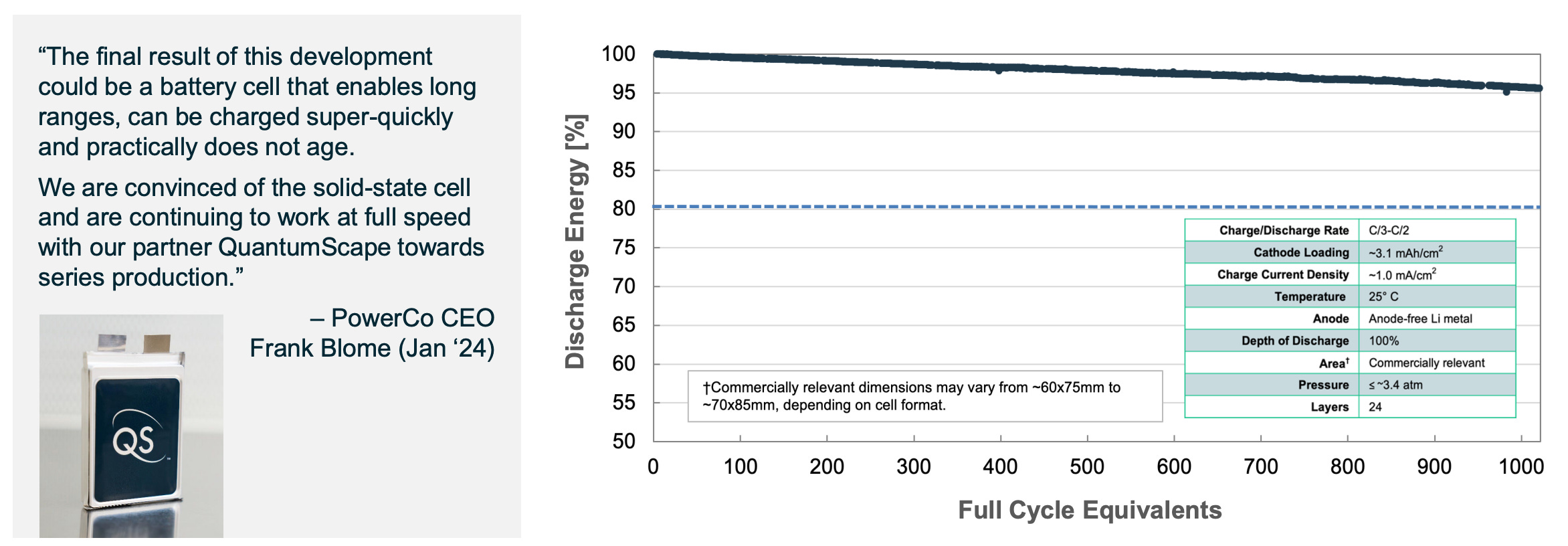

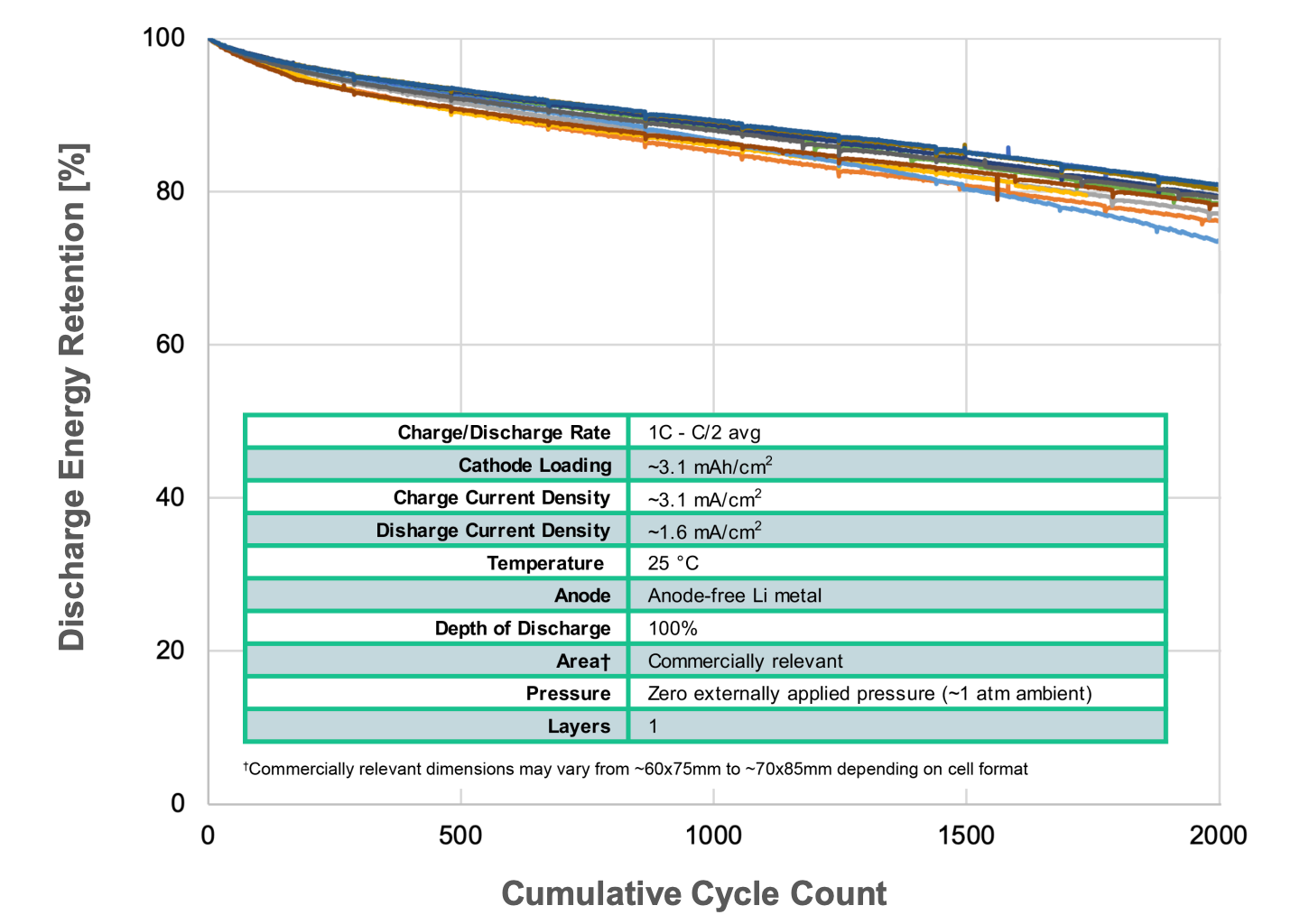

Finally, cycle life performance is a decisive hurdle for next-generation cells. QuantumScape has reported that its single- and multi-layer prototypes retain more than 80% of their capacity after hundreds of charge-discharge cycles, even under demanding test conditions. While this remains below the durability expectations of full automotive qualification (>1,000 cycles), the data trajectory indicates meaningful progress. The ability to maintain high energy density and fast charge rates without sacrificing longevity is central to the platform’s promise.

The performance characteristics form the cornerstone of the thesis. If QuantumScape can deliver on even a portion of these advantages at scale, it will have a differentiated product that justifies premium positioning with OEMs. However, until durability, cost, and manufacturability converge in a commercial-grade cell, the performance profile remains more of a forward-looking asset than a proven differentiator. This duality, clear theoretical superiority but unproven industrial reliability, defines both the upside and the binary risk of the investment.

Intellectual property & proprietary advantages

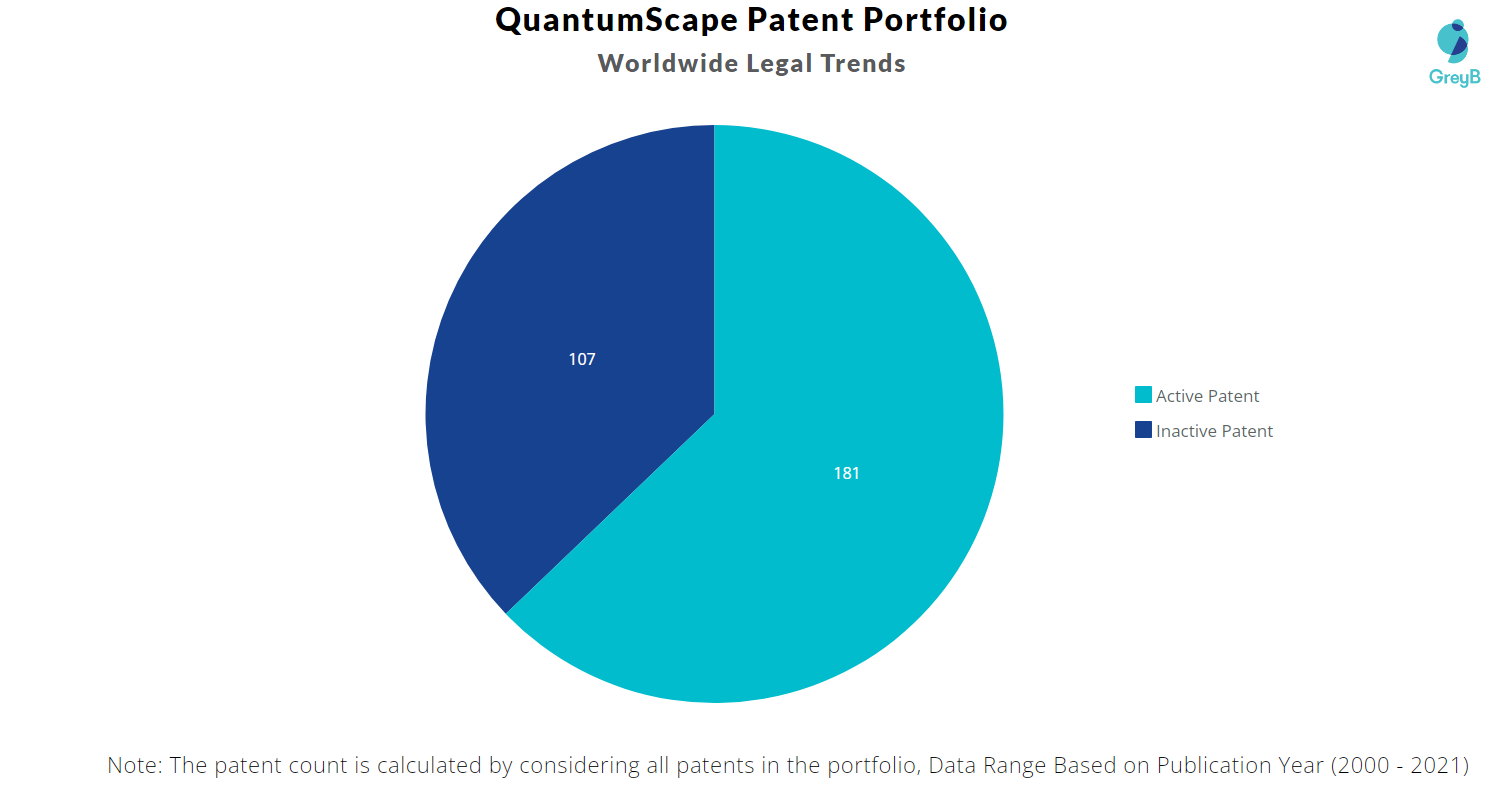

A core component of QuantumScape’s moat lies in its intellectual property portfolio and the proprietary know-how embedded in its platform. As of its latest disclosures, the company holds or has filed more than 200 patents and patent applications spanning materials science, electrochemistry, separator design, and manufacturing processes. These patents are not narrowly concentrated; rather, they cover the entire architecture of the solid-state cell, from the ceramic electrolyte composition to the methods of producing defect-free multilayer structures. For an early-stage energy storage company, such breadth is critical, as it protects against workarounds by competitors and strengthens the firm’s bargaining position in joint ventures or licensing negotiations.

The centerpiece of the company’s IP estate is its solid ceramic separator. This material is the enabling innovation that allows the use of lithium-metal anodes while suppressing dendrite formation. While many solid-state battery startups and academic labs have explored polymer-based or hybrid electrolytes, QuantumScape’s ceramic solution has demonstrated the best balance of ionic conductivity, stability, and mechanical strength in automotive-relevant conditions. Patents around the composition, processing, and integration of this separator provide defensive barriers against direct replication, effectively making the separator the “crown jewel” of the platform.

Beyond patents, QuantumScape’s accumulated process know-how represents an underappreciated proprietary asset. The company has spent more than a decade refining methods for stacking, sintering, and integrating multilayer cells. These techniques are often not fully disclosed in patents, remaining as trade secrets or institutional expertise embedded in the workforce and pilot line processes. For competitors, catching up would require not only replicating the materials science but also solving for the engineering challenges that QuantumScape has iterated on for years. This tacit knowledge creates switching costs for partners and raises the barriers to entry for would-be rivals.

The defensibility of the technology matters as much as the performance itself. The battery industry has historically been characterized by commoditization, with incremental innovations quickly diffused across suppliers. If QuantumScape’s IP portfolio succeeds in securing durable differentiation, it can justify premium pricing and ensure that the value of solid-state batteries accrues to the company rather than being competed away. Moreover, strong IP enhances optionality: QuantumScape could monetize its technology through licensing or joint ventures, not solely through direct manufacturing. This provides flexibility in capital allocation and reduces the risk that the company must bear all the costs of scaling alone.

Ultimately, the intellectual property and proprietary process knowledge serve as a foundation for investor confidence. They are what transform QuantumScape’s story from a promising lab result into a potentially defensible business model. Without this moat, the company’s long-term economics would be far less attractive; with it, the firm is positioned to capture disproportionate value if solid-state technology achieves commercial adoption.

Technology maturity & development progression

QuantumScape’s value proposition rests not only on what its technology can theoretically achieve, but on how far along the company is in proving that those capabilities can be translated into commercial-grade products. Over the past decade, the company has progressed from single-layer proof-of-concept cells to increasingly complex multilayer prototypes, demonstrating incremental advances in both performance and manufacturability. This trajectory matters because it provides a measurable roadmap of de-risking: each technical milestone narrows the gap between laboratory validation and automotive qualification, a journey that is essential for investor confidence.

The company’s development path began with single-layer coin cells that showcased the core properties of the ceramic separator and lithium-metal anode system. These early devices provided proof that the platform could suppress dendrite formation and maintain high coulombic efficiency. Over time, QuantumScape advanced to multilayer pouch cells, eventually producing 10-layer, 24-layer, and most recently 48-layer cells. These devices are closer to the format and complexity required for EV packs, though they remain in prototype stages. Each progression has been accompanied by performance data, such as cycle life retention, charge rate tests, and low-temperature operation, designed to validate that the core advantages persist at higher levels of complexity.

Today, the company is operating a pilot production facility (QS-0) that is intended to support both internal testing and limited customer sampling. The pilot line is not yet scaled to full automotive-grade volumes, but it represents a critical inflection point: QuantumScape is no longer a purely R&D organization but one engaged in early-stage manufacturing. This distinction is material for investors. Many advanced battery concepts fail not in theory but in practice, when laboratory conditions cannot be replicated at industrial scale. By investing in pilot-line engineering, yield management, and equipment qualification, the company is attempting to cross the so-called “valley of death” that separates research from commercialization.

| Seeking Alpha")

From an investor’s perspective, technology maturity is a leading indicator of credibility. While the company is still several years away from revenue, the steady cadence of progression from single-layer to multilayer prototypes and from lab to pilot line provides tangible evidence that execution risk is being managed systematically. That said, the journey remains incomplete: automotive qualification requires thousands of cycles, rigorous safety validation, and consistent manufacturability at scale. Until these are proven, the platform remains pre-commercial, with its valuation supported more by optionality than by cash flow. For long-term investors, the trajectory of maturity is therefore as important as the technology itself, as it dictates the probability that QuantumScape can eventually convert scientific advantage into economic value.

Taken together, QuantumScape’s architecture, performance claims, intellectual property, and staged development path form a technology platform with transformative potential. The innovations are defensible, the laboratory results are promising, and the company has demonstrated a methodical progression toward manufacturability.

Yet the challenges remain immense: scaling ceramic separators, achieving defect-free multilayers, and passing automotive qualification will determine whether the company’s promise becomes a commercial reality. This section underscores the asymmetric profile of QuantumScape, the possibility of unlocking a dominant position in a trillion-dollar EV battery market balanced against the execution risks inherent in industrializing a first-of-its-kind technology.

Understanding the underlying technology is only part of the picture; the real test lies in how these products translate into value across specific markets and customer applications.

6. Product Applications & Value Proposition

QuantumScape’s promise isn’t just about better batteries, it’s about reshaping entire industries, from cars and phones to the very grids that power our world.

QuantumScape’s technology is defined not only by what it is but by where it can go. While the automotive sector remains the company’s first and most critical proving ground, the platform’s flexibility extends to consumer electronics and even long-term stationary storage.

Each of these markets shares the same set of pain points, energy density, charge time, safety, and durability, that solid-state batteries are uniquely positioned to address. Understanding the breadth of these applications highlights why the company’s value proposition stretches beyond a single market, presenting investors with exposure to a potentially transformative energy platform.

Automotive applications

The automotive sector represents the primary and most strategically important application for QuantumScape’s solid-state battery technology. Electric vehicles (EVs) are the company’s first commercial target, and for good reason: the sector is both the largest near-term market for advanced batteries and the one where QuantumScape’s performance advantages translate most directly into customer value. Automakers today face three interrelated challenges that limit EV adoption: range anxiety, charging time, and safety concerns. QuantumScape’s platform is designed to address each of these, making its relevance to the automotive market particularly acute.

The most direct benefit lies in extended range. With energy density potentially 50-80% higher than conventional lithium-ion, QuantumScape’s batteries could allow EVs to travel significantly farther on a single charge without increasing pack size or weight. For OEMs, this creates optionality: extend range at current pack sizes to appeal to premium buyers, or maintain current range while reducing pack size, weight, and cost for mass-market vehicles. Either outcome improves vehicle economics and consumer appeal. Range improvements are not just a marketing advantage; they have a quantifiable impact on adoption rates, as surveys consistently show that limited range remains the top barrier to EV purchases.

Charging speed is a second differentiator. With demonstrated potential to reach 80% state-of-charge in roughly 15 minutes, QuantumScape’s technology approaches the convenience threshold of refueling a gasoline vehicle. For OEMs and charging infrastructure operators, this is strategically valuable, as it allows networks to serve more vehicles per charger and reduces consumer hesitation about long-distance travel. If validated at commercial scale, this advantage could help accelerate adoption in markets where charging infrastructure expansion is lagging.

Safety, while less visible to consumers, is another critical factor for automakers. Lithium-ion batteries remain vulnerable to thermal runaway and fire risk, raising both regulatory and reputational concerns. QuantumScape’s ceramic solid-state separator eliminates flammable liquid electrolytes and is designed to block dendrite penetration, substantially reducing these risks. This enhances not only consumer safety but also lowers potential liability for OEMs. In an industry under increasing scrutiny from regulators and insurers, a safer cell chemistry is a tangible strategic advantage.

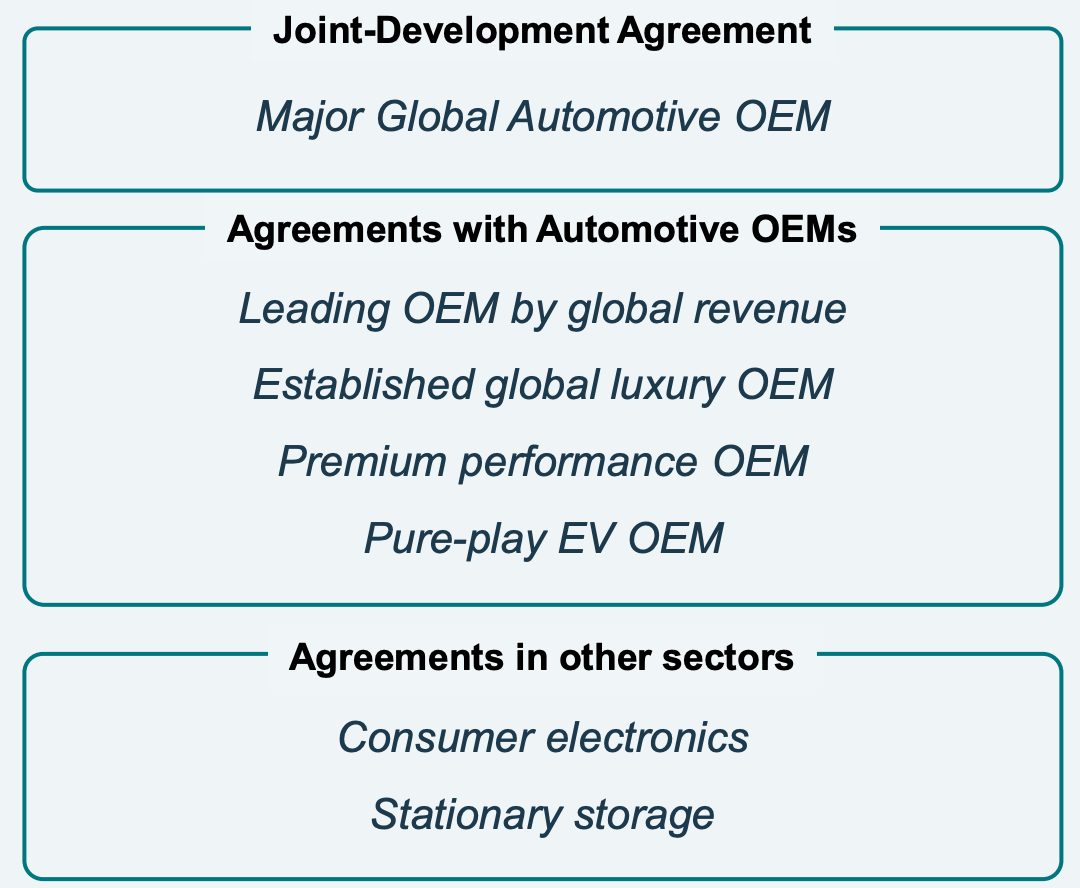

The automotive application is central to the QuantumScape thesis because it defines the scale of the opportunity. EV battery demand is projected to grow into the multi-terawatt-hour range by 2030, representing hundreds of billions in annual revenues. If QuantumScape captures even a modest share of this market through partnerships like Volkswagen’s PowerCo, it could generate significant long-term value. The flip side is that failure to prove automotive readiness would undermine the majority of the investment case, as other applications are smaller or longer-dated. The automotive market, therefore, is not just an application, it is the company’s proving ground and the single largest determinant of its long-term success or failure.

Consumer electronics & mobility

While the automotive sector is QuantumScape’s flagship opportunity, consumer electronics and light mobility represent secondary but strategically significant application areas. Devices such as smartphones, laptops, drones, and e-bikes face many of the same battery-related pain points as EVs, namely, limited runtime, lengthy charging cycles, and safety concerns associated with lithium-ion chemistries. Solid-state technology offers a pathway to extend device usage, reduce charging downtime, and minimize fire risk, all of which are commercially attractive in consumer markets where differentiation often depends on battery performance.

QuantumScape’s architecture is inherently modular, meaning that cells can be adapted to smaller form factors without altering the core chemistry. For consumer electronics, the promise of higher energy density translates into thinner and lighter devices, or devices with longer runtime at the same size. Fast-charging capability is especially relevant in this segment, where convenience is a key driver of purchasing behavior. The solid-state ceramic separator also provides a safety advantage in environments where batteries are used intensively, often under conditions of frequent charging, discharging, and exposure to heat. For manufacturers of laptops or smartphones, this could become a differentiating feature, particularly as consumers grow more aware of battery safety.

From a strategic perspective, consumer applications could serve as an early commercialization pathway for QuantumScape. The performance requirements for electronics, measured in cycle life, energy density, and power output, are generally less demanding than those for automotive systems. This makes consumer electronics a potentially attractive “stepping stone” market, allowing QuantumScape to validate its technology in commercial products ahead of full automotive qualification. Revenue generation from licensing or small-scale production in consumer devices could provide incremental cash flow, reduce reliance on equity raises, and demonstrate progress to investors and partners.

For long-term investors, the consumer electronics segment is not the core driver of valuation but a meaningful optionality play. While the addressable market for batteries in phones and laptops is large, it is still materially smaller than the automotive sector. However, the ability to generate earlier, lower-risk revenue streams could de-risk the timeline to commercialization and demonstrate the versatility of the platform. If QuantumScape can establish a beachhead in consumer applications while advancing toward EV readiness, it would enhance its credibility, provide validation of manufacturing scalability, and extend its cash runway. In this sense, consumer electronics are less about displacing incumbents at scale and more about proving out the technology in a commercial context, making them strategically important to the investment case even if not central to the ultimate market opportunity.

Stationary storage & grid applications

Beyond transportation and consumer electronics, stationary energy storage represents a long-term but potentially transformative application for QuantumScape’s solid-state platform. As renewable penetration increases worldwide, grid operators face a growing challenge: intermittency. Solar and wind generation often peak at times misaligned with demand, creating the need for scalable, safe, and durable energy storage solutions. Today, lithium-ion dominates grid storage, but it has clear drawbacks, thermal runaway risk, limited cycle life, and declining economics as cells degrade under heavy cycling. Solid-state batteries could address these pain points, positioning QuantumScape for eventual relevance in this multi-billion-dollar segment.

The characteristics that make QuantumScape’s technology attractive for EVs, high energy density, fast charge/discharge rates, and enhanced safety, also align with grid requirements, albeit with different emphases. In stationary storage, cycle life and safety are paramount. Utility operators demand batteries capable of enduring thousands of deep charge-discharge cycles with minimal degradation. If QuantumScape’s ceramic separator enables longer durability and lower degradation rates than conventional lithium-ion, it could create a strong value proposition in grid applications. Safety is equally critical: large-scale installations in urban or industrial areas face heightened scrutiny from regulators and insurers, and the elimination of flammable liquid electrolytes could lower both risk and insurance costs.

From a commercial strategy perspective, the grid storage market is attractive but secondary to automotive. Margins are thinner, customers are more cost-sensitive, and the supply chain is heavily commoditized. However, the market’s sheer scale and policy tailwinds, particularly in regions like the U.S., EU, and China where renewables build-out is accelerating, make it a potential growth avenue. QuantumScape is unlikely to target this segment in its early commercialization phase, but partnerships with utilities or energy storage integrators could become a realistic option once the platform matures. The modularity of the solid-state architecture provides flexibility for scaling cells into larger packs for stationary applications without requiring fundamental redesigns.

Stationary storage should be viewed as long-dated optionality rather than a near-term driver. The automotive sector will dictate valuation for the next five years, but the grid market extends the total addressable market and underscores the durability of the technology’s relevance beyond vehicles. If QuantumScape achieves success in EVs, expansion into stationary storage could multiply the commercial upside, turning the company from an auto-supplier into a broader energy storage platform. Conversely, if EV commercialization proves slower than expected, stationary storage could provide a secondary monetization path. This optionality, while not priced into the stock today, is an important consideration for investors evaluating QuantumScape’s long-term role in the energy transition.

Overall value proposition to stakeholders

QuantumScape’s value proposition extends beyond performance specifications; it lies in how the company’s technology creates differentiated benefits for stakeholders across the EV value chain. For automakers, the case is centered on product differentiation and compliance. Higher energy density translates into longer range and lighter packs, enabling OEMs to market superior vehicles while potentially lowering production costs.

Faster charging enhances consumer adoption, while improved safety reduces liability exposure. These attributes allow automakers to accelerate electrification roadmaps without waiting for incremental lithium-ion improvements. Importantly, the technology is compatible with existing cathode chemistries, which lowers the switching costs and facilitates integration into OEM supply chains.

For consumers, the value proposition is straightforward: an EV with greater range, faster charging, and lower safety risks represents a better product. Range anxiety has consistently ranked as the top barrier to EV adoption, while long charging times rank second. A battery that narrows these gaps between EVs and internal combustion vehicles has the potential to accelerate mainstream acceptance.

Safety, while less visible, is equally important. Consumers have become more aware of battery fires in both vehicles and consumer devices; a chemistry that mitigates these risks strengthens trust in electrification. Taken together, QuantumScape’s technology could meaningfully shift consumer preferences, particularly in markets where infrastructure is still catching up.

From a regulatory and policy perspective, the technology offers alignment with decarbonization goals. Governments worldwide are tightening fuel economy and emissions standards, while simultaneously incentivizing EV adoption. A battery platform that improves range and charging convenience helps OEMs meet these mandates while enabling policymakers to accelerate their electrification targets. QuantumScape’s technology could therefore benefit indirectly from regulatory momentum, even if it does not participate directly in subsidy programs.

The value proposition lies in both economic upside and defensibility. Solid-state technology, if proven, represents a generational shift that could reset the competitive landscape in batteries. QuantumScape’s patent portfolio, manufacturing know-how, and OEM partnerships provide barriers to entry that could allow it to capture a disproportionate share of the value created. The staged commercialization model, centered on joint ventures rather than standalone gigafactories, also provides a more capital-efficient pathway to scale.

Taken together, QuantumScape’s applications form a layered value proposition. Automotive markets provide the scale and urgency, consumer devices offer earlier revenue opportunities and validation, and grid storage represents longer-term optionality. Across all three, the benefits converge: higher energy density, faster charging, improved safety, and defensible integration with existing supply chains.

For stakeholders, whether automakers, consumers, or policymakers, the company’s technology addresses the central barriers to electrification. This breadth reinforces the asymmetric potential: success in EVs alone could be transformational, but the platform’s versatility creates additional pathways to scale and relevance over time.

But demonstrating value in principle is not enough,investors must also weigh whether QuantumScape can manufacture these products at scale and deliver them reliably to customers.

7. Operational Readiness & Manufacturing Scale-Up

The real test of QuantumScape isn’t science, it’s scale, and the company is now stepping onto the factory floor where theories meet reality.

If QuantumScape’s past was defined by discovery, its future will be determined by execution. The transition from lab-based prototypes to scalable manufacturing is the single most important, and riskiest, phase in the company’s evolution. The QS-0 pilot line, process development breakthroughs, and its joint venture with Volkswagen represent more than operational updates; they are the crucibles where industrial credibility is forged. Operational readiness is not a side story, it is the lens through which the entire value proposition must now be judged.

Pilot line infrastructure (QS-0 facility)

QuantumScape’s pilot line, referred to as QS-0, represents a critical inflection point in the company’s journey from a research-driven enterprise to a pre-commercial manufacturer. Located in San Jose, California, the facility is designed not as a revenue-generating plant but as a bridge between laboratory-scale prototypes and eventual high-volume production. Its primary function is to produce multilayer solid-state pouch cells in quantities sufficient for internal testing, external validation, and customer sampling. QS-0 is quite important, as it marks the transition out of pure R&D mode and into a phase where manufacturability, repeatability, and scale become measurable.

The facility houses the specialized equipment needed to fabricate QuantumScape’s proprietary ceramic separators and assemble them into multilayer cell stacks. Unlike conventional lithium-ion manufacturing, which leverages decades of process refinement, solid-state production requires new methods of handling, sintering, and stacking fragile ceramic components. QS-0 therefore serves as both a learning environment and a proof point: it allows the company to iterate rapidly on process flows while generating real-world data on yields, throughput, and defect rates. This is where QuantumScape begins to demonstrate whether its core technology can withstand the rigors of industrialization.

QS-0 also plays a key role in supporting the company’s relationships with OEM partners, particularly Volkswagen’s PowerCo. By delivering early cell samples produced on pilot-line equipment, QuantumScape provides customers with visibility into the technology’s progress and performance under conditions that are closer to production reality than lab-scale coin cells. These early samples are essential for securing customer confidence, guiding joint development work, and aligning roadmaps. In capital markets, such customer-facing milestones often serve as catalysts that reinforce credibility or, conversely, expose gaps in execution.

The QS-0 facility is less about output volume and more about risk reduction. The success or failure of this pilot line will reveal whether QuantumScape can control variability, maintain separator quality, and scale multilayer stacks without significant performance loss. Each incremental improvement in throughput or defect reduction increases the probability of successful scaling into joint venture facilities. Conversely, persistent bottlenecks or high scrap rates could signal that the company remains years away from manufacturability, undermining the commercialization timeline.

In short, QS-0 represents the linchpin between science and industry. It is the tangible platform through which QuantumScape can prove to OEM partners, regulators, and investors that its technology is not just theoretically superior but industrially viable. For long-term investors, the performance of QS-0 will likely serve as one of the clearest indicators of whether the company’s roadmap is credible and whether the eventual scale-up to automotive production is achievable.

Manufacturing process development

If the QS-0 pilot line represents the physical infrastructure for QuantumScape’s scale-up, the underlying manufacturing process development is the intellectual backbone that determines whether the company can ultimately succeed in commercialization. The central challenge is not only making a single solid-state cell work in the lab, but replicating that performance at scale with consistent quality and acceptable cost. This requires engineering solutions to problems that do not exist in conventional lithium-ion production, particularly around the handling and integration of QuantumScape’s ceramic separator.

Unlike polymer-based electrolytes, the ceramic separator must be produced with extreme precision to achieve the ionic conductivity and mechanical strength required for high-performance cells. Even microscopic defects can compromise performance or lead to premature failure, creating yield challenges that are magnified as the company transitions from single-layer cells to 24- and 48-layer stacks.

Process innovations in sintering, coating, and separator fabrication are therefore essential to achieve manufacturability. Similarly, the stacking and lamination of multiple layers must be performed with tight tolerances to avoid misalignments, air gaps, or micro-cracks that can degrade performance. These are engineering hurdles that no existing lithium-ion supply chain is currently optimized to solve.

QuantumScape has invested heavily in developing proprietary techniques for addressing these challenges. The company has reported progress in improving separator throughput and reproducibility, as well as advances in multilayer assembly. Automation, quality control systems, and yield management strategies are increasingly emphasized, reflecting the company’s recognition that commercialization is less a matter of pure chemistry and more a matter of industrial engineering. Investors should note that this mirrors the historical trajectory of lithium-ion itself: scientific breakthroughs often occur years before viable production processes catch up.

The critical implication is that process readiness is as central to the investment case as the core chemistry itself. Even if the separator delivers superior performance, the company must demonstrate that it can be produced in high volumes without prohibitive costs or yields that erode margins. This is why each quarterly update on separator throughput, defect rates, and multilayer reproducibility is closely scrutinized by institutional investors. Progress here reduces execution risk; stagnation increases the likelihood of delays, cost overruns, and dilution.

Process development is the lever that determines whether QuantumScape’s technology remains a scientific curiosity or matures into a scalable business. The competitive advantage of higher energy density will mean little if the company cannot translate lab-scale innovation into industrial consistency. In this sense, manufacturing process development is not an adjunct to the thesis, it is the core determinant of whether the company can eventually justify its valuation.

Joint venture and scaling strategy

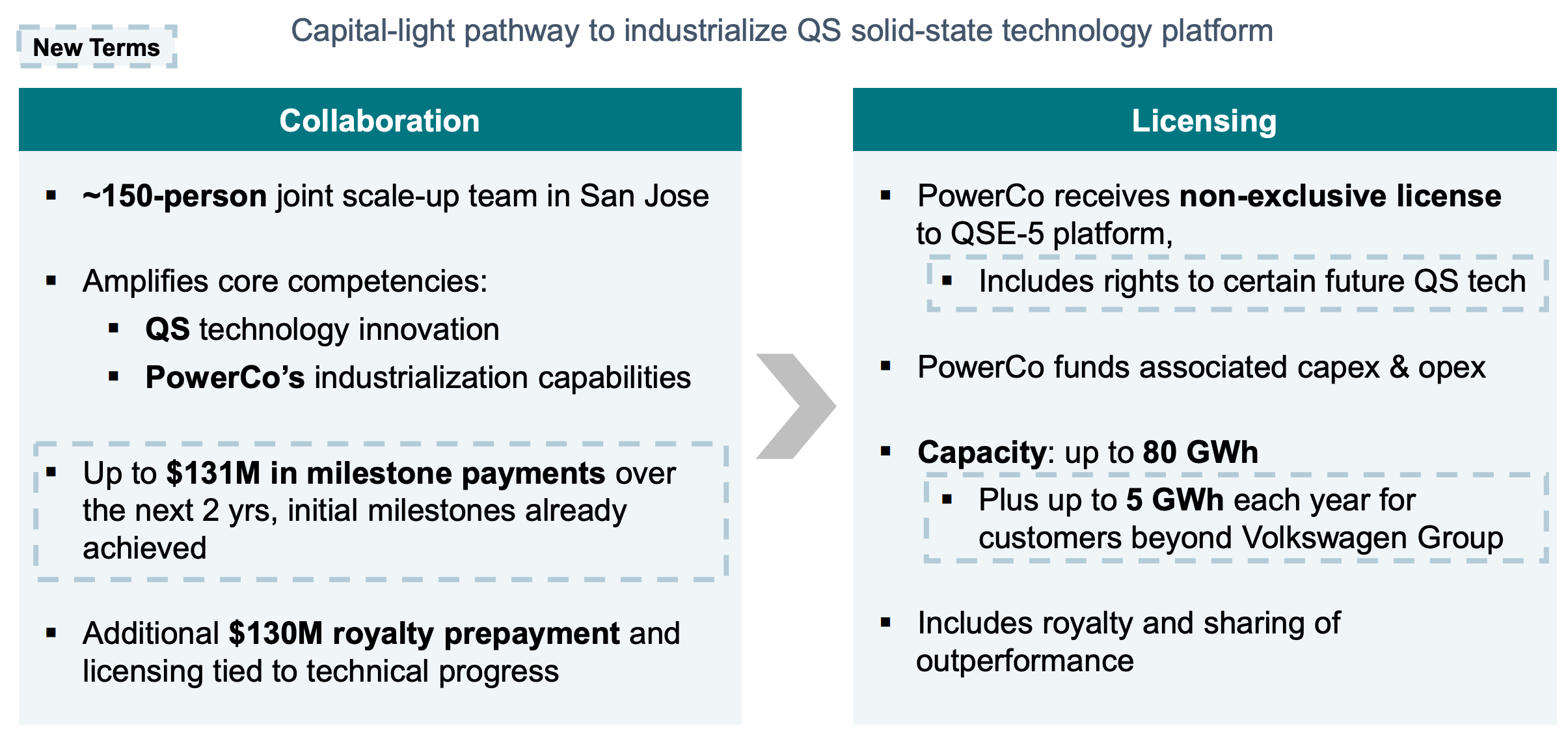

QuantumScape’s scaling strategy is built around partnerships, most notably its long-standing relationship with Volkswagen, which through its battery subsidiary PowerCo, has committed significant capital and resources to the joint venture. This approach reflects a deliberate decision to avoid the capital intensity of building standalone gigafactories, a path that has burdened other battery startups with heavy fixed costs and high cash burn. Instead, QuantumScape aims to leverage OEM partners’ manufacturing expertise, distribution channels, and capital bases to accelerate its commercialization timeline while maintaining a leaner balance sheet.

The Volkswagen joint venture is structured to eventually scale to multi-gigawatt-hour production capacity, with the first commercial facility (often referred to as QS-1) expected to be co-developed once pilot-line validation is achieved. Volkswagen has already invested over $300 million into QuantumScape, a signal of its strategic commitment. This alignment is important because it creates a ready-made customer and manufacturing partner, reducing go-to-market risk. At the same time, the JV structure helps to allocate capital expenditures more efficiently: QuantumScape contributes the core technology, while Volkswagen brings the scale, supply chain access, and integration expertise needed to industrialize production.

Beyond Volkswagen, QuantumScape has signaled openness to additional partnerships with other automakers and potentially non-automotive customers. The company’s business model envisions joint ventures or licensing structures as the primary commercialization pathway, rather than vertically integrating into a full-stack cell manufacturer. This is strategically significant because it suggests a capital-light approach relative to peers like Solid Power or ambitious vertical integrators such as CATL. If successful, the strategy could allow QuantumScape to scale faster and with less dilution, a key factor for investors monitoring cash burn.